Althom

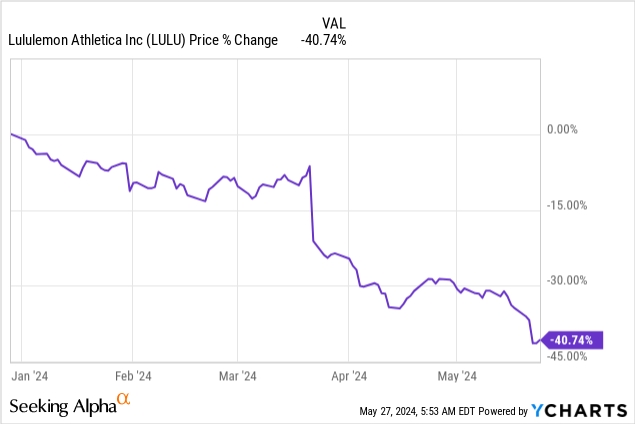

Collapse In Share Price

Lululemon Athletica Inc. (NASDAQ:LULU) has seen its share price collapse by a stunning 40% YTD. This was largely driven by two key events: (1) Underwhelming guidance for 2024 back in March and (2) Departure of Chief Product Officer just like week. Understandably, this has triggered the excitement and attention of numerous investors as LULU is seen to be a “high quality” company by many, and such a huge drop in share price could signal a buy opportunity. In this article, I will seek to objectively analyse the bull and bear arguments surrounding LULU and determine if the company is still a fundamentally strong business amidst all the market noises.

Recap on FY23 Earnings

Let’s take a quick recap on FY23 earnings for LULU, which caused the biggest dip and weakening investor sentiment surrounding the stock.

As a whole, FY23 and 4Q23 results were actually good for LULU. FY23 revenue was up 19% while net income grew 81% (this huge spike was largely due to impairment reduction amidst business growth). Other metrics like same store sales growth remained robust too, growing at 12% in 4Q23, while gross margin continued to expand 430bp to 59.4% in the same quarter.

However, the bad news came in the guidance. For 2024, the company expects 11% to 12% top-line growth reaching $10.700 billion to $10.800 billion, below the Wall Street estimate of $10.9 billion. CEO Calvin McDonald also stated, “…in the US is where we are really navigating the dynamic retail environment with the consumer. That is a little soft coming into the year”. Coupled with similar sentiments from Nike (NKE) and Adidas (OTCQX:ADDYY), this seemed to spook investors that the macro environment in the US is indeed weakening, which could hurt consumer focused stocks.

What The Market Is Saying

#1: Athleisure Is No Longer A High-Growth Category

Looking at some statistics, the U.S. athleisure market size was valued at USD 86.41 billion in 2023 and is expected to reach around USD 211.23 billion by 2033, growing at a CAGR of 9.40% from 2024 to 2033. On the other hand, Asia Pacific, LULU’s 2nd biggest market, is expected to grow from US$ 122.77 million in 2021 to US$ 247.48 million by 2028, at a 10.5% CAGR.

From this, it is evident that growth in athleisure is definitely slower than pandemic days when 20-30% annual growth could be experienced as work from home and changing office norms were the catalyst that drove athleisure adoption. As these catalysts now become the norm, the once powerful growth engine will expectedly subside down. However, I still view ~10% growth as a relatively good growth rate, as it is still much higher than sportswear and footwear; hence LULU still operates in a good market.

Additionally, I believe that LULU still has the opportunity for above market growth rate as it still only has a relatively small market share in the US of around 7.2% and 1-2% in Asia. Compared to market leader Nike with 16% share, LULU definitely still has room to increase share.

Verdict: While lower than before, market growth is still attractive and LULU still has upside potential by gaining market share.

