Paper Boat Creative/DigitalVision via Getty Images

The iShares Micro-Cap ETF (NYSEARCA:IWC) offers diversified exposure to the smallest U.S. publicly traded companies. The attraction from this segment of stocks is that some hidden gem can emerge as “the next big thing” with potentially significant returns over the long run.

While that may be true, it appears the idea doesn’t quite work in this ETF structure. The challenge is that the best micro-caps ultimately grow out of the fund, leaving behind a collection of fundamentally weaker companies.

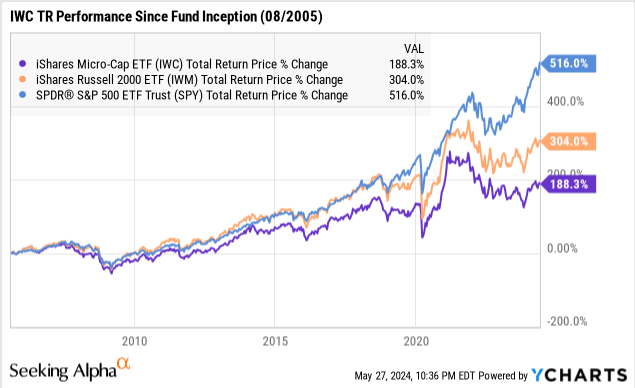

Indeed, IWC has lagged the return from broad-market indexes going back nearly two decades, also underperforming the small-cap focused iShares Russell 2000 ETF (IWM). Here’s what you need to know.

What is the IWC ETF?

IWC is intended to track the “Russell Microcap Index” which consists of the smallest 1,000 companies within the Russell 2000 Index, plus the next 1,000 smallest eligible securities by market cap.

The median micro-cap index company has a market cap of just $213 million, which is under the $300 million threshold where “small-caps” are normally classified. The index and fund are reconstituted annually by each stock’s float-adjusted market capitalization weighting.

A key point is that IWC utilizes a sampling indexing strategy which means it doesn’t hold all 2000 micro-cap stocks, but instead has a current portfolio with 1,468 names that are expected to closely represent the index return and risk profile.

That also includes companies that are not technically micro-caps, but fit within the investing mandate that allows for up to 20% of the overall exposure in stocks that have similar economic characteristics that are substantially identical to the index constituents. This is important in the world of micro-caps because some of the stocks are simply too small for IWC to take a meaningful position

IWC Portfolio

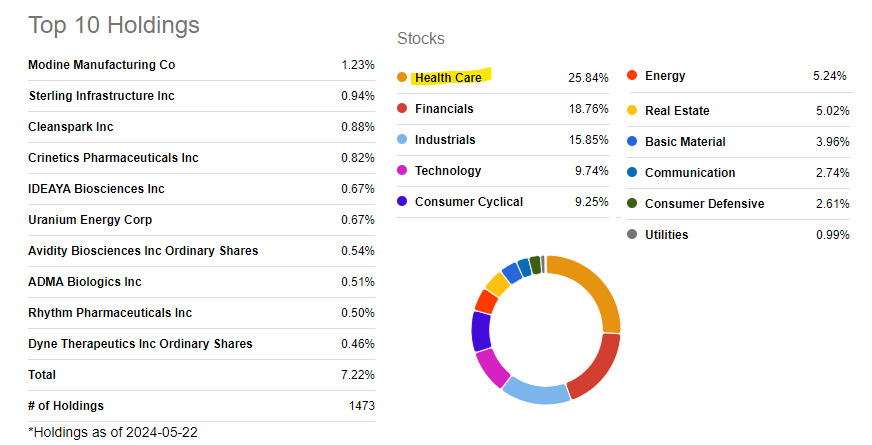

Going through the IWC portfolio, we find an eclectic group of established companies and some obscure names. Modine Manufacturing Co (MOD) is the current largest holding with a 1.2% weighting, followed by Sterling Infrastructure, Inc. (STRL).

Shares of MOD are up more than 420% over the past year, benefiting from strong demand for its data-center cooling solutions within AI infrastructure. STRL has a similar story as a construction and engineering provider that has specialized in building data centers. STRL is up 44% in 2024.

