A view of a NAPA Auto Parts store exterior and parking lot. M. Suhail/iStock Editorial via Getty Images

As a dividend growth investor, there are many businesses that I appreciate and own. This probably doesn’t come as a shocker to learn.

When somebody researches as many quality dividend stocks as I do, there are bound to be quite a few that stand out in some way. For some businesses, it’s remarkably high profit margins and capital-light business models. Think Visa (V).

For others, it is flawless earnings growth track records in the past 20 years. Think NextEra Energy (NEE). Earnings have compounded by 8.5% annually in the past 20 years due to this earnings growth consistency per FAST Graphs.

Last but not least, we have businesses with exceedingly lengthy dividend growth streaks (e.g., Dividend Kings). Out of all the Dividend Kings, few stand out quite like Genuine Parts Company (NYSE:GPC). The company’s 68-year dividend growth streak is only bested by the 69-year streak of American States Water (AWR).

When I last covered GPC with a hold rating in January, I liked its dividend growth streak, growth prospects, and investment-grade balance sheet. My only hang-up was that GPC’s valuation was a bit excessive to me.

Well, that all has recently changed. GPC’s first-quarter results announced on April 18 demonstrated the operating fundamentals to be sound. The company’s interest coverage ratio remains exceptionally high. As I’ll discuss in a bit, now the shares offer a much better value proposition. Thus, I’m upgrading shares back to a buy.

Starting 2024 With An Earnings Beat And Raised Guidance

GPC Q1 2024 Earnings Press Release

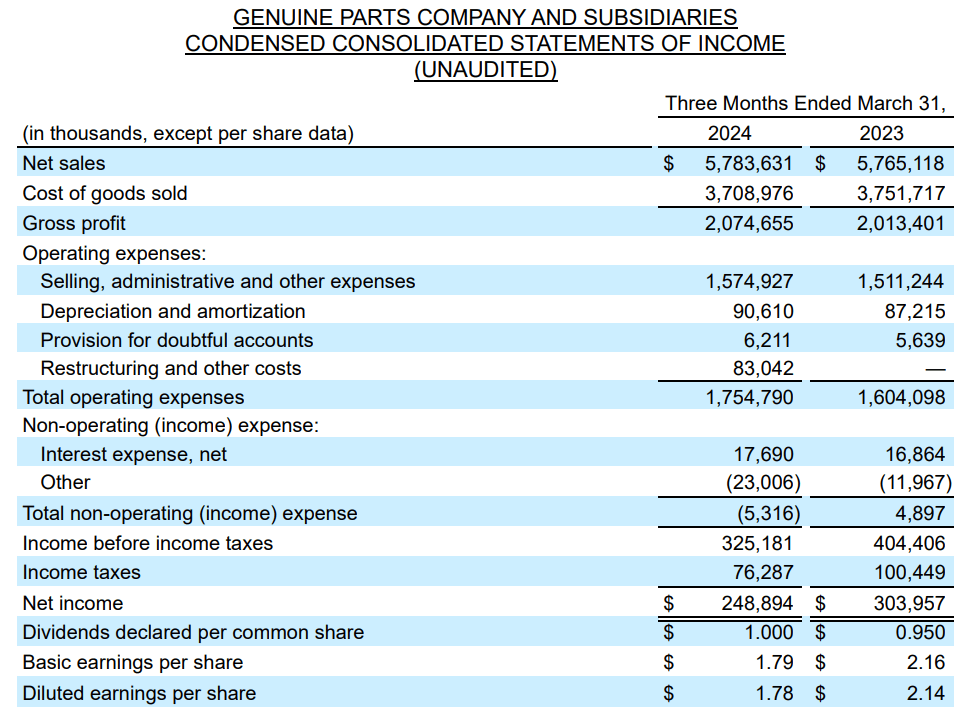

When GPC shared its financial results for the first quarter, it wasted no time getting off to a proper start in 2024. The company’s net sales grew by 0.3% year-over-year to $5.8 billion during the quarter. According to Seeking Alpha, this was $40 million below the analyst consensus.

