Michael Vi

Investment thesis

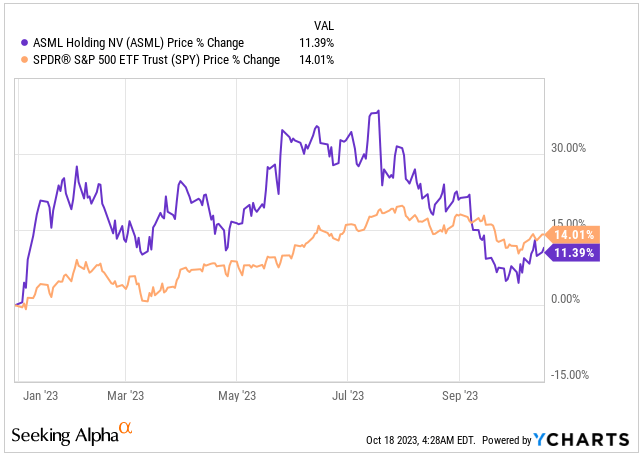

ASML (NASDAQ:ASML), the third-largest European company with a market capitalization of $237 billion, has experienced a rollercoaster year. At the beginning of the year, the company fared well, riding the tailwinds of the AI craze heading into the summer.

At that time, I had written an in-depth article delving into ASML and Q2 earnings, which you can access here. In the article, I praised the business and recommended it as a BUY due to its monopoly-like position, wide moat and management increasing the guidance for the second time in 2023.

However, as more negative economic news surfaced, coupled with a “higher for longer” narrative and broader consumer spending pullback in electronics, as well as delays in the development of new semiconductor fabs in the US and Europe, ASML began to underperform the broader market.

Price Return (Seeking Alpha)

ASML, a company I regard as one of Europe’s finest in terms of fundamentals, management, and its promising future amidst the ongoing digital evolution, has unveiled its Q3 earnings today.

Let’s look into the details of the Q3 report and explore what lies ahead for the company.

Q3 was solid, yet FY24 no-growth outlook is worrisome

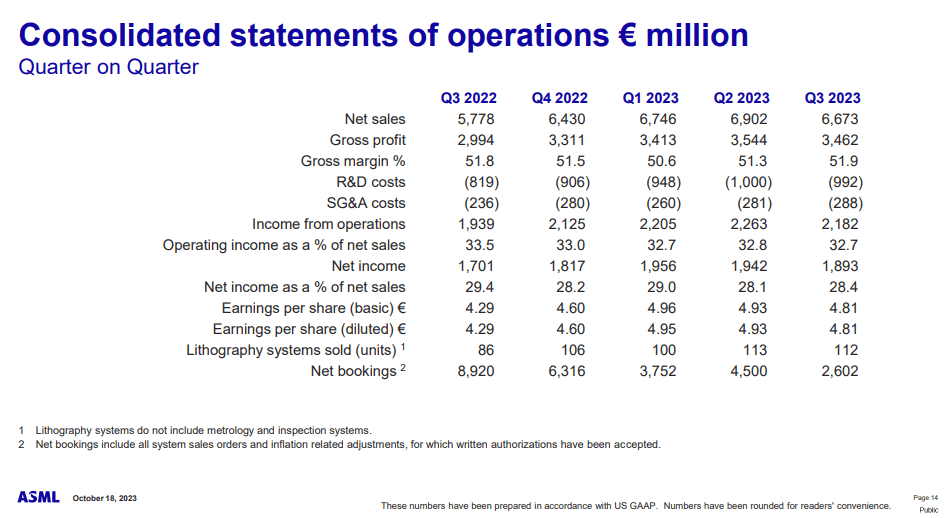

ASML’s Q3 earnings were very solid. The company reported sales of €6.7 billion, in-line with analysts’ expectations, but significantly higher than the €5.8 billion reported in the previous year. This translates to a net income of €1.9 billion or €4.81 EPS, representing a 12% increase from the previous year.

What’s even more significant is the sustained high Gross Margin at 51.9% in Q3 2023, surpassing the already impressive 51.3% of the previous quarter. This is remarkable, especially considering the higher sales and EPS back then. It indicates that the company is becoming more efficient with its COGS and manufacturing processes, a trend I anticipate will continue.

However, one concerning aspect of the report is the relatively low net bookings in Q3, totaling only €2.602 billion, marking a 42% decrease from the previous quarter. This decline underscores the slowdown in demand and the prevailing market uncertainty. Nevertheless, it is expected that this represents the bottom of the cycle, and improvements are anticipated from this point onward.

