JHVEPhoto/iStock Editorial via Getty Images

I’ve been dwelling on luxury and prestige brands. The main thesis is that luxury brands are great to have during negative economic events due to the persistence of the revenue streams, which are usually capable of weathering recessions with small revenue losses and quick recoveries, which translates into better stock performance in the aftermath of recessions. I have made this case for Louis Vuitton (OTCPK:LVMUY) and will now test it for L’Oréal (OTCPK:LRLCY).

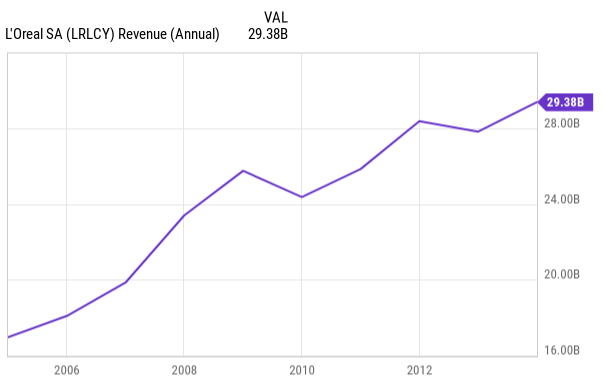

L’Oréal operates in prestige self-care beauty segments through dermatological products, cosmetics, and fragrances. Most of their segments target the high-end of self-care, and the company’s several brands have a lot of recognition and appeal among the consumers. A good way to examine the company’s revenues during the period between the subprime crisis and the European debt crisis.

YCharts

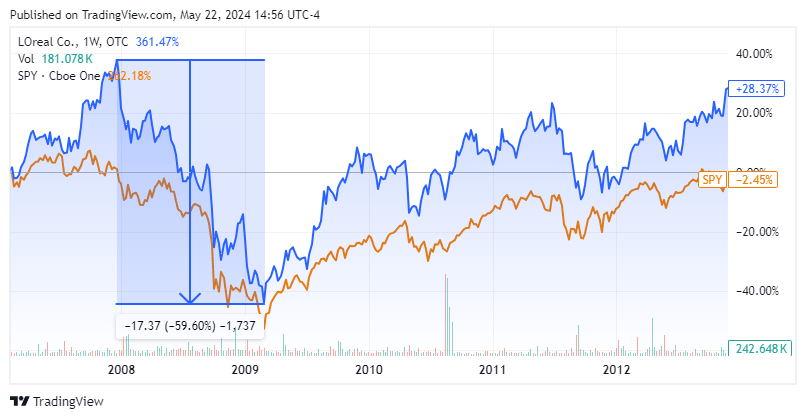

The results were very interesting. The company was capable of weathering two main financial crises with relative ease and by 2013 was already posting all-time revenue records. In terms of stock market action, during the subprime crisis from peak to valley the company lost close to 60% of its stock price. Hardly a safe haven.

Seeking Alpha

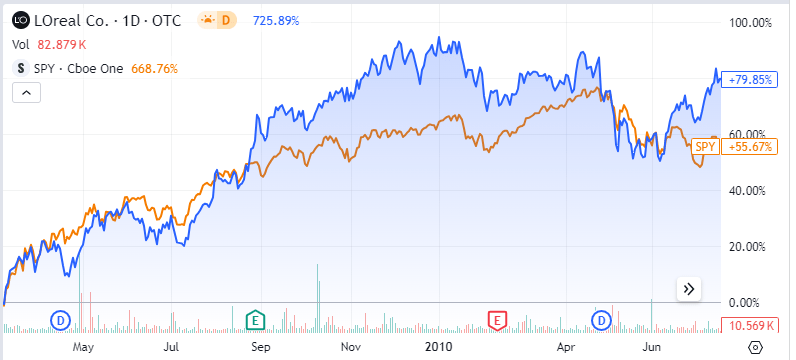

However, that result doesn’t surprise us. For those who remember the panics in 2008 and 2009, it will be recalled that these type of flight to liquidity behavior does not leave any company immune. More important to me is how fast the company was able to recover after the bottom of the general market in 2009.