#2: US Consumer Spending Is Weakening

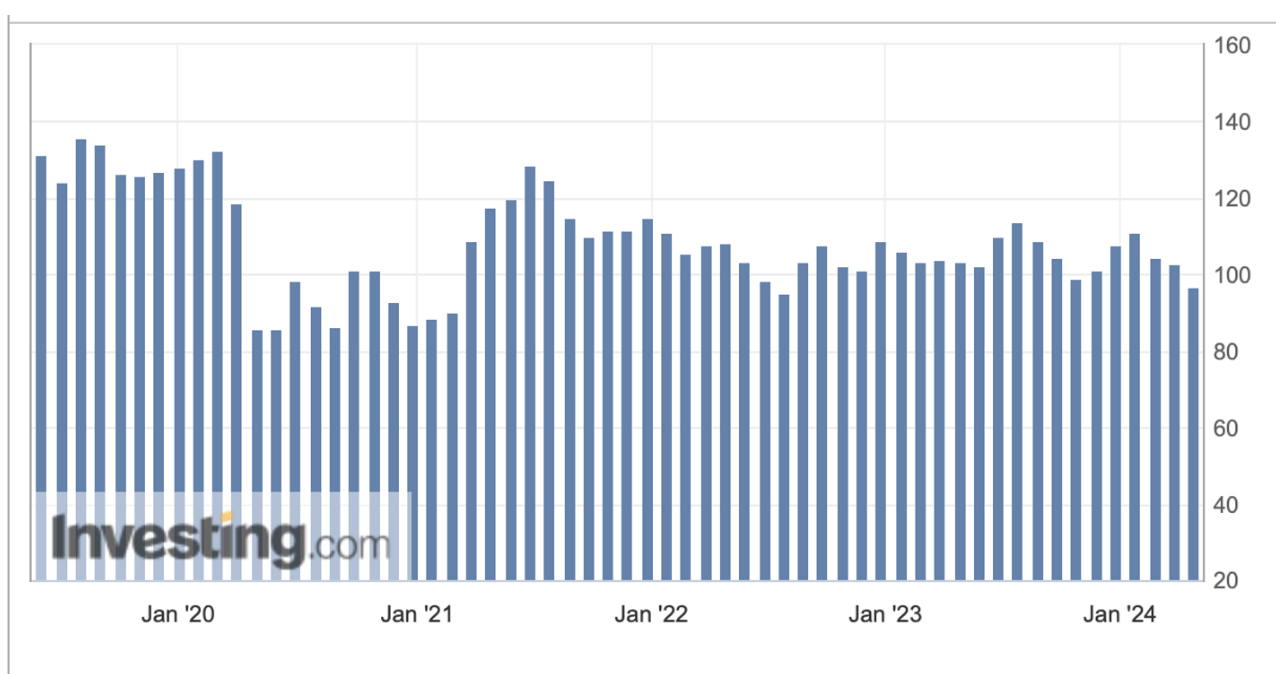

Consumer Confidence Index (CCI)

From the Consumer Confidence Index, we can see that this worry is likely justified. CCI is currently at 97 in April 2024, and much lower than the forecast of 104. Additionally, when CCI falls below 100, it means consumers are more pessimistic than in 1985. To add fuel to the fire, we can also see a faint downward trend in the past year.

US Consumer Confidence Index (Investing.com)

Hence, from the CCI, we can infer that the US consumer is indeed getting more pessimistic about the economy and their spending.

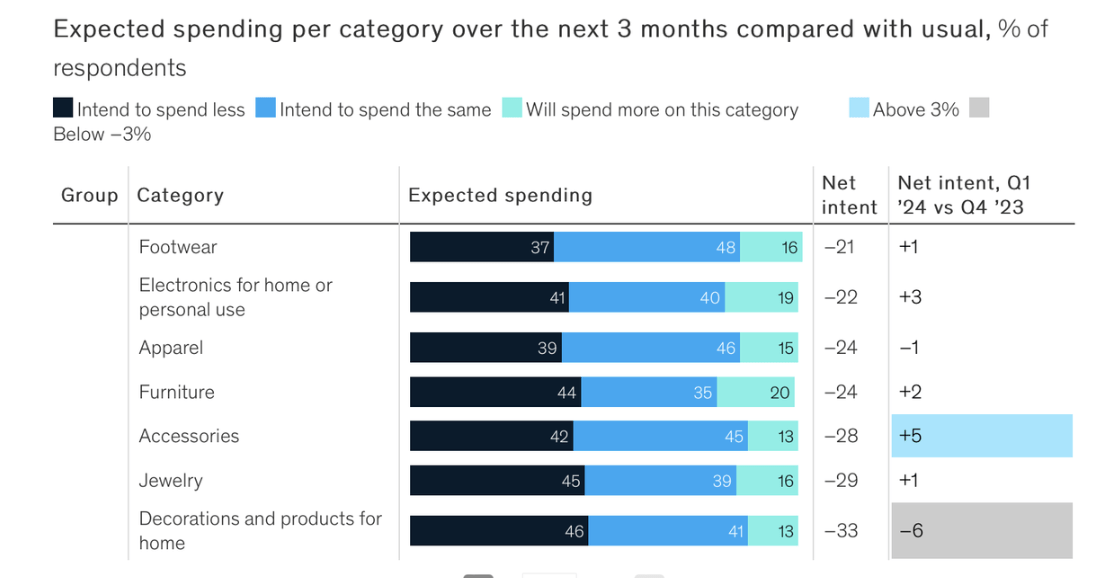

McKinsey Consumer Report Feb 24

Turning to a consumer report, McKinsey asserts that consumers are looking to spend more on essentials (e.g. fresh produce, meat), as well as on travel and home. Notably, net intent on apparel spending remains flat. Given that there is not a huge decline for apparel, this should still be considered positive news for the athleisure industry.