Consolidated Financial Statement (ASML IR)

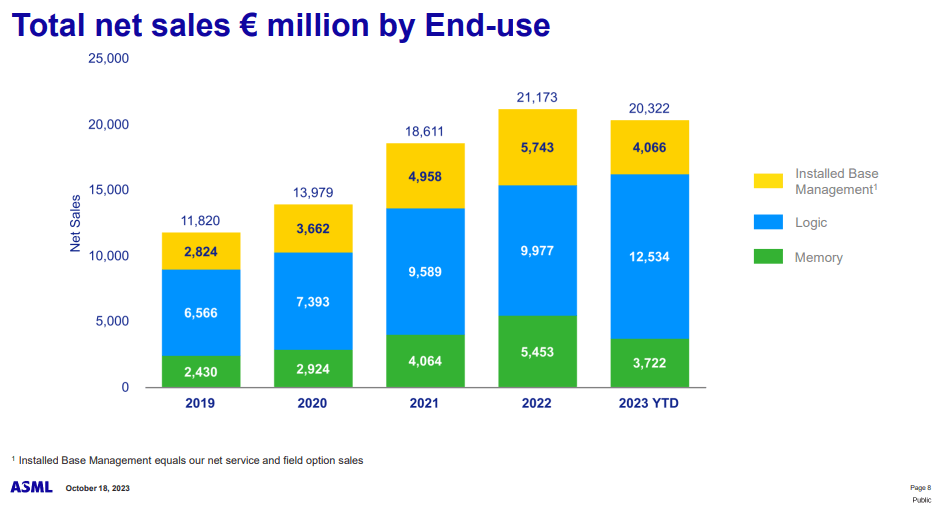

In terms of the total net sales breakdown, Logic has dominated the YTD results, contributing 61.6% to the total net sales. This trend, although not aligning with the success story of ASML’s Q3 earnings where Memory was perceived as the smaller but faster-growing segment, is noteworthy. Despite the YTD performance not being stellar, Memory has shown significant growth, increasing from 16% of Net Sales in Q2 to 24% in Q3.

I expect the robust growth of the Memory sector to resume, particularly with the rising AI trends in Q4 and throughout 2024. Memory chips serve as the backbone of AI and ML, playing a critical role in storing extensive datasets.

Total Net Sales (ASML IR)

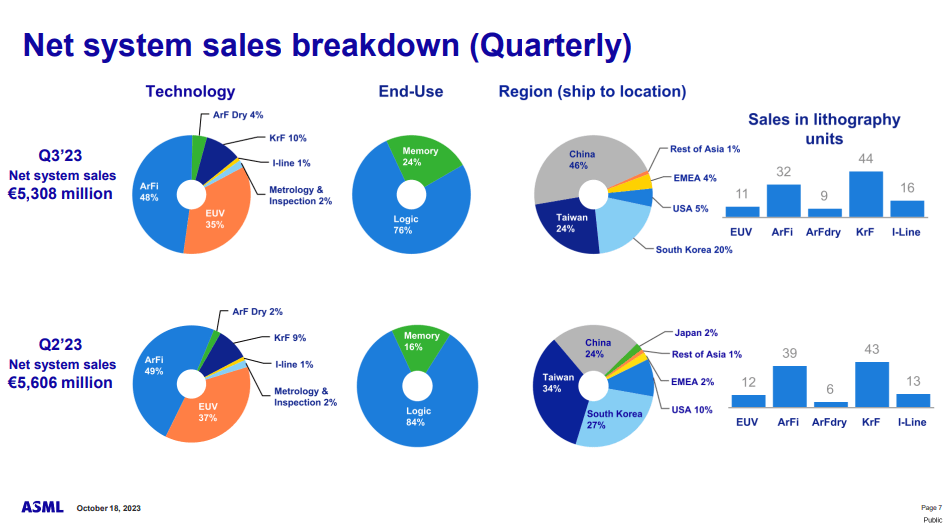

In Q3, ASML sold 112 lithography systems, a number similar to the 113 systems sold in Q2.

The concerning aspect lies in the performance of the EUV systems. While Q2 saw relatively low EUV sales at 12 units, Q3 witnessed a further decline to 11 of these high-value machines, each priced between €300-€350 million. The primary cause for this decline is the delays in the development of new fabs in Europe and the US, with companies such as TSMC (TSM), Intel (INTC), and Samsung (OTCPK:SSNLF) experiencing significant setbacks due to a lack of skilled talent in these regions.