Seeking Alpha

Business Model

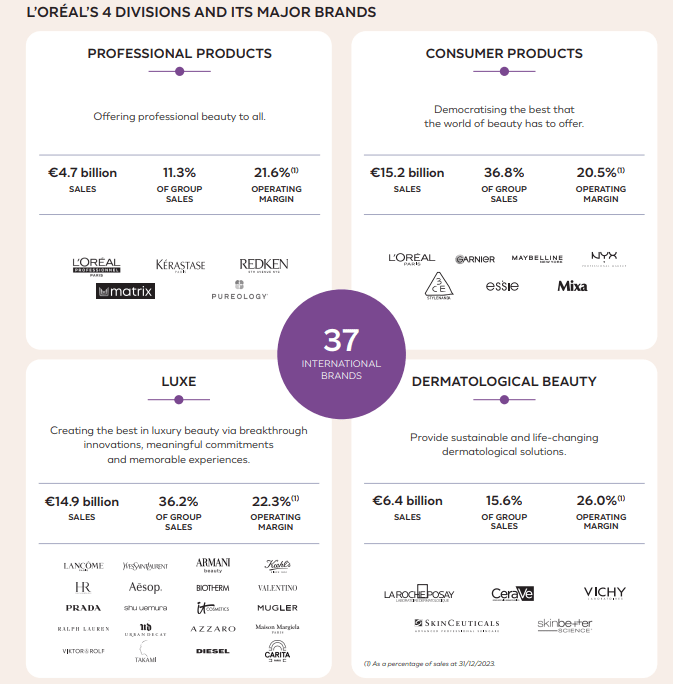

The company operates through four different divisions, each with brands catering to diverse markets. The brands share L’Oréal’s R&D platform and its extensive network of retailers, as well as publicity and advertising expertise. This interconnectedness seems to allow them to have flexibility in reallocating resources based on market traction, enabling it to reinforce what is working.

L’Oréal

One very important feature of the company’s model is acquiring early-stage brands that they think can become global players. For instance, they bought Kiehl’s in 2000 with sales of $40 million for the year, the brand crossed the $1 billion revenue line in 2016. This tells us that once a brand is acquired that’s when the brand-building work starts. After buying the brand, L’Oréal integrates it into the distribution and visibility channels of the group, while retaining the identity of the brand.

The company is also taking advantage of online channels to be able to cater to a hyper-segment beauty market. Although social media lowered the barriers to entry for new brands, the truth is that barriers to scaling up still exist. When played well, social media has the power to leverage even more big brands like L’Oréal.

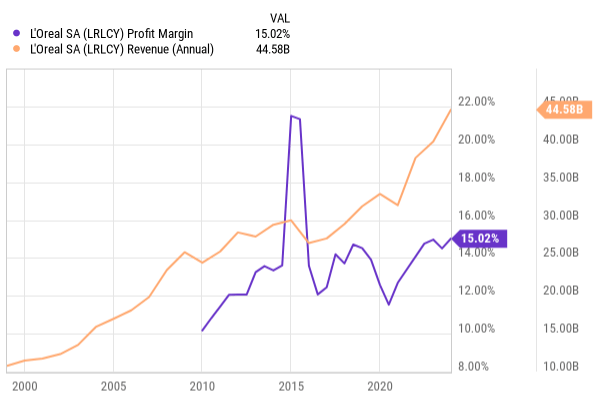

Financials

Many companies attempt brand conglomerate strategies, but most fail at it. You can see that a company fails at a brand conglomerate strategy when it holds brands for a long time without signs of growth while going on an acquisition spree that leaves the balance sheet full of debt.

In L’Oréal’s case, the strategy has worked, and the company has been able to post revenue growth over the long term while improving margins. The main reason for this should lie in the company’s ability to centralize R&D for its diverse products, while also serving as a platform to launch new brands into the spotlight. The fact that these brands cater to different market segments helps to keep their exclusivity while not giving up on conflicting consumer segments. The financial performance reflects this.

YCharts

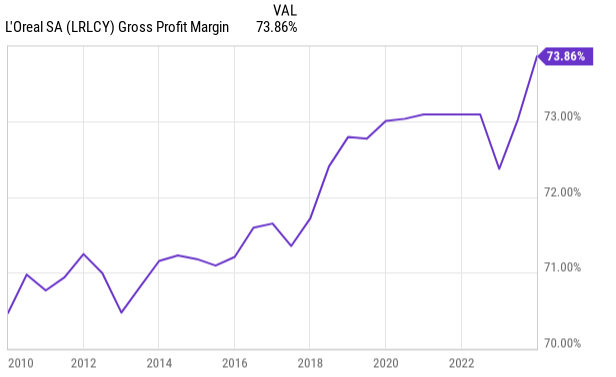

The pricing power becomes evident in the gross margin evolution through time.

YCharts

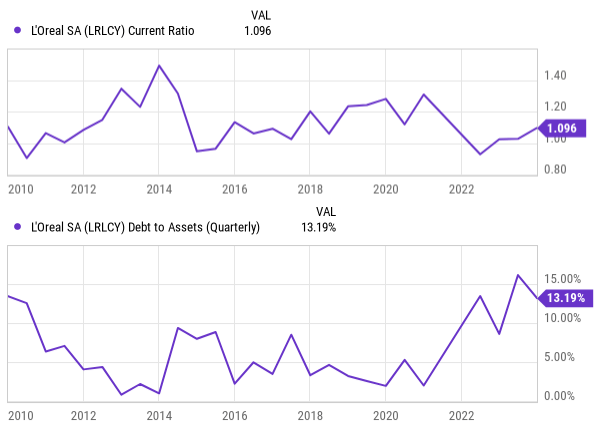

The balance sheet also reflects the strategy’s success. Even though the company has acquired several brands over the last decades, the debt-to-assets ratio is still very healthy. The current ratio is in line with the historical figures.

