jetcityimage

Introduction

I recently wrote an article titled “The Tractor Supply Company + Real Estate Combo: A Recipe For Superior Returns.”

In that article, I did two things:

- I explained what makes the Tractor Supply Company (TSCO) just a fascinating consumer dividend growth stock.

- Because the company has a strategy of selling real estate to fund growth (sale-leaseback deals), I showed a model portfolio consisting of TSCO and one of its landlords, which turned out to deliver elevated income, consistent dividend growth, and a highly favorable risk/reward profile.

Based on this, I thought about Dollar General (NYSE:DG).

My most recent article covering this dollar store was written on January 9, titled “The Bull Case For Dollar General To Return >9% Per Year.“

Since then, DG has returned 9%, lagging the S&P 500 by roughly 200 basis points.

Today, I’m revisiting the company for a number of reasons, including my bigger focus on its real estate.

Over the past months, I’ve spent a lot of time looking for physical net lease real estate deals – inspired by major REITs like Realty Income (O).

Bear in mind that this was mainly educative. As I’m not based in the U.S. – at least not yet – I won’t be able to invest in physical real estate.

I’m bringing this up because Dollar General is a highly attractive tenant. The internet is filled with single-tenant net lease deals with Dollar General as a tenant – like the one below (just an example, not advertising).

LoopNet

In this article, I’ll focus on both Dollar General and its real estate, as I believe it’s a fascinating company that offers more than one way for investors to make money.

So, let’s get to it!

Dollar General Is Becoming Critical Real Estate

The other day, I was watching a fascinating documentary about “neglected” communities in Mississippi.

One of the people who was interviewed said he wished a Dollar General would open in his town.

Generally speaking, he’s not the only one who has this thought, as Dollar General brings low-cost merchandise and food items to often underserved communities, which tends to add a lot of value for many people – especially in times of elevated inflation.

Two years ago, CNN reported that due to inflation, the target audience of Dollar General is rapidly expanding.

Dollar General CEO Todd Vasos this week said the retail giant has been attracting customers earning $100,000 a year in recent weeks. Inflation has pushed up prices for groceries and gas, and now these shoppers are turning to Dollar General and others to try to save money. – CNN (2022)

Based on this context, last month, The Wall Street Journal published a fascinating article on these trends last month.

The Wall Street Journal

According to the article, Dollar General and its peer, Dollar Tree (DLTR), are moving in opposite directions.

- Dollar General, which has a focus on rural areas, is expecting to open about 800 new stores this year.

- Dollar Tree, which focuses on urban and suburban areas, is expected to close 600 Family Dollar stores.

The rural focus also comes with cost savings. As reported by the article, the real-estate costs of Dollar General are roughly a third lower.

That said, this isn’t supposed to be a comparison.

What matters is that dollar stores, in general, are increasingly becoming an important part of U.S. retail.

Dollar stores have powered the U.S.’s recent retail expansion, comprising more than a quarter of the U.S.’s total store openings in 2022 and last year, according to Coresight Research. Dollar General operates 20,000 stores in the U.S., up from 5,000 in 2001. Walmart, by contrast, has just over 4,600 locations.

Dollar General and Family Dollar both target the lower-income consumer and sell items such as dish towels, shampoo, dog food and laundry detergent, said Jonathan Hipp, principal, U.S. Capital Markets and head of the U.S. Net Lease Group for real-estate firm Avison Young. – WSJ (emphasis added)

Interestingly enough, one major thing that set Dollar General apart was its real estate.

While other dollar stores spent a lot of time keeping costs low (sometimes leading to “beat-up” stores), Dollar General built a great footprint of locations in attractive areas.

That’s also why so many Dollar General real estate deals are quite attractive.

Investors often get relatively new buildings with solid tenants in areas with increasing demand for low-cost products.

