JHVEPhoto

Introduction

Cryptocurrencies have been hot ever since the pandemic took the value of major cryptocurrencies like Bitcoin and Ethereum “to the moon.”

As a result, major financial institutions want in.

After the official approval of Bitcoin ETFs in the U.S., we’re now seeing more interest from major financial corporations, including CME Group (NASDAQ:CME).

According to the Financial Times, the largest futures exchange in the world is planning to launch bitcoin trading, aiming to make money from the increasing demand for crypto-related investments.

CME Group, which already hosts major futures, including Bitcoin and Ethereum, would allow investors to trade Bitcoin more easily through basis trades – competing with companies like Coinbase (COIN).

A common strategy among professional bitcoin traders and a staple of the US Treasury market, basis trading involves borrowing money to sell futures while buying the underlying asset, and extracting gains from the small gap between the two. The bulk of the Treasury basis trade takes places on CME venues. – Financial Times

I’m bringing this up because CME Group continues to do what it does best: using its platform to capture growth from the ever-increasing demand for futures, options, and related products from organizations and individual traders.

As I have highlighted the stock in a number of recent articles (like this one), it’s time to dive into the details of this Chicago-based giant again, as it continues to be one of my best ideas in finance.

My most recent article on the company was written on February 14, 2024, when I said buying the house is a winning strategy.

A Wide-Moat Financial Giant With A Special Dividend

The finance sector is dominated by banks.

As much as I love to buy undervalued banks during recessions, their business models often do not have a moat, while the longer-term risk/reward is poor due to steep corrections when economic times are tough.

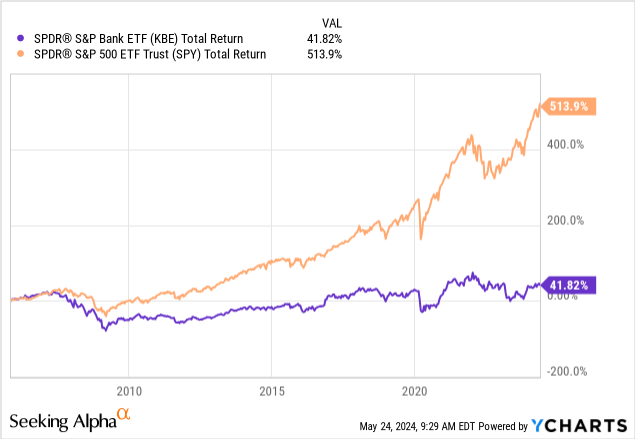

Since the inception of the S&P Bank ETF (KBE), the total return has been just 42%. During this period, the S&P 500 has returned 514%.

CME is different, as I’m convinced it has a superior business model.

It has a wide-moat business model that comes with a massive portfolio of futures, options, cash, and over-the-counter (“OTC”) products.

These products are accompanied by tools to optimize portfolios, analyze data, and manage risks.

As this may sound vague, let me add some color.

Founded in 1898, CME Group owns a number of major exchanges where the products I just mentioned are traded.

Through a number of acquisitions, the company now owns four of the biggest exchanges in the world, each with a unique focus on essential trading products.

- CME (Chicago Mercantile Exchange) offers a diverse range of futures and options contracts, including interest rates, equity indices, foreign exchange, agricultural commodities, and more.

- CBOT (Chicago Board of Trade) trades futures and options contracts for agricultural products, interest rates, and equity indices.

- NYMEX (New York Mercantile Exchange) specializes in energy and metals trading, including contracts for crude oil, natural gas, and various metals like gold and silver.

- COMEX (Commodity Exchange, Inc.) focuses on metal products, offering contracts for gold, silver, copper, and other base metals.

This portfolio provides the company with a wide moat advantage, as it has exclusive licenses to offer futures on the S&P 500, as part of a bigger portfolio of exclusive rights.

In 2010, CME Group acquired a majority stake in Dow Jones Indexes, which was combined with S&P’s index business in 2012 to form S&P Dow Jones Indices LLC, of which CME Group now has a 27% ownership stake. S&P Dow Jones Indices LLC combines the world class capabilities of the S&P and Dow Jones Indices, and is a significant player in passive investing, including the exchange-traded fund (ETF) industry value chain. As part of the joint venture, we acquired a long-term, ownership-linked, exclusive license to list futures and options based on the S&P 500 Index and certain other S&P indices. – CME 2023 10-K

In other words, not only does CME offer some of the (world’s) most important futures and options, but it also does this with very limited competition risk in major product categories – all while increasingly rolling out new products to boost volumes and attract new clients.

