wdstock

Shares of Vornado Realty Trust (NYSE:VNO) have significantly underperformed the market over the past year, even as they have recovered substantially from their lows. Still, shares are down 15% since I recommended selling last year, and as feared, the company had to postpone its quarterly dividend earlier this year. On Monday, Vornado reported Q3 earnings, making this an opportune time to reevaluate the stock.

Seeking Alpha

In the company’s third quarter, Vornado earned adjusted funds from operations (FFO) of $0.66, down from $0.81 last year. This was $0.01 ahead of estimates. Of the $30 million drop in FFO to $127 million, higher net interest expense drove $7 million of the decline. Rising interest expense has been a concern of mine because the company has $2.2 billion of floating rate debt. I am not a fan of REITs carrying floating rate debt because real estate valuations are already tied to rates. This means when rates rise, their properties tend to have lower valuations; to simultaneously having interest expense rise compounds this problem.

Having floating rate debt in its capital structure aided VNO in the 2010s when rates were frequently near zero, but it has turned into a headwind now. The company does strategically uses swaps to transform floating rate debt into fixed rate obligations, though these swaps do not last forever. For instance, a $840 million loan swapped at 2.29% will rise to 6.03% in May 2024. That alone will be a $30 million hit to cash flow over the ensuing year or about $0.15/share. This is why I expect FFO to remain under pressure.

Beyond rates, its core business remains challenged. New York occupancy was 89.9% with office of 91.6% and retail of 74.5%. Same-store net operating income was down 3%. While New York was up 4%, the MART in Chicago was down 54% as occupancy is just 76.8%. New York now accounts for 87% of net operating income.

Leasing activity is also modest. Last quarter, two of its three leases saw cash rents fall with a weighted average decline of 0.8%. Just over 330,00 square feet were leased. As such, occupancy is drifting lower. Occupancy fell by 20bp sequentially in NY and by 40bp from last year. The MART has struggled to replace tenants as leases expire—with another 10% of leases due in 2024, it is hard to see a material improvement in leasing.

Vornado Realty Trust

Given how many people are still working remotely or in a hybrid environment, the fact NY is still running 90% may be surprising. This is where it is important to remember that office leases tend to run for multiple years. In the first three quarters of the year, 6.5% of its leases came due, so that 50bp drop means a net 8% chose not to renew while those who renew are paying slightly less in rent. Again, this is not catastrophic, but it points to an ongoing bleed in the business’s cash flow.

