Radachynskyi

WFC stock: uneven 2024 Q1 results

Wells Fargo’s (NYSE:WFC) operating results were uneven in the first quarter of 2024 in my view. And the thesis of this article is to argue why such results point to an uncertain outlook in the next 1~2 years and make the stock a HOLD under current conditions.

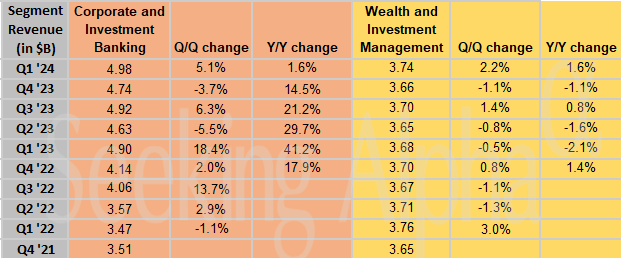

At a global level, the bank beat market expectations on both lines with non-GAAP EPS of $1.26 (which beats market expectations by $0.17) and total revenue of $20.86B (which beats market expectations by $710M). However, digging into the financials a bit deeper, its net interest income pulled back 8% in the March 2024 quarter from the prior-year period, due to lower average loan balances (down 2%) and a narrower net interest margin (down 39 basis points, to 2.81%). But, on the other hand, noninterest income advanced 17% in the first quarter. The key drivers here include higher investing banking fees, wealth and investment advisory fees (see the table below), deposit-related income, and gains on trading activity. On balance, earnings per share were nominally lower to open the year, dipping from $1.23 to $1.20. The company’s performance metrics have been a mixed bag as well. Credit quality weakened in the first quarter, with net charge-offs at 0.50% (versus 0.26% a year ago), the allowance for loan losses at 1.56% (compared with 1.38% in 2023), and nonperforming assets at 0.89% (up from 0.65%).