Although I do not trade futures and options, I monitor CME futures on a daily basis, this includes the e-mini (S&P 500), NYMEX crude oil, NYMEX Henry Hub (natural gas), CBOT corn/soybeans/wheat, and COMEX metals.

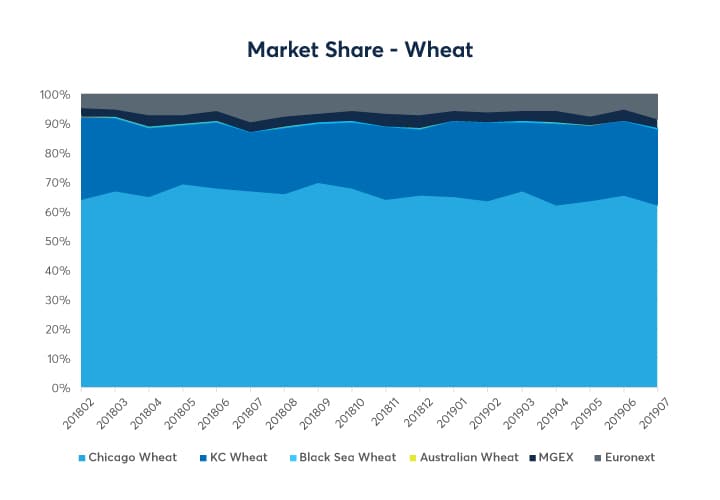

To give you another example, the company’s wheat futures have a market share of roughly 90%, without any declines in recent years.

CME Group

With that in mind, one might make the case that one disadvantage of CME Group is that it is highly dependent on transaction volumes instead of recurring revenue services.

Its peer Intercontinental Exchange (ICE), which I also like, is building a massive business in mortgage services.

The good news is that CME’s dependence on transaction volumes has a huge benefit: Whenever volatility spikes, CME tends to grow its revenue.

While the CME stock price is not recession-proof, its revenue is – at least to some extent.

During the Great Financial Crisis and the pandemic, CME’s stock sold off.

However, its revenue accelerated as increased volatility resulted in much higher trading volumes.

Moreover, the company has three other major (related) benefits.

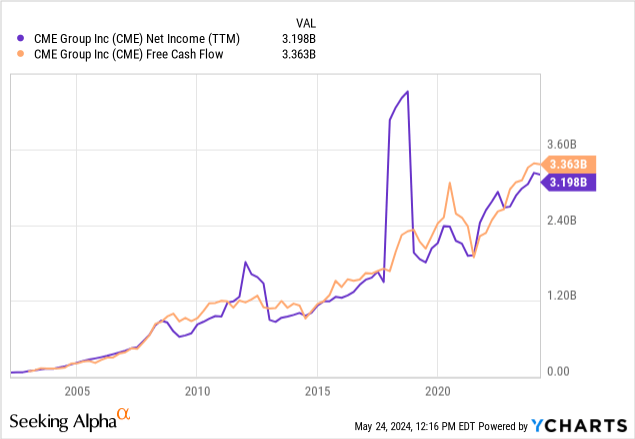

- The company is a cash machine.

As we can see below, the company consistently generates more free cash flow than net income, which means it has a >100% FCF conversion rate. That’s a sign of high-quality earnings, as a huge portion of its earnings end up as cash.

There’s no “waste” like high capital requirements or other “leaks” that result in subdued cash generation. That’s the benefit of having a high-margin business that runs with relatively low upkeep.

After reporting $3.4 billion in free cash flow last year, the company is expected to grow that number to $3.7 billion this year – that’s roughly 5% of its market cap.

- The company has a very healthy balance sheet.

This year, the company is expected to end up with less than $100 million in net debt. This implies a 0.02x net leverage ratio.