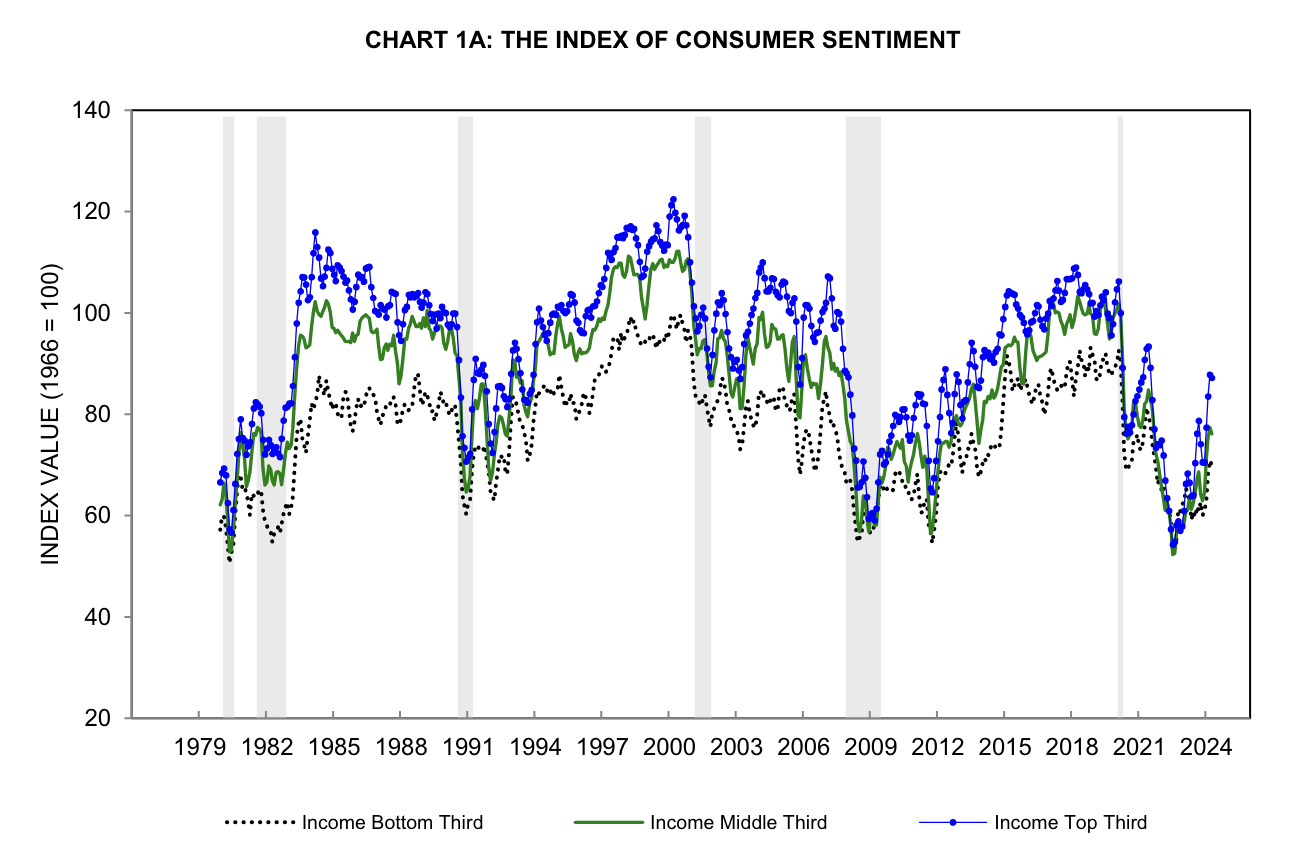

After all, while consumer sentiment has rebounded, the sentiment of lower-income consumers remains at depressing levels.

University of Michigan

Ironically, while Dollar General benefits from new customers, it’s a tough environment to operate in when your “usual” customers are pressured by economic challenges.

During its 4Q23 earnings call, the company noted it executed over 3,000 real estate projects in 2023, including opening 987 new stores, relocating 129 stores, and remodeling more than 2,000 stores.

On top of that, during the fourth quarter, the company reported same-store sales growth of 0.7%, driven by a 4% increase in customer traffic.

According to the company, this foot traffic improvement was a result of brand strength and customer loyalty.

Even more important, the company grew its market share in both consumables and non-consumables.

As discussed by The Wall Street Journal, the company confirmed it has an edge over a lot of peers, which it is expanding by adding cooler doors to many stores and expanding the availability of fresh produce and related products.

The company is also growing through a new store concept called pOpshelf, which is a non-consumable store offering more upscale items that allow Dollar General to better align its offerings with market conditions – despite current pressure on non-consumables (due to high inflation).

pOpshelf

In general, DG believes its ability to adapt to changing consumer preferences – coupled with a real estate network with a store within five miles of 75% of the U.S. population, puts it in a great spot to generate substantial shareholder value.

With that said, on May 30, the company will release its 1Q24 earnings. While it’s hard to say what the company will comment on regarding consumer strength, it will be interesting to see if the company changes its guidance.

For now, this is what DG expects for FY2024:

- Net sales growth between 6.0-6.7%

- Same-store sales between 2.0-2.7%.

- Diluted EPS between $6.80 and $7.55.

If the company is able to show that its core customers are capable of providing it with consistent revenue growth with support from a bigger target audience, I expect shares to do very well.

Two Top-Tier Dollar General Landlords

So, who are its landlords?

One of its largest landlords is Realty Income, which is one of the largest net-lease REITs in the world.

The company has a 6% yield and hiked its monthly dividend for 30 consecutive years (4.3% CAGR).