Seeking Alpha

WFC stock: profitability metrics and outlook

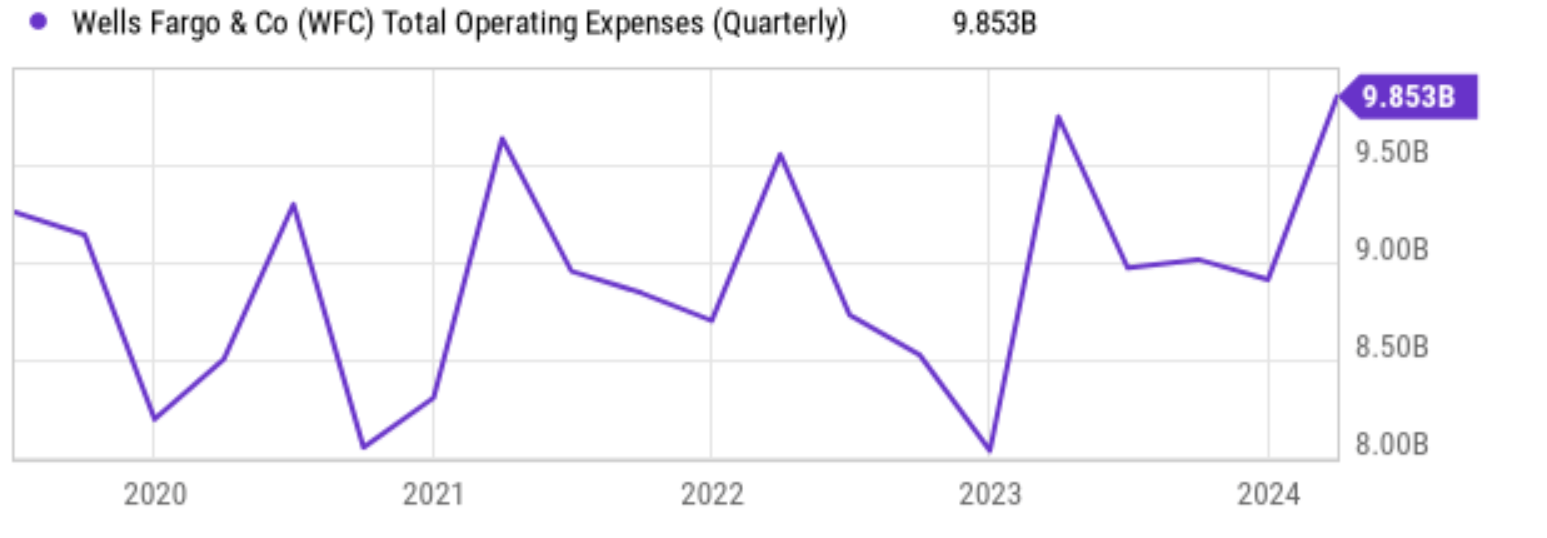

Looking ahead, I see many of the headwinds from Q1 persist in the next 1 or 2 years. As a result, I expect earnings per share to retreat in the income year (FY 2023). To be completely fair, part of the retreat is due to the tough comparison set by FY 2023’s results, which set an all-time high EPS. But part of this retreat is also due to the macroeconomic headwinds. For these headwinds, I do not expect its earnings to stage a full recovery to the 2023 level in the next 1~2 years. I anticipate the loan portfolio to slightly decline (say 1%–2% ) as Wells Fargo continues to tighten its lending standards. I expect net interest income to largely stay flat due to the combined effects of loan size decline and better credit quality on the loans. Rising operating expenses are another source of profitability pressure which I anticipate persisting given the elevated inflation and labor costs. More specifically, the chart below shows the operating expenses for WFC stock in the recent few years. As seen, despite some seasonal fluctuations, the bank’s operating expenses have been on an overall upward trend and the past quarter’s expenses were a record high in recent years.

(see the chart below).