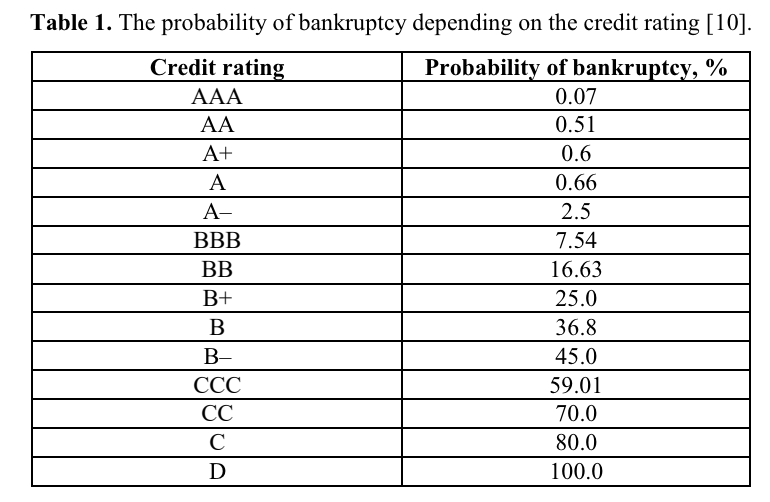

It has a credit rating of AA-, one of the best ratings in the world.

While everything above BBB- (investment-grade threshold) is great, a double-A credit rating implies a bankruptcy probability below 0.6%.

Pirogova et al. (2019)

The mix of strong cash generation and a healthy balance sheet brings me to the third benefit.

- The company has the habit of returning all of its free cash flow to shareholders.

$1.15 per share per quarter. That’s the company’s regular quarterly dividend.

This translates to a yield of 2.1%.

That’s not very exciting, is it?

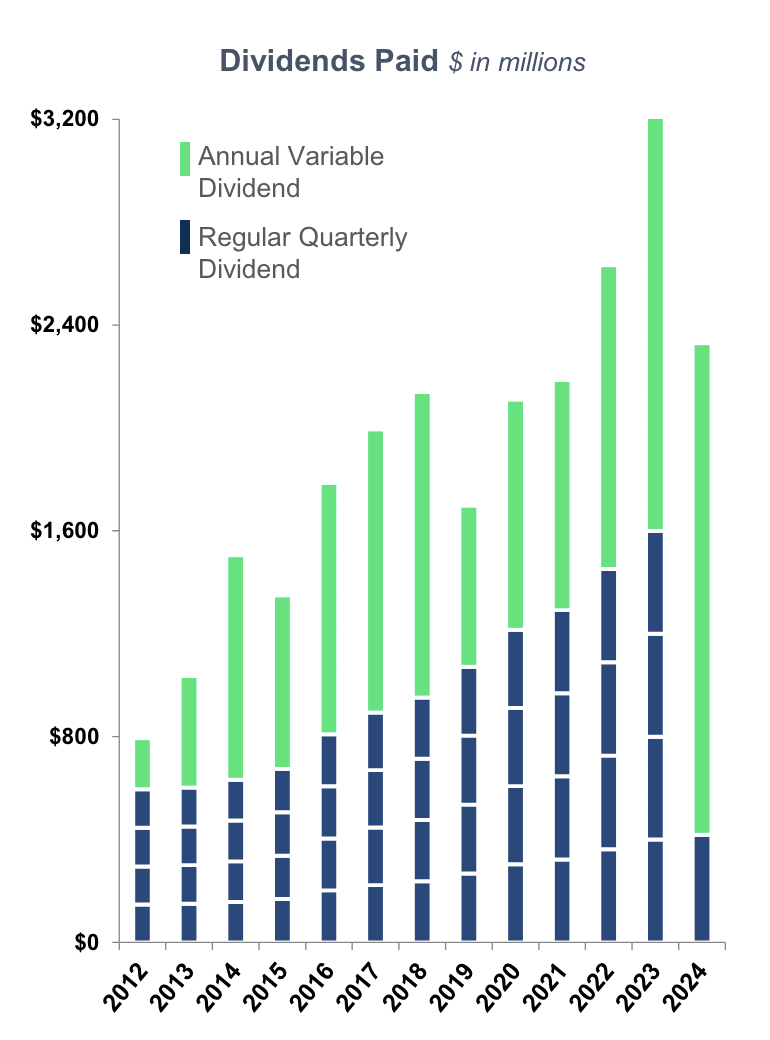

However, what makes CME special is its annual special dividend – announced in 4Q and paid in 1Q of the next year.

As the chart below shows, the company has paid a special dividend every year over the past 12 years. While it’s based on an educated guess, I think this year, we’ll likely be looking at a total dividend yield of 5%, as that’s the expected free cash flow.

