bowie15/iStock via Getty Images

Performance Assessment

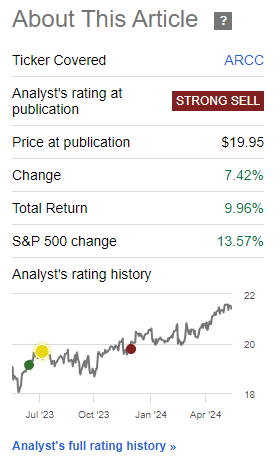

Since my last update on Ares Capital (NASDAQ:ARCC), ARCC has delivered a total return of +9.96% vs the S&P500’s (SPY) (SPX) +13.57% over the same period, leading to underperformance over the market index of +3.61%. Thus, I deem my ‘Strong Sell’ view to have been correct.

My ratings are always relative to the S&P500. Please refer to the bottom of this article to understand how to interpret my ‘Strong Sell’ rating.

Performance since last update on ARCC (Author’s Last Article, Seeking Alpha)

Thesis

I continue to believe, with a high degree of confidence, that Ares Capital will lag the S&P500. Hence, I am retaining my ‘Strong Sell’ view based on the following considerations:

- Deal activity is improving

- But investment yields and net investment margins may see some stress

- Valuations are at premium levels

- Relative technical analysis shows a clear sign of underperformance ahead

Deal activity is improving

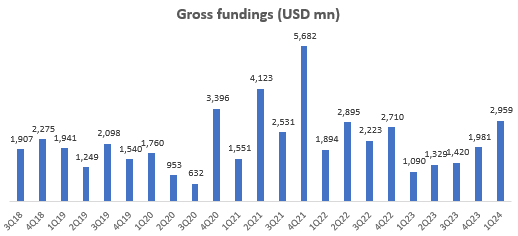

In my last article in December 2023, I noted how BDC deal activity was expected to improve in 2024. After a relatively quiet 2023, Ares Capital is seeing this play out. Gross fundings are up almost 50% QoQ and 172% YoY to almost $3 billion in Q1 FY24:

Gross Fundings (Company Filings, Author’s Analysis)

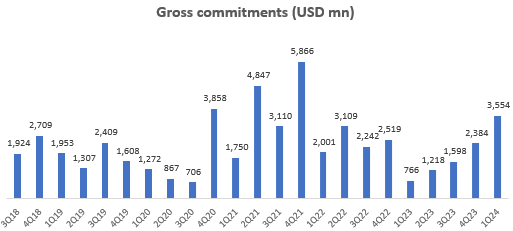

Commitments are a leading indicator of future fundings. Here too, Ares Capital has seen an almost 50% QoQ growth and 364% YoY growth in its rebound:

Gross Commitments (Company Filings, Author’s Analysis)

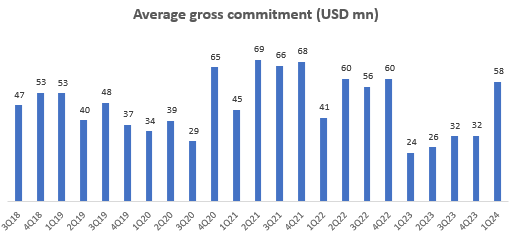

The average gross commitment value has spiked from ~$30 million levels to $58 million. I believe this reflects a more vibrant deal environment too.

Average Gross Commitment (Company Filings, Author’s Analysis)

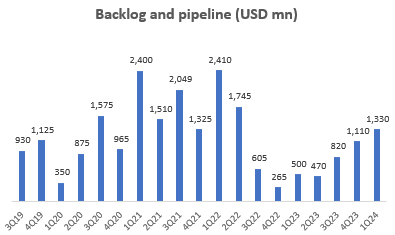

Lastly, backlog and pipeline figures are leading indicators of future deal closures. Here too, the rebound in the last 3 quarters is quite clear, giving confidence in a sustained period of higher deal activity, which helps increase the size of Ares Capital’s investment portfolio:

Backlog and Pipeline (Company Filings, Author’s Analysis)

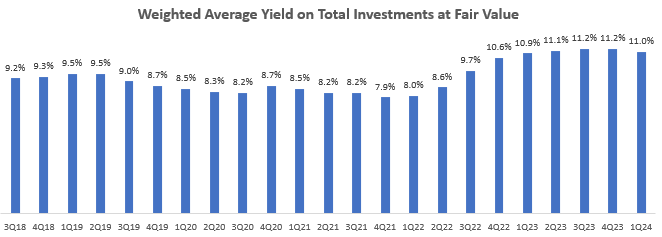

But investment yields and net investment margins may see some stress

Deal activity is picking up, but the average yield on Ares Capital’s investments at fair value seems to be peaking at 11.0%:

Weighted Average Yield on Total Investments at Fair Value (Company Filings, Author’s Analysis)

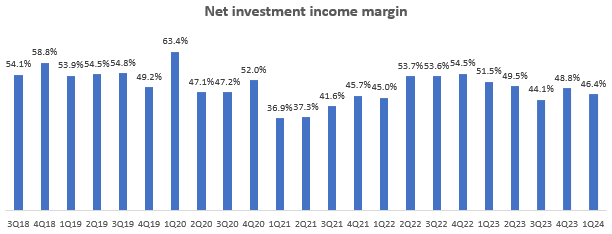

Moreover, the net investment income margins continue to be on a broad downward trajectory since Q4 FY22:

Net Investment Income Margin (Company Filings, Author’s Analysis)

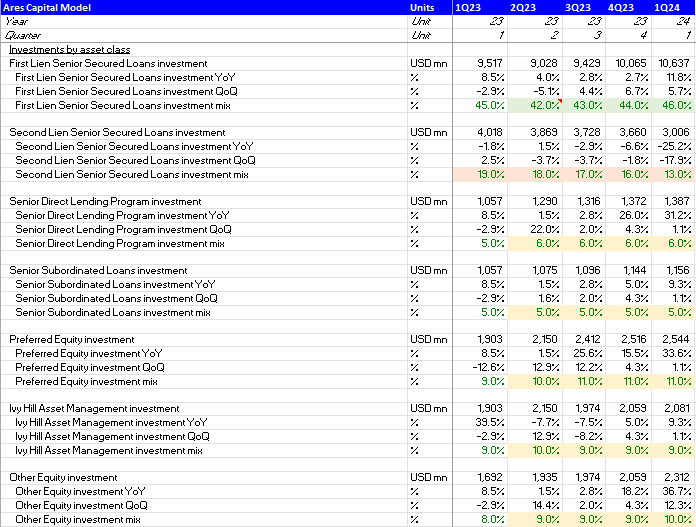

A key reason for this is due to a shift in the company’s investment portfolio toward higher first-lien investments and lower second-lien investments, with other categories being roughly equal in share:

Investments Mix Shift (Company Filings, Author’s Analysis)

As second-lien investments are higher yielding, this has put a downward pressure on the company’s overall yield and investment income margins. In the Q1 FY24 earnings call, management noted that:

…there aren’t as many second lien opportunities right now

– Co-President, Partner and Co-Head of US Lending Kort Schabel in the Q1 FY24 earnings call

This commentary makes sense given the higher competition in the deal environment, particularly by banks. According to Fitch Ratings,

Intensifying competition for deals is likely in the coming months as private credit lenders continue to grow and banks re-enter the space, which could pressure deal terms. The larger sizes of BDCs and affiliated platforms have allowed them to increase participation in upper middle market deals, but banks are taking back market share in recent months.

– Fitch Ratings’ BDC Sector Commentary in April 2024

I believe these competitive headwinds are likely to continue for Ares Capital.