At first, that may seem to be a bit disappointing. However, it’s worth pointing out that the company’s topline miss can entirely be attributed to international operations. Unfavorable foreign currency translation was a 0.7% headwind to net sales in the first quarter.

GPC’s comparable sales decreased by 0.9% over the year-ago period for the first quarter. The Automotive segment’s comparable sales edged 0.2% higher during the period. That was because, as the average U.S. vehicle age climbed to a record of 12.6 years, consumers invested in repairs to their existing vehicles to keep them on the road.

This was offset by a 2.6% comparable sales decrease in the Industrial segment. According to President and COO Will Stengel’s remarks during the Q1 2024 Earnings Call, this was due to a difficult comparative period. In the year-ago period, sales were up 12%.

GPC’s strategy of bolt-on acquisitions was able to more than counter these headwinds. The company’s strategic acquisitions of 45 NAPA stores from independent owners in the quarter and in the past few quarters largely contributed to a 1.9% bump in net sales.

Moving down to the bottom line, GPC’s adjusted diluted EPS grew by 3.7% year-over-year to $2.22 for the first quarter. That was $0.06 better than the Seeking Alpha consensus.

Disciplined cost management helped the company’s non-GAAP net profit margin to improve by 10 basis points to 5.4% during the quarter. Combined with a 1.1% reduction in the share count via share repurchases, that is how adjusted diluted EPS growth outpaced net sales growth in the quarter.

