EschCollection

The Franklin FTSE Japan ETF (NYSEARCA:FLJP) is a mostly value-weighted slice of the Japanese markets, putting a little more emphasis on some sectors like consumer discretionary as opposed to financial services. Firstly, we agree with that positioning given the Japanese Yen situation, where discretionary exports benefit from the weaker Yen. But in general, we are beginning to have some concerns about how low the Yen has gone, and believe that it is beginning to become counterproductive particularly as household outlays are just now beginning to see some sequential improvement. The issue is that there are some structural issues that may keep the Yen low in the current market set up. We did not foresee these issues in the last coverage, where we thought that the Yen would go up in accordance with BoJ plans. Nonetheless, we continue to be highly overweight Japan, with it being more than 50% of our Investment Group’s model portfolio. Although, while the FLJP may benefit some more from Yen weakness, it’s not the safest pick if the Yen gets stronger, which is possible depending on eventual rate cuts by the Fed. We have our own way of playing Japan.

Quick FLJP Breakdown

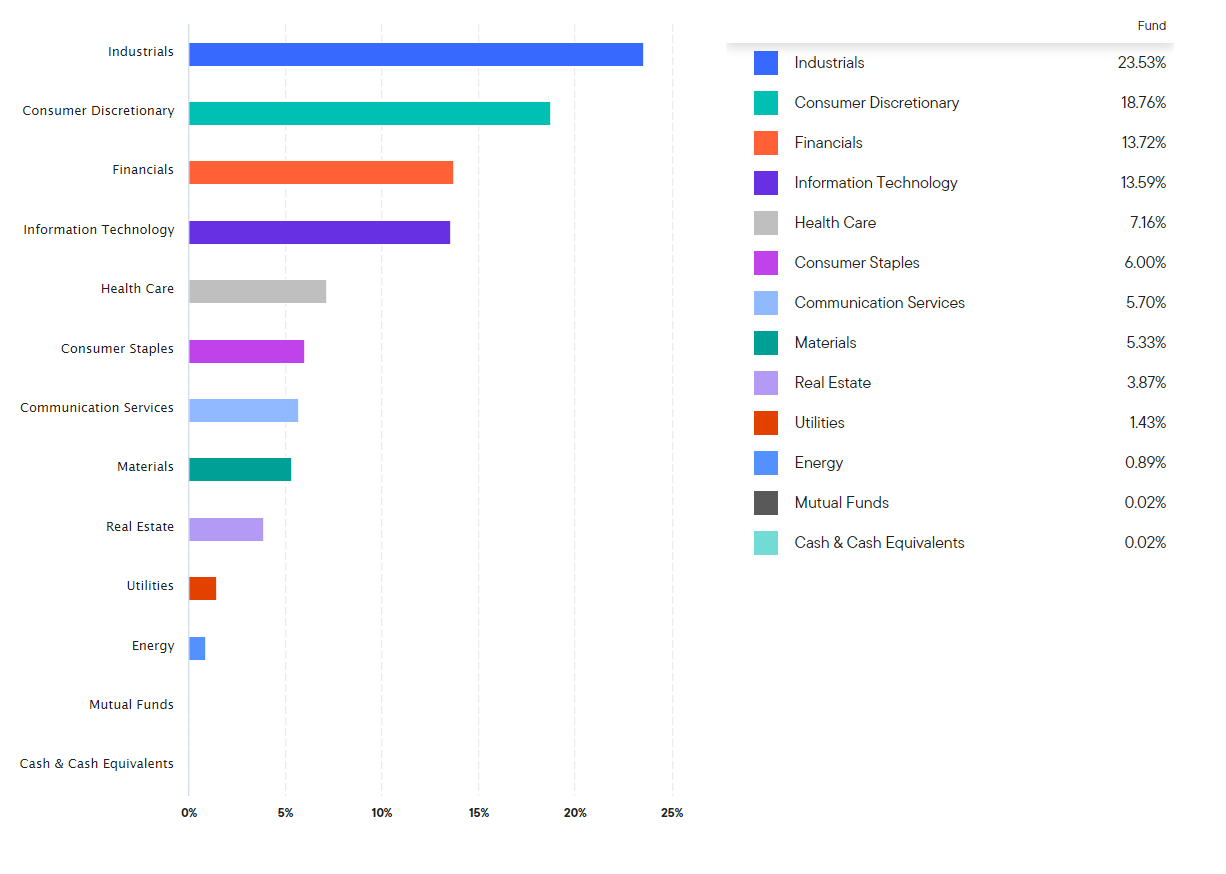

Sectors (Franklin Templeton)

The sector allocations have changed a little since our last coverage. There is less IT and more financials instead. Financials are still a lot lower in the mix than they are in the iShares Japan ETF (EWJ). There is an overall overweight in the FLJP to consumer discretionary, and overweight overall to IT even if it’s smaller, and underweight to the key industrial exposure that otherwise features highly in the EWJ.