CME Group

With regard to dividend growth, I mainly look at total dividends paid, as there’s no need to look at regular quarterly dividend growth when we get a payout of roughly 100% anyway.

In 2013, the company paid dividends of $4.40. In 2023, that number was $9.65. This implies a CAGR of 7.4%.

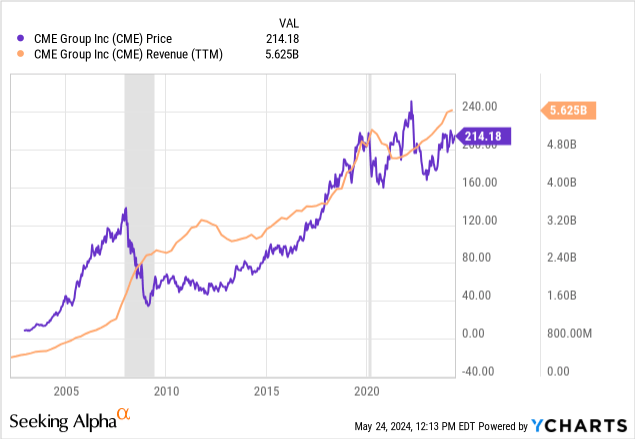

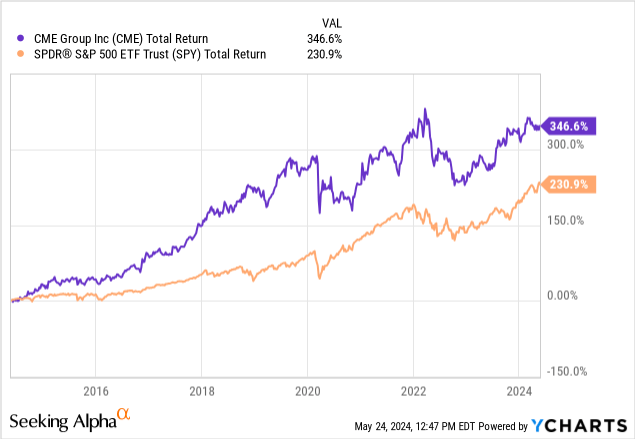

It has also allowed CME Group to consistently outperform the market.

Including dividends, the company has returned 347% over the past ten years alone, beating the 231% return of the S&P 500 by a considerable margin.

This brings me to the next part of this article.