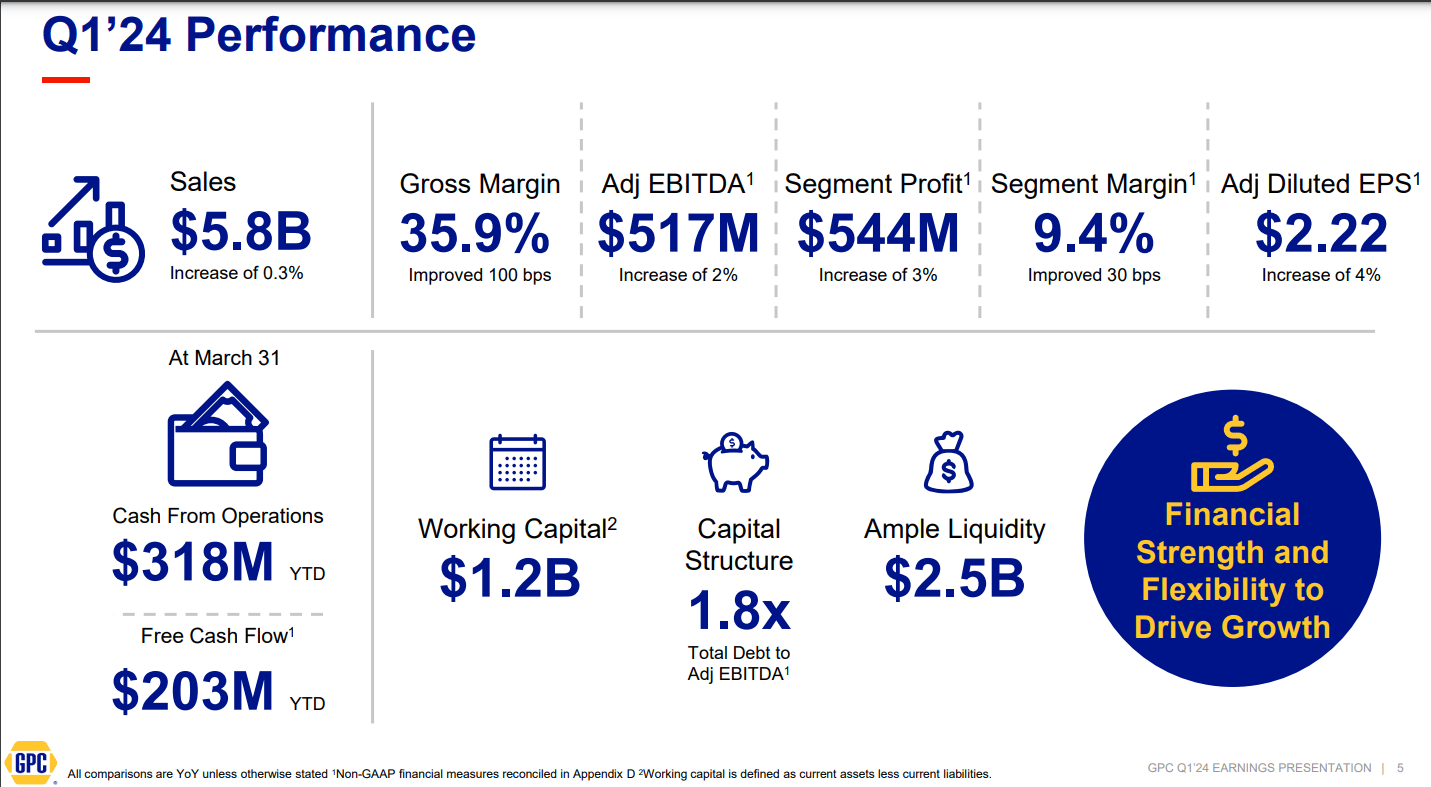

GPC Q1 2024 Earnings Presentation

Thanks to strong first-quarter results, management upped its adjusted diluted EPS guidance for 2024. The previous adjusted diluted EPS midpoint was $9.80 ($9.70 to $9.90) and the updated outlook is for $9.875 in midpoint adjusted diluted EPS ($9.80 to $9.95).

From the $9.33 base for 2023, this would be a 5.8% growth rate. That’s about in line with the $9.90 in adjusted diluted EPS or 6.1% growth rate of the FAST Graphs analyst consensus for 2024.

Beyond this year, the expectation is for adjusted diluted EPS to climb another 9.1% to $10.80 in 2025. For 2026, another 7.7% growth in adjusted diluted EPS to $11.63 is anticipated.

I believe GPC has a clear path to deliver this growth to shareholders. That’s because the company operates in an addressable market that’s $350 billion and growing ($200 billion automotive parts and $150 billion industrial parts).

These markets are consistently growing by between 2% to 3% annually. Keep in mind that GPC tends to execute acquisitions that boost net sales by around 2% annually. Throw in modest margin expansion and share repurchases and this is how I believe high-single-digit annual adjusted EPS growth can persist.

GPC also has the balance sheet to keep completing bolt-on acquisitions to juice its growth. The company’s total debt-to-adjusted EBITDA ratio was 1.8x as of March 31, 2024. This was below the targeted range of between 2x and 2.5x. GPC’s interest coverage ratio was also 19.4 in the first quarter (unless otherwise sourced or hyperlinked, all info in this subhead was according to GPC’s Q1 2024 Earnings Press Release and GPC’s Q1 2024 Earnings Presentation and GPC’s May 2024 Investor Presentation, which can each be downloaded here).

