Luis Alvarez

Investment Thesis

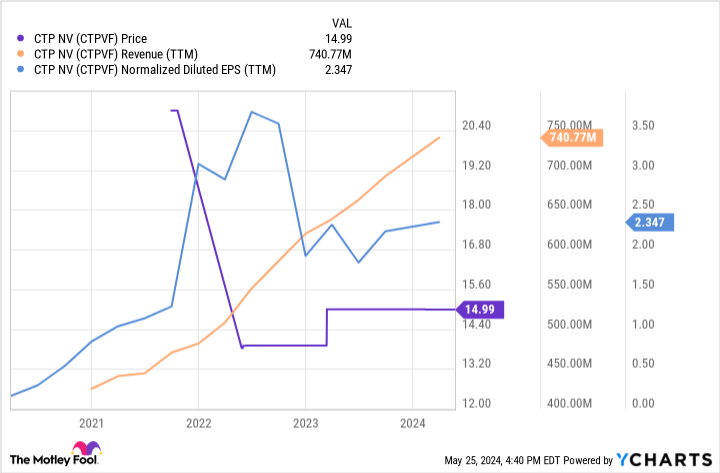

Since its IPO in 2021, the CTP N.V. (OTC:CTPVF) (AMS:CTPNV) share price has not changed a lot. I believe the company is still relatively undiscovered by the broad investor audience, and once it becomes known, the company’s shares may experience a significant rally.