For instance, TSMC initially planned to have its first chip factory in Arizona operational by late 2024, but confirmed delays have pushed the start date to 2025.

ASML’s EUV machines are completely prohibited for export to China, and as of September 2023, new regulations mandate that ASML needs a license from the Dutch government to export equipment capable of producing sub-5nm chips. It is unlikely that new licenses for the export of ASML’s most advanced DUV equipment to China will be approved beyond the end of this year.

Despite these challenges, China has played a significant role, contributing to 46% of new system sales in Q3, a sharp increase from 24% in Q2 and 9% in Q1. The reason is straightforward: while the delays in new fabs in the US and Europe have led to reduced sales in these regions, China has been striving to import as many devices as possible before access to ASML’s top-tier DUV technology becomes restricted.

I anticipate this trend to further intensify in Q4. However, as we move into 2024, we should expect a notable increase in system sales in the US and Europe, coupled with a decline in sales to China.

Keep in mind, that despite both the EUV and DUV machines for these new fabs are being manufactured, ASML can recognize the revenue for the sale, only once the machines were successfully delivered to the customer.

Net Sales Breakdown (ASML IR)

Despite the setback in net bookings and what I would describe as an unfavorable trend in the geographical distribution of sales, the earnings were actually impressive.

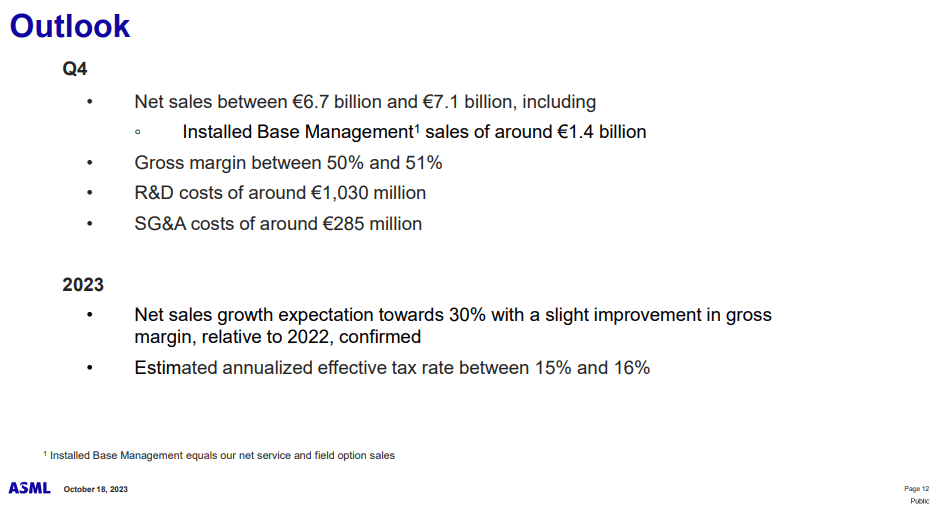

Simultaneously, ASML has reiterated its outlook for Q4, anticipating sales between €6.7 to €7.1 billion, with margins remaining at the higher end of the historical range. The company still anticipates a 30% YoY sales growth. However, for 2024, the company does not foresee any top-line growth, indicating a transitional year with virtually flat YoY sales.

Outlook (ASML IR)

Cheap(er) valuation, promising outlook

In simple terms, Q3 earnings for ASML have been positive. However, the concern arises from the company’s lack of growth expectations in 2024. The forecast indicating sales in-line with 2023 has caused the stock to drop by approximately 5% this morning.

Nevertheless, the combination of robust earnings and the underperformance of the share price in 2023 has created a favorable valuation scenario.