Fair Value Could Be Around $160

FAST Graphs, FactSet

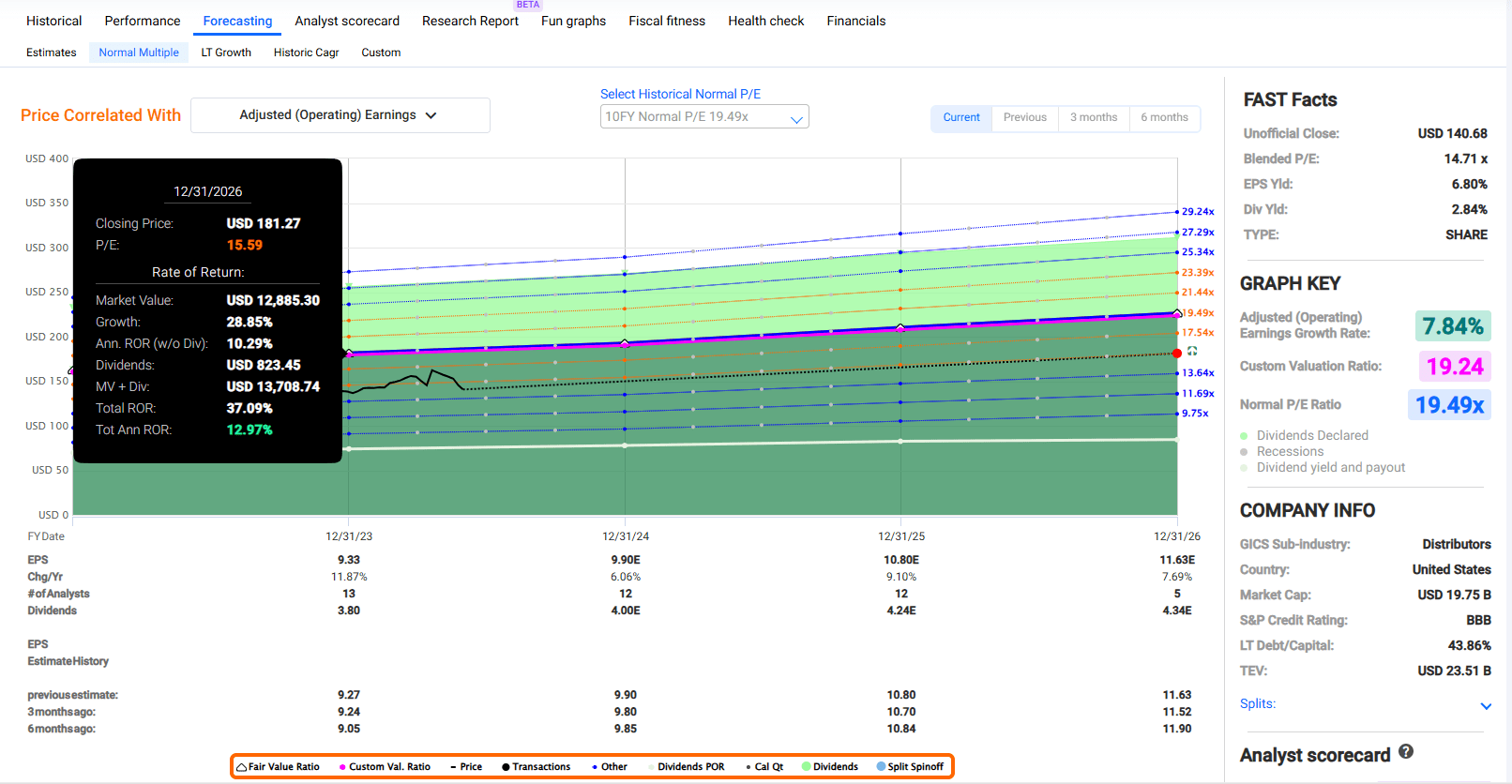

As the S&P 500 index (SP500) has returned 8% in the past four months, shares of GPC are up just 1%. This comes as my fair value estimate is quite a bit higher due to earnings inputs moving from 2023 and 2024 into 2024 and 2025.

GPC’s current-year P/E ratio of 14.6 is well below the 10-year normal P/E ratio of 19.5. To be fair, I don’t think the 10-year normal P/E ratio is a realistic fair value estimate anymore.

That’s because of my expectation that interest rates will remain higher than the 10-year average for at least quite a while. This means GPC no longer has a there is no alternative environment buoying its valuation.

The company’s growth prospects have also cooled a slight bit. The three-year forward annual adjusted diluted EPS growth forecast of 7.8% is just below the 10-year average of 8.1%.

For these reasons, I think a reversion to a valuation multiple two standard deviations lower is reasonable. That would be a multiple of 15.6.

