ipuwadol/iStock via Getty Images

Sometimes, certain tech companies just fall out of fashion: not just with investors, but with their customers as well. This is especially true in competitive software categories like CRM, where ZoomInfo (NASDAQ:ZI) has dragged its feet and ended up becoming a distant laggard behind much more formidable players like Salesforce (CRM).

Year to date, ZoomInfo has seen its share price crumble by more than 30%. While buying the dip on this once-hot tech stock may be tempting, I have very little confidence that this stock is anything but a falling knife and a value trap, especially as its growth has cranked down to near-zero.

I last wrote a bearish article on ZoomInfo in March, when the stock was still trading closer to $16 per share. Since then, the stock has continued to fall, and the company has announced a fresh $500 million (just over ~10% of the company’s current market cap) for new buybacks. And yet, with the company’s net debt position, I’m not certain that these buybacks will be able to turn the tide: and with Q1 results worsening as well, I remain quite bearish on ZoomInfo’s prospects for the remainder of the year.

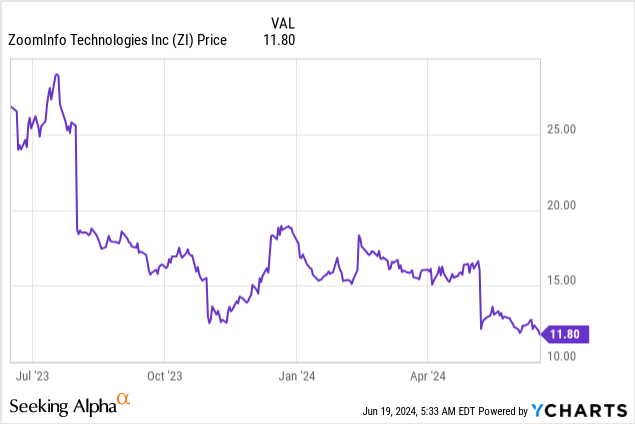

It’s worth noting that alongside Q1 results, which we’ll discuss in the next section, the company recently cut its full-year outlook (on both revenue and operating income/cash flow) in mid-May, owing to weaker end-customer trends:

ZoomInfo outlook (ZoomInfo Q1 earnings deck)

Even the new high end of the company’s guidance range at $1.27 billion represents only 2.5% y/y revenue growth for the full year.

ZoomInfo is banking on its new AI features, dubbed “ZoomInfo Copilot”, to resuscitate its sales momentum. The product comes with several cookie-cutter generative AI features, including AI-driven recommendations and ratings for prospective customers, as well as the ability to draft emails to clients.

ZoomInfo Copilot (ZoomInfo Q1 earnings deck)

The product released in late May, and while performance is yet unknown, I don’t think adding AI features will immediately drive a rebound in growth for a platform that is already struggling.

Here are all of the core risks for ZoomInfo:

- High customer exposure to other software companies. ZoomInfo’s core business is in selling to fellow software companies, which makes it even more exposed to the current macroeconomic situation, which has driven many tech companies to axe their sales and marketing headcount.

- Don’t trust a software company that’s barely growing. ZoomInfo is expecting only low single-digit growth in FY24. After dramatically rising in the pandemic, ZoomInfo’s growth has decelerated sharply – exhibiting a lumpy growth trend versus the more stable growth patterns that mature, higher-quality software companies have been able to manage.

- Very competitive landscape for CRM software. ZoomInfo is one of many CRM-style products and competes with much more recognizable names such as Microsoft’s (MSFT) LinkedIn and Salesforce. These competitors also have the capability to cross-sell CRM solutions with other platform products, while ZoomInfo stands alone as its own solution. In an environment where many IT departments are trying to consolidate vendors and limit budgets, this may hurt ZoomInfo more than in the pre-pandemic period.

- Large debt load. Unlike many tech peers, ZoomInfo is in a net debt position, and its floating debt structure exposes it to high interest costs.

- Not making progress on profitability: Despite a slowdown in growth rates, ZoomInfo has not made much headway in turning its focus to improving operating margins – despite laying off ~120 employees in FY23.

Steer clear here: there’s more downside ahead for ZoomInfo as its key metrics continue to deteriorate.