YCharts

The final evidence that this strategy has worked for the company is that goodwill and intangibles have grown in line with assets, meaning they didn’t accumulate too many mistakes regarding acquisitions.

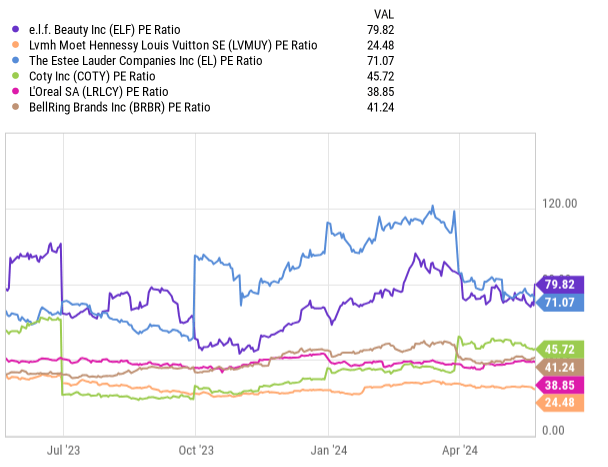

Valuation & Risks

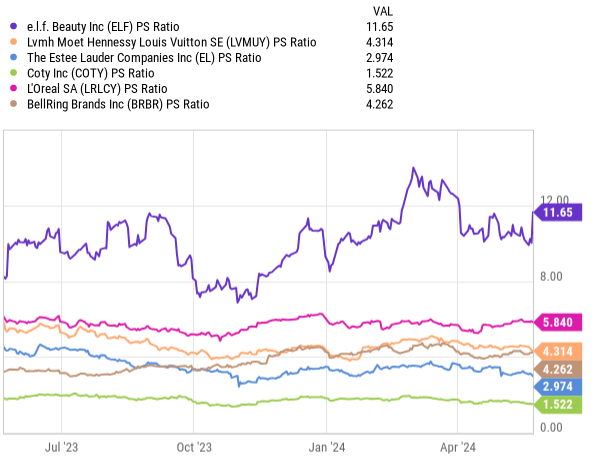

We have seen how L’Oréal works and how it has performed during the last decades. Let’s now check how the company fares in terms of valuation regarding a set of peers. The PE ratio is on the lower end of the peer list, but still 38 times earnings is not cheap.

YCharts

The sales multiple is the second highest, only trailing e.l.f. (ELF) by a wide margin. These metrics show us that this stock is clearly not trading at a discount. At best, we are talking about buying a quality company at a fair price.

YCharts

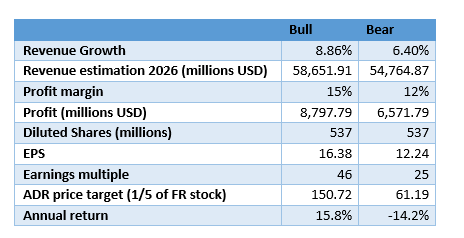

With these goalposts, we can now proceed to create a bull and bear scenario for the stock. The 10-year annual average growth rate for revenues was 6.41%, however, that has accelerated to 8.86% in the last 5 years.

Seeking Alpha

For our bull case, we will use the last 5-year rate, 8.86%, while for our bear case, we will use the 10-year rate, 6.41%. Additionally, for the bull case we will use a 15% profit margin, while for the bear case, we will use 12%. Finally, the earnings multiple for the bull case will be 46 (we used Coty as a reference), while for the bear case, it will be 24, (we used Louis Vuitton as a reference). Please, bear in mind that one LRLCY ADR share is equivalent to one-fifth of the France-based stock.

Author’s computations

These results suggest a slightly positive asymmetry, but the difference is not big. This means that the current price does not offer a margin of safety against the materialization of risks to our thesis. A couple of major risks come to mind. One of the most troubling is changing consumer preferences that could hinder one or more of the company’s brands. In a more extreme scenario, we can even envisage a disruption to the luxury and prestige markets coming from a new form of digital retail facilitated by social media.

Another important risk would be the inability to keep adding brands successfully to the portfolio. That could result in a scenario where the company’s profitability suffers, and the balance sheet gets bloated with debt.

On a more granular level, there is always the risk that one acquisition goes wrong, and the company ends up suffering during a short period from write-offs and financial losses. One has to bear in mind that there is a limit to how many brands a management team can efficiently hold and that successful management tends to get ossified and lose grip on the business.

So far, we have seen the company execute impeccably over the past decades. Even today, we don’t see evident signs that the management team is losing grip on the business. If anything, during the last 3 years the company’s revenues have even accelerated. Given that the prestige market has huge pricing power and the current macro setup seems inflationary, it might be wise to pay a fair price for this company and include it in a portfolio, therefore I am rating it a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")