US Consumer Spending Net Intent (McKinsey)

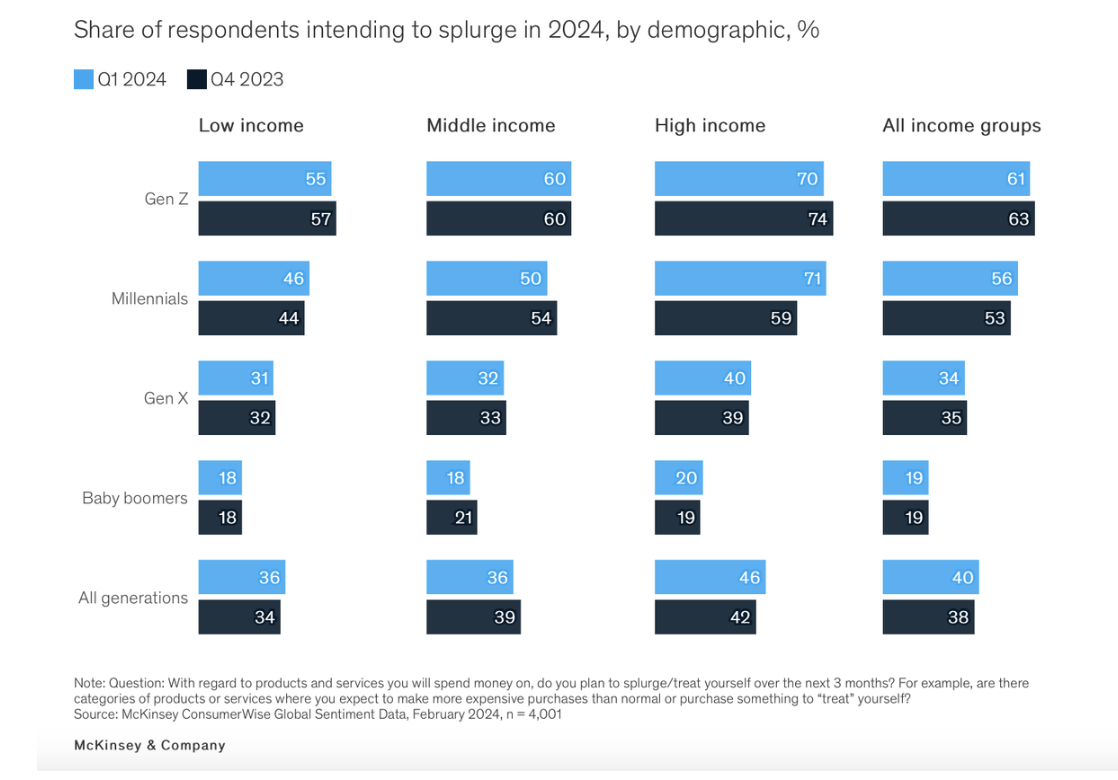

Another good news is that millennials and Gen Zs, especially high-income ones, are the demographic that are intending to splurge in 2024. This coincides with LULU’s target demographic and should be a positive for the company.

Willingness to Splurge in 2024 (McKinsey)

Past Analysis of Recession

From these data, I gather that consumer sentiment is indeed weakening, but LULU’s target demographic and industry still appears to be relatively robust. Therefore, my next analysis would be on how LULU may perform in a downturn.

