bjdlzx

The last article on Logan Energy (OTCPK:LOECF) mentioned that experienced management is probably the best help in a situation like this. That experience came in very handy when there was a pipe failure which took nearly 1 thousand BOED offline in the first quarter. In a larger company, someone picks up the phone and makes a call for another department to handle it. Here, management has to “roll up their sleeves and get their hands dirty” as there is really no one else. There are far fewer employees that tend to be a “jack-of-all-trades” to keep something like this from being a major problem that wrecks the quarter. In the end, wells were drilled and lots of measures still pointed up despite the challenge as the startup year continues.

First Quarter Summary

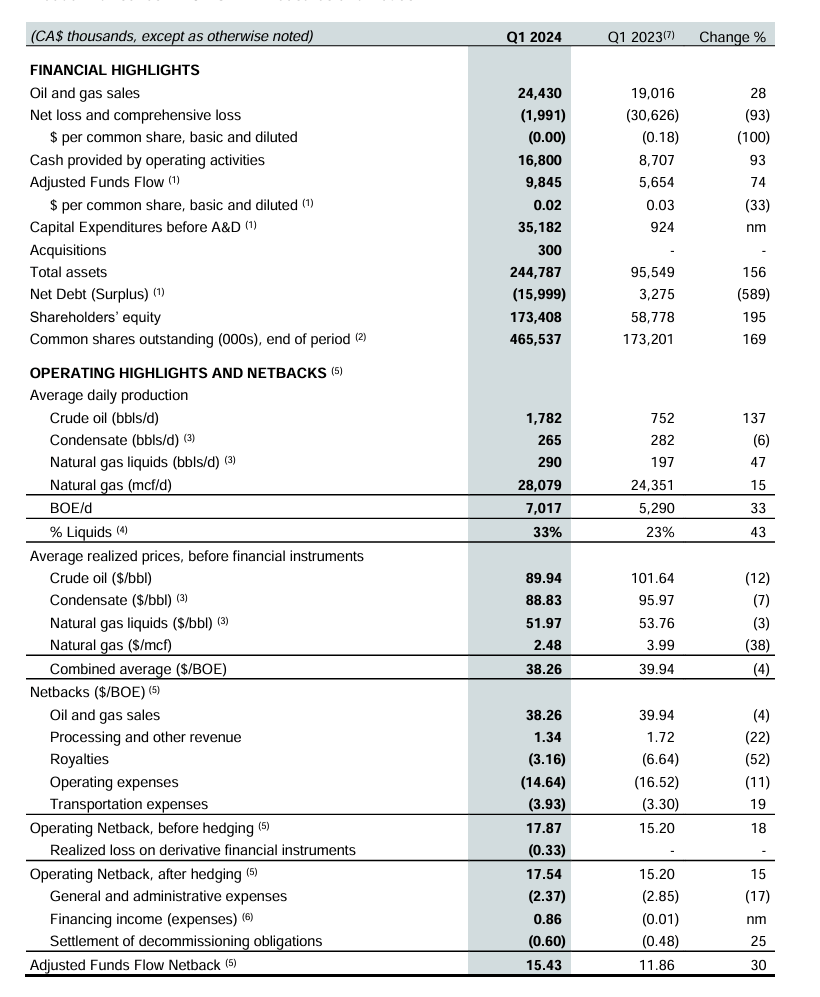

The first quarter made solid progress over the first quarter last year. Notice that despite the first quarter production that was offline, both production and (more importantly) cash flow are up compared to the previous fiscal year.

Adjusted cash flow is probably the number to use when gauging progress because the GAAP number gets a boost from selling natural gas at considerably higher prices a year ago while billing at the lower prices presently to show a big drop in the accounts receivable balance.

One consideration is that this company did not exist in the first quarter of last year. Therefore, what is in the first quarter column for fiscal year 2023 is likely a representation constructed from the previous company records before the spinoff. That has to be looked at with the idea it was not a priority for previous management at the time. This management has made these leases a primary focus area.

Logan Energy First Quarter 2024 Summary Of Results (Logan Energy First Quarter 2024 Earnings Press Release)

Note that the production still increased despite an unexpected accident of a pipe failure. Sometimes during startup, production is so concentrated that a failure like that could materially interrupt the growth goals. It certainly did slow progress. But the growth story remained intact.