Q1 download

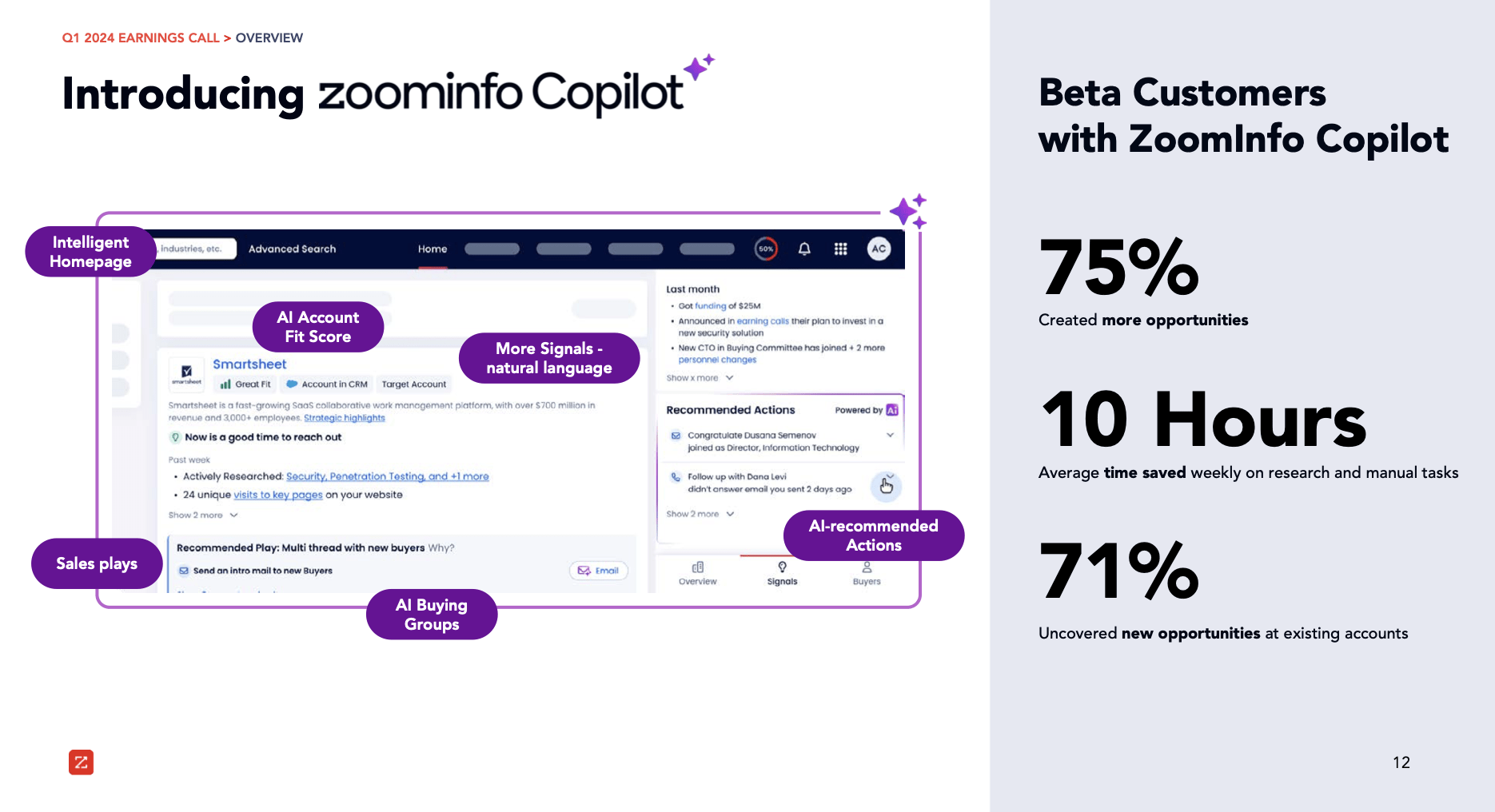

Let’s now go through ZoomInfo’s latest quarterly results in greater detail. The Q1 earnings summary is shown below:

ZoomInfo Q1 results (ZoomInfo Q1 earnings deck)

ZoomInfo’s revenue grew just 3% y/y to $310.1 million, decelerating versus Q4’s 5% y/y growth pace.

Continued churn in the SMB (small and midsized business) segment, which is ZoomInfo’s core target segment, was the main culprit – especially with continued layoffs among sales and marketing departments. The company hopes it has reached a bottom in terms of churn and retention. Per CEO Henry Schuck’s remarks on the Q1 earnings call:

We continue to navigate through a difficult operating environment, one that has not improved over the last few months. We had expected that this quarter would be challenging, and it was, but we are starting to see signs of stabilization. As it relates to net revenue retention, in the quarter, our SMB business continued to be challenged and performed worse than prior periods, and while down in Q1, given the higher mix of those businesses coming up for renewal, company-wide NRR was better-than-expected at 85%.

Mid-market retention was similar to Q4, and Q1 was the second quarter in a row of sequential renewal rate improvement, reflecting sustained stabilization. We saw enterprise retention stabilize, and we saw renewal rate there improve year-over-year for the first time since 2022.

