miniseries

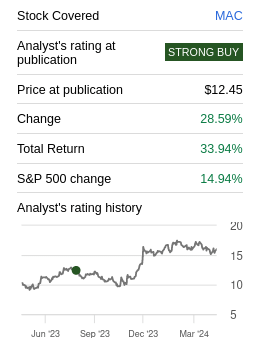

The last time we covered Macerich (NYSE:MAC) was about nine months ago, and at the time we were very optimistic given the low valuation and signs of receding headwinds. Since then, shares have outperformed even the mighty S&P 500 index (SPY) on a total return basis, by a wide margin.

Seeking Alpha

At the same time, we are less confident about the fundamentals, with interest rates increasingly looking like they will be maintained at elevated levels for longer, and the company delivering results below expectations. On April 30th the company announced Q1 2024 results, with a big miss on funds from operations (FFO), at only $0.33 compared to expectations of $0.39, and same center net operating income (NOI) had a slight decrease. Occupancy also appears to be stalling despite its robust pipeline, as it appears new tenants are mostly offsetting troubled retailers that either go bankrupt or decide to reduce their footprint. This has been particularly true for department stores like Macy’s (M), and Nordstrom (JWN) that continue pruning their store footprints and are also increasingly favoring smaller off-mall stores when they do open new locations.

Massive Headwinds

While we continue to believe that the best quality class A malls will survive, and that the media over-hyped the “death of the mall”, we do see massive headwinds. As already mentioned, traditional anchor department stores are not performing well, and many are reducing their store counts. Even luxury brand owners like LVMH (OTCPK:LVMHF) and Hermès International (OTCPK:HESAY) are being more cautious with their store openings, and some luxury brands like Kering (OTCPK:PPRUF) owned Gucci are making headlines given their significant revenue declines. Some new tenants malls had found included electric vehicle (EV) companies like Tesla (TSLA) and NIO (NIO), which were opening stores in high-end malls so consumers could see the cars and learn more about them. With current headwinds experienced by the EV industry, we expect these companies to moderate their store openings too.

A second important headwind is the high likelihood of interest rates staying at elevated levels for longer, which will mean the company will have to continue refinancing debt at more expensive rates compared with maturing bonds.

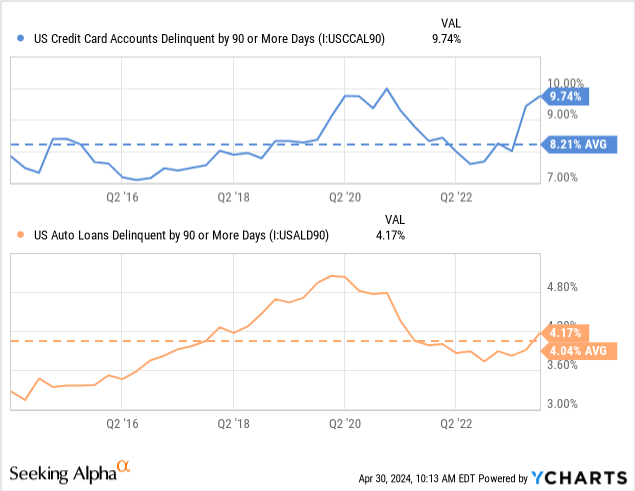

Finally, we see significant pressures on consumer spending in malls. Consumers are also being pressured by higher rates, which are reducing their discretionary income. There is also increased competition for whatever discretionary income is left, with not only the likes of Amazon (AMZN), Costco (COST), and Walmart (WMT) offering deep discounts, but now we have to add overseas Chinese competitors targeting U.S. consumer directly, such as Temu (PDD) and AliExpress (BABA) even if the quality of the products on these platforms leaves a lot to be desired. Still, some, like Shein have managed to generate massive revenue despite the low cost of the products they sell. Shein reportedly reached around $45 billion in revenue last year, despite mostly selling very low cost clothes. This is taking money from traditional mall tenants like H&M (OTCPK:HNNMY) and Zara (OTCPK:IDEXY). Making matters worse, consumers are showing signs of distress, with credit card and auto loan delinquency rates rapidly increasing.