Furthermore, management materially increased the liquids content of production. Investors need to keep in mind that the established production on these properties was done with an older technology. Therefore, the newer wells may or may not follow the older wells to gassier production.

As will be noted later, the latest wells are completed deeper in the formation to tap into more liquids. That could prove to be anything from a temporary advantage to a permanent one. Future cash flows are likely to heavily depend upon that outcome.

The liquids are actually a majority of the sales dollars. Therefore, every percentage increase in liquids, especially oil, is likely to prove very important. It will likely be important even more so as the production ages and total production declines.

Management essentially has results at breakeven because the loss is accounted for by the derivative valuation process, which is noncash. That points to a very favorable breakeven point (and hence a very tight control on costs).

Some of those expenses will be gyrating until there are enough wells for a stable average. Even on good acreage, well results will vary, as will the accompanying costs. The fact that acreage is good or even great does not mean there will not be a lemon or two somewhere along the line.

That is just part of the upstream business. Most of the time, investors do not see that when a company does (for example) 30 wells in a quarter because that lemon would have offsets. That will not be the case here for a little bit. There will be exploration wells and those risks will show from time to time quarterly for probably the first year or two. But the acreage appears to be good enough that such a problem will relatively quickly be overcome through larger operations as planned by management.

The funds flow grew even with the expenses of a pipe failure and the relatively low production at this stage of the company development. The profitability demonstrated by that increase points to a minimal need for debt in the early stages of production build. Therefore, a continued strong balance sheet appears to be a reasonable expectation going forward.

Cash Burn

Based upon the information in the last article and in the current company presentation, this management and the board as well, would likely be classified as serial company starters.

Based upon the experience of the management group, the company already has a substantial bank line. There is really a very reduced risk that the company would run out of money. In fact, that risk is about as close to zero as an upstream management can get.

Right now, management is projecting to need to borrow an amount that is equal to about one-half of the current annualized cash flow rate. There are more wells already drilled that will come online during the heating season to provide still more cash flow. Right now, there are no cash worries.

