Morsa Images

An intellectual is a man who takes more words than necessary to tell more than he knows.” – Dwight D. Eisenhower.

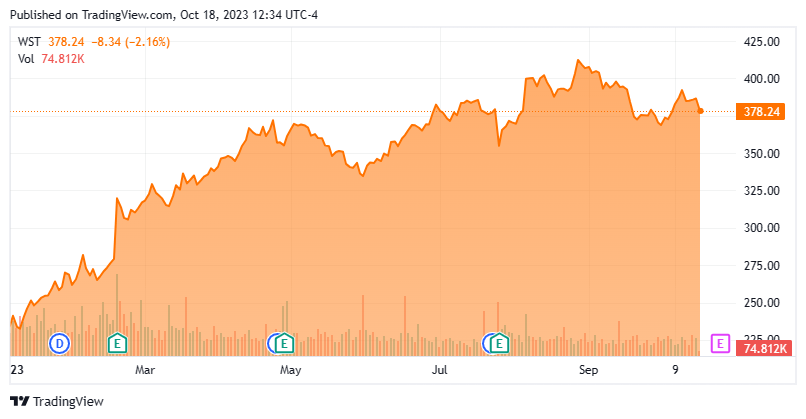

Today, we put West Pharmaceutical Services, Inc. (NYSE:WST) in the spotlight for the first time. This manufacturer supplies various parts of the healthcare industry. The stock has delivered for shareholders so far in 2023 with a better than 60% gain, but the shares have seemed to have hit some recent technical headwinds. Insiders sold a decent chunk of their shares in August and September as well. Higher or lower from here? An analysis follows below.

Seeking Alpha

Company Overview:

West Pharmaceutical Services is headquartered just outside of Philadelphia in Exton, PA. The company designs, markets, and manufactures containment and delivery systems for injectable drugs and healthcare product globally. These include items such as stoppers and seals for injectable packaging systems; syringe and cartridge components, as well as custom solutions for the needs of injectable drug applications. The company operates via two main business divisions: Proprietary Products and Contract-Manufactured Products. The stock currently sells for just under $380.00 a share and sports an approximate market capitalization just over of $28 billion.

Second Quarter Results:

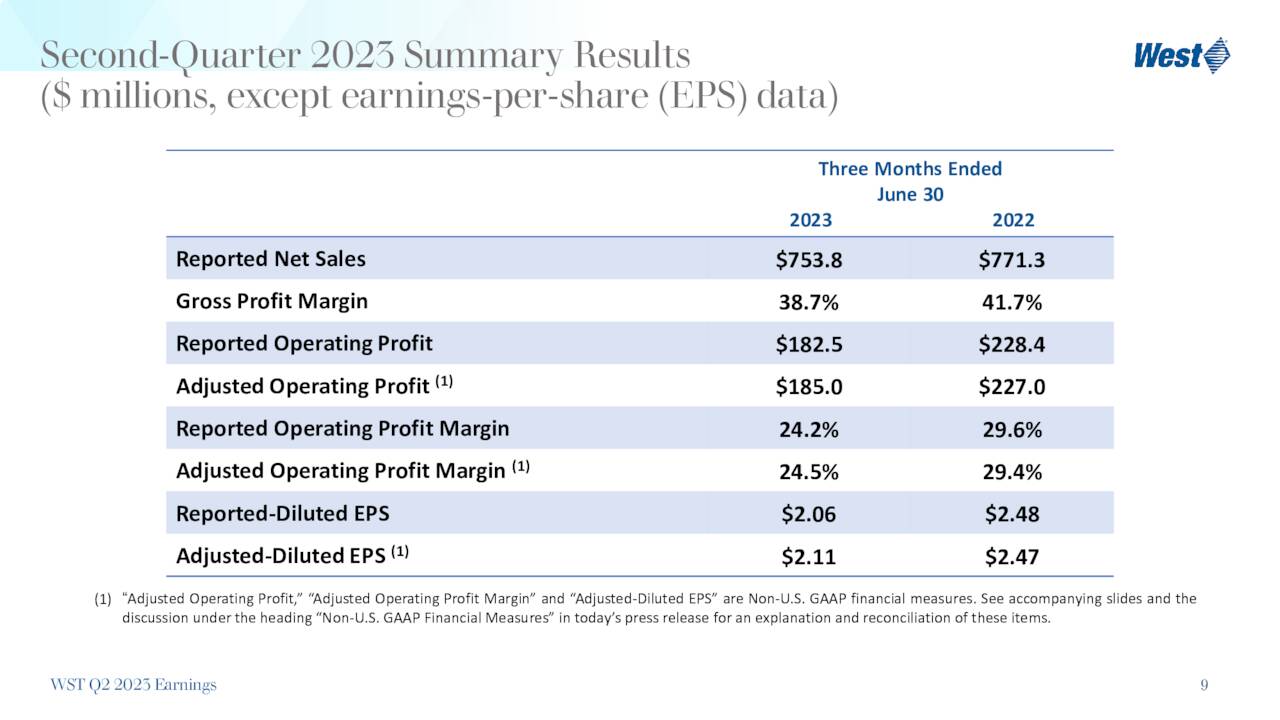

The company posted its second quarter numbers on July 27th. West Pharmaceuticals had a non-GAAP profit of $2.18 a share, 18 cents a share above the consensus even as sales fell just over two percent on a year-over-year basis to just under $754 million. Both EPS and margins fell from the same period a year ago it should be noted.

July Company Presentation

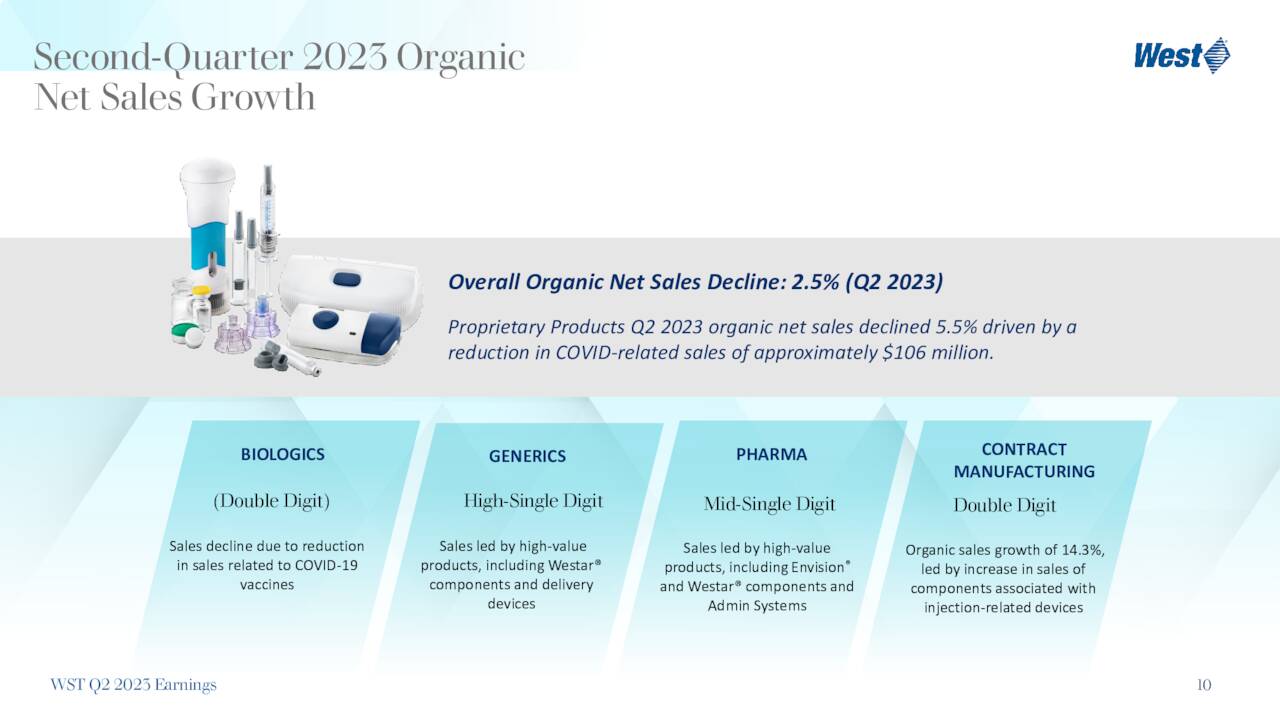

Leadership noted the small y/y sales decline was due “primarily driven by an expected reduction in COVID-19 related sales.” Net sales in West’s Proprietary Products division declined by 5.5% to $618.0 million. Management noted that if not for the fall in Covid-related sales, this division would have seen double digit year-over-year revenue growth. Contract-Manufactured Product net sales grew just over 15% from the same period a year ago, to $135.8 million.

July Company Presentation

Management lifted FY2023 ever so slightly to a range of $2.970 billion to $2.995 billion and also bumped its non-GAAP earnings guidance to $7.65 to $7.80, up 15 cents a share from its previous forecast.

Analyst Commentary & Balance Sheet:

Since July, Stephens ($420 price target, up from $400 previously), Bank of America ($405 price target) and KeyBanc ($440 price target, up from $415 previously) have reissued Buy ratings on the stock. UBS maintained their Neutral rating on the stock in July, but did lift their price target to $400 a share from $365 previously.