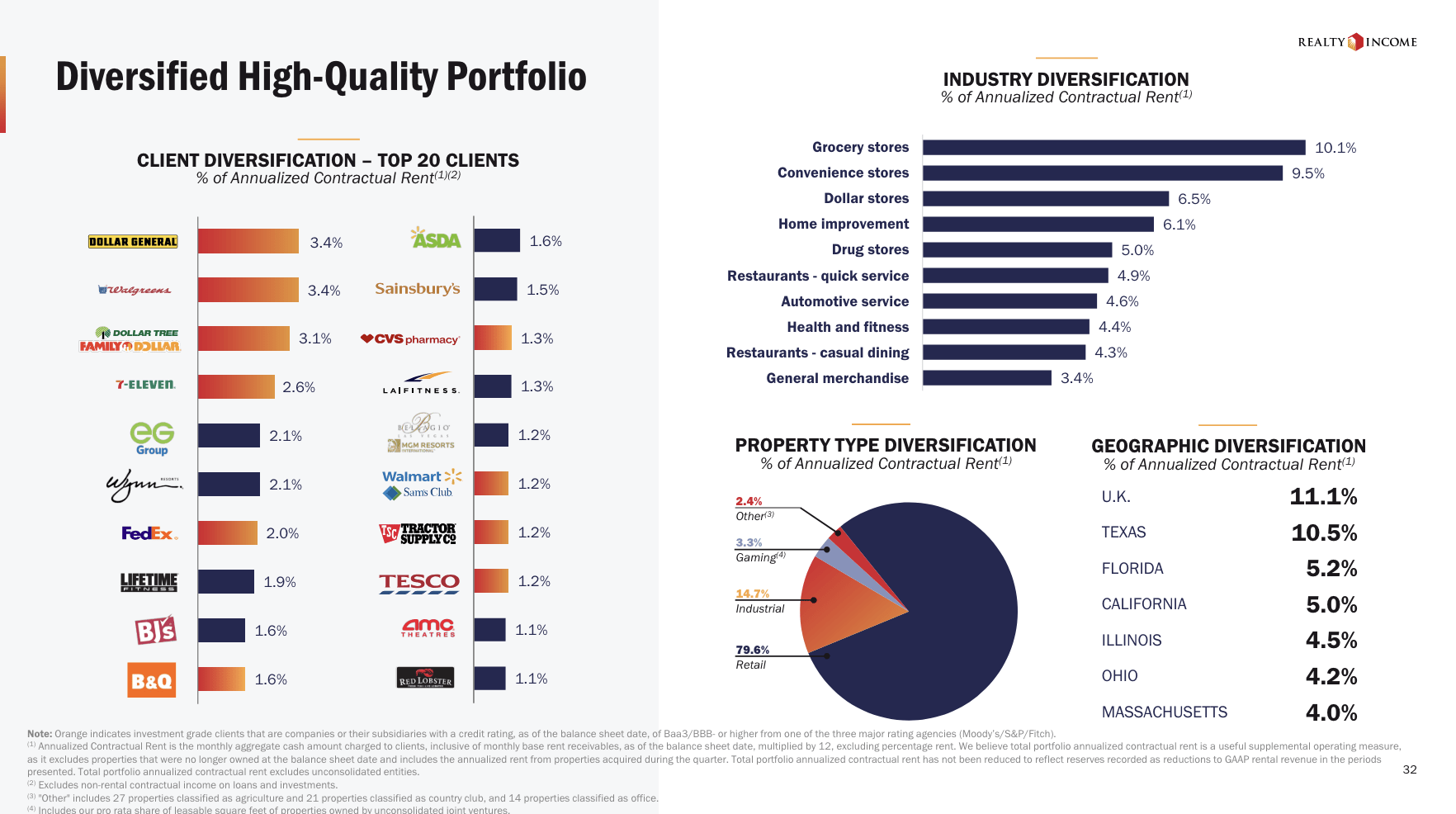

Going into this year, it owned 1,659 Dollar General stores, accounting for 3.8% of its total portfolio rent. This makes DG its largest tenant.

In general, it has a very defensive tenant base consisting of grocery stores, convenience stores, dollar stores, home improvement giants, drug stores, and others.