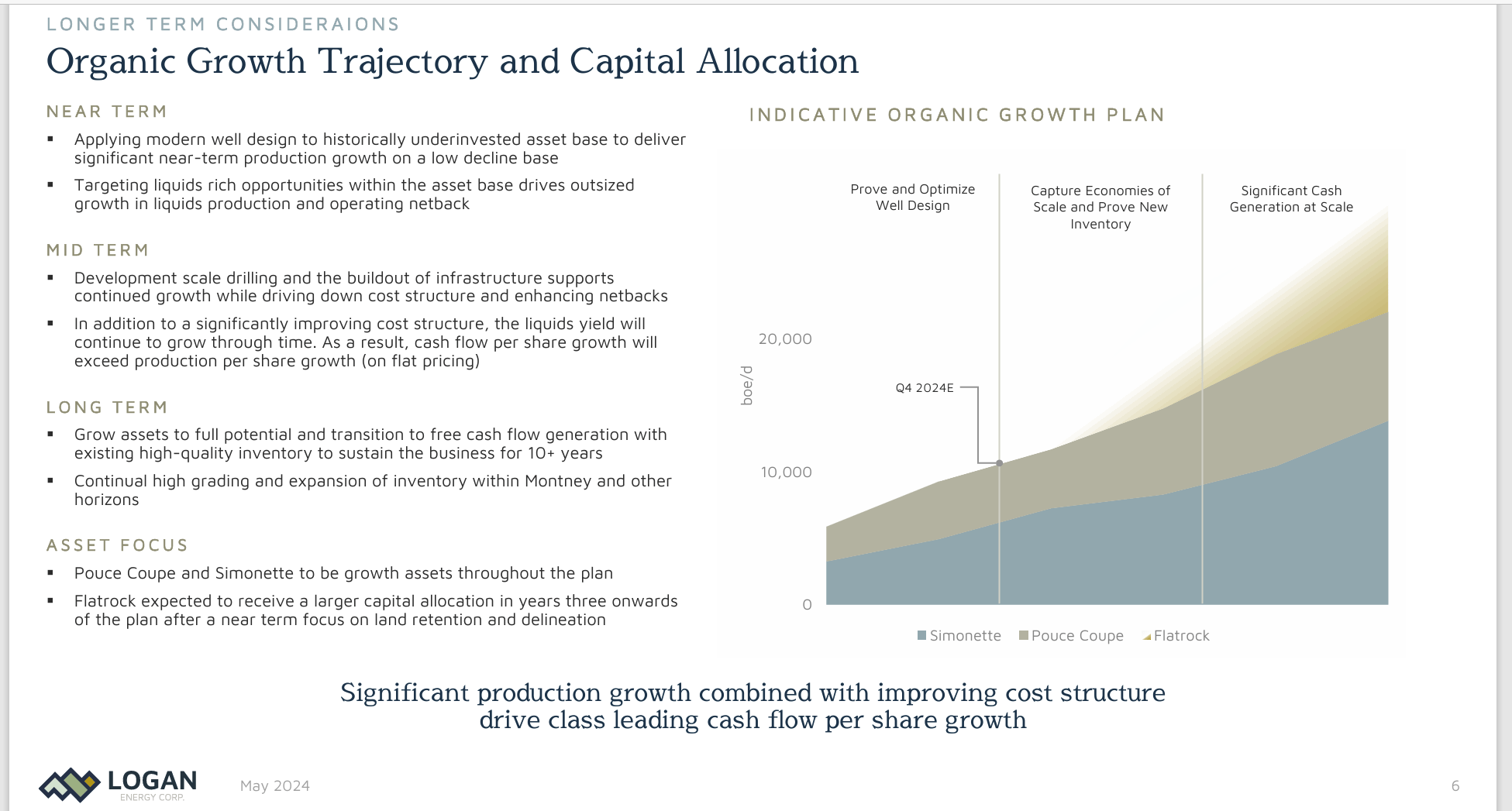

Initial Strategy

Here is the overall plan. Despite the first quarter issues, this plan appears to be mainly intact.

Logan Energy Organic Growth Strategy (Logan Energy May 2024 Corporate Presentation)

The main correction to the guidance for the fiscal year is that so far natural gas prices are weaker than expected. But with the overall plan to increase the amount of liquids in the production mix, it makes sense to not change the plan.

This does mean that management plans on borrowing a little bit more than originally planned. But that can change with a La Niña summer and winter supposedly in the forecast (at least for now).

The second quarter is likely to have much lower activity because of Spring Breakup in Canada. But then again, bringing on production of more natural gas in time for the heating season has long been a preferred industry practice.

The time of relatively low activity could result in material guidance changes for the second half of the fiscal year. The one thing that Spring Breakup often causes is a “full stop” to some activities. Therefore, psychologically, management has an actual break to fully evaluate industry conditions. This is very different from the United States, where things keep going most of the year (and therefore there is not that “full stop” to some activities).