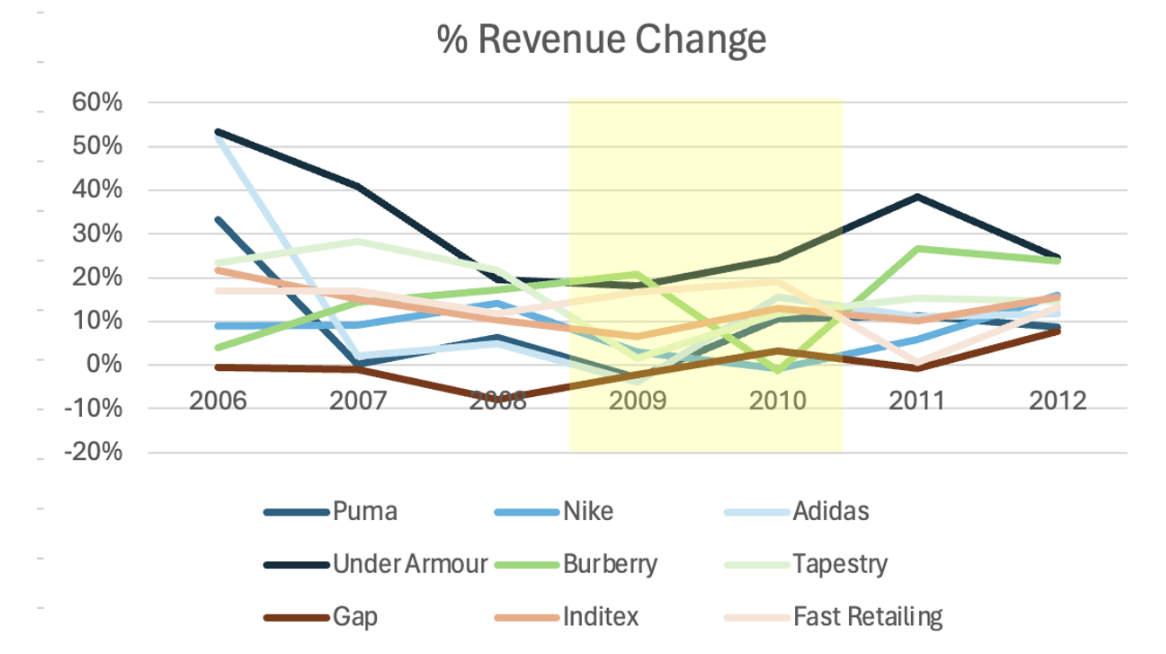

With reference to the GFC, I compare 3 category of companies — “sportswear”, “contemporary luxury” which refers to lower-end luxury since LULU is more premium than normal sportswear (defined by LePrix), and “fast fashion”.

Consequently, “Luxury” in green tends to hold up slightly better than “Sportswear” in blue with the exception of Under Armour, which is likely because it is still a small and fast-growing company (>30% growth). “Fast fashion” in green is more mixed, some high and some underperformance.

Sportswear, Luxury and Fast Fashion Growth Rates 2006-2012 (Author’s compilation)

Considering LULU was a high-growth company >~20% before FY24, as well as a more luxury option, it will likely weather a downturn better than its sportswear peers.

So how does this apply to today’s market? Looking at competitors, Nike guided 1% growth in FY24 and LSD decline in revenue in 1H25, while Adidas guided MSD sales in 2024. The market may worry that LULU will also experience muted growth, and this is a sentiment echoed by Jefferies, who expect LULU’s US revenue growth to turn negative next year. Given the analysis of industry performance in poor economic conditions, I expect LULU to hold up much better than peers. Additionally, I would like to note that LULU grew top-line well in 4Q23 while Nike had NA sales fall by 3%; hence I would disagree with the most bearish case of negative US sales growth next year for LULU.

Verdict: Consumer sentiment is indeed weakening in the USA, but apparel and high-end young consumer spending remains strong. LULU should perform better than sportswear peers like Nike and Adidas, and investors shouldn’t be pessimistic on LULU just because of weaker guidance from peers. However, I believe LULU’s 11-12% revenue growth may still have room to be revised lower to ~HSD growth, so investors should navigate cautiously.

#3: LULU Still Has Multiple Engines of Growth via Increased Penetration in US Women, Men and International

According to CEO McDonald, LULU’s unaided brand awareness has grown in the US from 25% to 31% in 2023, and from 9% to 14% in China. Unaided brand awareness is the percentage of consumers in a survey who are aware of a brand without being assisted, per The Motley Fool. According to Zackfia, rival brands like Nike have over 80% awareness. LULU definitely sees growing penetration rates as a growth driver.

However, considering LULU’s niche target market, is this brand awareness considered low?

Women Athleisure In USA

Let’s take the core LULU demographic in the USA. To be generous, I will consider all of 15-44 women as the “wider and potential” target demographic of LULU as they are young and willing to spend, even if it is one or two purchases per year. Currently, there are over 65 mn of aged 15-44 women in the US.