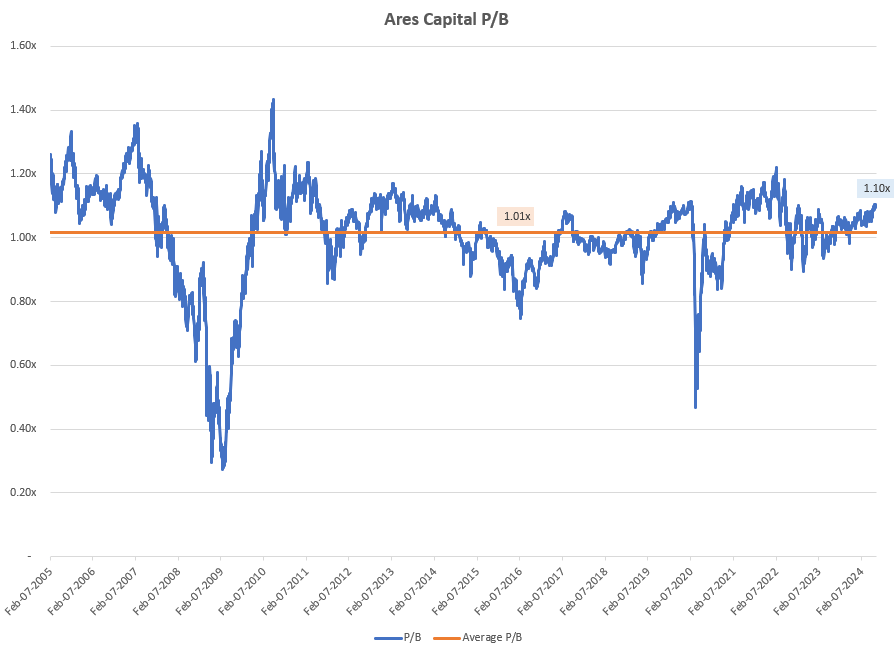

Valuations are at premium levels

Ares Capital is trading at a P/B of 1.10x; a 8.1% premium to the longer-term average P/B multiple of 1.01x:

Ares Capital P/B (Capital IQ, Author’s Analysis)

Hence, I believe there is limited margin of safety for buys, especially after considering the stress on yields and margins.