Software retention also stayed flat sequentially for the first time since Q1 of ’22. These stabilization trends have continued into Q2, and are promising signs that suggest we have reached a bottom, which we view as a precursor to a potential inflection to growth. We also had another quarter of strong win-back performance. Customers continue to come back in record numbers after trying low-cost, low-quality providers.”

The company’s 85% net retention rate is quite low – many other software companies are still reporting net expansion trends well above 100%.

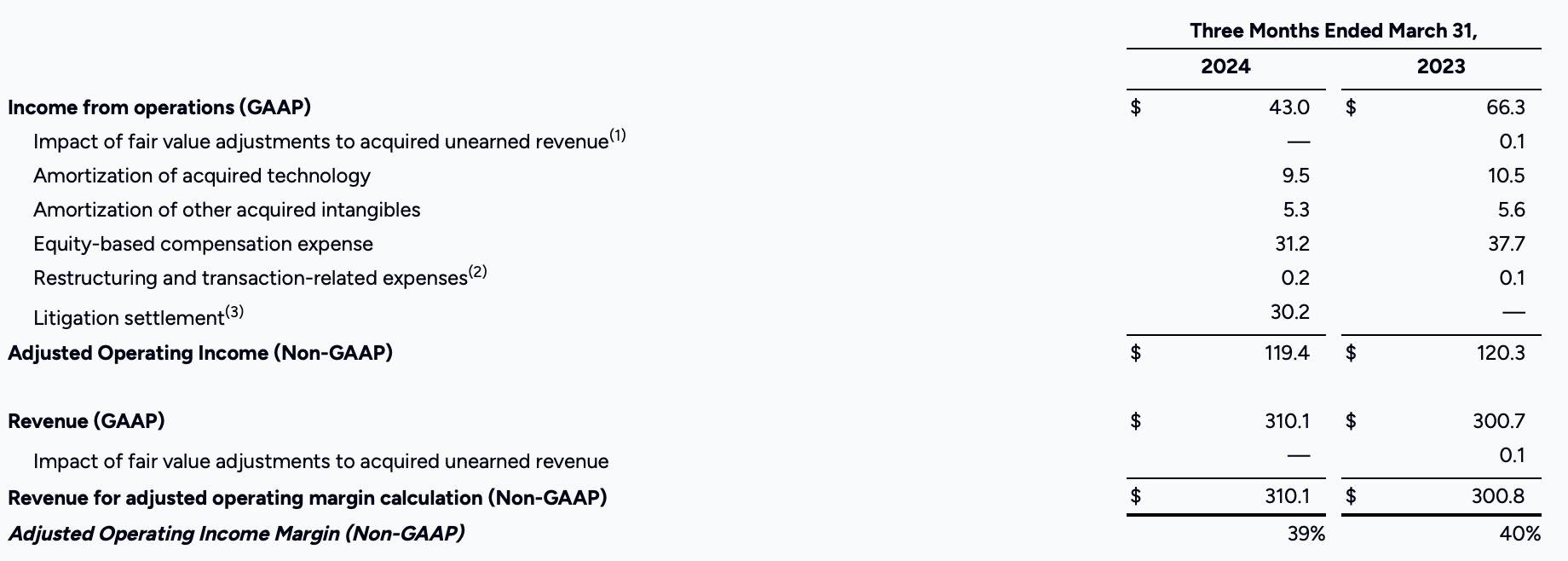

And in the wake of weaker top-line trends, we note as well that ZoomInfo isn’t making progress on profitability. Adjusted operating margins in Q1 clocked in at 39%, which were one point weaker than 40% in the year-ago Q1:

ZoomInfo margins (ZoomInfo Q1 earnings deck)

Valuation and key takeaways

Amid business turmoil, ZoomInfo’s stock remains unsurprisingly cheap. At current share prices near $12, ZoomInfo trades at a market cap of $4.41 billion. After we net off the $440.2 million of cash and $1.23 billion of debt on the company’s most recent balance sheet, ZoomInfo’s resulting enterprise value is $5.20 billion.

Against the $1.26-$1.27 billion revenue estimate for this year, the stock trades at 4.1x EV/FY24 revenue. That low multiple, however, factors in the stock’s meager growth, incredibility competitive CRM environment, and its exposure to SMBs.

There are upside risks here, of course. The Copilot AI product could sell better than anticipated (the company notes that Copilot is differentiated from other CRMs’ gen AI solutions as Copilot’s data stack draws from holistic business data, not simply the sales/contact information within the CRM); and a macro turnaround could bring more SMBs back to the fold.

Given poor and choppy execution so far, however, I’m not inclined to invest any further into this name. Continue to steer clear here.

Q2 2024 Earnings Call Transcript")