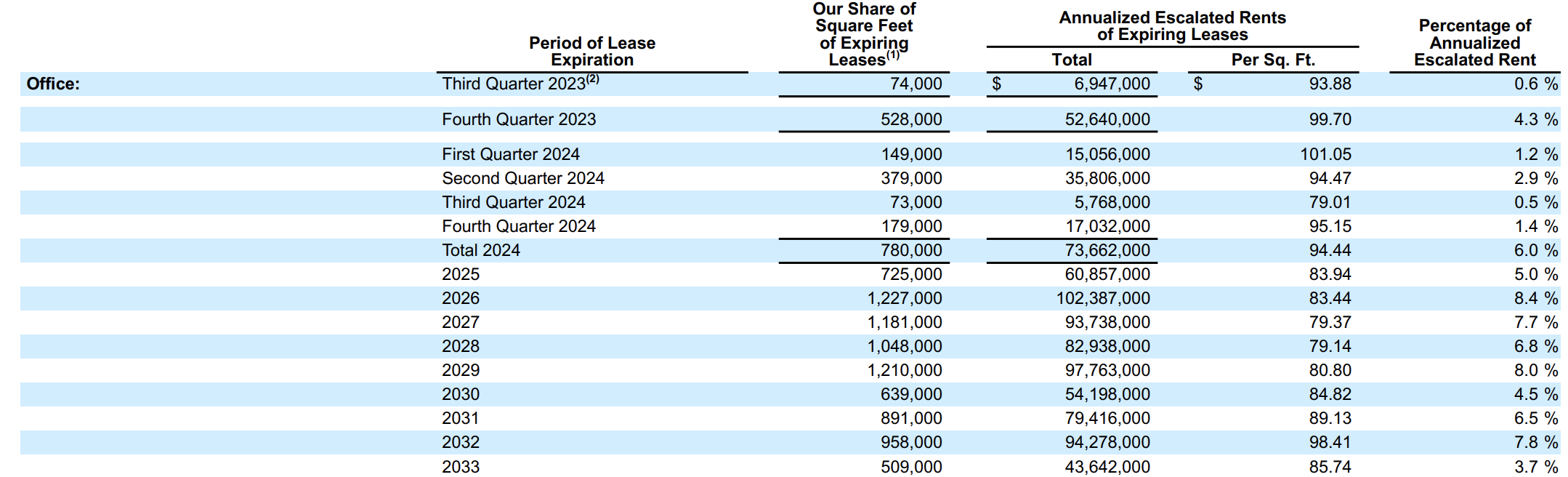

I have viewed office landlords as facing more of a “slow-moving train wreck” than a sudden crash because of how staggered their lease maturities are. It will take several years for occupancy to hit its new normal. This buys time for REITs to reshuffle assets, pay debt, or diversify, but it means many may see ongoing declines for some time (which is where I fear VNO is). As you can see below, VNO has meaningful Q4 lease expiries, and then mid-to-high single digits for several years. As such I expect to see ongoing incremental occupancy declines at least through 2025.

Vornado Realty Trust

Now, much remains uncertain about the future of work. We could see remote accelerate or reverse. One of the bigger uncertainties is what does hybrid work means for office space. In a 3/2 system, you likely still need more than 60% of your former layout, but you may not need the entire 100%. Exactly where this lands will be difficult to tell. Still, over time, a 5% decline in occupancy would reduce quarterly FFO by about $0.08-$0.10. This is before any headwind from higher interest rates.

In Q1, VNO “postponed” its dividend. Generally speaking, REITs need to pay out 90% of net income to shareholders, and so later this year, it will make a final dividend payment, in cash or stock, to ensure it satisfies this requirement. It will mean its dividend runs lower than the $0.53 it was paying last year. Thus far this year, it has earned $0.54 in net income and paid $0.38 in dividends, meaning its end-of-year payout will likely be below $0.40. In the quarter, VNO spent $6 million on share repurchases, and has $171 million of the $200 million authorization remaining.

When thinking how to value VNO, we can first consider its net asset value. VNO has $4.88 billion of book common equity and just a $4 billion market cap. The market is saying its assets are worth ~$900 million less than their carrying value. VNO has $10 billion in real estate, which implies a 9% below book value of its properties.

Now, I would also note that VNO took $600 million of impairments in Q4 2022. Considering this, this market is saying VNO’s buildings are worth about 15% less than what it costs to build and upgrade them, after depreciation and charges. Given the magnitude of pressures on commercial real estate valuation, just from higher rates, let alone the secular challenges facing office, this does not jump out as being very undervalued. Indeed, Kilroy (KRC) shares imply a 20% discount, and they have a 7+% dividend yield fully covered.

Given the challenges facing the office sector, I think investors should expect ongoing declines in NOI as more and more leases mature and occupancy gradually falls. VNO earned $0.66 in NOI this quarter, but this will likely fall next year. Assuming just a 1% decline in occupancy, flat operating expenses), and scheduled higher interest, VNO’s quarterly earnings-run rate in a year will fall to $0.58-$0.60.

That gives shares a 12% FFO yield. Even assuming a 1.5x coverage ratio, in theory, the distributable yield is 8%. In practice, given its ongoing development portfolio and focus on paying down high-cost debt, we are unlikely to see it return its dividend to such a level. I expect VNO will continue to postpone dividend payments in 2024 and pay closer to 90% of the taxable income floor.

While the interest rate headwind may peak in 2024, the pressure on office occupancy is not going away, meaning this potential distributable income will likely continue to fall beyond next year. At an 80% long-term occupancy rate, VNO would have about $0.45-0.48 in FFO or $1.92/year, and at 1.5x coverage that would support a $1.28 long-term dividend. At an 8% yield, shares would be worth $16. At that price, the stock would be assuming a 25% loss on its real estate holdings relative to book value (including the $600 million impairment).

While shares may not get there immediately, that is where I see long-term fair value, given the secular challenges I see for office. Investors may look at VNO’s earnings today and view the stock as cheap, but given rising interest expense and ongoing incremental declines in occupancy, I fear one would be buying into a melting ice cube. That can work when the business is priced for decline, but shares are not there yet. I would use the recovery in recent months to sell and wait for $16 before considering buying.

Q2 2024 Earnings Call Transcript")