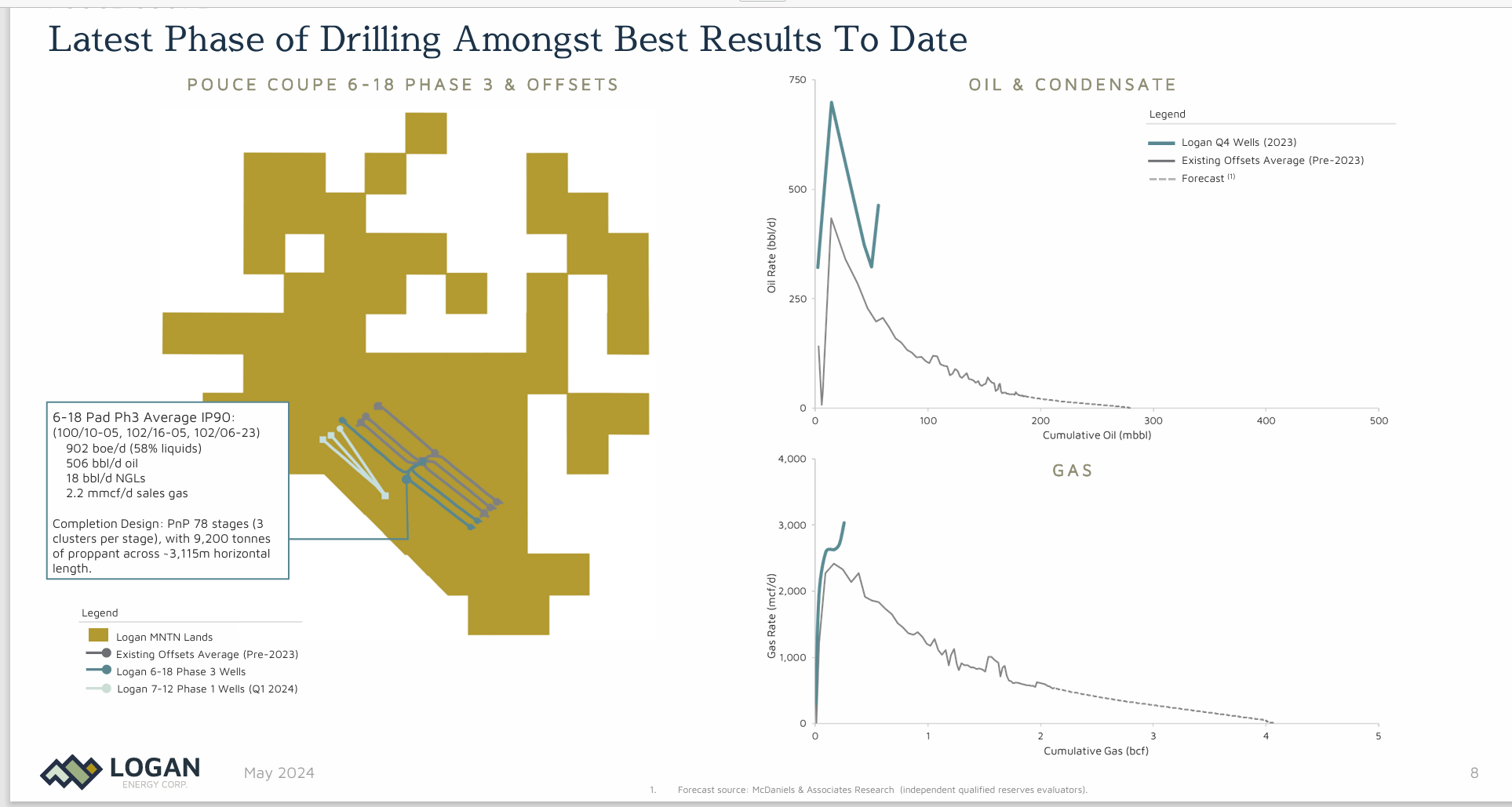

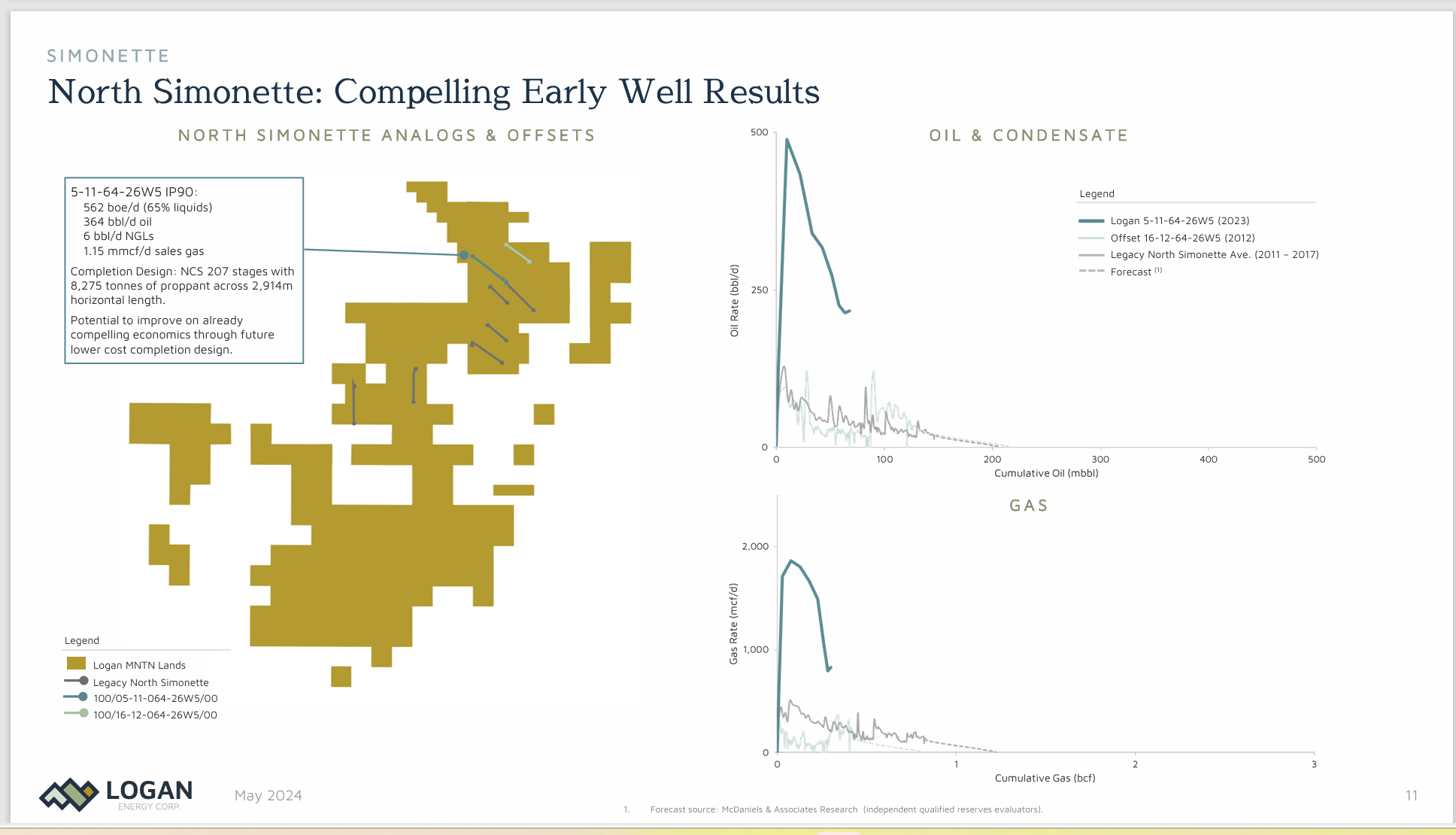

Latest Well Results

Management largely became interested in the acreage because they thought they could produce materially better results. This would, in effect, “revolutionize the play” after years of production at a certain level. One example is shown below:

Logan Energy Organic Growth Strategy (Logan Energy May 2024, Corporate Presentation)

As shown above, the increase in liquids production is what is important, as that is far more valuable than the natural gas production. It is particularly important to aim for light oil and condensate production, as those are the most valuable products to produce. They can often increase the profitability of a well materially over the older designs.

The other consideration is the value of the products produced compared to the well costs so that the payback is as short as possible. This management is looking for cash flow. Therefore, the faster the payback period, the more wells that can be drilled with the same capital. Then the company gets off to a relatively fast start with low debt. The result of this is that many times, the amount of projected oil and condensate production often has an outsized effect upon whether the well is a “go or no go” decision.

Logan Energy Production Results Well Design Comparison With Older Wells (Logan Energy May 2024, Corporate Presentation)

Here is an area with a higher liquids percentage of production. However, what usually determines capital competition results is the payback period and well profitability as measured by management. That normally means the production curve for valuable products like oil and condensate will largely determine the profitability for an area. The production mix itself is a secondary consideration.

