stanciuc/iStock via Getty Images

Introduction

Verizon Communications (NYSE:VZ) reported their latest earnings recently, and Mr. Market apparently didn’t like the results. The stock dropped roughly $3 but has since regained some of those losses. The company has been doing all the right things, like strengthening their fundamentals, in which I’ll touch on later in this article. But for now, dividend investors should have no fear as Verizon is likely to keep making improvements in the coming months, offering shareholders some upside in the process. But for those holding the stock, don’t worry, be happy, and enjoy the dividend income while you wait.

Previous Rating

I last covered Verizon this past January in an article: Turning The Ship Around For A Favorable 2024. Since that article published, the stock saw some decent price appreciation before the market decided to bring the stock back down to earth after its Q1 earnings.

The company had been focusing on improvements to grow the business, like rolling out the myPlan offering, which was expected to contribute to subscriber growth. It worked as Verizon saw an uptick in subscribers and its postpaid & broadband segments. Furthermore, the company saw more than 125k net adds for the 9th consecutive quarter and more than 400k net adds in its broadband segment for the 3rd consecutive quarter. Fast-forward to Q1 and the company is still on the right track to deliver solid results for the year.

Latest Earnings

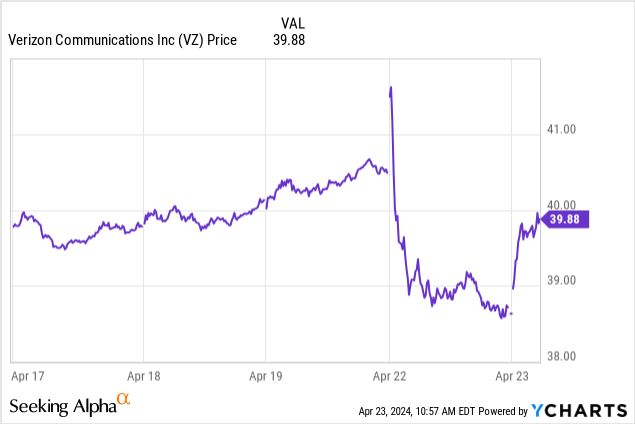

Verizon reported Q1 earnings on April 22nd and saw its share price slip to under $39 a share. Since then, the company has bounced back to roughly $40 a share, where it trades at the time of writing. In my opinion, the market overreacted to this, causing the share price to fall sharply. For me, it was nothing new or anything to worry about from the company. Honestly, the market can be tough and unpredictable on companies sometimes. Post a huge beat and the stock declines, post a miss, and sometimes you can be awarded with a higher share price. It doesn’t seem to make any sense sometimes, but hey, that’s the name of the game.