YCharts

Corporate Profile

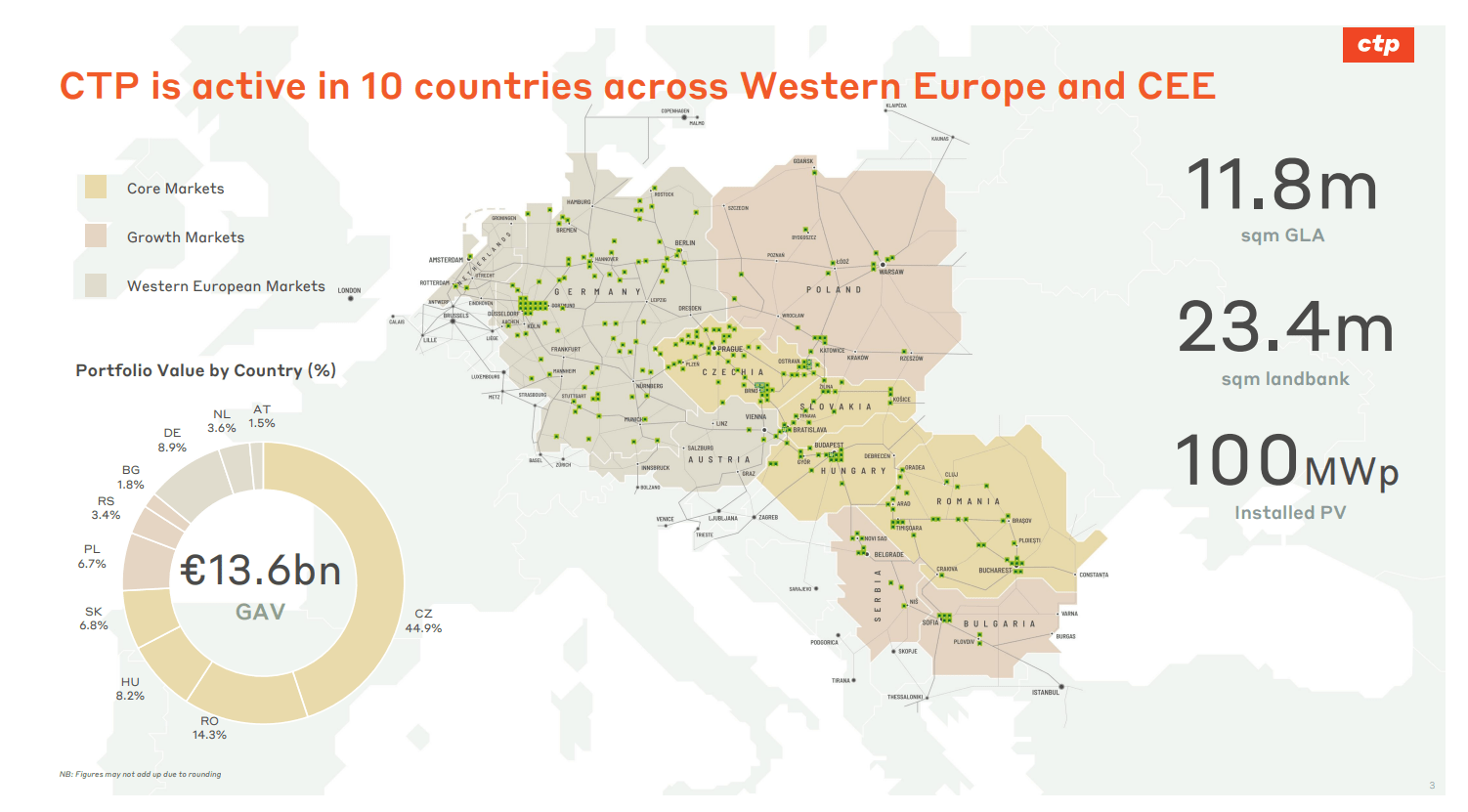

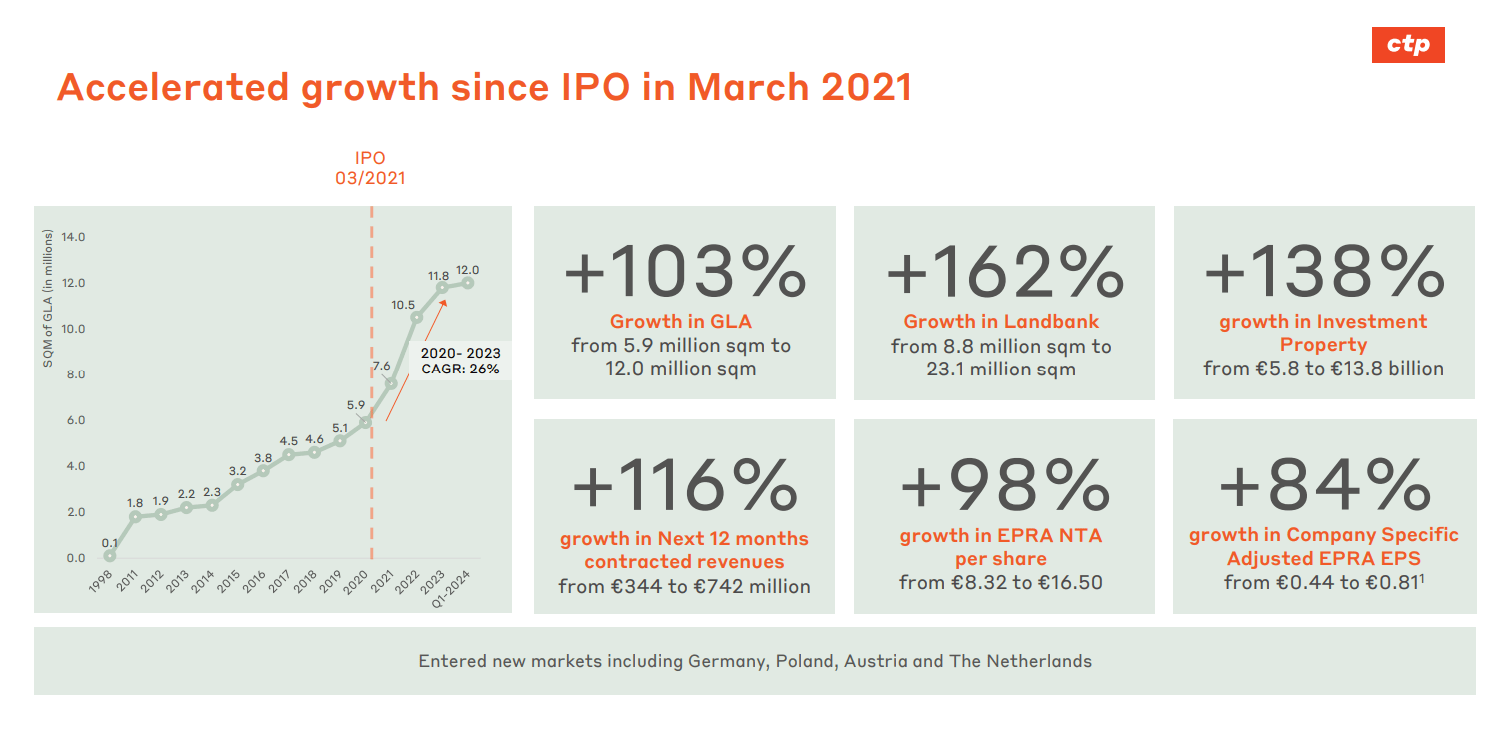

CTP is a leading European industrial property developer and operator, specializing in the development and management of high-quality business parks. Headquartered in the Netherlands, CTP operates an extensive portfolio of logistics and industrial properties across key locations in Central and Eastern Europe, including the Czech Republic, Slovakia, Hungary, Romania, Serbia, and Poland. CTP’s integrated approach encompasses the entire property lifecycle, from site acquisition and development to long-term ownership and management, ensuring consistent quality and performance. With a commitment to sustainability, CTP aims to minimize environmental impact through innovative building practices and energy-efficient solutions, positioning itself as a responsible and forward-thinking leader in the real estate sector. As of recent years, CTP has seen robust growth, driven by strong demand for industrial space and strategic expansions into new markets.

CTP’s latest earnings presentation CTP’s latest earnings presentation