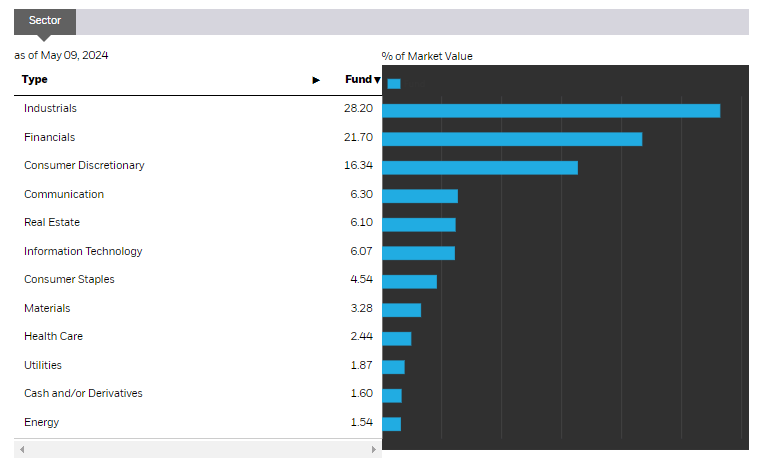

Sectors (iShares.com)

Bottom Line

We prefer the underweight to the financials, since while there are positives to Japanese financial picks, such as stronger IPO markets than in the West and more scope for secular M&A and retail engagement in markets, they are all very levered to the Yen’s performance for foreign investors and are also not being helped by a higher NIM due to still very low rates. While the BoJ raised rates, they didn’t do so by much, and the Yen has actually continued to fall since just after the rate hike announcement.

There are some structural issues with the Yen, that despite being an overcrowded short trade are difficult to tackle. The Yen is being driven low by leveraged pair trading with the dollar and other currencies that offer better local yields. In principle, a short squeeze could unwind these trades and benefit the Yen, but there are issues. It would be wise to hedge Yen exposure as a major foreign allocator while taking advantage of local undervaluation. But doing so will just put more pressure on the Yen. So the undervaluation of the markets leads to hedging activity that further weakens the Yen through non-speculative shorting.

Also, while some speculators focus on the possibility that the BoJ might intervene in markets, those interventions will likely have to be financed at some point by sales of US Treasuries. That will only raise US yields and make the pair trade more attractive for the marginal speculator.

In line with this, we also like that the FLJP is overweight consumer discretionary. While at some point a weak Yen will start noticeably inflating costs, as some components are imported, the net effect is still positive since so much of the manufacturing of automotive parts for the consumer discretionary automotive industry happens in Japan. Japanese companies’ cost bases are mostly in Japan – they’re not as outsourced to China as other nations are. We cover this frequently, a weak Yen supports market share gains and a margin wedge for consumer discretionary companies. While Industrials are underweight in FLJP, the weak Yen also helps those exposures, which are still substantial.

The IT exposures which are overweight in FLJP consist of semiconductor companies, which have been a phenomenal bet in Japan on AI and also geopolitical and strategic semiconductor considerations.

The arguments for the Japanese market continue. The PE of the Japanese market and the PE of FLJP which is 16.3x trails that of other developed markets. There is also the fact that basic financial optimsiation levers have not yet been pulled in Japan that offer low hanging fruit of value creation. The weak Yen is generally positive for the FLJP, but there is a point where it becomes counterproductive due to the effects of imported inflation, which are not negligible, particularly for Japanese household spending which remains muted. While Japanese markets and the FLJP portfolio benefits from incremental Yen weakness, there is enough domestic market exposure where you start to get a U-curve effect from a weak Yen. Moreover, the general economic makeup benefits less from a weak Yen than the FLJP exposure, so there’s also the matter that governmental entities will be making efforts to try to restore the Yen, especially as levels become alarmingly weak. Finally, the ball is in the Fed’s court as to whether the Yen gets stronger. If the US sees rate cuts, which probably is still a while off even if there are signs of weaker employment coming, the Yen shorts should start to unwind pretty dramatically considering how crowded the trade is.

For FLJP though, which has lost value since March despite continued Yen weakness, things actually look better than even the EWJ. We wouldn’t bother with an ETF though and would at this point make our own picks, particularly as large-cap has already run ahead and brought the index with it. Moreover, if the Yen eventually does make a recovery, which it must at some point, FLJP is probably not the best play.

Q2 2024 Earnings Call Transcript")