Balance Sheet

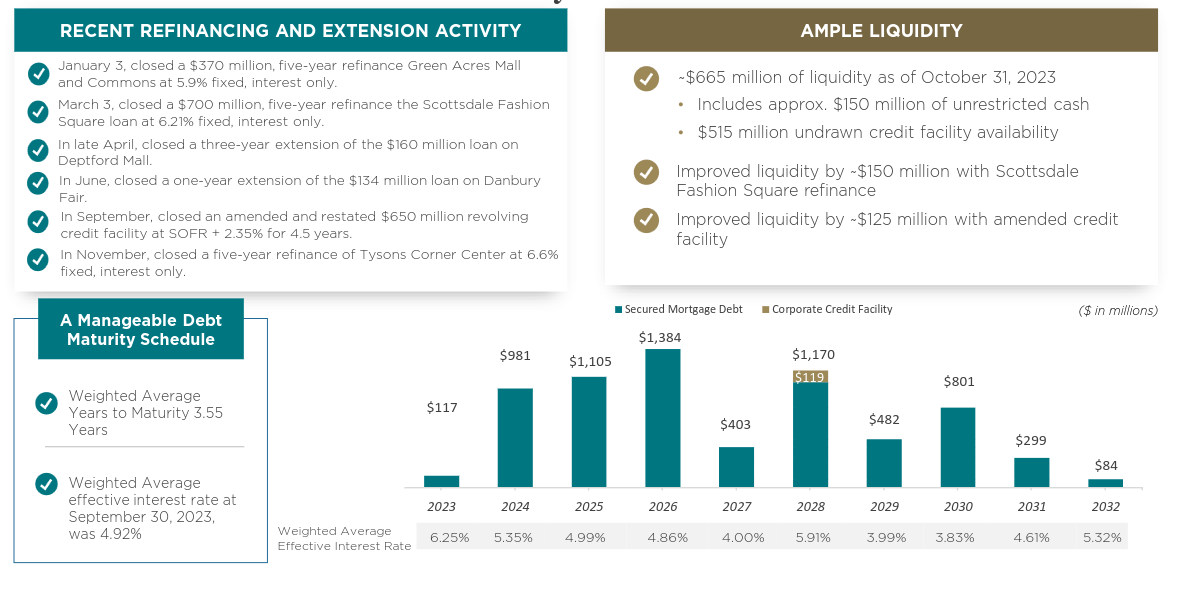

While we give credit to the company for managing well a difficult situation, the fact is that refinancing has proven expensive. Fortunately the company has generated significant liquidity, including by up-financing assets like Scottsdale Fashion Square, but this has come at the price of significantly increased interest expense.

Several refinancing transactions have been done at rates exceeding 6%, which is significantly higher compared to their weighted average interest rate which stood at less than 5% last quarter. The weighted average years to maturity is not very high either, at roughly 3.5 years, which means higher-for-longer interest rates will worsen the situation. The company has said that once the market permits they will try to elongate the maturity schedule with 10-year duration mortgages, but it is becoming less clear that the market will allow them to do this anytime soon.

Macerich Investor Presentation

Opportunity Cost

Another reason we are less enthusiastic about Macerich is the opportunity cost of investing in its shares is now higher, when many other quality REITs are currently trading at very attractive valuations, and with good dividend yields.

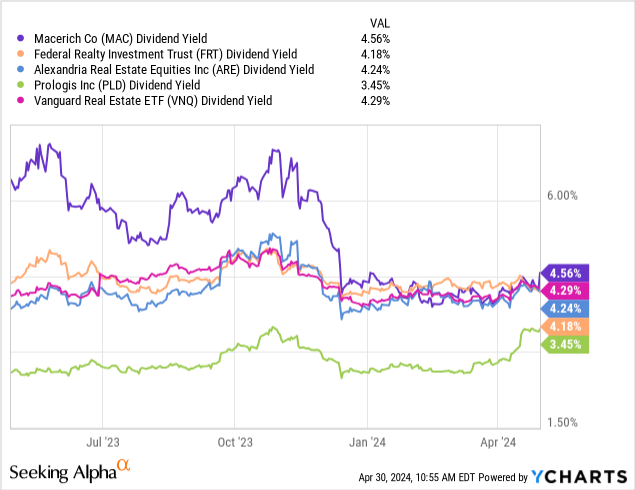

Not long ago the dividend yield Macerich was offering was substantially higher compared to other REITs. Now it is only slightly higher than the popular Vanguard Real Estate ETF (VNQ), and the difference is also very slim compared to very solid REITs like Federal Realty (FRT), Alexandria Real Estate (ARE), and Prologis (PLD), among others.