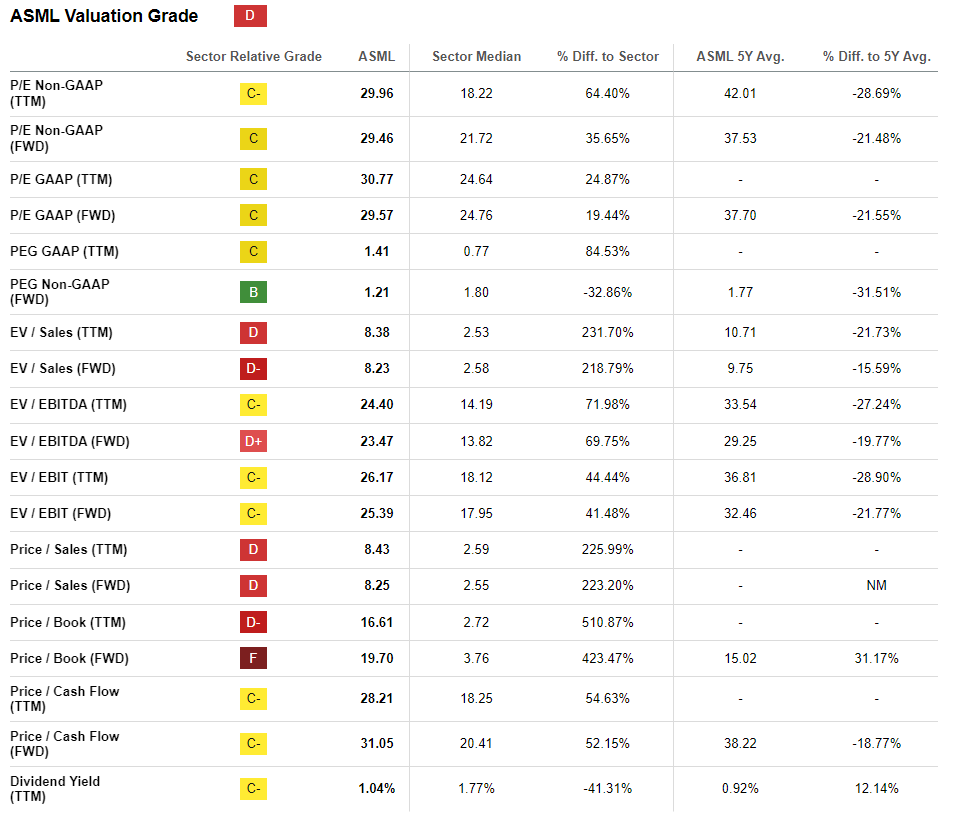

Despite receiving a “D” grade valuation from Seeking Alpha, ASML is currently trading at a significant discount compared to its historical valuation metrics.

The Forward PE Ratio is presently at 29.46x FY24 earnings, whereas the 5-year average has been 37.70x, indicating a 21.5% discount.

Furthermore, the Forward EV/EBITDA sales ratio also demonstrates a 20% discount, currently standing at 23.47x FY24 earnings.

Valuation Grade (Seeking Alpha)

Naturally, when growth companies slow down their expansion, they often experience significant drops in their stock prices and increased volatility.

However, despite the single-digit fall in ASML’s stock price this morning, the situation is somewhat unique. The company anticipates 2024 to be a transition year, as emphasized by Peter Wennink, the CEO of ASML. According to him, this period is crucial for preparing for the substantial growth expected in 2025.

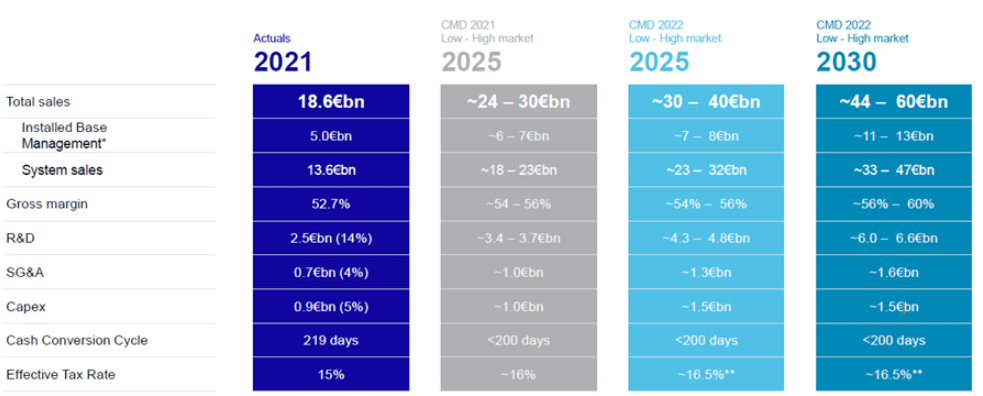

What’s even more noteworthy is ASML’s commitment to the guidance provided during ASML’s Capital Market Day in 2022. During this event, the company introduced a revised financial model for 2025 and 2030. As per this model, ASML aims to achieve sales ranging from €30-€40 billion in 2025, escalating to a substantial €44-€60 billion in 2030.