Seeking Alpha

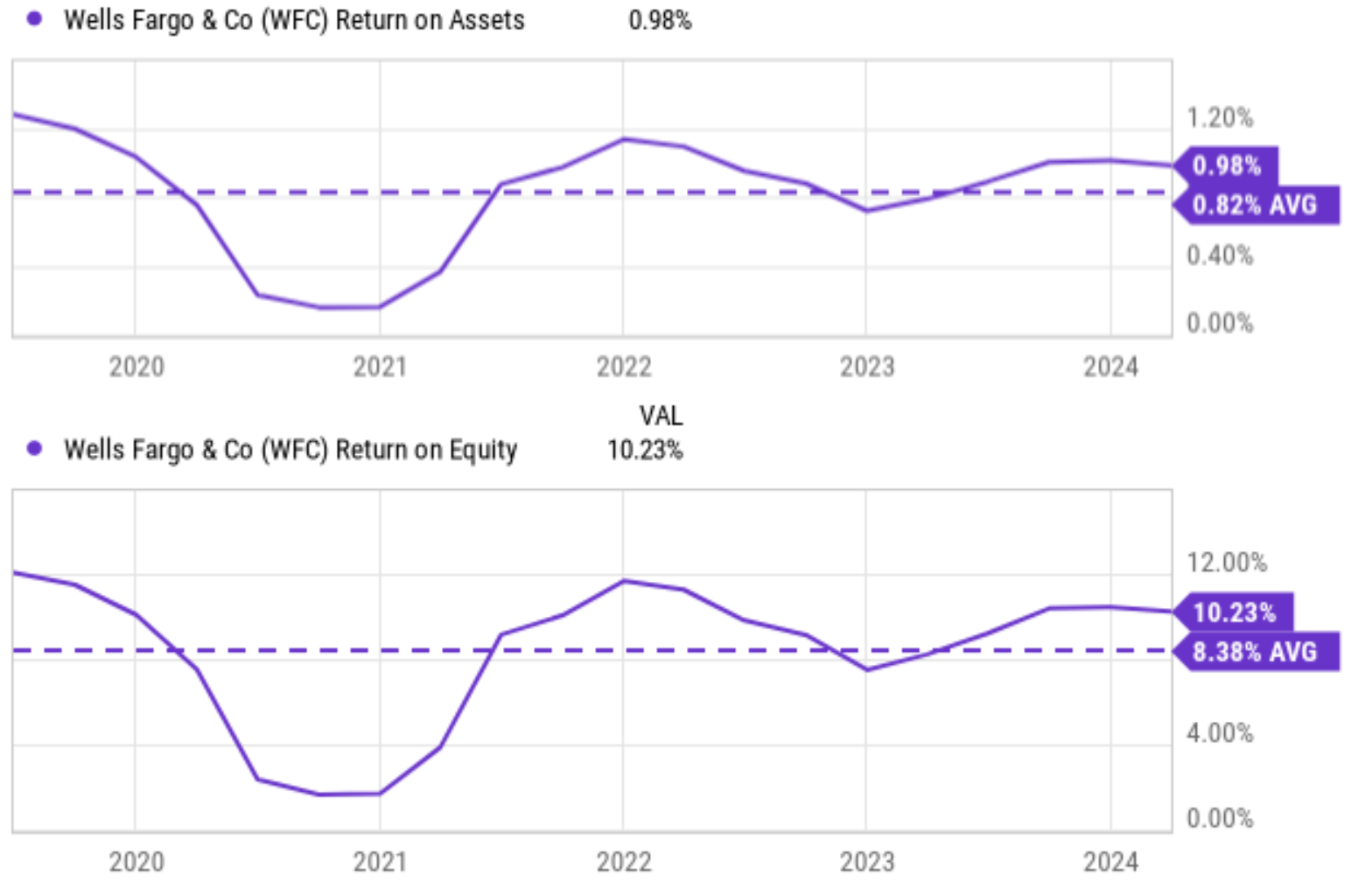

On the positive side, WFC’s financial measures remained sound, with the common equity Tier-1 capital ratio expanding from 10.8% to 11.2%, tangible book value rising 9% to $39.17 per share, and the efficiency ratio (a lower number is better) at a solid 69%, versus 66% in the year-earlier period. The profitability metrics are also stable and slightly better than its historical means both measured by Return on Assets (“ROA”) and return on equity (“ROE). As seen in the top panel of the chart below, its ROA has fluctuated in the past, reaching as high as ~1.20% and dipping as low as ~0.2%, but the long-term average is about 0.8%. WFC’s current ROA sits at 0.98%, noticeably above its historical average and also quite close to the 1% gold standard of the banking sector. Its ROE has also displayed similar fluctuations and the historical average ROE for WFC is 8.38%. WFC’s current ROE is 10.23%, also higher than its historical average and close to the sector’s standard of 10%.

Seeking Alpha

WFC stock is overvalued

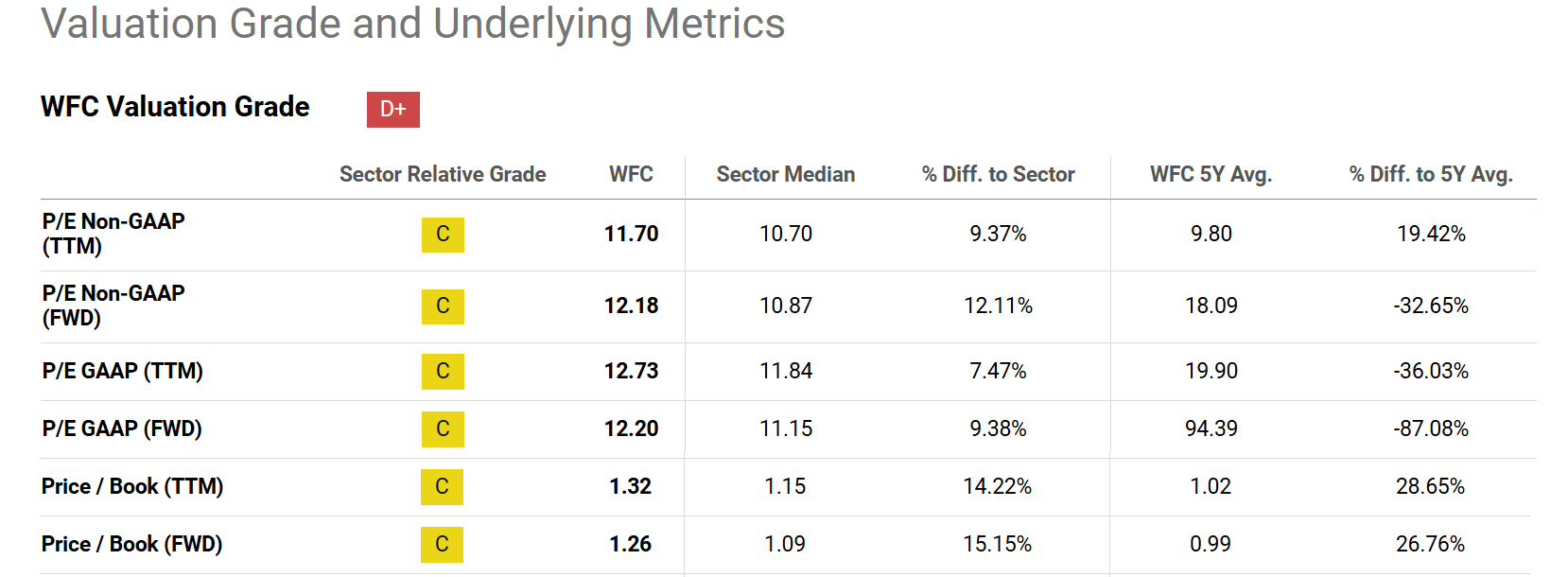

In terms of valuation, the stock is currently priced at a premium compared to its fair valuation in my view. More specifically, the following chart below summarizes WFC stock’s valuation grade.