Realty Income

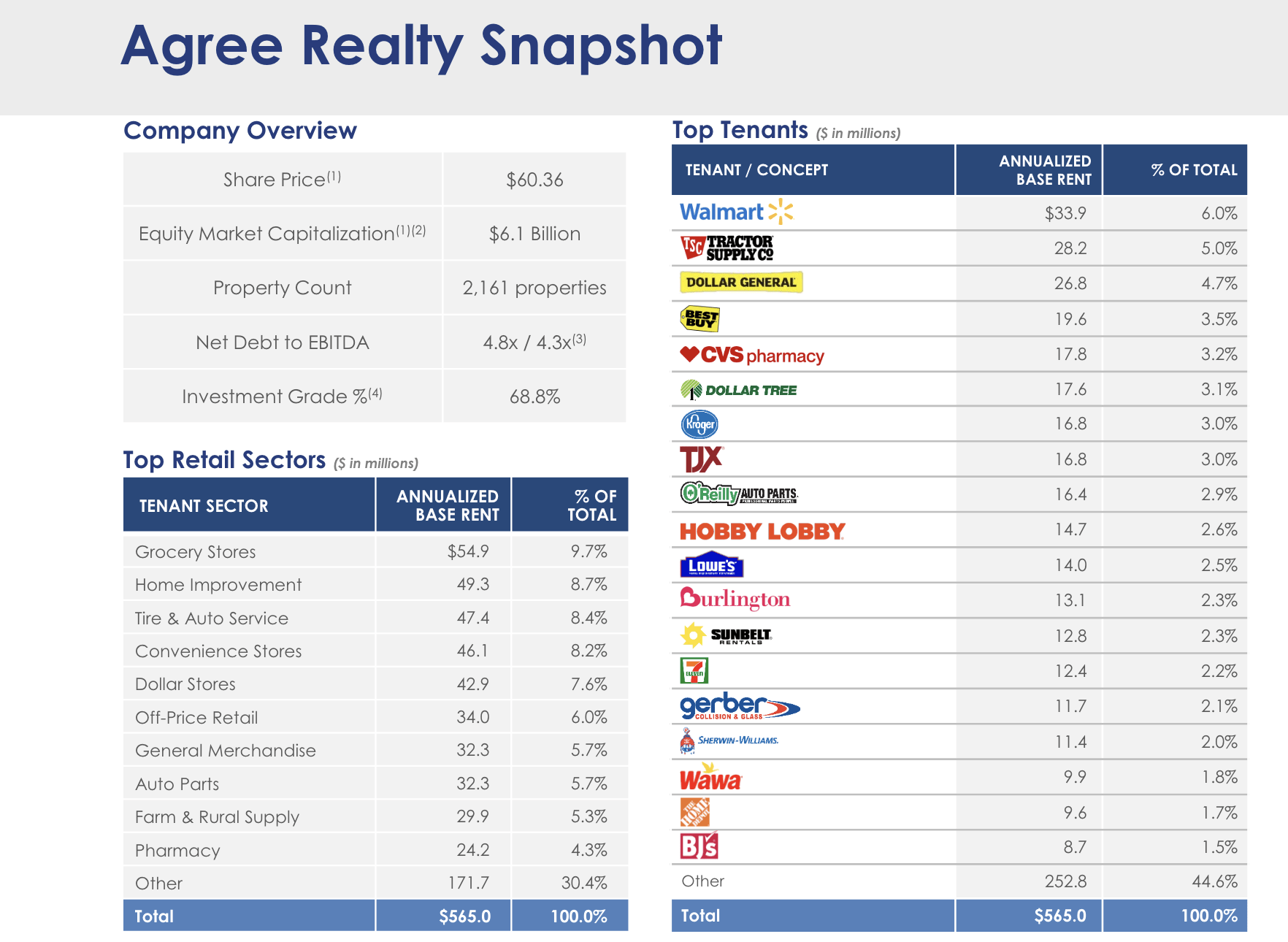

The second company that comes to mind is Agree Realty (ADC), the smaller net lease peer of Realty Income.

As of May 14, it generates 4.7% of its annual rent from Dollar General stores. In fact, 69% of its tenants are investment-grade tenants, which is unique in its industry. I’m fairly sure that most readers will be familiar with most of the company’s largest tenants.