Naturally, the best-performing stocks will gain relative importance within the fund as their weighting contribution climbs. This comes at the expense of the decliners.

We mentioned IWC holds stocks that are not technically micro-caps. In this case, MOD with a market cap of $5.4 billion, and STRL valued a $3.9 billion are already in “mid-cap” territory, which means they will likely fall out of the IWC portfolio at the next reconstitution.

Seeking Alpha

IWC Performance

Given the overall size of the IWC portfolio where the top-10 holdings represent just 7% of the total weighting, the performance of a single stock ends up dominated by the bigger themes facing the micro-cap segment.

What stands out to us is the exposure to the Health Care sector, currently representing 26% of the fund. Within the world of micro-caps, the bulk of the companies are biotech names, which are recognized as highly volatile and speculative on their own.

In many cases, micro-cap biotechs are simply in the development stage of a commercialization strategy with limited or no revenues. While some survive, recurring losses and dilutive financing are common themes that keep the group under pressure absent a blockbuster drug approval.

The same can be said with micro-cap Financials sector holdings that represent 19% of the fund. In this case, the numerous tiny regional banks are a tough bet eyeing the lingering fallout from the short-lived 2023 banking crisis that saw several institutions go under.

In our view, micro-cap stocks are at a structural disadvantage against large-cap leaders, who often have more competitive resources and stronger fundamentals.

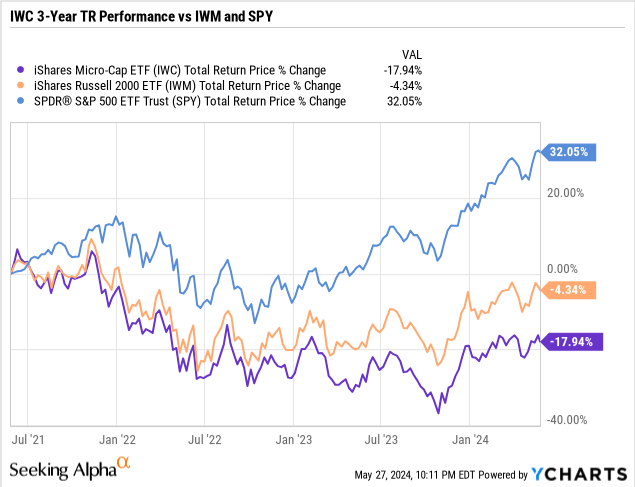

Over the past three years, IWC has lost about 18% which is a major spread compared to the 32% gain from the SPDR S&P 500 ETF Trust (SPY). Investors holding IWM haven’t fared much better, with the small-cap fund still down 4% over the same period.

Another factor explaining IWC’s weakness is also its limited Technology sector holdings, at just under 10% of the fund. Overall, it’s a tough segment to get excited about.

What’s Next for IWC?

There is a thought that micro-caps could lead higher during the next phase of the equity bull market.

One scenario for IWC is that the U.S. economy remains resilient, and a path for interest rates to pull back, opens the door for more positive risk sentiment toward the riskiest types of investments. Highly leveraged companies, or those with poor fundamentals, stand to benefit as credit conditions improve.

Still, we’d say that the number of shortcomings in IWC would keep it from significantly outperforming to the upside. The best micro-caps move on to bigger classifications, leaving the fund with lower-quality leftovers.

If there is a good reason to buy IWC, it would be its diversification properties, considering it holds companies not found in most other index funds. Still, the iShares Russell 2000 ETF (IWM) is likely a better middle ground that has a better chance of converging toward S&P 500 returns.

On the downside, the bearish case for IWC is that economic and market conditions deteriorate from here going forward. A setback in the inflationary outlook or the possibility that interest rates need to climb would add significant volatility to the stock market’s smallest and most vulnerable companies. We expect that IWC will underperform to the downside in the next market correction.

Final Thoughts

Micro-cap stocks represent an overlooked but important corner of the market. Unfortunately, IWC with the passive indexing strategy fails to deliver a compelling investing vehicle. We suggest readers avoid this fund.

Q2 2024 Earnings Call Transcript")