Since the survey is likely conducted among working age adults e.g. 15-64, 31% awareness out of 210 mn consumers is also around 65 mn people. Given that LULU’s customers are predominantly female, we can say that almost all of their target demographic should be aware of LULU. Any incremental awareness should mainly come from men.

Hence, I believe that there is little room for growth in the US women’s apparel for LULU as this is a mature market is at peak penetration.

Menswear

One of LULU’s drivers is menswear. It adds another 65 mn potential target customers for LULU in the US, and men are generally wealthier than their female counterparts. Mens reached $2.25 bn in sales in 2023, up 15% yoy. However, this is relatively low growth considering women grew by 17% yoy. Per LULU’s 2026 mid-term target, they are only forecasting ~14% annual growth in the mens segment, so this growth rate is not an anomaly.

Compare this to Under Armour (predominantly men), which was growing top line above 20-30% annually when its revenue was in the $1 bn – 4 bn range. Hence, I believe that while mens is a growth driver for LULU, it is not going to bring astronomical growth for the company. One reason for this could be because LULU still has a relatively feminine image attached to it. A quick Instagram search also shows how female oriented online communities are for LULU’s customers.

In my opinion, LULU has built a very strong brand in yoga & via its trademark pants. It is going to be very hard and a poor business decision to move its brand away from its core. Investors should just accept that it is unlikely that LULU becomes a common apparel for men in a way that Nike or Adidas has been for both genders. Menswear can supplement growth but will not be a viable long-term growth driver for the company.

International Expansion

LULU is largely focused on China for international expansion, with China revenue larger than other geographic areas. China revenue has also grown 66.5% the last year, vastly outpacing that of the Americas. In the coming year, LULU aims to open 35-40 net new company operated stores, 5-10 in Americas and the rest primarily in China.

I believe LULU benefits from strong industry tailwinds in China. For one, there is no homegrown Chinese brand that has the same recognition or positioning as LULU. This is unlike in the sportswear industry, where Anta and Li Ning are gaining share at the expense of Nike and Adidas. LULU also benefits from trends such as the growing middle class, “Healthy China 2030” initiative & pivot towards health and wellness in China.

As a testament to their strength, LULU has a #1 ranking across all Yoga categories in Maigoo rankings. In Tmall, LULU has 3.8 mn followers with a 5.0 rating, compared to Nike with 47 mn followers and a 4.0 rating. This shows large room for growth and a very satisfied consumer base for LULU.

Verdict: Bullish analysts may be overly optimistic about LULU’s growth prospect. US women are relatively mature, while mens don’t provide explosive growth. However, I am positive on international expansion, given LULU’s strong brand equity and lack of notable competition in overseas markets. I believe this will be the key driver going forward that investors should focus on.

#4: Rising Competition In USA Is Eroding LULU’s Brand Position

Barrons estimates that in the three years following the pandemic, around 200 new brands have entered the athleisure market. The two key brands that analysts are worried about are Alo Yoga and Vuori.

Alo Yoga and Vuori have been seeing exponential growth the past years. To show their strong success:

- Vuori’s store foot traffic surged by 704% on average, in the first eight months of 2023 compared with the same period in 2019, according to data from Placer.ai. Alo, a favorite of celebrities and influencers, saw foot traffic rise by 120% during the same time frame.

- In Piper Sandler Spring 2024 survey, Alo Yoga was the No. 11 favourite brand and Vuori was the No. 15 favourite brand, compared to No. 35 and No. 24 respectively in the fall.

However, I believe that LULU remains well positioned and its brand is holding up against competition well.

