Maksim Safaniuk/iStock Editorial via Getty Images

Introduction

Mapfre (OTCPK:MPFRF) (OTCPK:MPFRY) is a Spanish insurance company generating the majority of its net income from its LatAm division which also is a strong driver for growth. Additionally, the company continues to invest in its reinsurance division and noticed some strong results in the first nine months of the year. This indicates the company is on track to generate EPS of 0.23-0.24 EUR (on a normalized basis, and thus adjusted for a goodwill impairment charge recorded during the first nine months of the year) and I expect the dividend of 15 cents per share to remain stable.

Yahoo Finance

Mapfre’s primary listing is in Madrid where the stock is trading with MAP as its ticker symbol. The average daily volume in Spain is 1.9M shares for a total value of roughly 4M EUR. I will use the Euro as base currency throughout this article considering the company trades in Euro and reports its financial results in Euro. The company has 3.08B shares outstanding, resulting in a market capitalization of roughly 5.9B EUR given the share price most recently closed at 1.93 EUR per share.

A closer look at the Q3 results

Mapfre recently reported its Q3 results and I was really looking forward to three elements. First of all, I obviously wanted to see the insurer’s earnings profile to see how it navigates through these volatile times. Secondly, I also was keen on seeing how the Spanish company performed in South America, as that division is the largest contributor to its consolidated net profit. And finally, as Mapfre has been spending more time, money and effort on building out its reinsurance division, I also wanted to see if those investments are paying off.

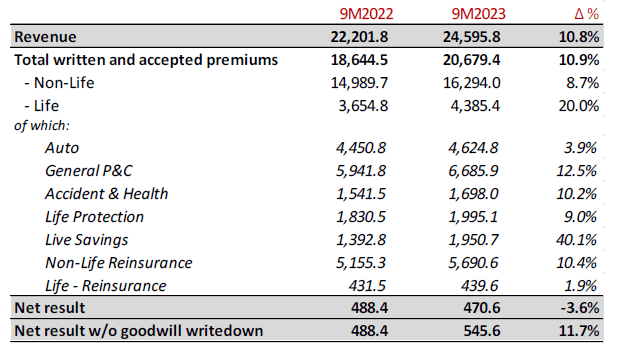

Let’s start with the first element. The company reported a total revenue increase of almost 11% to 24.6B EUR thanks to a strong 20% increase in the life division although we obviously should not ignore the 8.7% revenue growth in the non-life division either.

Mapfre Investor Relations

As you can see in the image above, total net income was approximately 471M EUR on a reported basis, which represented a decrease of 3.6% compared to the 488M EUR in net profit it reported over the first nine months of 2022. However, this year’s 9M results included an impairment charge of approximately 75M EUR on the value of the goodwill in the United States. While this is a non-cash charge, it obviously does weigh on the company’s financial results and that explains why net income decreased. Excluding the impairment charge, Mapfre would have posted an 11.7% net profit increase which is very robust as that indicates its net income increased at a faster pace than its revenue.

Also keep in mind the 9M 2023 results include a hit of about 105M EUR related to the earthquake in Turkey earlier this year. This impact was felt in the Reinsurance division (which I will discuss later in this article) and as this had pretty much the same impact as the 106M EUR hit due to the drought in Brazil a year earlier, the net impact on the financial results caused by Natural Catastrophes remained pretty stable. That’s important to know as it means the net income was not unreasonably high due to the lack of Nat Cat events, and despite recording a 105M EUR net impact, Mapfre’s net profit remained very robust.

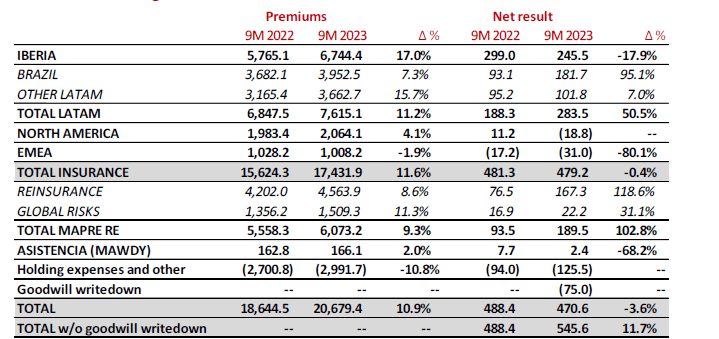

Secondly, I wanted to check if the company’s LatAm division still is an important driver of results. That indeed is the case, and although you might be surprised to see the contribution of the LatAm division to the net result increased by 50%, keep in mind the 9M 2022 results were negatively impacted by the drought in Brazil.

Mapfre Investor Relations

So yes, although the comparable basis is a little bit skewed and the LatAm contribution appears to be more impressive than expected, I’m satisfied with the performance in LatAm.

And finally, Mapfre continues to grow its reinsurance segment. The total amount of premiums at Mapfre RE increased by in excess of 9% to 6.1B EUR and the insurer’s pricing mechanism boosted the combined ratio, which improved to 95%. As mentioned before, the earthquake in Turkey had a net impact of around 100M EUR on the net result and it looks like that may be the only noticeable weather event. While Europe had to deal with storms, the slow hurricane season has offset the higher losses in the European division. This boosted net income for the reinsurance division to 190M EUR which is more than twice the reported net income in the first nine months of 2022.

Taking all these elements into consideration, I now expect the underlying EPS to come in at 23-24 eurocents per share and I don’t expect Mapfre to make any changes to its dividend of 15 cents per share. This means the company’s current dividend yield is approximately 7.8%, subject to the standard 19% dividend withholding tax in Spain.

Investment thesis

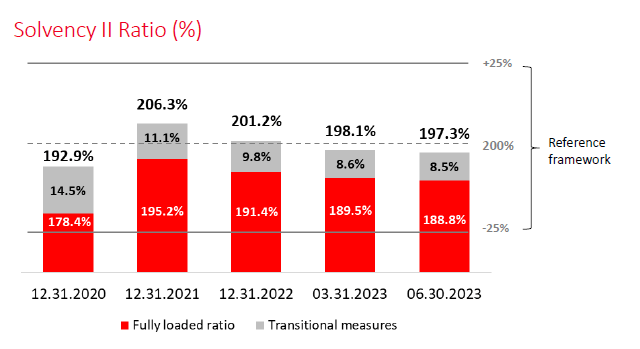

Mapfre’s financial performance in the first nine months of the year met all my expectations. Although the reported net income was lower than I had anticipated, this was caused by an impairment charge on the value of the goodwill in its US division. But with a total ROE of 9.1% and a solvency II ratio of 197% (which is substantially higher than the required minimum of 100%), Mapfre appears to be in a very good shape.

Mapfre Investor Relations

Despite already very decent results, Mapfre mentioned on its conference call it’s still reversing premium short falls and the management indicated it needs a few more months to complete all planned tariff adjustments (with a specific focus on the Brazilian and Spanish markets although the Brazilian division is already outperforming thanks to a surprisingly low combined ratio). Further improvements should increase the net income and will help Mapfre to mitigate the impact of unrealized losses in its investment portfolio. That being said, the stock’s current 20% discount to its book value offers an attractive entry price.

I currently have no position in Mapfre as I elected to add to my other insurance positions in Europe.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")