Valuation

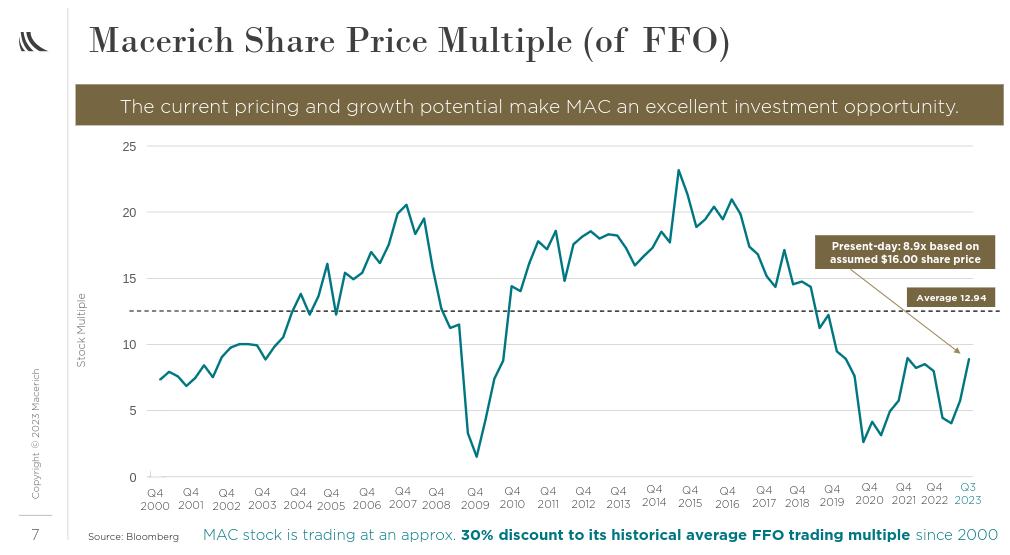

While Macerich makes the case that its historical Price/FFO multiple has been higher, around 13x, we believe that the massive headwinds should result in a lower valuation compared to its historical average. We are changing our rating to “neutral”, as shares do not appear excessively priced either. It is simply the combination of a higher valuation, increased headwinds, and more attractive alternatives that make Macerich less attractive today, compared to about a year ago.

Macerich Investor Presentation

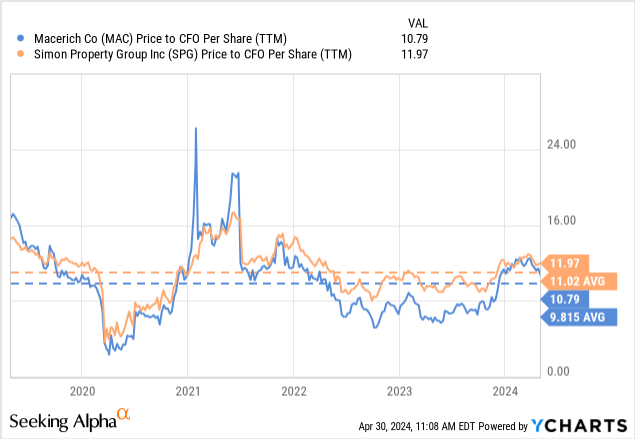

Both Macerich and its competitor Simon Property Group (SPG) are trading slightly above their 5-year average Price to Cash-flow from Operations per Share, reaffirming our belief that a “neutral” rating is appropriate.

Risks

We have already mentioned most of the risks and headwinds we see for Macerich, this includes refinancing risks, tenants facing increased competition from e-commerce platforms including Chinese apps that have grown tremendously in the past few years.

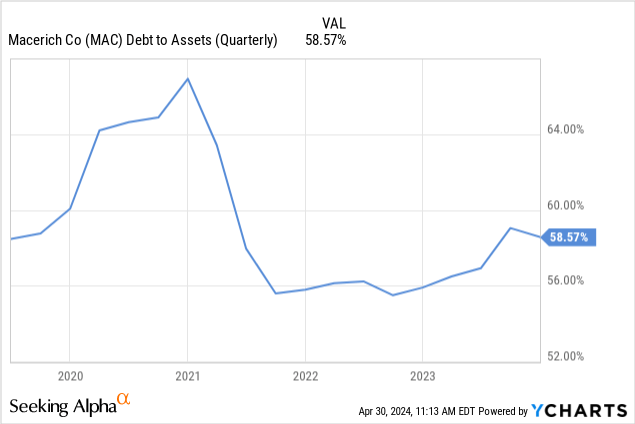

The balance sheet has been improved, but leverage remains very high, as can be seen with the company’s debt to assets ratio.

Conclusion

Macerich’s first quarter of 2024 results were disappointing, and the valuation is no longer very attractive. At the same time we see massive headwinds for the company, with increased competition and a weakened consumer. Some of the new tenant categories, like EV manufacturers will probably moderate their new store openings, while some traditional tenants like clothing and department stores have announced plans to reduce their footprints. Coupled with higher interest costs that are likely to persist for longer than most economists were previously expecting, we no longer consider shares to be attractive.

Q2 2024 Earnings Call Transcript")