Recent Events & Valuation

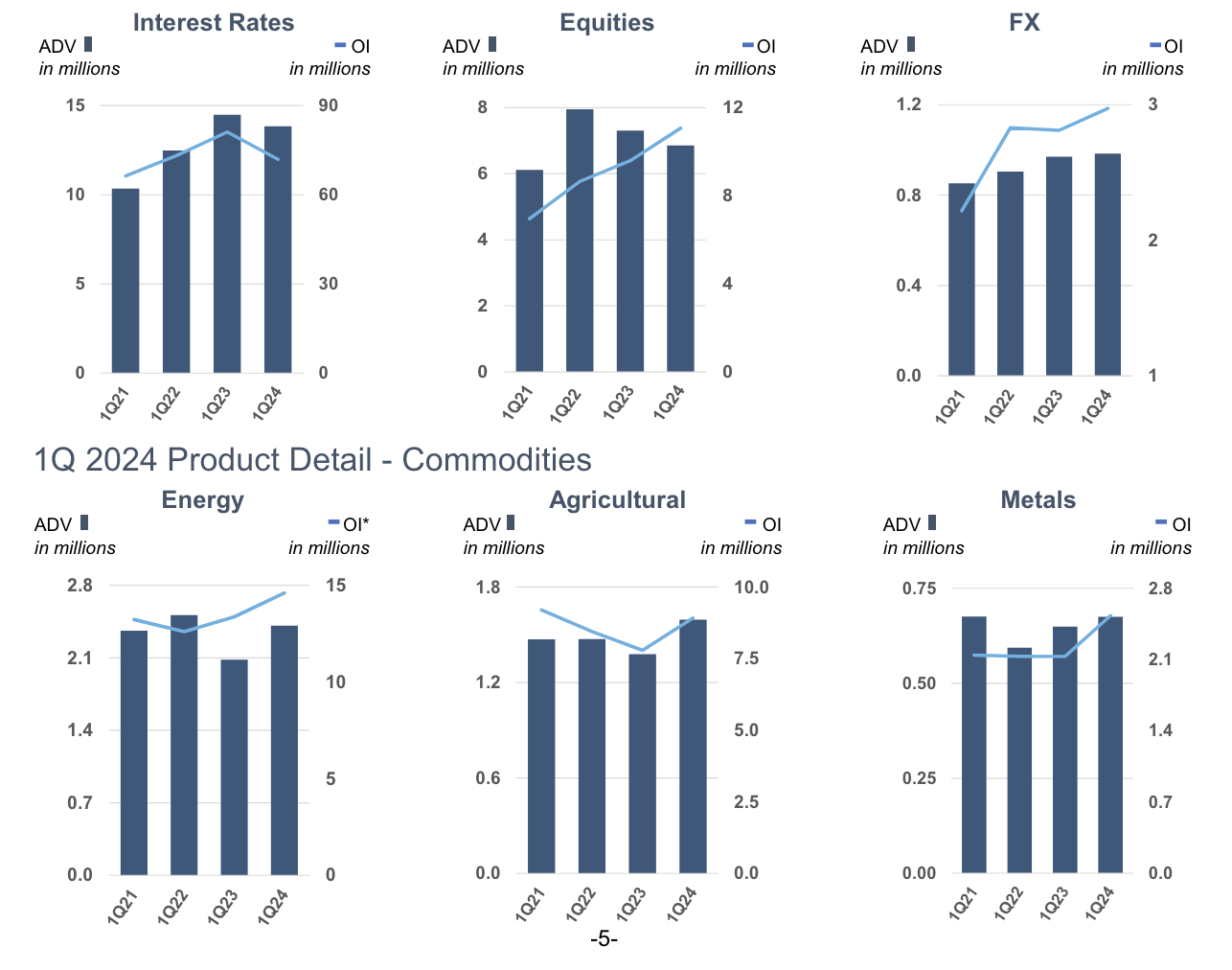

In the first quarter of this year, the company was able to show what it’s capable of, as it reported an average daily volume (“ADV”) of 26.4 million contracts, the third-biggest first quarter in history.

Even better, this happened during a period of subdued (equity) volatility!

The only two better first quarters were 1Q20, when the world was hit by the pandemic, and 1Q23, when financial markets were shaken by banking bankruptcies.

CME Group

Moreover, it reported blowout numbers in non-US ADVs.

Our non-U.S. ADV also reached a record level of 7.4 million contracts. This was driven largely by 38% growth in energy, 29% in ag products, and 7% in metals. In total, we delivered 14% ADV growth across our physical commodity products to 4.7 million average daily volume, which included 16% year-over-year growth for both energy and ag products. This strong first quarter activity across our business lines helped generate record adjusted quarterly financial results which Lynne will detail in just a moment. – CME 1Q24 Earnings Call

It also grew its margins, with adjusted operating margins rising to 68.9%.