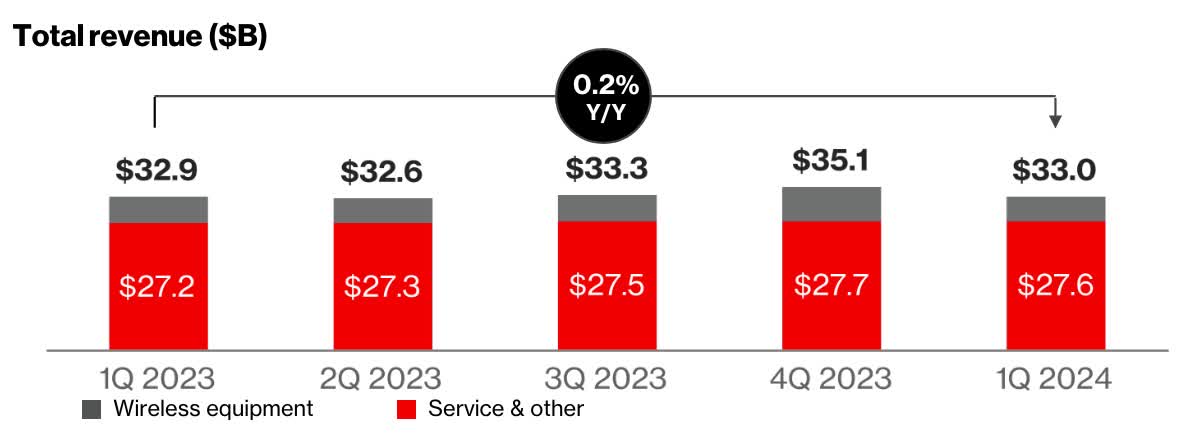

Verizon reported EPS of $1.15, beating analysts’ estimates by $0.03, but missed on revenue by $230 million. Earnings were down roughly 4% year-over-year from $1.20 while revenue of $33 billion increased slightly from $32.9 billion from Q1 ’23. This also declined quarter-over-quarter, but I expect this to creep up over the next 3 quarters, similar to 2023. However, management still expects earnings in a range of $4.50 – $4.70. Even if this comes in at the higher end, it would be a slight decline from the $4.71 the company brought in for 2023. And could be one of the reasons for the decline in share price.

Verizon investor presentation

I think this is nothing to worry about, and I expect earnings to come in somewhere between $4.65 to $4.80. I also suspect management may increase the earnings range as they get more clarity on the economic backdrop later in the year. It’s still early, and much of it is dependent on if interest rates are lowered or not.

Wireless service revenue grew 3.3% while the postpaid phone segment grew by 253,000. This improved year-over-year, and the company mentioned how its value proposition is resonating with customers. And despite a net loss of 68,000, this was still a 59,000 net loss improvement from the prior year. The broadband segment saw subscriptions grow by 389,000 over the same period.

But this was down from the 400,000+ they saw in the third quarter last year for the 3rd consecutive quarter. However, this improved from 10.3 million subscribers to 11 million in the quarter. And VZ’s broadband business continues to be a key growth engine for the telecom giant. And while these aren’t eye-catching numbers, the company is still on the right track, seeing growth in its segments.

Getting A Piece Of The AI Pie

Unless you’ve been living under a rock, you’ve probably heard about all the AI hype that’s been going on. And like many companies, Verizon expects it to be beneficial to the company going forward. Moreover, they’ve already had AI projects going live, so investors should see more of these roll out in the near future.

Their CEO Hans Vestberg touched on this during earnings:

Our AI strategy focuses on three priorities. First, optimizing internal processes and operations through machine learning, such as creating efficiencies in fuel consumption. AI is already centered to our cost transformation program and will become even more important over time. Secondly, enhancing product experiences with AI capabilities like the personalized plan recommendation on myPlan, which is producing good early results. And thirdly, establishing an AI-based revenue by commercializing our network’s unique low latency, high bandwidth, and robust mobile edge compute capabilities. Generative AI workloads represent a great long-term opportunity for us. As we expand our network and increase our performance advantage, we’re also making Verizon a more efficient organization.

