Abstract Aerial Art

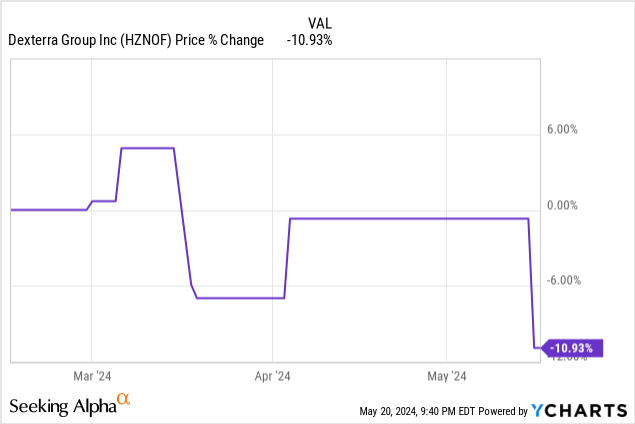

In the last year, Dexterra (OTCPK:HZNOF) (TSX:DXT:CA) traded in a narrow range between $5.40 and $6.00. Whenever shares touched around $6.00, selling pressure would send the stock price lower. Since I last wrote about Dexterra, the stock lost 5.52% excluding dividends, compared to the S&P 500’s return of 11.23%.

Last week, the company posted first-quarter results. It lost C$0.06 a share as revenue increased by 7.2% Y/Y to C$231.64 million. Why did markets react negatively to the report? Shares are down 10%.

First Quarter Results

In Q1, Dexterra Group attributed the revenue growth to new contract wins in Integrated Facility Management (“IFM”) and activity in Workforce Accommodations & Forestry and Energy Services (“WAFES”). Adjusted EBITDA of $19.6 million was similar to year-ago results. Workforce accommodation activity fell due to normal seasonal patterns. Fortunately, matting activity increased, as did IFM from both CMI Management and the defense sector.

Financial Highlights

Dexterra achieved a free cash flow of $10.6 million, up from a deficit of $5.1 million last year. The firm benefited from strong collections and a drop in inventory levels. It converted its adjusted EBITDA to FCF at 54%. This enabled it to buy back 279,300 shares at a weighted average price of $5.91 a share. The Board approved the buyback. As a result, the firm will buy back up to 165,600 shares.

The company posted a net loss of $3.6 million. This included the Modular discontinued operations loss of $8 million. Additionally, Dexterra incurred rework and remediation costs for its social affordable housing projects.

On the balance sheet, Dexterra’s debt increased to $132.7 million, up from $89.6 million. It rose because of related funding for the CMI acquisition, along with capital expenditures of $5.7 million.

Opportunities

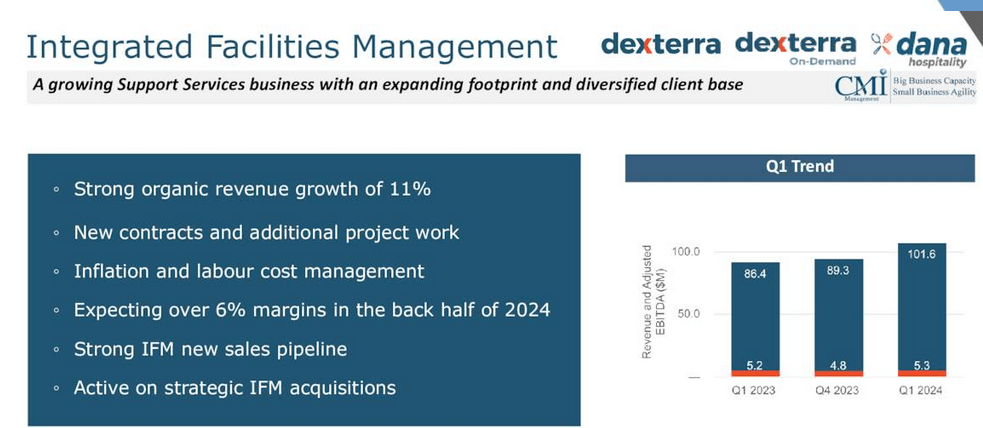

Dexterra has growth potential in IFM. Revenue grew organically by 11%. Margins of over 6% are sustainable as the firm manages inflation and labor costs. CEO Mark Becker said that inflation is starting to abate. Pressure from labor costs continues for a few years. As a result, the company will focus on managing those two costs.

Dexterra Group

In the slide above, the company identified a strong new sales pipeline and strategic IFM acquisitions as growth catalysts. For 2024, management has a goal of continuing to build its IFM and WAFES business that is competitive for the long term.

