thitivong

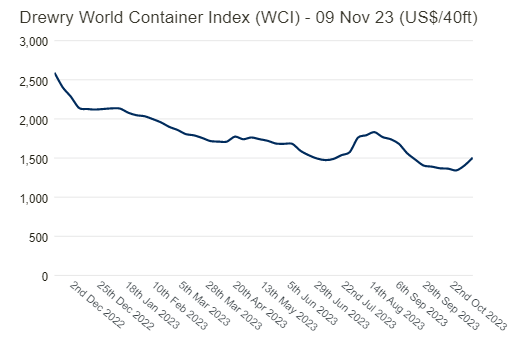

Global shipping rates continue to sag, but is the trend about to turn? I noticed that the benchmark Drewry World Container Index (WCI) has bounced modestly in recent weeks. That is a potentially bullish harbinger of profitability for shipping companies. Still, the Utilities sector, renewables, in particular, has been beaten up amid rising interest rates. Weakness in China is another soft spot. Finally, geopolitical turmoil in Israel is a third factor to weigh for one international diversified player.

I am downgrading Kenon Holdings (NYSE:KEN) from a buy to a hold. I outlined a bearish fundamental situation for the firm earlier this year but was sanguine on a short-term trading play. That did not pan out, and I would rather stand on the sidelines ahead of its next earnings report.

Global Shipping Index Stabilizing Somewhat

Drewry

According to Seeking Alpha, Kenon Holdings Ltd., through its subsidiaries, operates as an owner, developer, and operator of power generation facilities in Israel, the United States, and internationally. It operates through OPC Power Plants, CPV Group, and ZIM segments. The company engages in the generation and supply of electricity and energy; development, construction, and management of solar and wind energy, and conventional natural gas-fired power plants; and provision of container liner shipping services. It also operates a fleet of 150 vessels.

The Singapore-based $1.1 billion market cap Independent Power and Renewable Electricity Producers industry company within the Utilities sector does not have positive trailing 12-month GAAP earnings and it has paid $2.79 of dividends this year after a large $13.75 total per-share payout in 2022. Given less favorable industry developments this year, I would not expect a very high distribution total to be announced early next year. Moreover, we have not yet heard about any year-end payouts (we had seen that in 2018, 2019, and 2020).

Back in August, the company posted Q2 2023 results. OPC reported a net loss of $11 million, with adjusted EBITDA of $47 million, as compared to a net loss of $10 million and adjusted EBITDA of $26 million in Q2 2022. That included a net loss of $4 million for CPV versus a loss of the same amount a year earlier. ZIM, meanwhile, reported a net loss of $213 million, with adjusted EBITDA of $275 million. ZIM earned a net profit of $1.3 billion in Q2 2022 with adjusted EBITDA of $2.1 billion.

The management team noted that Kenon had returned approximately $24 million of capital to shareholders through stock buybacks, which represented approximately 1.8% of its total outstanding shares since the start of the $50 million share repurchase plan announced this past March. Be on the lookout for future buyback plans in its Q3 results due out later this month. Kenon’s stand-alone cash was $632 million as of June 30, 2023, so there is some liquidity cushion to help weather these tougher times. Lastly, OPC Eshkol’s involvement in a tender for the sale of the Eshkol power plant could help the liquidity picture as well.

On valuation, it’s difficult to gauge how future earnings will progress, but given the heightened tensions in the Middle East, higher borrowing costs, uncertainty in China, and a soft global shipping landscape, the profitability outlook appears murky. Moreover, lower dividend payments in the coming quarters appear likely given such headwinds. Finally, negative free cash flow in the last four quarters suggests the valuation of the stock could be significantly below where the stock trades today if these trends persist. Still, upside potential could stem from a rebound in the renewable energy industry and if operations at ZIM improve.

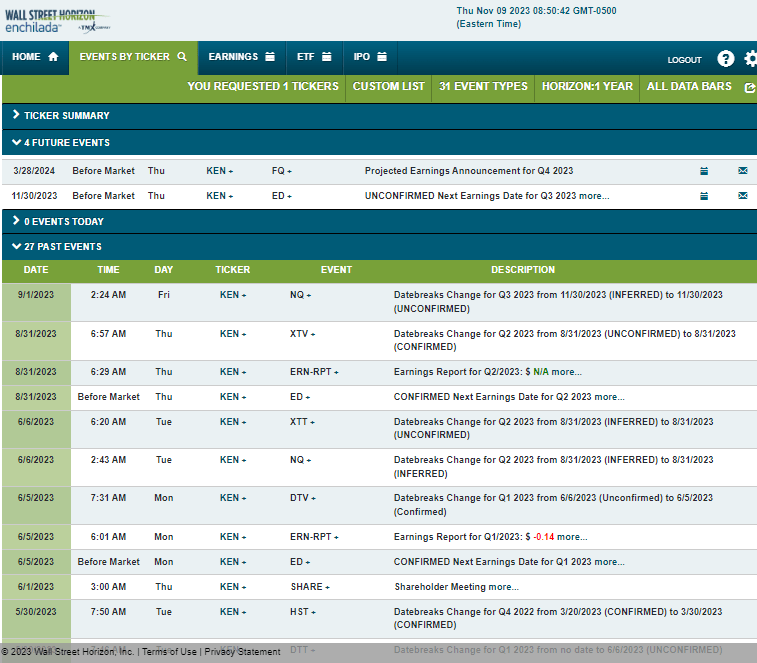

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q3 2023 earnings date of Thursday, November 30 before the open. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