As seen, in terms of P/E ratio, WFC’s valuation P/E ratios are modestly above the sector median. For example, its TTM P/E ratio is currently 11.70x, which is about 9% higher than the sector median of 10.70x. I think such a modest premium is totally justifiable given WFC’s scale, strength, and role as a money-center bank.

For bank valuation, I pay more attention to the price-to-book value ratio. And the numbers here point to some degree of overvaluation. As seen, on a TTM basis, its P/BV ratio sits at 1.32, which is 14.22% higher than the sector median of 1.15x. More importantly, it is also 28.65% higher than WFC’s 5-year average of 1.02x. The forward P/BV ratio paints the same picture.

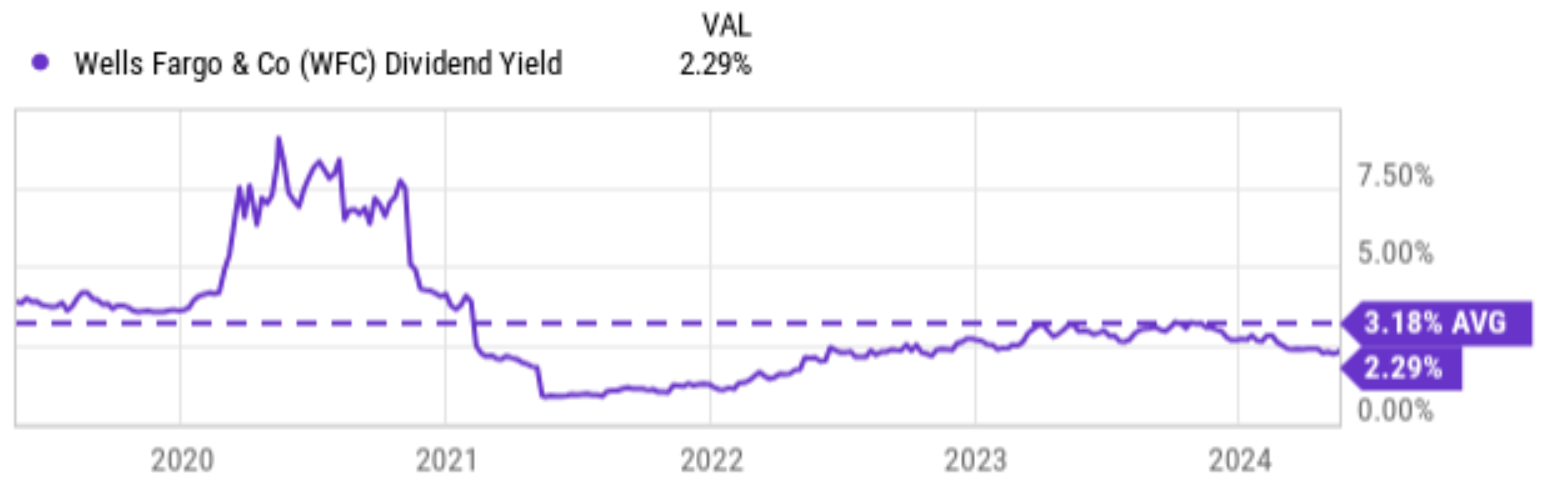

Finally, as a mature bank that pays regular dividends, its dividend yield serves as another reliable valuation metric for the long term. As seen in the second chart below, Wells Fargo’s current dividend yield is 2.29%, which is significantly lower than its historical average of 3.18%, again indicating some degree of overvaluation.

Seeking Alpha Seeking Alpha

Other risks and final thoughts

Admittedly, the risks mentioned above (loan size, operating expenses, the impact of elevated interest on profit margins, etc.) are not unique to WFC and are largely common to other banks as well. However, beyond these common risks, WFC does face some more specific challenges. The top one on my mind is the recent (or perhaps still ongoing depending on your perspective) reputational damage from past scandals, which could continue to erode customer trust and lead to higher costs associated with litigation and regulatory scrutiny. The second one on my mind was the performance of its wealth management fees. As aforementioned, this has been a key profit driver in recent quarters – largely thanks to the terrific performance of the stock market in recent years. Now, the stock market’s valuations stand at some of the most expensive levels in several decades, I do not expect the same momentum for its wealth management segment going forward. If the stock market corrects (which is very likely in my view, this could even shrink its fee as the value of its clients’ assets declines.

In summary, I see WFC as a case for a hold under its current conditions given the mixed outlook here. The bank boasts a strong financial foundation with solid profitability, as evidenced by its ROA and ROE, which are above its historical averages. However, WFC’s growth prospects appear mixed due to the factors analyzed above. Finally, its current valuation, especially in terms of P/B ratio and dividend yield, indicates some degree of overvaluation.

Q2 2024 Earnings Call Transcript")