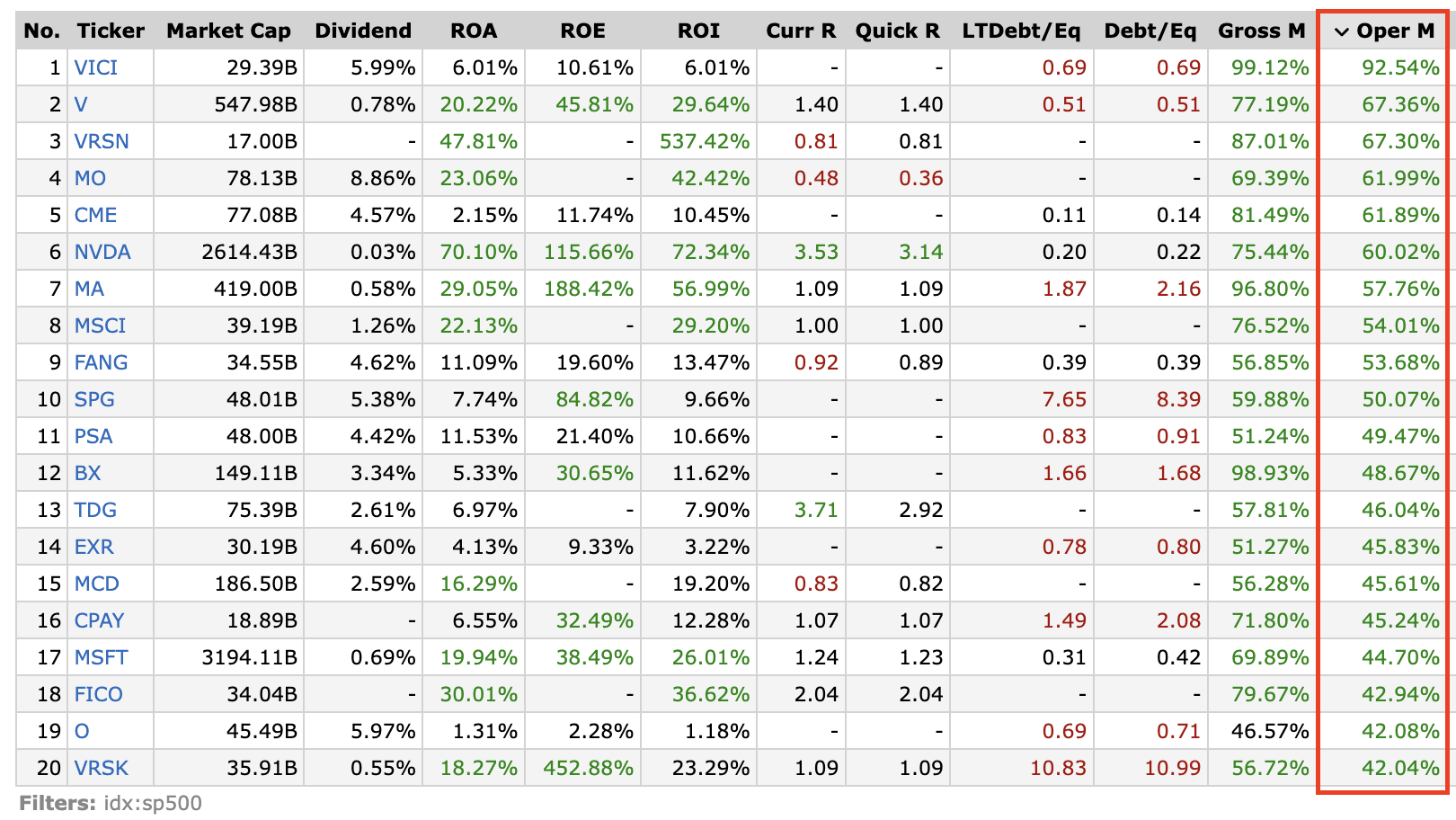

Using FINVIZ numbers (I’m assuming they are using GAAP data), we see that CME is a top-five company in the S&P 500 when it comes to operating margin profitability!

FINVIZ

This allowed the company to turn the third-best 1Q ADV ever into the highest quarterly earnings result ever, as it generated $2.50 in EPS, which is a 3% year-over-year improvement.

So, what about its valuation?

