JHVEPhoto

Today, we take a look at giant home builder Lennar Corporation (NYSE:LEN). The company’s stock seems reasonably valued at just over 11 times trailing earnings, given the median analyst firm growth projections for both sales and profits in FY2024 and FY2025. That comes with the caveat that home builders almost always trade at a significant discount to the overall market due to the historical cyclicality of the industry. That said, the S&P 500 (SP500) currently is valued at just over 21 times forward earnings. The shares also sport a 1.3% dividend yield.

Lennar is headquartered in Miami, FL, about an hour drive south of me sans traffic on I-95. The company primarily sells homes under the Lennar brand and serves mostly the first-time, move-up, active adult, and luxury part of the housing sector throughout most of the United States. The company also provides financing, title and insurance services to its customers. The stock currently trades around $155.00 a share and sports a market capitalization of approximately $42.5 billion. Despite being “cheap” compared to the overall market, there are several reasons I would avoid the shares at the current trading levels.

Technical Resistance:

Seeking Alpha

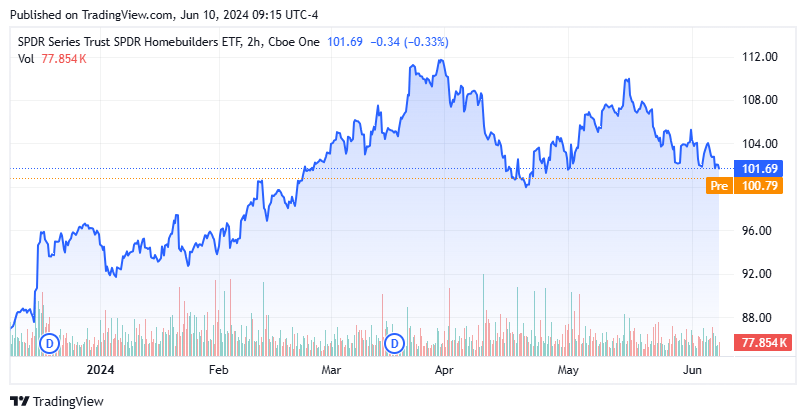

The first of the concerns around the stock is purely on a technical level. The equity seems like it is topping out in 2024 after a sharp rise since late October of last year at the end of a summer swoon in the overall market. The stock trades at the same levels of mid-December even as the NASDAQ (COMP.IND) is up nearly 19% and the S&P 500 has risen 17% over the past six months, including dividends. It also should be noted that the SPDR® S&P Homebuilders ETF (XHB) is also up over 16% since mid-December, as Lennar has become a laggard.

Seeking Alpha

Housing Headwinds:

MBIA, WolfStreet, Investing.com

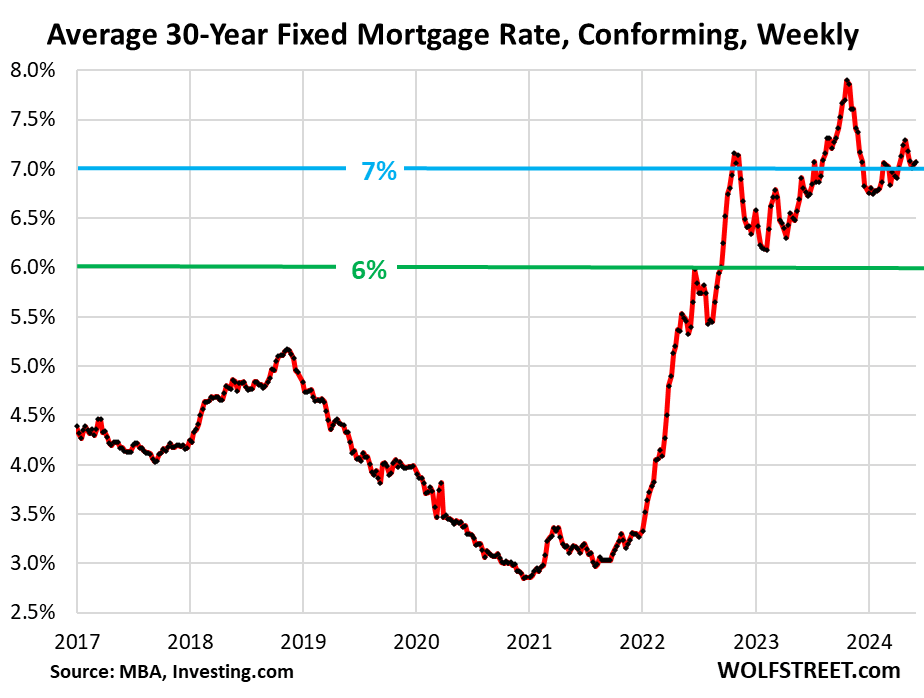

As I noted in an article earlier this month, the headwinds facing the housing sector are considerable and seem to be worsening. Thanks to considerable housing price appreciation since the pandemic and average 30-Year mortgage rates shooting up from just over three percent at the start of 2022 to around seven percent now; housing affordability is right at historical highs, which is captured nicely below.

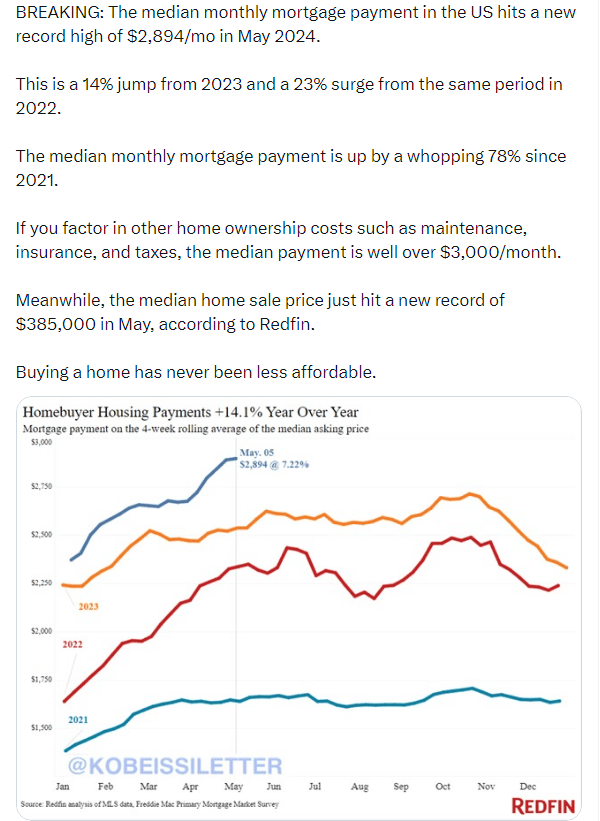

KOBEISSILETTER

High mortgage rates and few affordable houses on the market triggered the lowest level of U.S. existing home sales in 2023 since 1995. In addition, pending home sales in April plunged nearly eight percent, far below estimates. This also was the lowest level of monthly pending home sales since the early spring of 2020 when Covid lock-downs were being implemented across the U.S.

While the “golden handcuffs” of low existing mortgage rates have kept inventory low as few homeowners want to give up their existing three to four percent mortgage, that might be changing. Realtor.com recently reported that this May had the highest number of new existing home listings of any May since 2020 and the most price reductions for the month since 2017. More existing home inventory on the market combined with historically high housing unaffordability is likely to result in housing prices going down in the foreseeable future. At the very least, these forces will force home builders to lower prices and/or increase incentives (mortgage buy downs, free upgrades, etc.). This will negatively impact both margins and earnings at most home builders.

A Slowing Economy:

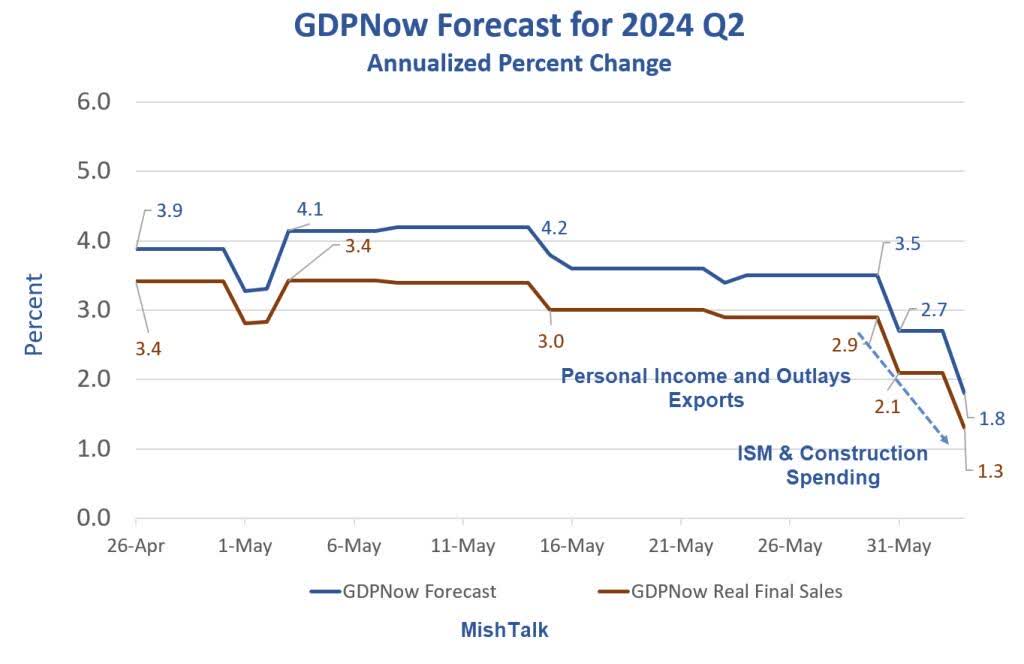

The economy is clearly slowing. After GDP growth of 4.9% in the third quarter of last year, GDP growth has slowed to 3.4% in the fourth quarter and a paltry 1.3% in the first quarter of this year. In addition, growth projections for second quarter GDP growth have also cratered in the second quarter, largely on weakening forecasts for consumer spending.

GDPNow/ZeroHedge

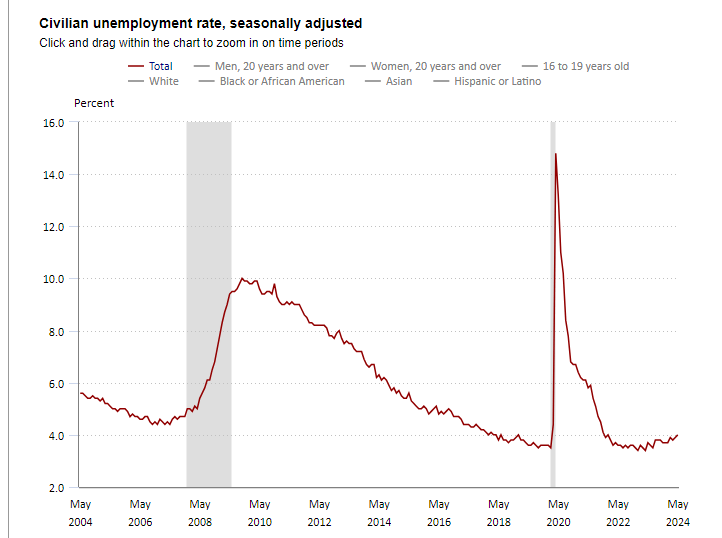

Despite the robust BLS jobs numbers for May on Friday, the unemployment rate continues to tick up and now stands at four percent. A slowing economy combined with rising unemployment will reduce housing demand further and likely will put more existing homes on the market. Obviously, this would be an additional headwind for home builders.

U.S. Bureau of Labor Statistics

Conclusion:

Despite flat-lining over the past six months, Lennar Corporation stock is still up some 50% from its late October low. The economy is also starting to get worse and housing inventory levels are increasing. While selling at 11.2 times trailing earnings per share looks cheap compared to the overall market, this valuation is still higher than other large home builders like D.R Horton (DHI) (10.2x trailing EPS) and PulteGroup, Inc. (PHM) (9.6x trailing EPS).

Also of note, after the equity saw no insider selling since late 2023, two insiders disposed of nearly $5 million worth of shares collectively in May. Therefore, LEN at current trading levels seems dead money at best and could be susceptible to profit taking if the economy continues to head south.

Q2 2024 Earnings Call Transcript")