aydinmutlu

National Grid Plc (NYSE:NGG)(OTCPK:NGGTF) is past the RIIO-ED1 compensation regime as of March 2023 and is now in ED2, and it’s been working on the RIIO-T2 regime since 2021 for the transmission networks. ED2 was appealed and contested by operators, as always, over the fact that its compensation may not be sufficient for the operators of the transmission and distribution concessions. Not just now but also in 2021, lowered regulated cost of equity brings down compensation rates to the point where National Grid has actually done a rights issue in order to expand its coffers, possibly to deal with grid improvements in order to handle the electrification trend, already having maximised their comfortable debt capacity. We addressed this as the primary issue in our last coverage. Still, their major RAB growth and capital investments are allowing for growth on a constant currency (C.C.) basis. While it’s not a business we’re interested in due to a moderate absolute valuation and relatively poor economics, we do note that it’s valued better than other regulated utilities that might be considered in a business-unfriendly environment.

Earnings Breakdown

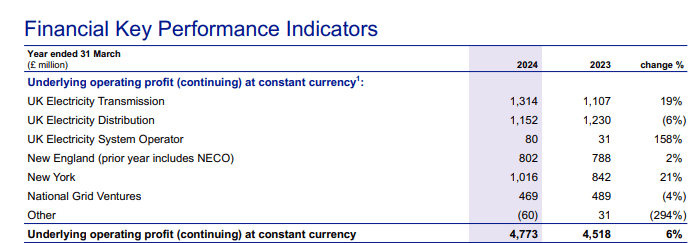

The C.C. figures pan out as follows for the full year:

FY IS Highlights (FY PR)

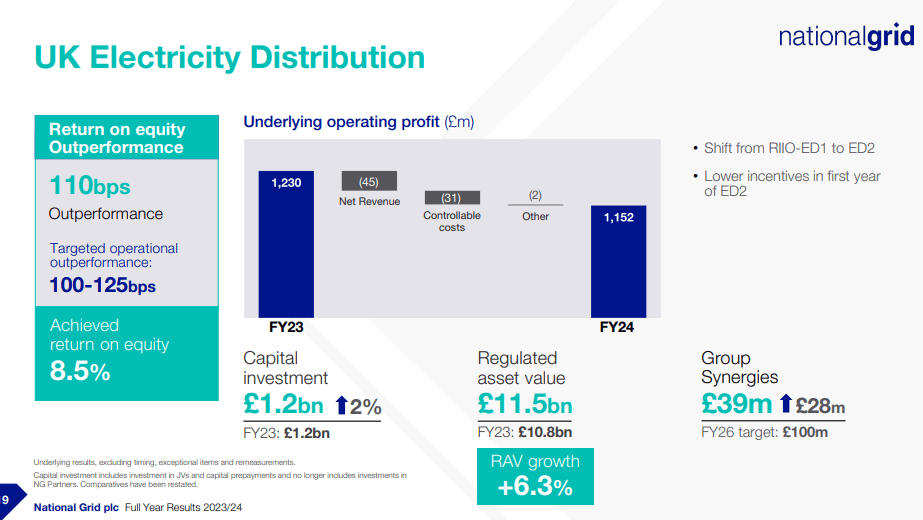

Distribution fell on account of lower baseline compensation from the RIIO-ED2 regime which was not offset by investments and higher RAB. Additionally, there was cost inflation in operating the distribution network for electricity. This is the ED2 regime. It is still benefiting from a RAB that is indexed to inflation, but the lower baseline is the issue, even after revisions up from the first draft, which was rough.

Distribution Concession (FY Pres)