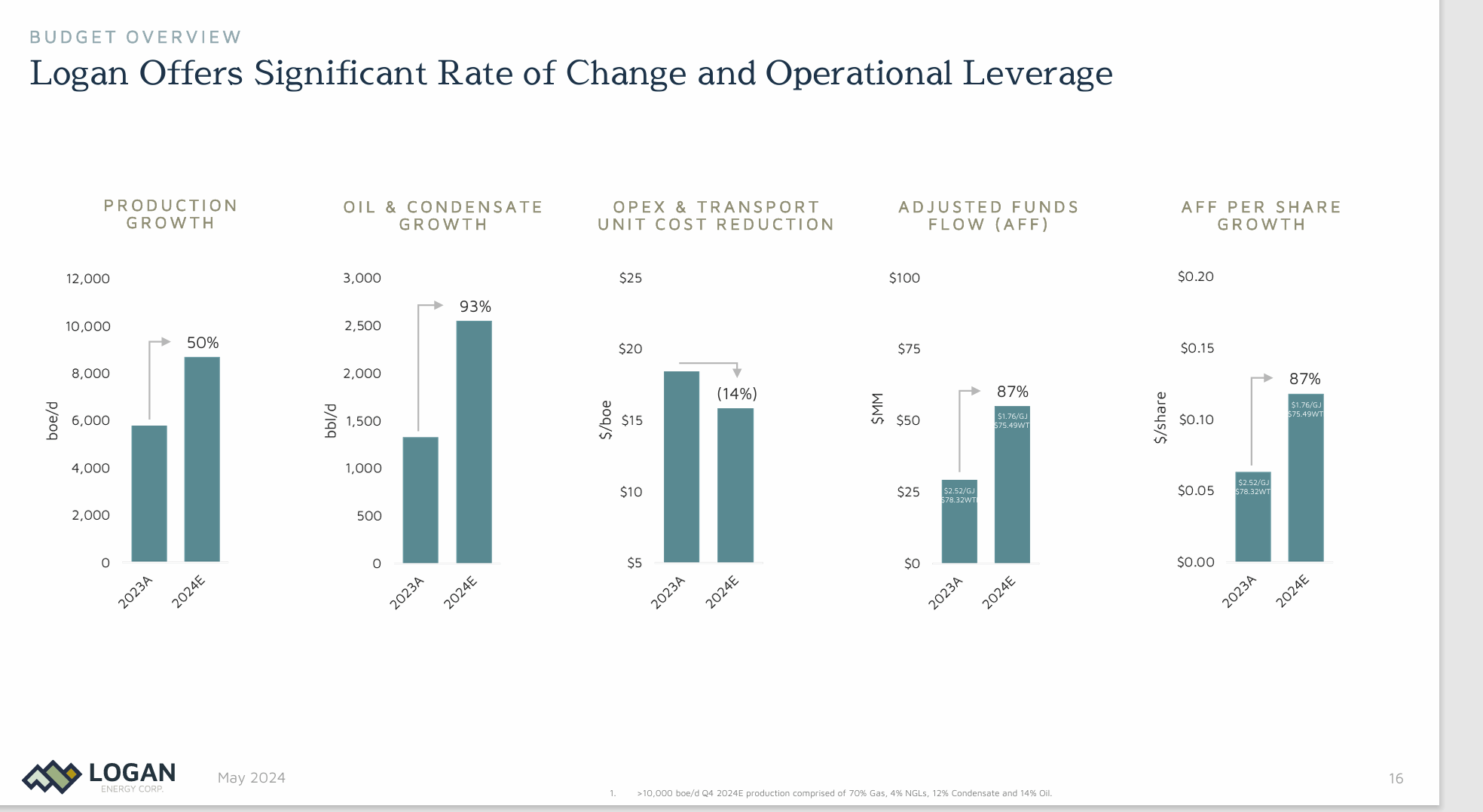

The Guided Results

Management believes that the 2024 budget is still on track. Most managements build some “slack” into the budget for all those unforeseen things that can happen. That appears to be the case here, as the first quarter did not really result in a material change to plans (so far).

That can confuse a lot of investors who often hear about production mix. But many times, that production mix discussion “assumes” a level well production for comparison purposes. That is often not the case. Hence, managements often focus upon the valuable liquids production.

Logan Energy 2024 Guidance Compared To 2023 Actual (Logan Energy May 2024, Corporate Presentation)

The second quarter will likely be the weakest progress towards the full-year goals. Probably the most important part of any plan for a natural gas producer is to have as much production as possible ready to go for the important heating season. For a company as small as this one, there is an excellent chance of meeting that goal as the heating season really gets underway months after Spring Breakup, even if it lasts longer than expected.

That means that the growth during the third and fourth quarters are likely to make up the most significant progress for the fiscal year.

The above graphs also would tend to imply an exit rate significantly above the annual average production. That means that next year would begin at a significantly higher cash flow rate.

This company, despite the low stock price, rates a speculative strong buy as it is a legitimate growth company in the part of the market known for a lot of stocks that are nothing close to legitimate. This management has built and sold companies before (as was shown in the last article and is still in the current presentation). That experience is being demonstrated with the results so far.

Risks

Any upstream company is subject to the volatility and low future visibility of upstream commodity prices. Any unexpected severe and sustained downturn could materially alter the future outlook.

The periodic technological advances that sweep the industry could stop at any time. This management appears to be counting upon using those advances to the advantage of shareholders on the current lease-holdings. But that could prove not to be the case in the future.

The loss of a key person could materially set back this company both financially and slow the future growth plans.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")