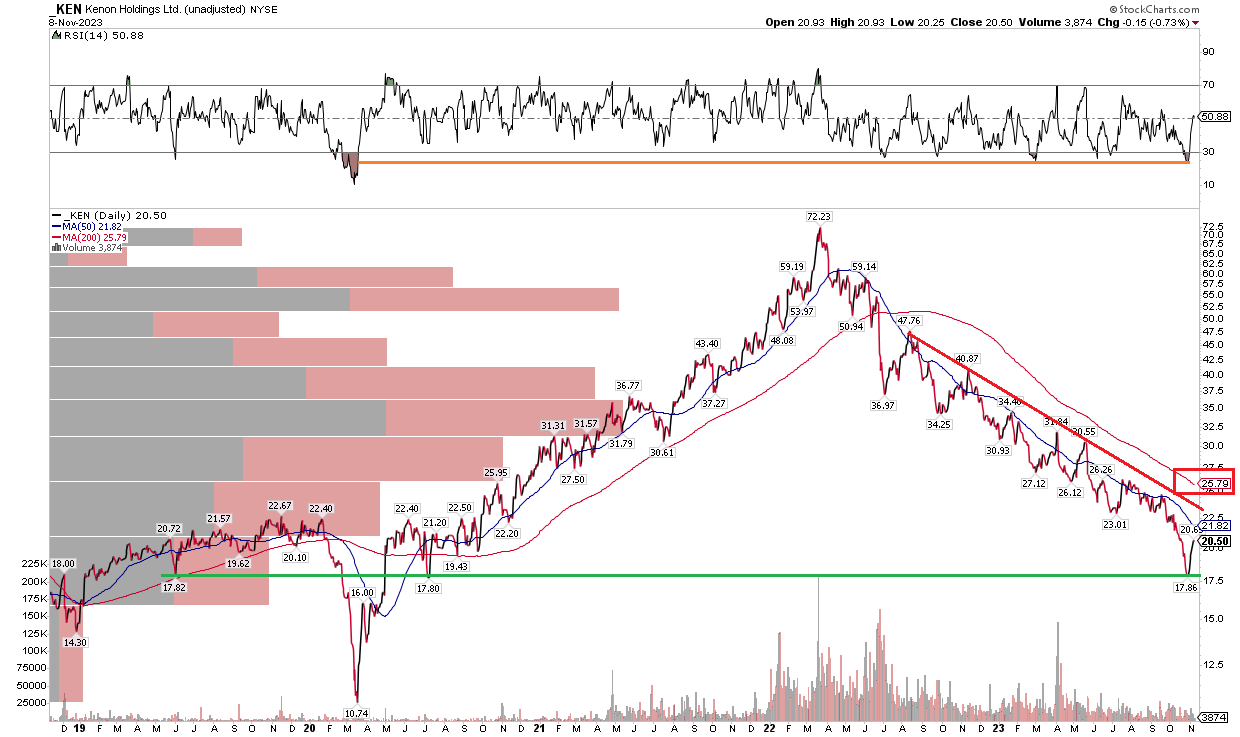

With a continued bearish outlook, I assert that the chart is just modestly more appealing. Notice in the graph below that KEN found some buyers in the high $17s – that was the low from July 2020. Still, the long-term 200-day moving average is very much negatively sloped, indicating that the bears are in charge. $23 could be resistance on a bounce attempt – the low from this past June. Still, it is important to remember that KEN has historically been a big dividend payer, so on a total return basis, the drawdown off the March 2023 high is about 63% – not as severe as the price-only chart below illustrates. Also possibly encouraging from a bullish perspective is the reality that KEN shares’ RSI notched the most oversold reading since early 2020 – so a further bounce to $23 is feasible.

Overall, however, the chart and its trend are generally bearish, and those who are long should consider placing a stop loss under $17.

KEN: Bearish Downtrend, Holding Key Support Under $18

StockCharts.com

The Bottom Line

I am downgrading KEN from a tactical buy to just a hold. With possible support in play and after a severe drawdown, a lot of pessimism has been baked in, but the company needs many macro factors to reverse for the future earnings picture to improve.

Q2 2024 Earnings Call Transcript")