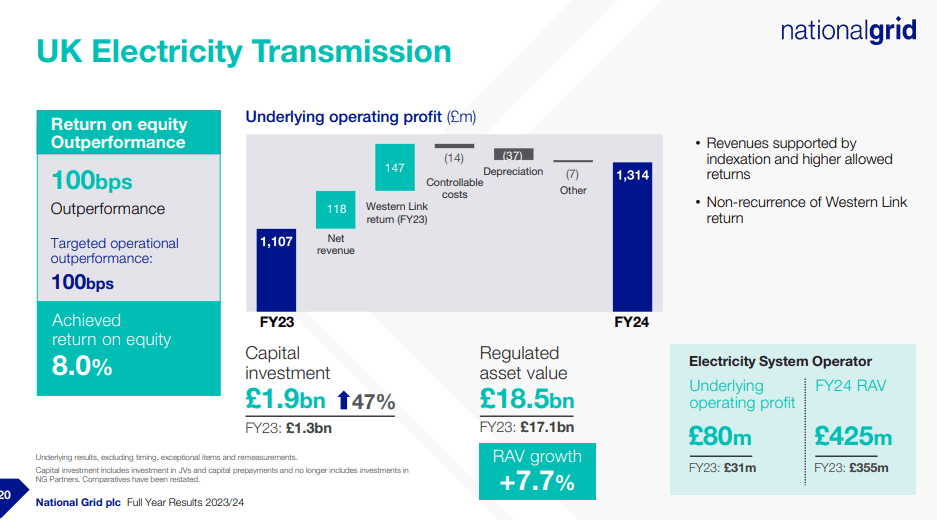

The RIIO-T2 regime was also complained about by the operators, but at least it has indexation in it which has allowed for higher costs of capital, indexed to the prevailing rate environment, to up the compensation accordingly over the last couple of years since the regime came into effect in 2021. Half the growth in the segment was due to liquidated damages from Western Link, which is a major project among UK regulated utilities to allow for export of clean energy from Scotland to the English and Welsh grids. This is a non-recurring positive effect and related to investigations around the timely delivery of the project.

UK Transmission Concession (FY Pres)