Agree Realty

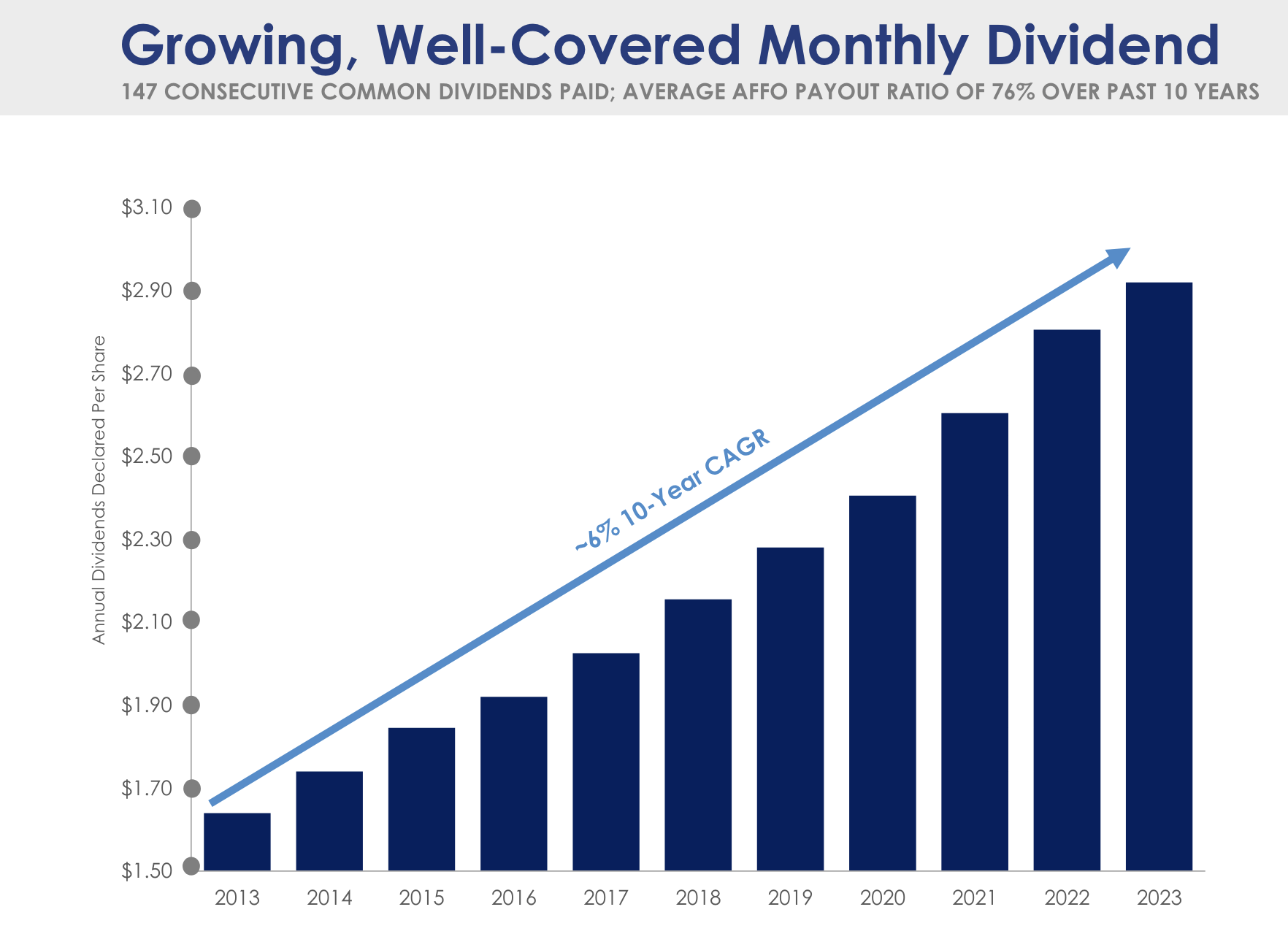

As I wrote in the TSCO article, Agree Realty brings a unique mix of value and growth to the table, as it has fantastic tenants, an investment-grade balance sheet, and a 5.1% dividend that comes with a 10-year CAGR of 6%.

Agree Realty

Building Value With DG (And Landlords?)

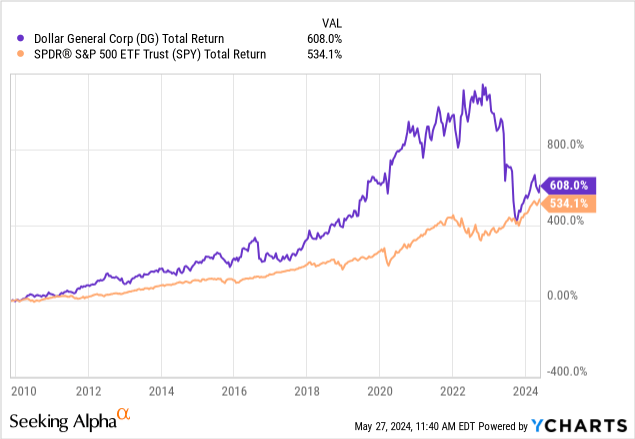

Despite its recent stock price weakness, DG shares have returned 608% since the 2009 IPO, beating the S&P 500 by a substantial margin.

This performance includes its dividend.

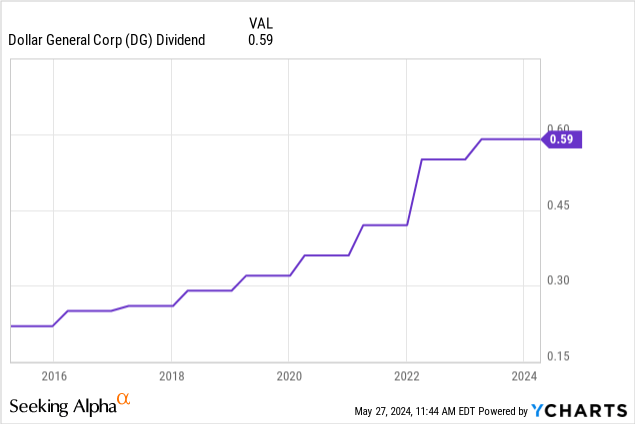

Currently, Dollar General yields 1.6%.

This yield is protected by a 31% payout ratio, an investment-grade BBB credit rating, and comes with a 14.7% five-year CAGR.