Reaching the €60 billion sales milestone in 2030 would signify an annualized sales growth of 16% from their 2022 revenue. Although slightly below the past decade’s CAGR of 17.3%, this growth trajectory is nonetheless exceptional.

Multi-year Guidance (ASML IR)

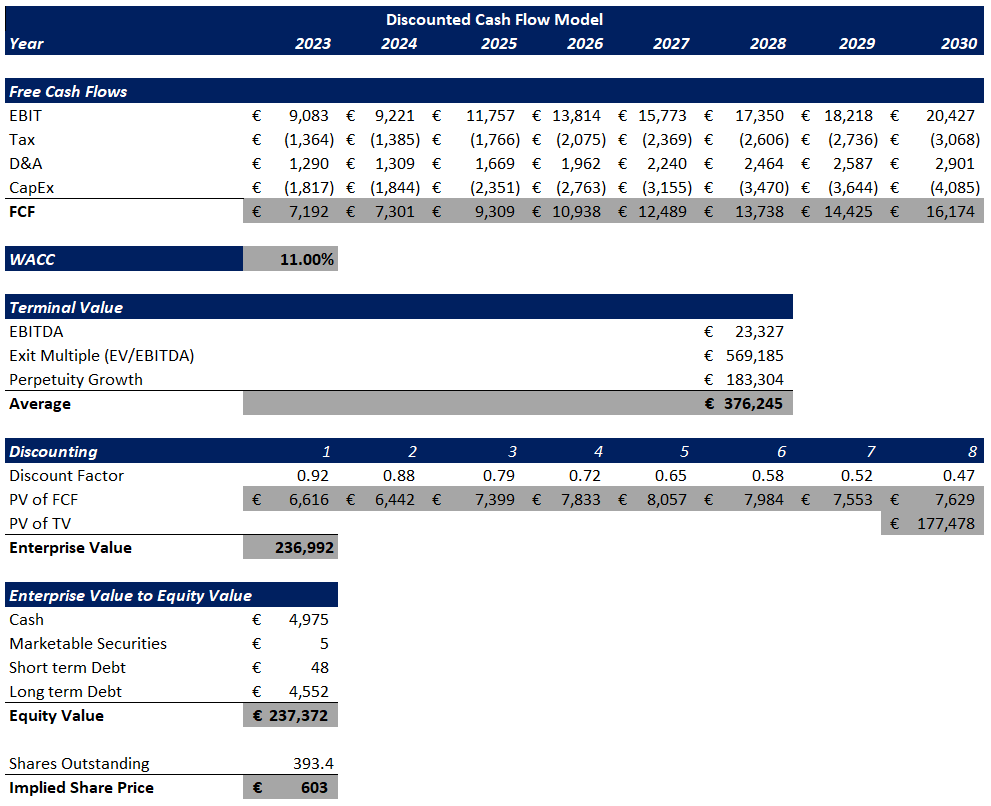

The question at hand is how to adjust DCF given the assumption of a no-growth year in 2024 and a slightly higher cost of capital due to interest rate hikes, compare to my previous article.