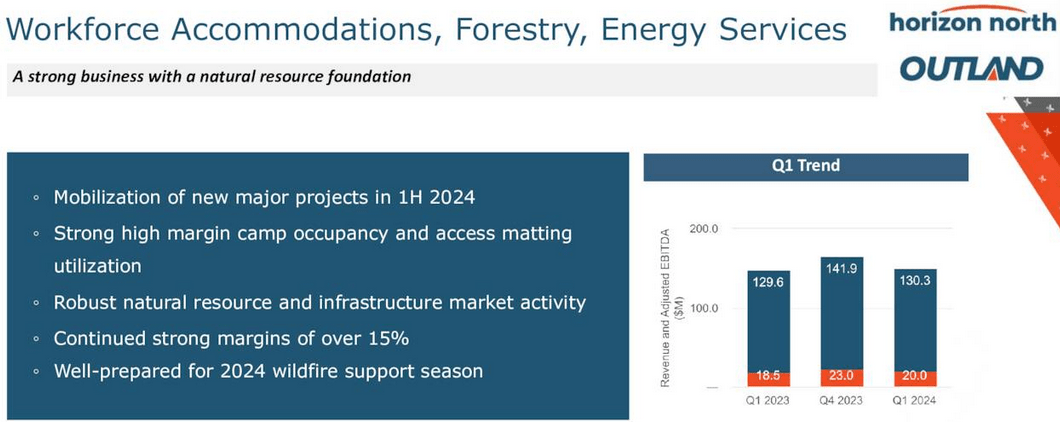

New major projects in the first half of this year are a growth catalyst for WAFES. Margins of over 15% are sustainable, above that of IFM.

Dexterra Group

While the company identified large key projects from LNG Canada and Coastal GasLink winding down, it saw several large new contracts initiated in the first quarter. It expects to have operational contracts by the end of the second quarter. HZNOF stock fell after Q1 results as investors doubted the new work.

Above: HZNOF stock in the last three months.

Expect Dexterra to deliver on increased utilization, margin expansion, and revenue growth. Activity levels in all segments of the Workforce accommodation services show signs of positive momentum in 2024. Furthermore, the company has favorable seasonality ahead. The tree planting season is underway. Last year, tree planting volumes were at around 31 million trees. Expect similar volumes this year.

The wildfire season is underway, too. Dexterra supports communities through its contracts with fire-based support camps.

Risks

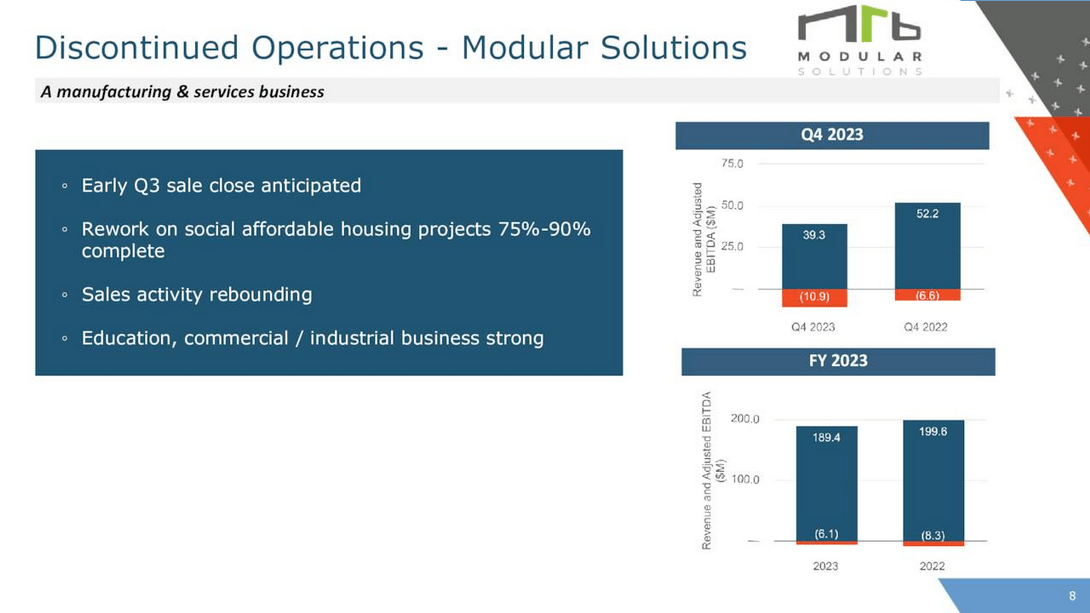

Dexterra sold its modular business. Although it expects an early Q3 sale, any delay risks distracting management. On the conference call, Chief Executive Officer Mark Becker said that projects are at 75% to 90% completion. It will complete most of the work by the end of the second quarter. At worst, it may have a few carryover work activities into the third quarter.

The business lost $8 million in Q1 due to remediation and rework activity. The firm needed to rework some of its lump-sum turnkey social affordable housing projects in Ontario.

Dexterra Group

Fortunately, the projects are up to 90% complete.

When Dexterra closes the modular unit sale, it will use the proceeds to reduce its debt level significantly. Its debt level will fall below one time’s an adjusted EBITDA from continuing operations.

Your Takeaway

Dexterra is positioned to stay on a strategic path for acquisitions. Once it closes the modular unit sale, its balance sheet will improve. Expect management to take a disciplined approach to acquisitions. One that is within its capability and complements its platform would add meaningfully to its growth over the next year.

In the near term, shareholders benefit from the stock buyback, regular dividends, and the reduction in the company’s debt levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")