Financial Analysis

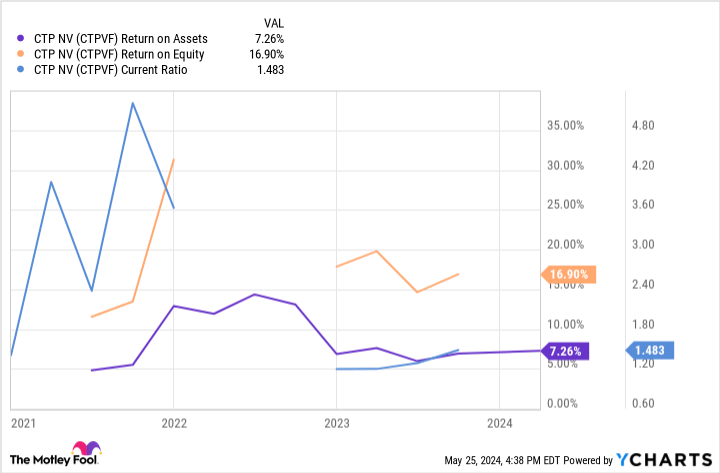

Regarding financial statements, the company’s balance sheet has a healthy amount of debt (long-term loan-to-value ratio of 45-50%) which helps to translate an ordinary level of 7% ROA into an extraordinary almost 17% ROE. Finally, the company has sufficient liquidity, with the current ratio hovering above 1.4 level.

Looking at individual years, CTP’s financial position was even better earlier in 2022. Since then, it has slightly deteriorated, but it is more likely that this trend is over rather than ongoing. The company also has a superior EBIT margin, currently of 65 percent, which has followed more or less the same dynamic over the past few years but does not seem to be about to dramatically rise or fall in the upcoming years as well.

YCharts

Catalyst On The Horizon

Even though analysts now expect a “higher for longer” interest rate policy, it seems to be a question of time before interest rates go down once again and that could be a macro catalyst for stocks and CTP as well. The impact of lower rates on the DCF model is clear, so no need for further explanation.