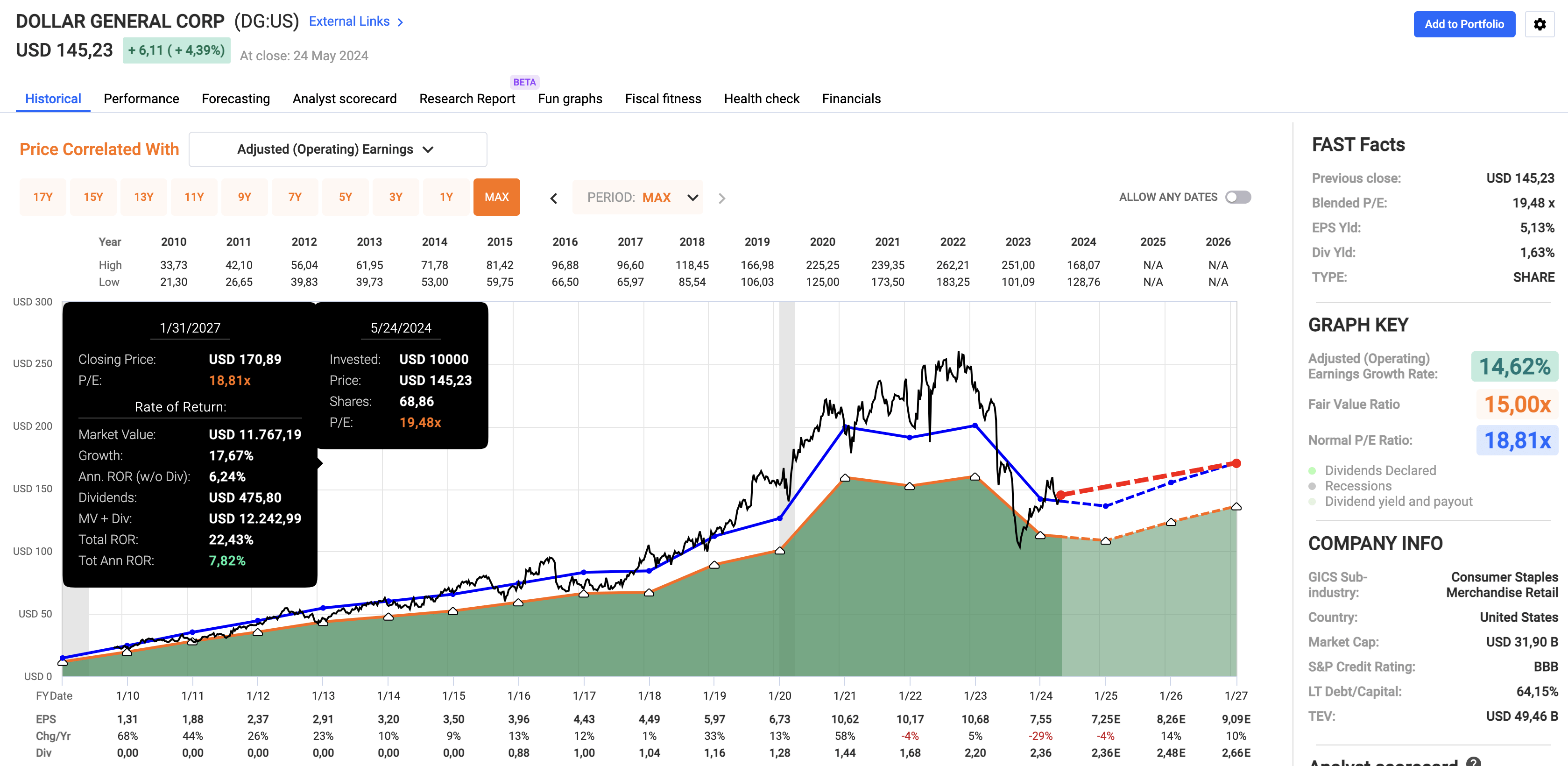

With that said, DG is also attractively valued, trading at a blended P/E ratio of roughly 19.5x.

Using the FactSet data in the chart below, 2024 is expected to see 4% lower EPS.

However, analysts expect double-digit growth in the years after 2024, which, using its 18.8x normalized P/E ratio, translates to a fair stock price of roughly $171, 18% above the current price.

FAST Graphs

With that said, I like Dollar General. I think it’s a consumer dividend growth stock with a bright future.

However, if I were to buy DG, I would likely combine it with one of its landlords, as I would like to own the real estate as well.

In this case, the only REITs I like for this idea are Agree Realty and Realty Income. Both have significant DG exposure and overall fantastic business fundamentals that make for great individual investments.

That’s where the data below comes in.