Just a touch over one percent of the outstanding float in the shares are currently held short. Numerous insiders have been heavy sellers of the stock in 2023. They sold just over $11 million of equity collectively in September after disposing of north of $25 million worth of stock in total in August.

July Company Presentation

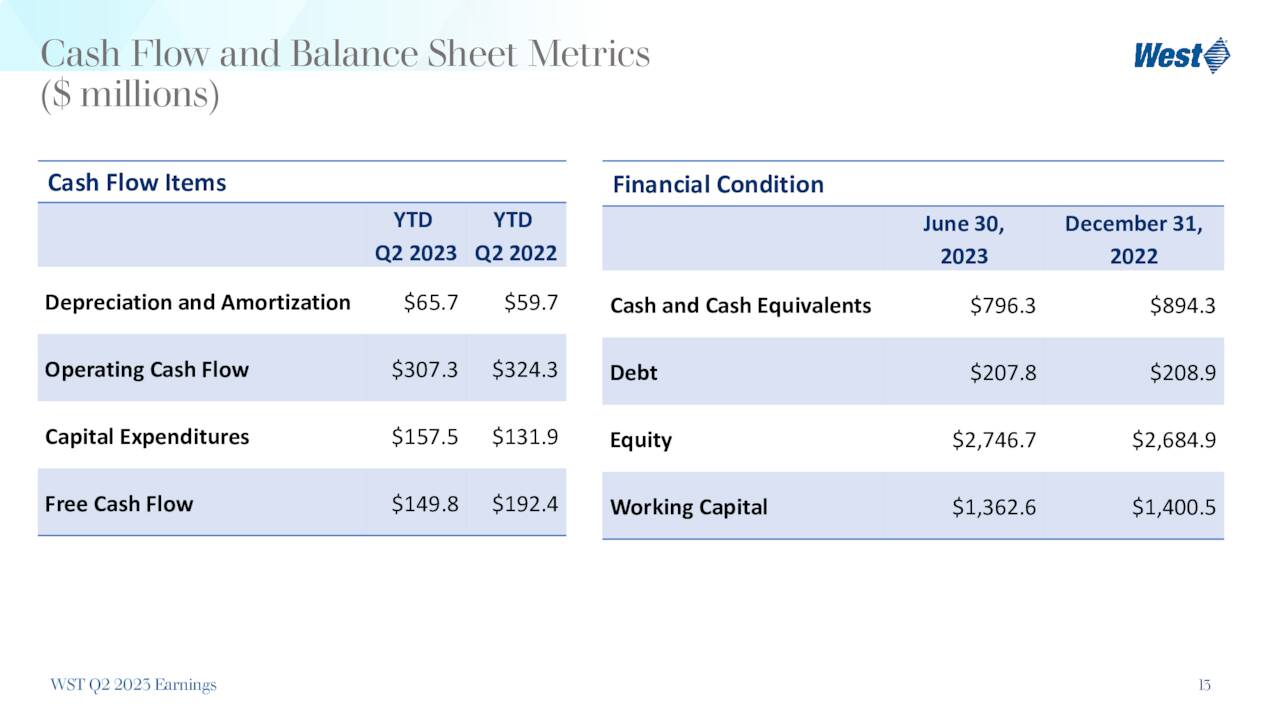

The company ended the second quarter with just under $800 million in cash and marketable securities on its balance sheet against just over $205 million in long-term debt, according to the company’s second quarter 10-Q statement. The company produced just under $150 million of free cash flow [FCF] in the second quarter, which was down from just over $190 million in the same period a year.

At the second quarter run rate and with the stock at current trading levels, West Pharmaceuticals has a current FCF of approximately 2.1%. West Pharmaceuticals repurchased nearly $225 million worth of its own shares in the second quarter at an average price of just over $345 a share.

Verdict:

West Pharmaceutical Services, Inc. made a profit of $8.58 a share in FY2022 on sales of $2.89 billion. The current analyst firm consensus sees profits falling in FY2023 to $7.99 a share even as sales rise by $100 million. They project earnings will rebound in FY2024 to $8.83 a share as sales growth by nearly 10%.

It is hard to see any compelling valuation in West Pharmaceutical Services, Inc. shares at these current trading levels given its near-term profit and revenue growth prospects, which should improve once Covid impacts are fully in the rearview mirror. The stock currently trades at over 45 times forward earnings and over nine times sales. The shares FCF yield of just over two percent is also dwarfed by the 5.5% yield provided by “risk free” short-term treasuries. Insiders seem to be prudent in paring their holdings after 2023’s big run up in the stock. Therefore, the investment recommendation on West Pharmaceutical Services, Inc. is Avoid.

Intellectuals solve problems, geniuses prevent them.” – Albert Einstein.

Q2 2024 Earnings Call Transcript")