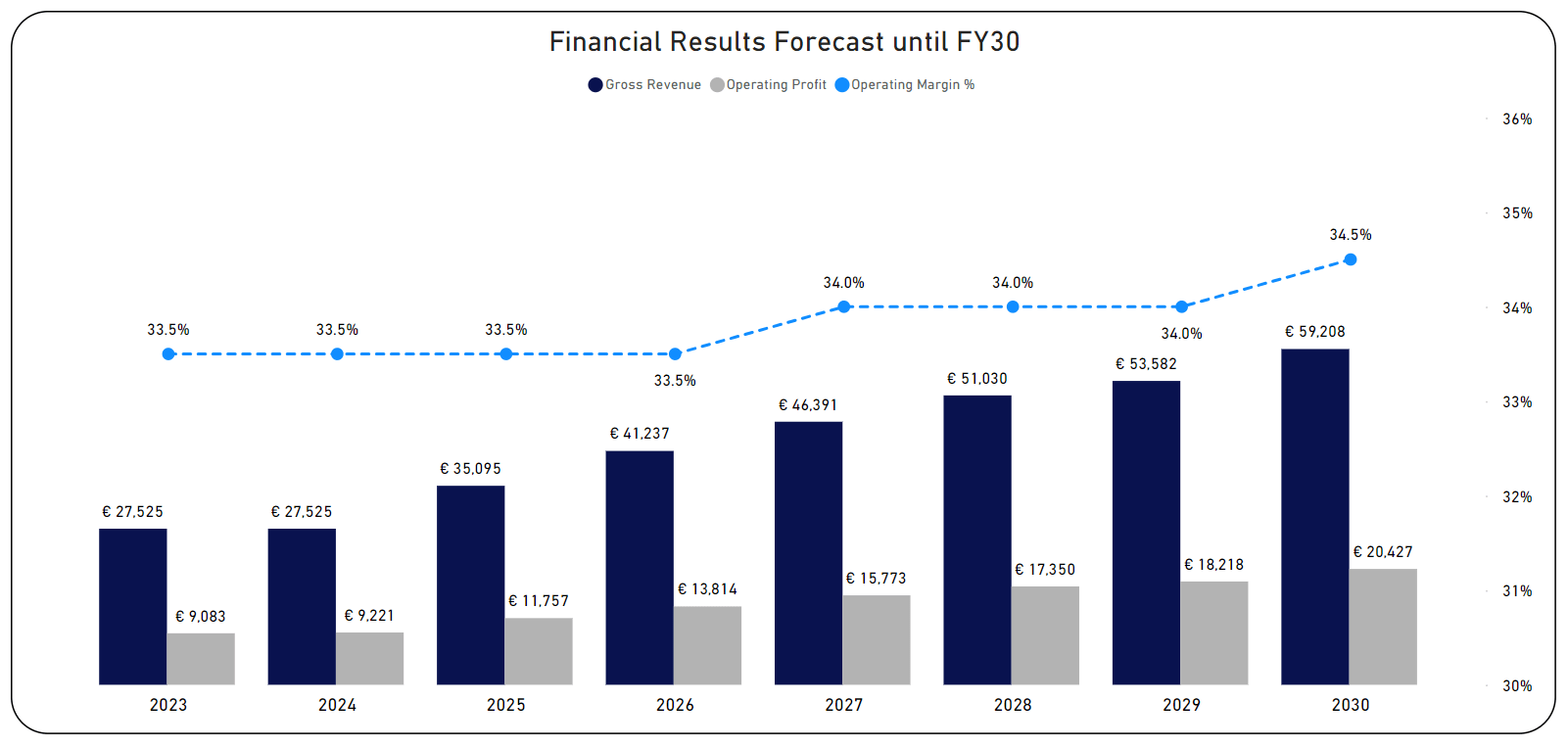

Based on ASML’s guidance indicating a 30% YoY sales growth for 2023, it is expected that they will achieve sales of approximately €27.5 billion by the end of the year, with an operating margin around 32.5%.

Considering 2024 as a no-growth year, there is the anticipation of at least a slight improvement in margins, a trend that is expected to continue until 2030.

Simultaneously, the projection incorporates the assumption that the company will experience a 16% annualized sales growth over the next seven years, culminating just below the upper end of ASML’s guidance at €59.2 billion.

Financial Forecast (Author’s Graph)

Certainly, considering the heightened cost of capital due to increased interest rates, it’s prudent to adjust the WACC from 10.5% to 11%.

Other assumptions I am using for the DCF model:

- Tax 15%

- D&A and CAPEX at 14.2% and 20% of EBIT respectively

- EV/EBITDA 24.4x

- Perpetuity Growth 2%.

DCF Model (Author’s Graph)

Based on this calculation, I estimate the fair value to be €603. This implies a discount of approximately 10% to today’s share price of €546.

Conclusion

ASML reported its Q3 earnings today, demonstrating what I would consider reasonably good performance by adhering to their projected 30% sales growth for 2023.

However, due to economic uncertainty, a decline in demand for consumer electronics, and delays in new fabs in the US and Europe, the company has guided for flat YoY growth in 2024.

This announcement has raised concerns among investors, considering ASML’s status as a growth company with valuations higher than the market average.

Nevertheless, ASML’s CEO has acknowledged that the years 2023-2024 seem to mark the bottom of the semiconductor cycle, with 2024 being a transitional year, paving the way for significant growth in 2025 and beyond.

The company also remains committed to its long-term guidance of 16% annualized growth until 2030.

Given the current price below €550, ASML appears to be trading at a 10% discount to its fair value. This suggests that there might be a good investment opportunity, with potential for investors to capitalize on the market bottom.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")