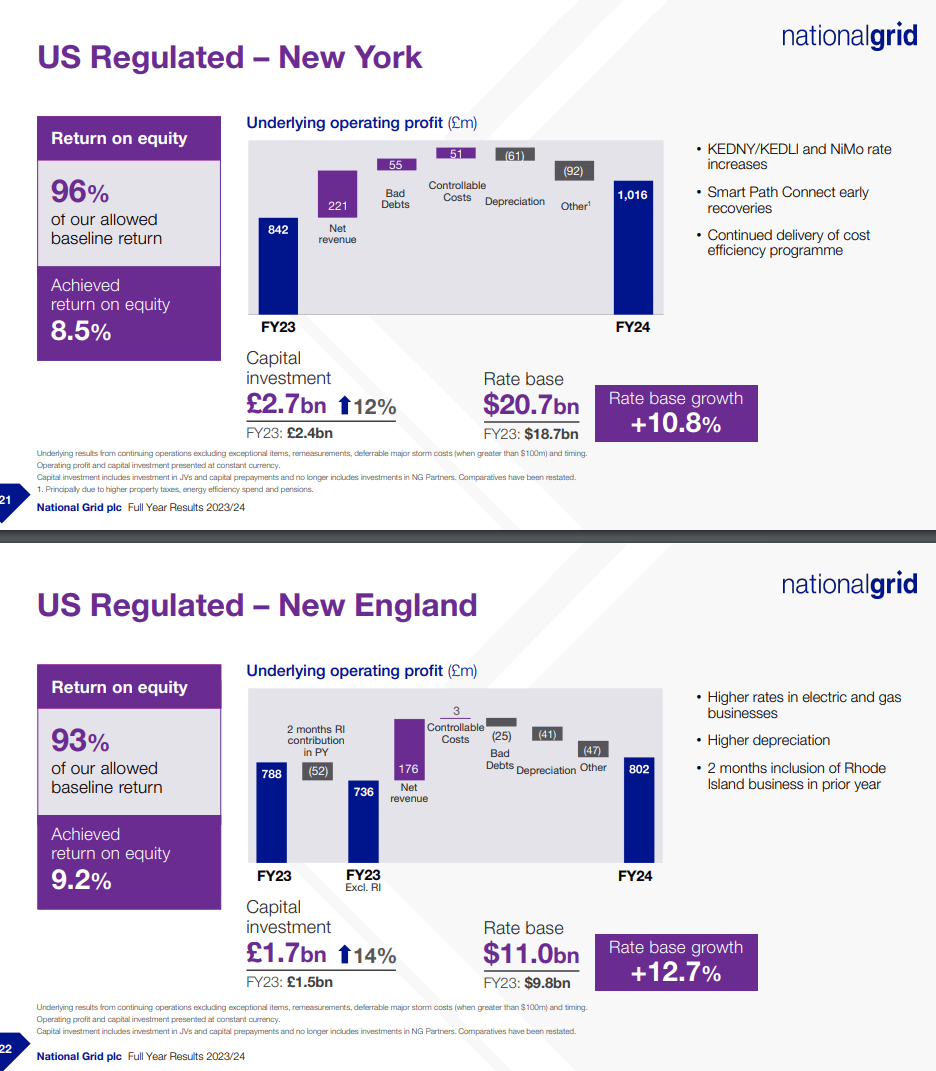

In terms of regulatory pressure, the later adoption of electrification in the US means that it’s less intense, and NG has been able to negotiate rate increases with the public utility authorities, getting pretty substantial raises to its rates in New England and in New York. In general, these US concessions, which are around 40% of operating profit, are attractive from a regulatory point of view.

US Concessions (FY Pres)

Bottom Line

Ofgem lowering cost of equity to levels that are notionally in line with a lower-beta equity return, around a 5.23% total at low assumed interest rates, has been a blow to the distribution business. The RIIO-T1 used to be unusually attractive for the transmission concessions before, but the change to T2 had brought things back to Earth in 2021. Together, the last few years have been a period of greater regulatory pressure and virtually no excess returns on the infrastructural investments. Of course, NG receives in exchange a less volatile cash flow, but things aren’t that great in the UK concessions, particularly in a rather inflationary environment where one will be concerned whether broad indexation fully does the job of compensating the operators who have to take the risk of operating the network at inflating costs. The US concessions don’t have that issue and are close to 50% of the business on a normalised basis.

It is still technically a growth business, as there is a lot to do in terms of growing RAB and meeting demand from the grid from consumers, but when that incremental investment is done at more or less fair value, there is no scope for outstanding value creation in the economic set up of the UK concessions. Again, the US concessions offer more latitude.

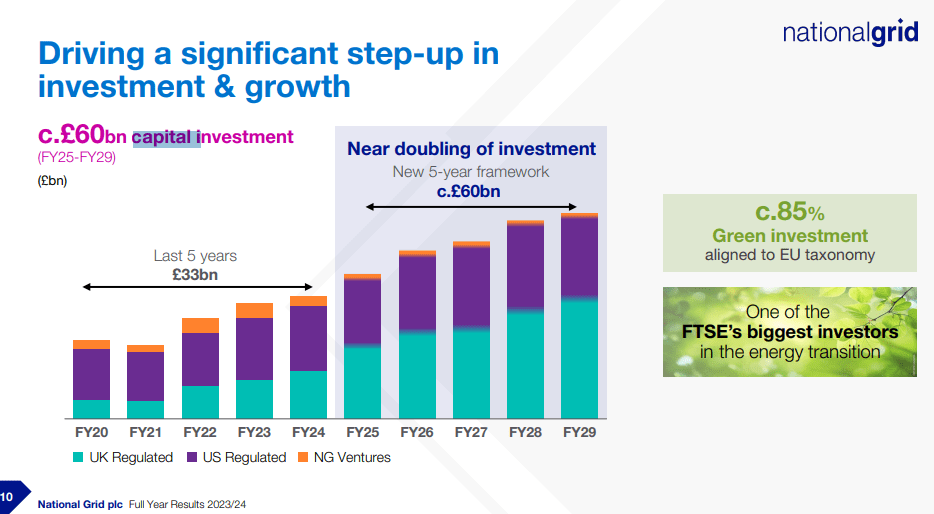

Highlighting the issues is the rights issue, which is increasing share counts by about 30%. This is of course dilutive, and also reflects perhaps a peaking debt capacity, with net debt at around 10x underlying operating profits and cash flows. The need for this outside financing at peak debt capacity reflects the lack of a compounding engine, so some negative market reaction was unsurprising. The return will be lower than the cost on those funds incrementally, but NGG is basically obligated to make improvements. This is all on top of the high pace of asset growth they are currently sustaining, skewed almost entirely to the UK and not the US concession.

CAPEX Mounting (FY 2023 Pres)

These are all negative considerations, and it’s why we aren’t really interested in it at a 13x multiple due to the relatively weak absolute earnings yield, even in the face of guided 6-8% EPS growth even after the rights issue. However, we note that on average, it’s in a much better place than a peer like Redeia (OTCPK:RDEIY). The CNMC in Spain is perennially more difficult than the UK regulators around compensation, and NGG has its US concessions. Yet, Redeia trades at around a 17x PE on a forward basis.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")