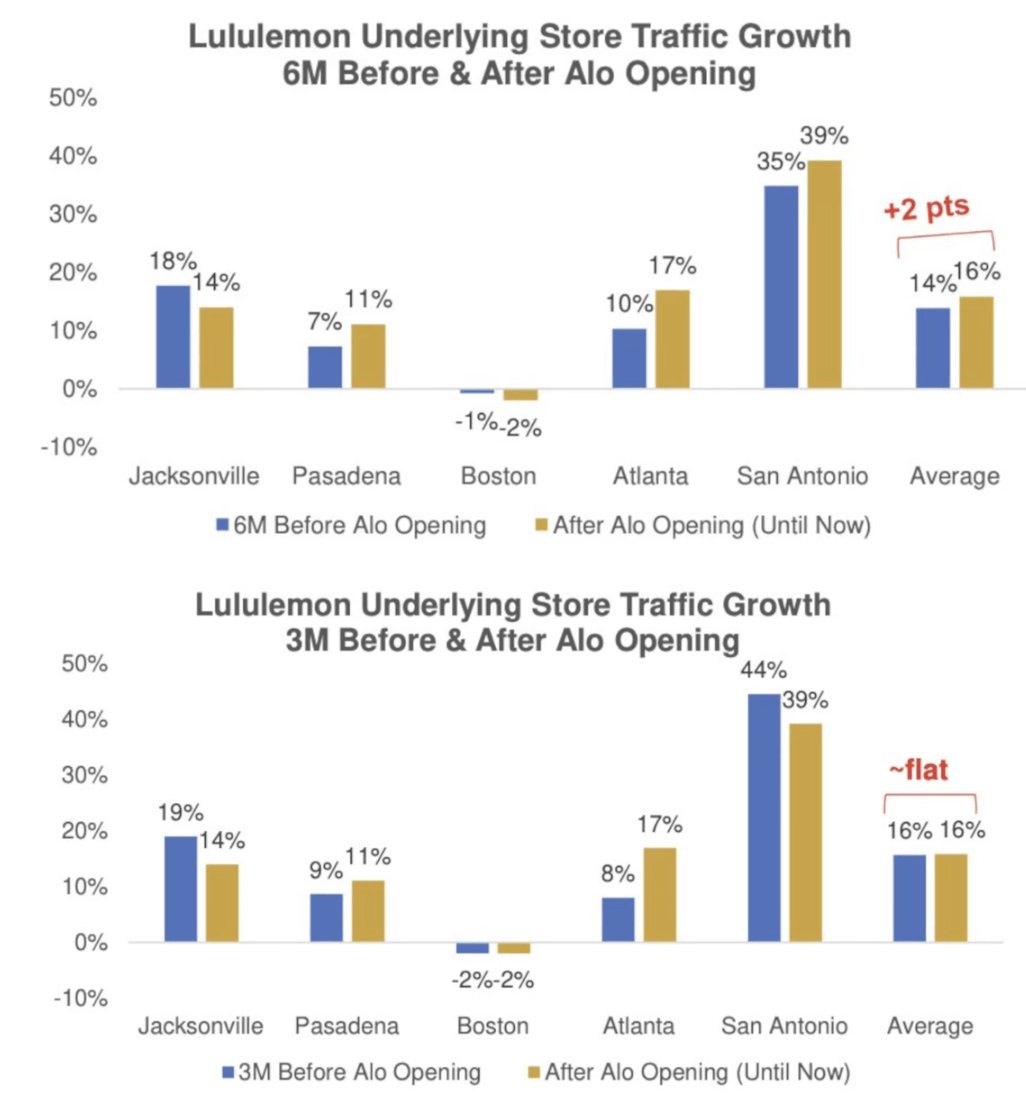

First, research shows that store traffic for LULU remains steady 3M and 6M before and after an Alo Yoga opening near to an existing LULU store.

LULU Store Traffic after Alo Opening (Placer.ai)

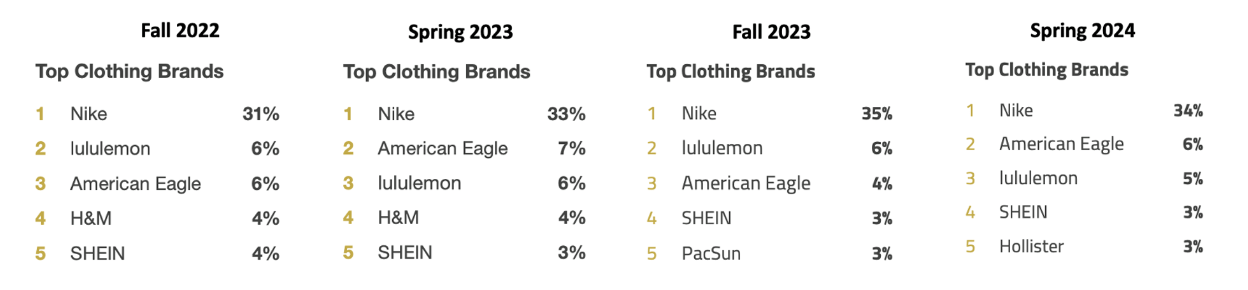

In the same Piper Sandler survey, LULU remains the highest ranked athleisure brand and its favourite brand percentage has remained stable at 5-6%. I would be more worried if LULU’s percentages start to fall to around 3% while Alo and Vuori enter the Top 5.