Valuation

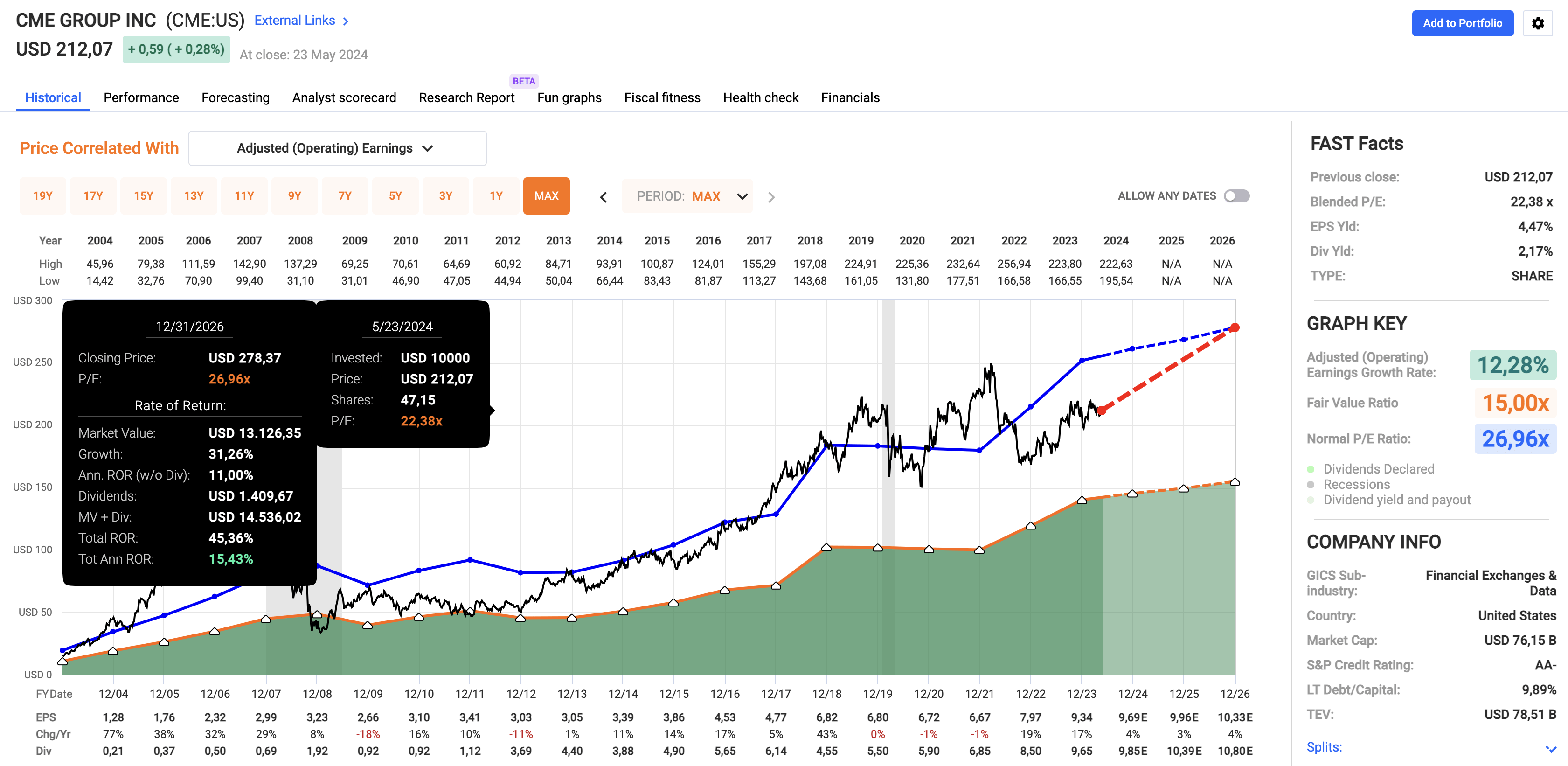

CME Group trades at a blended P/E ratio of 22.4x. It has a normalized P/E ratio of 27.0x.

While 27.0x may seem like a lofty valuation, I need to add that this is quite normal for a company with elevated margins and a free cash flow conversion rate of 100% or more.

As the quality of its earnings is high, it squeezes more shareholder benefits from every dollar it makes. That’s why an “elevated” P/E ratio is justified.

FAST Graphs

On top of trading at a discount, CME is expected to maintain consistent EPS growth, with 4% average annual EPS growth through 2026.

This implies a fair stock price target of $278, 30% above the current price.

Hence, I stick to a Buy rating, as I believe CME offers a great mix of growth and value, backed by a fantastic wide-moat business model with a very bright future.

Takeaway

CME Group stands out as a financial powerhouse with a solid, wide-moat business model.

By leveraging its exclusive rights and extensive portfolio of futures and options, CME captures significant market share and benefits from volatility-driven revenue growth.

The company’s strong cash generation, fantastic balance sheet, and consistent dividend growth, including special dividends, make it a compelling investment.

Even better, with an attractive valuation and a consistent growth outlook, CME offers a fantastic mix of growth and value.

Pros & Cons

Pros:

- Wide-Moat Business Model: CME has an impressive portfolio of futures and options, which offers unique market access and exclusive licenses.

- Strong Cash Generation: The company consistently generates more free cash flow than net income, translating to high-quality earnings.

- Volatility: CME thrives on market volatility, which provides investors with safety during most recessions.

- Consistent Dividends: CME usually distributes 100% of its free cash flow to shareholders, using regular quarterly dividends and one special annual dividend.

- Healthy Balance Sheet: The company has a double-A-rated fortress balance sheet.

Cons:

- Dependence on Transaction Volumes: Revenue is highly reliant on trading activity, which can limit growth opportunities.

- Volatility Sensitivity: While benefiting from volatility, CME’s stock price is still dependent on market sentiment.

Q2 2024 Earnings Call Transcript")