The 2024 calendar year is going to be 42% complete after the current week. I’m thinking about the 58% of 2024 left after this week and the 42% of 2025 ahead in the coming 12 months with my fair value estimate. This is how I’m getting a 12-month forward adjusted diluted EPS input of $10.28.

Plugging that in with a 15.6 fair value multiple, I compute a fair value of $160 a share. This would mean shares of GPC are trading at a 10% discount to fair value from the current $144 share price (as of May 31, 2024). If the company grows as anticipated and returns to fair value, 35%+ cumulative total returns could be posted by the end of 2026.

No End In Sight To Dividend Growth

The Dividend Kings’ Zen Research Terminal

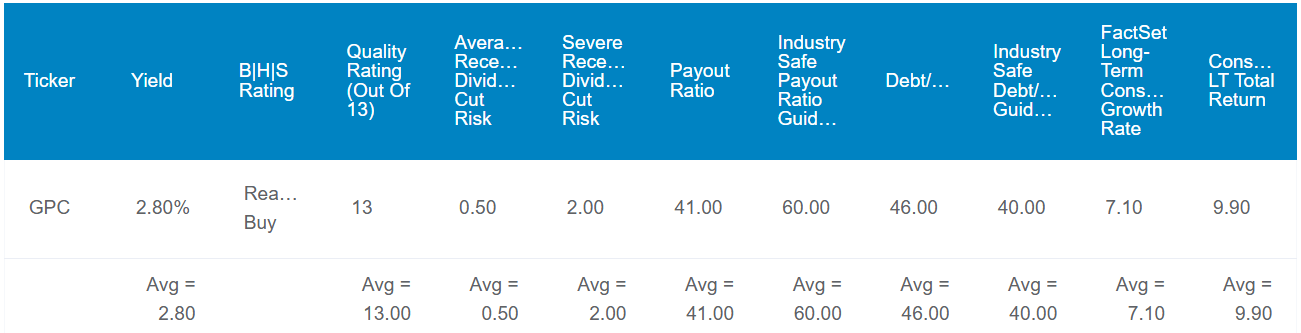

GPC’s 2.8% forward dividend yield registers moderately higher than the 2.1% median forward dividend yield of the industrials sector. This is why Seeking Alpha’s Quant System awards a B grade to the company for forward dividend yield.

Where GPC shines is its dividend consistency. The company’s 68-year dividend growth streak is leagues higher than the sector median of 3 years. This handily earns an A+ grade for that metric from the Quant System.

Moving forward, I believe dividend growth should be around 6% annually. This is because GPC’s 41% EPS payout ratio is well below the 60% that rating agencies like to see from the industry. That leaves the company with a buffer to keep raising the dividend, completing bolt-on acquisitions, and executing share repurchases.

Risks To Consider

For a “boring” business, GPC is firing on all cylinders. Yet, it still has risks that must be contemplated and occasionally monitored.

GPC operates in large and fragmented addressable markets. That means that it will have to keep providing customers with a mix of value and quality service to maintain its market share. If GPC can’t do so, plenty of other competitors will likely step in and swipe away market share. That could impair the company’s growth potential.

GPC also depends on suppliers to sell products at favorable prices. If these suppliers encountered supply chain interruptions, products could be in short supply. Prices could also be much higher. If GPC can’t pass on higher prices to customers, its profit margins could suffer. The balancing act is that the company must also consider its competition to avoid deterring customers with excessive prices.

Finally, GPC’s Industrial segment is sensitive to economic ebb and flow. If a recession materialized, temporary challenges in this segment could weigh on growth potential.

Summary: An Excellent Dividend Growth Stock On Sale

GPC’s 0.7% weighting within my portfolio leaves me with room to boost my position. The company is doing well fundamentally, and the valuation is becoming appealing. So, I am upgrading back to a buy rating. I am also weighing adding to my position in the coming weeks.

Q2 2024 Earnings Call Transcript")