Top Clothing Brand Piper Sandler (Piper Sandler)

Additionally, Vuori and Alo Yoga are competing directly in LULU’s turf, in the higher end yoga/athleisure market, with prices just slightly lower as seen in the core leggings prices.

- Vuori: $89 – $128

- LULU: $98 – $168

- Alo Yoga: $80 – $130

Branding is a form of competitive advantage which LULU has and as I quote the book 7 Powers, “A strong brand can only be created over a lengthy period of reinforcing actions (hysteresis)”. Competitors like Vuori and Alo simply do not have the track record and history to build a brand that could topple LULU, considering that LULU is not having any missteps in its strategy. Without significant innovation, it will be very difficult for rivals to topple LULU.

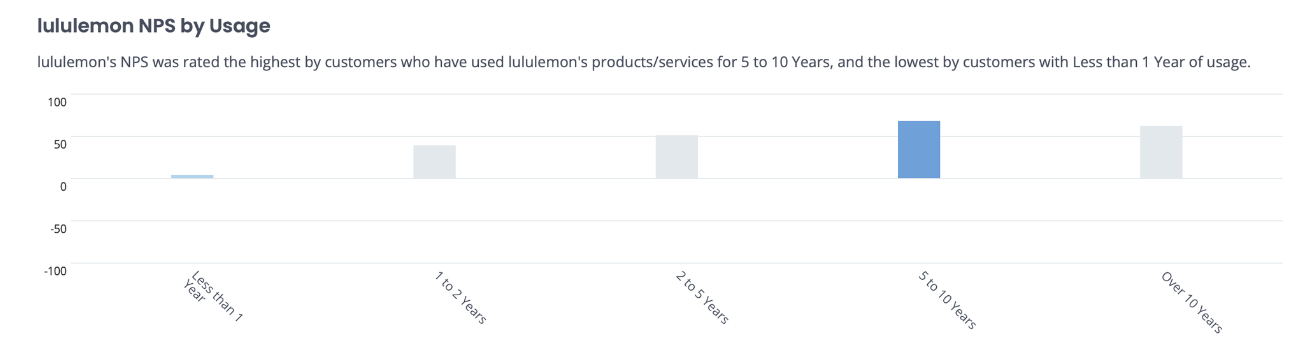

The Net Promoter Score of LULU is very high at 43, flat yoy, suggesting that there is no significant detraction of brand loyalty to the company. Furthermore, the highest NPS come from customers who have shopped for 5-10 years with LULU, reinforcing the strong customer loyalty of long-time customers.

Lululemon NPS (Comparably)