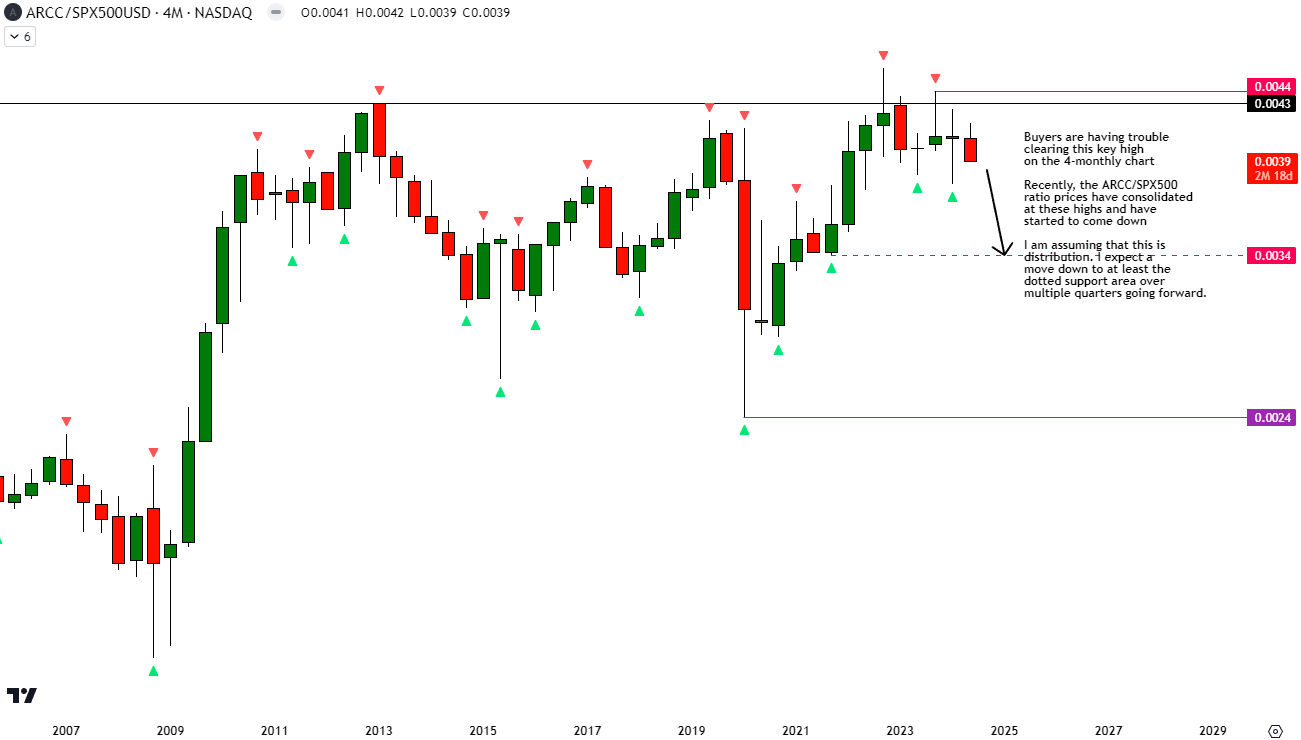

Relative technical analysis shows a clear sign of underperformance ahead

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do

Relative Read of ARCC vs SPX500

ARCC vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

On the 4-monthly chart of Ares Capital vs the S&P500, I see that the ratio prices have failed to breakout of the key high marked by the black line for many years now. More recently, since late 2022, the ratio prices have consolidated at these highs and is now starting to move down. Thus, I anticipate a breakdown to at least the dotted pink line over the next few quarters and possibly years. This would translate into alpha erosion vs the S&P500.

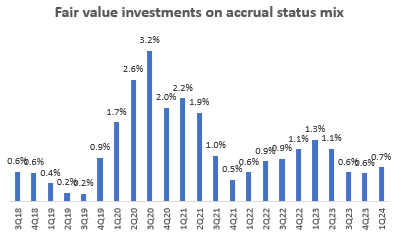

Key Monitorable

In their BDC sector commentary, Fitch Ratings noted that:

…U.S. business development companies (BDCs) face persistent headwinds in 2024, with rising paid-in-kind (PIK) income and continued markdowns of investments during 1Q24 signaling additional credit issues and resultant net investment income (NII) pressure

As a large market leading BDC that by its nature has a defensively positioned portfolio, Ares Capital is unlikely to witness such accrual problems early on. Indeed, this is what the numbers show too:

Fair Value Investments on Accrual Status Mix (Company Filings, Author’s Analysis)

Fair value investments on accrual status is near the lows at 0.7%. That said, I view this metric as a key monitorable as any sharp rise here would mean industry headwinds are getting significant enough to impact even the largest and most stable companies in the sector.

Takeaway & Positioning

My earlier ‘Strong Sell’ stance – which reflected a confident view of underperformance vs the S&P500 (see the how to interpret ratings section below) – has played out in Ares Capital since my last update; the stock has lagged the S&P500 by 3.61%. I think this trend is likely to continue:

Although deal activity is rising now, the numbers and commentary highlight how Ares Capital is facing competitive pressures, which is leading to a reduced share of higher-yield investments in its portfolio. This is putting some stress on yields and net investment income margins.

Despite this headwind, valuations are at a modest premium to historical levels. And according to my read, the technicals vs the S&P500 look more bearish now. Altogether, this leads me to retain my ‘Strong Sell’ view on Ares Capital, as I believe it would continue to underperform the S&P500 over the next few quarters and potentially years.

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P500 on a total shareholder return basis, with higher than usual confidence

Buy: Expect the company to outperform the S&P500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

Q2 2024 Earnings Call Transcript")