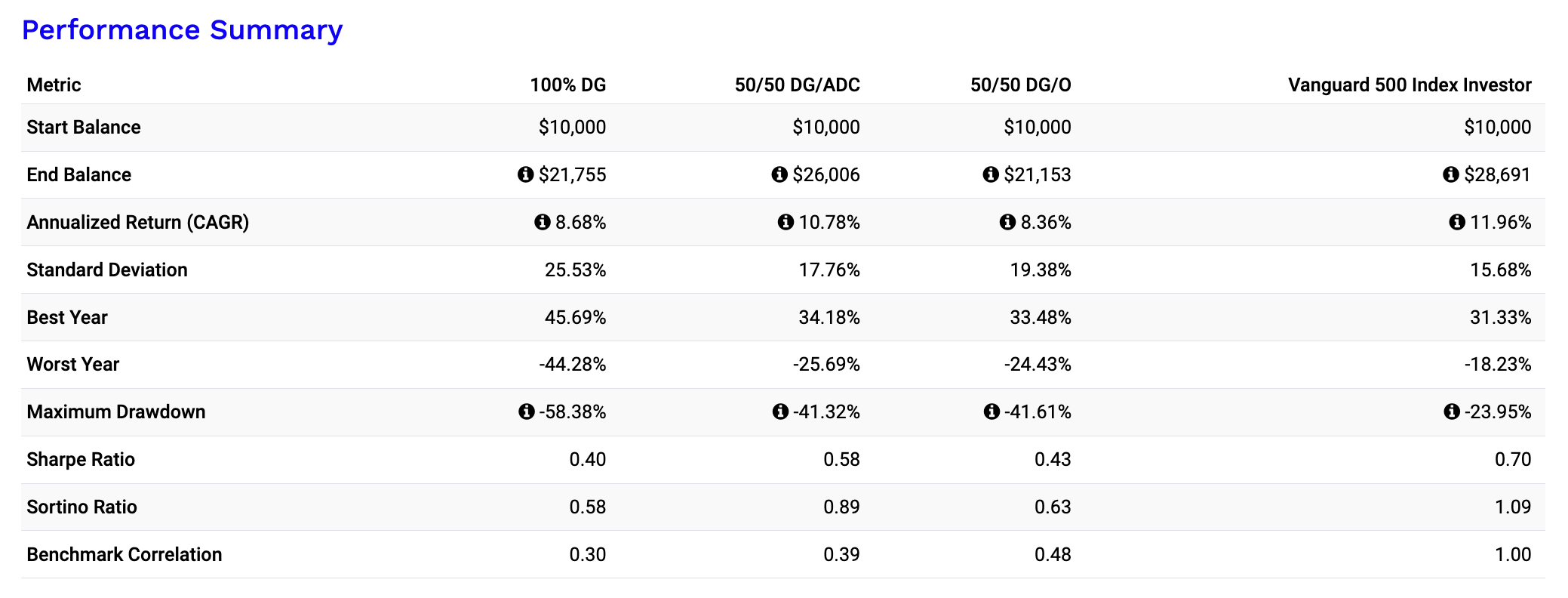

- Since December 2014, Dollar General has returned 8.7% per year with a 25.5% standard deviation. During this period, the S&P 500 returned 12.0% with a 15.7% standard deviation.

- A 50/50 portfolio of DG/ADC shares would have returned 10.8% per year, almost beating the S&P 500, which benefitted from high-flying tech/growth stocks during this period. Moreover, the standard deviation drops to just 17.8%. This 50/50 portfolio has a dividend yield of roughly 3.4% with high-single-digit annual dividend growth.

- A 50/50 DG/O portfolio has returned just 8.4%, which is less than a 100% DG portfolio. All this portfolio achieved is boosting the average yield to 3.8% and lowering the standard deviation to 19.4%.