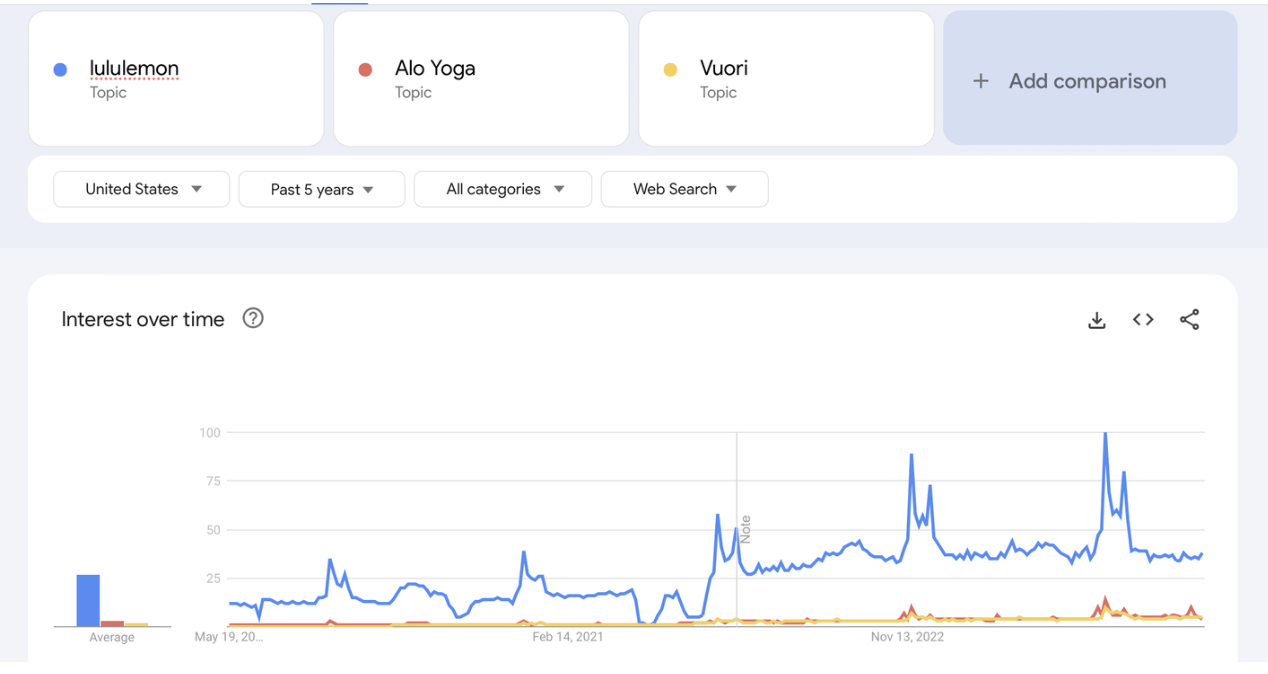

Finally, on Google trends, LULU’s interest has remained stable over time, and we can see that Alo Yoga and Vuori remains much lower than LULU.

Lululemon, Alo, Vuori Google Trends (Google Trends)

Other Notable Brands Have Tried & Failed

Finally, I would like to mention how other athleisure brands have tried to disrupt LULU but failed. One example is Athleta, Gap’s (GPS) very own athleisure brand, which did well during the pandemic. According to Gap, same-store sales for fiscal 2021 rose by 39% compared with fiscal 2019. By May 2022, however, the segment started losing ground as Athleta struggled with “product acceptance challenges” as their apparel was not resonating with shoppers. In the most recent 4Q23, Athleta’s comparable sales were down a stunning 10% while revenue was down 4%.

This data suggests that it is not easy to be a lasting challenger to LULU. Alo Yoga and Vuori could very well be the brands which are considered a “fad” and “trend” rather than LULU.

Verdict: LULU’s strong branding remains intact as shown by store traffic, net promoter score and consumer surveys. Worried about Alo Yoga and Vuori significantly disrupting LULU seems to be an overreaction.

Relative Valuation

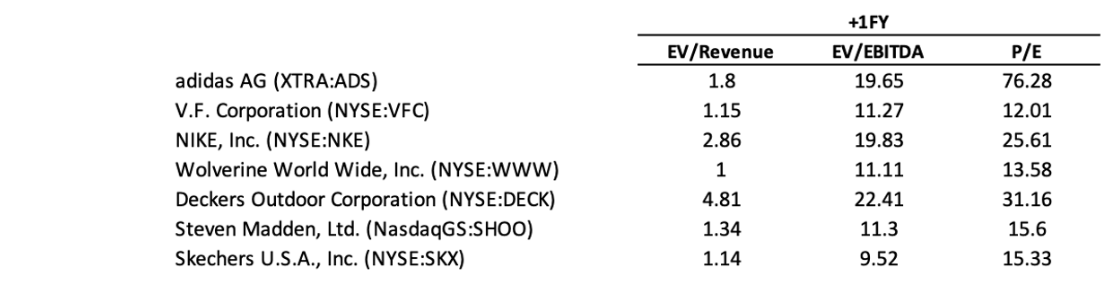

Given that LULU’s business fundamentals remain intact, I will now turn to a quick relative valuation. The median forward P/E for sportswear is around 16x, 75th percentile is 28x, while Nike is 26x. Nike’s 10Y median forward P/E is 28; this is for a top quality company that has withstood the test of time.

Sportswear Relative Valuation (Author’s compilation)

With LDD growth, higher margins and strong brand equity, LULU could possibly command a P/E of 25 in the long run, which is what it is currently trading at. Hence, I believe LULU is currently fairly valued. I would be more attracted if the forward P/E comes down to ~ 18-20x, which affords some margin of safety → $12.2*1.1 = $13.42 → $242 – $268.

Summary

LULU’s stock decline is largely due to a re-rating into a lower growth company, since expectations are now LDD top-line growth. Research supports lower growth going forward, with US women already at peak awareness, mens steady at ~15%. International is the only major catalyst, but store openings are at a relatively slow pace. Despite fierce competition, I am content that LULU’s strong branding remains intact given store footfall, consumer survey, Google trends and net promoter score. While LULU should hold up better than peers in a recessionary environment, the weakening consumer outlook + fair valuation makes me want to take a wait & see approach with LULU. There is not enough margin of safety. A P/E below 20 would be an attractive entry point.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")