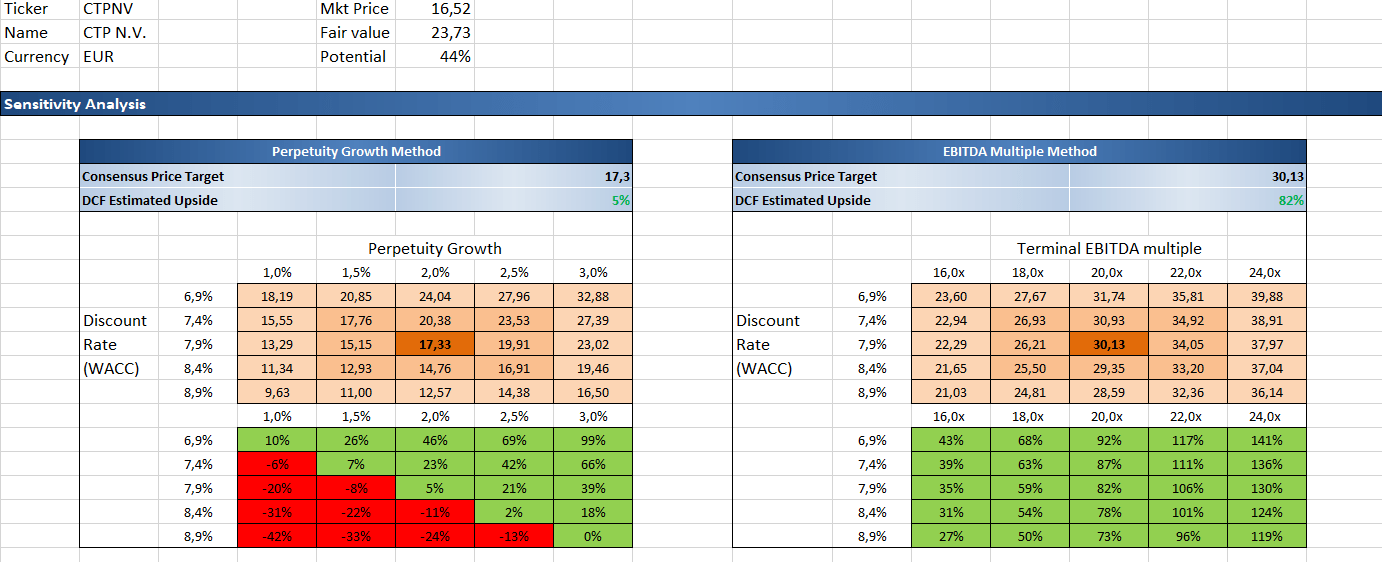

DCF Analysis

Plugging in CTP’s financial statement figures into my discounted cash flow (“DCF”) template, the company’s shares show to be undervalued. Under the perpetuity growth method with a terminal growth rate of 2 percent, 23 percent annual revenue growth gradually decreasing by 1 percent over the next five years, and a stable operating income margin of 65 percent assumption, the model’s estimate of the intrinsic value of the stock comes at 17.3 EUR. Under the EBITDA multiple approach of a discounted cash flow model, the intrinsic value per share of the company stands roughly at 30 EUR if we assume that the appropriate exit EV/EBITDA multiple in five years’ time is around 20x.

Of course, the DCF model is just an estimation of the intrinsic value of the company’s shares and greatly depends on the analysis inputs. The rationale behind my terminal growth rate figure is an expectation that the economy to grow at 2 percent indefinitely. The revenue growth figures are simply a linear extrapolation of revenues’ current growth pace and the 65 percent operating margin assumption is based on being an average of the margin’s percentages over the past few years, assuming it stays flattish in the foreseeable future.

Author’s own model

Key Risks

Investing in CTP shares entails several key risks that potential investors should be aware of. Firstly, fluctuations in the real estate market can affect the company’s property values and rental income. Economic downturns or changes in market demand can lead to decreased occupancy rates and rental prices, impacting CTP’s revenue and profitability. Additionally, regulatory risk is pertinent, given that changes in local or international property laws, environmental regulations, or tax policies can adversely affect CTP’s operations and financial performance.

To a certain extent, the company also faces liquidity risk, as real estate investments can be relatively illiquid, potentially complicating the process of selling properties or shares quickly without substantial loss in value. Furthermore, interest rate risk is notable, as increases in interest rates can raise the cost of borrowing and reduce the attractiveness of real estate investments. Lastly, operational risks, including management effectiveness, property maintenance issues, and the ability to secure and retain tenants, can all influence the company’s success and, consequently, the performance of its shares.

CTP’s latest earnings presentation

The Bottom Line

To sum up, CTP N.V. is a typical example of a smartly indebted company with a very low cost of debt (only around 2 percent), helping to minimize the weighted average cost of capital and maximize overall return on shareholders’ equity. The company has a strong and diversified international client base, minimizing individual counterparty risk exposure, and a high occupancy rate of above 90 percent. With a trailing-twelve-months price-to-earnings ratio of just 8 and price-to-book of 1.1, CTP N.V. stock trades with an attractive valuation, with its shares ready to soar.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")