Portfolio Visualizer

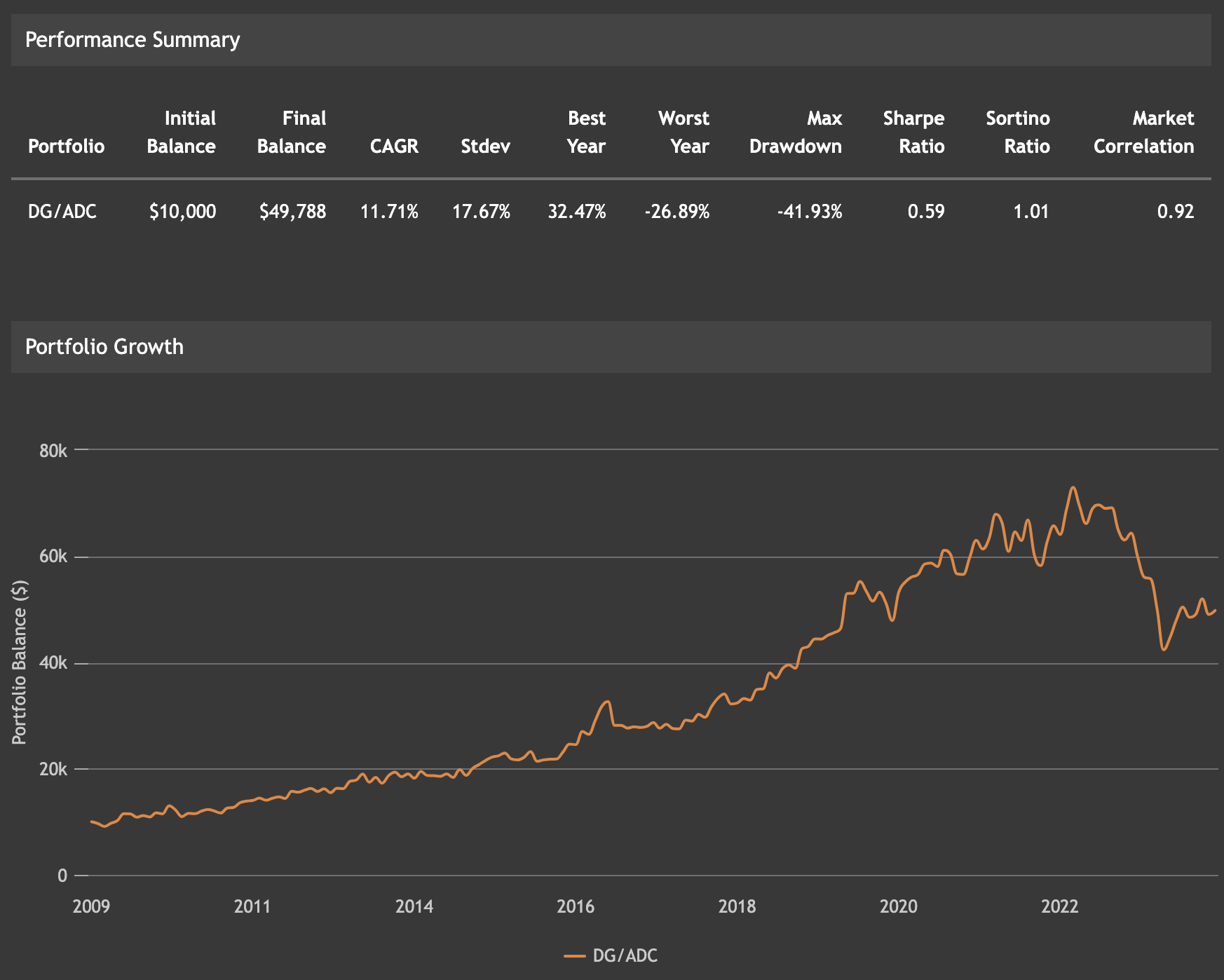

Going back to DG’s 2009 IPO, a 50/50 DG/ADC portfolio (with annual rebalancing) has returned 11.7% annually with a standard deviation of just 17.7%, which is highly favorable.

ValueInvesting

This is obviously not a call to get people to buy Agree Realty.

However, as I view portfolio management as making a great puzzle (without guidelines), I like to combine stocks.

Combining cyclical Dollar General with one of its anti-cyclical landlords can result in elevated returns, a better yield, and a more favorable volatility profile.

While I like Dollar General, I’m not a huge fan of the cyclical nature and competitiveness of its industry.

Nonetheless, especially given the Dollar General store expansion, growth initiatives, and the outlook of accelerating earnings, I believe DG is a buy both as a standalone stock and as a combo with one of its landlords.

I think it’s also fair to say that DG has an edge over its peers.

Takeaway

Dollar General stands out by serving underserved communities with essential, low-cost goods, which becomes especially valuable during inflationary times.

Its strategic focus on rural areas allows for cost savings and rapid expansion, making DG a critical part of the U.S. retail landscape.

Interestingly, combining DG with its top landlords, like Realty Income and (preferably) Agree Realty, can create an interesting investment combo.

This blend not only offers high returns, decent income, and stable dividend growth but also reduced volatility.

Whether as a standalone company or as a combo with a landlord, I believe Dollar General has a bright future – even if headwinds persist.

Pros & Cons

Pros:

- Strong Community Presence: Dollar General serves (underserved) rural communities with essential goods, providing consistent demand.

- Cost-Effective Expansion: DG’s rural focus results in lower real estate costs and solid store growth. So far, this continues to result in an increasing market share.

- Resilience During Inflation: As prices rise, more consumers turn to DG for affordable products.

- Solid Dividends: With a 1.6% yield protected by a 31% payout ratio and an investment-grade credit rating, DG offers stable dividends.

- Growth Potential: DG’s ongoing store openings and innovative concepts like pOpshelf position it well for future growth.

Cons:

- Cyclical Profile: DG operates in a competitive and cyclical industry, which is sensitive to economic downturns.

- Pressure on Low-Income Consumers: Economic challenges for its primary customer base can impact sales and profitability.

- Operational Challenges: Managing a rapid expansion and maintaining store quality can be a tough challenge.

Q2 2024 Earnings Call Transcript")