It was one of the more bizarre claims in a list of demands issued to Keir Starmer by a fringe Muslim group, which earlier this month threatened to stand against Labour MPs at the General Election.

Pro-Gaza activist group the Muslim Vote handed the opposition leader an extraordinary list of 18 demands at the beginning of May, which it claimed he must agree to carry out to win the support of the four million Muslim voters in the UK.

Included in this list was that Sir Keir ensure that people with the name Muhammad do not pay more for insurance than others just by virtue of their first name.

For years it has been widely known that insurance customers are quoted differently based on various factors, including their age, postcode and medical history.

Insurance companies have taken these personal details into consideration when calculating premiums, using them as tools to assess the risk they run in providing a policy.

Mo Money? The Muslim Vote group are demanding Labour leader Kier Starmer ensures men called Muhammad do not pay more for insurance than others

But can it really be true that a person’s first name can influence how much they are charged?

Money Mail investigated and put the claim to the test to see whether two people with identical details – living at the same address, with the same car and job – but with different first names would be quoted different premiums for the same level of car insurance cover.

We found that, contrary to the Muslim Vote’s claim, people with the name Muhammad pay the same as those with other common names – and, surprisingly, in many instances, less on their car insurance than people with the name John.

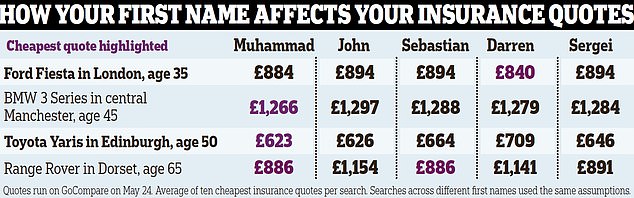

Across the dozens of quotes we ran on price comparison website GoCompare, someone called John Smith typically paid marginally more than someone with the name Muhammad Smith.

We used identical details in our searches across four different scenarios, changing just the first name. The first names we used were Muhammad, John, Sebastian, Darren and Sergei.

In the most shocking example, Muhammad was charged £553.89 less than John and Darren for the same level of cover.

When 65-year-old Muhammad Smith, who lived in Dorset, requested a quote for cover on his Range Rover, he was charged around a third less than John Smith on five of the ten cheapest quotes.

In another test, we ran a search for a 35-year-old man with a Ford Fiesta, working as an IT consultant and living in Hammersmith, in west London.

Of the top ten cheapest quotes on comparison website GoCompare, seven were cheaper for Muhammad than John, while two charged the same and just one was more expensive. Meanwhile, John was quoted the same levels as Sebastian and Sergei.

Sometimes running multiple searches from the same computer can raise fraud alerts, however, Money Mail ran the name searches in random order to ensure that there was no bias. GoCompare was contacted for comment.

On comparison site MoneySuperMarket, John Smith and Muhammad Smith were quoted the same premiums in most of our searches.

However, in one case, 35-year-old Muhammad, who drives a Ford Fiesta in Hammersmith, was charged £188 less than John. A spokesman for MoneySuperMarket says: ‘We are a price comparison site that collects customer information.

Results: Of the top 10 cheapest quotes on GoCompare, seven were cheaper for Muhammad than John, while two charged the same premium and just one was more expensive

‘This information is shared with insurers who use their own pricing models to calculate insurance premiums. The pricing models insurers use are commercially sensitive and typically include information like location, the type of car and driving history.’

Mark Wilkinson, managing director at Norton Insurance Brokers, says that using first names to calculate a premium could be classed as discriminatory.

He adds: ‘I have been in the industry for over 20 years and I have never come across any occasion where someone’s first name has been called into question for a quote. We deal with all nationalities and it just isn’t a thing – everyone is treated equally no matter their first name.’

However, he suggests that the areas where people with the name Muhammad live could have a bearing.

‘What I think could be happening is it might be a case that certain areas where people with the name or a certain ethnicity live might have a higher claims frequency.

‘So rather than their name having an effect, it is their home address and insurers might be charging more because of that. The name might be a consequence rather than the cause.’

When working out a quote, insurance companies use details about you, your vehicle and how you drive. Your personal information is used to predict how likely you are to make a claim, and therefore how much they will charge you for cover.

Personal details: For years it has been widely known that insurance customers are quoted differently based on various factors, including their age, postcode and medical history

According to insurer the RAC, living in a built-up area will increase your chance of accidents through sheer probability, as there will be more vehicles on the road.

It says: ‘If you live in an area with a high crime rate, you could see the added risk to your car reflected in your premium since vandalism and theft may be more common.’

The weather in your area might also play a role. For example, if you live on the coast or near a river prone to flooding your insurance payments will consider the cost of potential water damage.

Frontrunner: Activist group the Muslim Vote handed Kier Starmer an extraordinary list of 18 demands

Similarly, your occupation will play into your final premium, the RAC says. ‘Occupations associated with high stress levels are considered a “higher risk”, so while a senior position may indicate responsibility, some insurance providers may charge high-powered professionals a costlier insurance premium.’ Jobs that involve a lot of driving will also typically push charges higher.

Price comparison website Comparethemarket says that even similar job titles can result in different premiums. For example, construction worker and bricklayer, or chef and kitchen staff.

It says: ‘If your job title fits in more than one category, it might be worth checking quotes for all of them. But remember the details you give should be as accurate as possible and not misleading, otherwise you could invalidate your policy.’

A spokesman for the Association of British Insurers says: ‘Insurers will consider a wide range of risk-related factors when calculating the price of a car insurance policy, such as age, driver experience and type of vehicle.

‘First and last names themselves are not used as a rating factor, but an individual’s full name may be cross-referenced against other databases to understand their driving record or claims history. Insurers do not and cannot use ethnicity as a factor when setting prices and our members comply with the Equality Act 2010.’

City watchdog the Financial Conduct Authority says it wrote to insurers last year ‘making clear that they must assure themselves that their pricing is not discriminatory in line with the Equality Act 2010’.

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")