Further Improvements

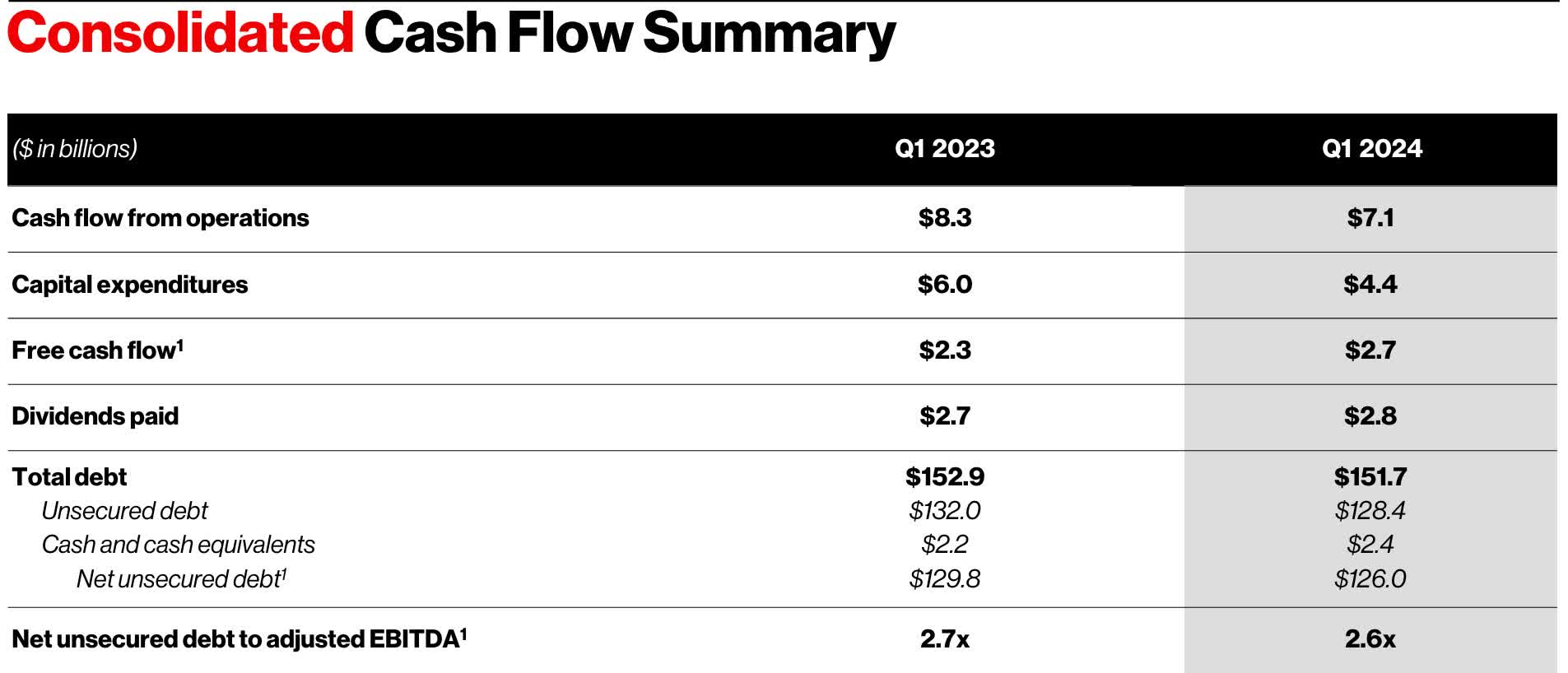

Aside from the decline in revenue, cash from operations also declined from $8.3 billion to $7.1 billion due to pressures from higher interest expenses. But thanks to further improvements in CAPEX, free cash flow increased from $2.3 billion to $2.7 billion.

Moreover, this improvement is not only essential for the company’s dividend safety, but in deleveraging efforts as well. VZ managed to decrease leverage year-over-year from 2.7x to 2.6x, with total debt down from $129.8 billion to $126 billion.

For comparison purposes, AT&T (T) had a net debt-to-adjusted EBITDA slightly below 3x and expects this to be 2.5x by 2025. Furthermore, they have $3.6 billion due this year and expect to continue decreasing their debt load, more so in the second half of the year. All in all, Verizon delivered solid first quarter results and I expect improvements in the coming quarters.

VZ investor presentation

Catalysts/Risks

With higher interest rates, this is a double-edged sword for the telecom giant. Not only does it have an impact on interest expenses, but higher rates also drag on consumer sentiment, as management mentioned the quarter was a little slow for consumers and business when it comes to wireless. And if they remain higher, and we see no rate cuts soon, this will likely continue to impact sentiment going forward.

On the other hand, if interest rates are cut as expected, then this should provide the possibility for potential upside for the company. Additionally, consumer sentiment could shift, increasing phone adds in the wireless & broadband segments. And the telecom behemoth will likely continue to roll out perks to attract new customers as the macro environment picture becomes clearer.

Collect A Near 7% Yield And Be Happy

While investors wait for lower interest rates and Verizon to offer potential upside, they also get more than a 6% yield that’s well-covered. For me, Verizon is strictly an income stock, and if it gives me some upside, then I’ll take it. But for now, I’m happy collecting a higher yield while I wait.

Furthermore, the company continues to make improvements to its free cash flow with lower capital expenditures. Management guided for a CAPEX range of $17 – $17.5 billion for the full-year, down from nearly $19 billion last year. I don’t think it’s going out on a limb here to see free cash flow of more than $20 billion for 2024. This is in comparison to peer AT&T, who expects free cash flow of $17 -$18 billion for 2024. Coupled with lower interest rates, Verizon could stand to reward those willing to hold the stock.

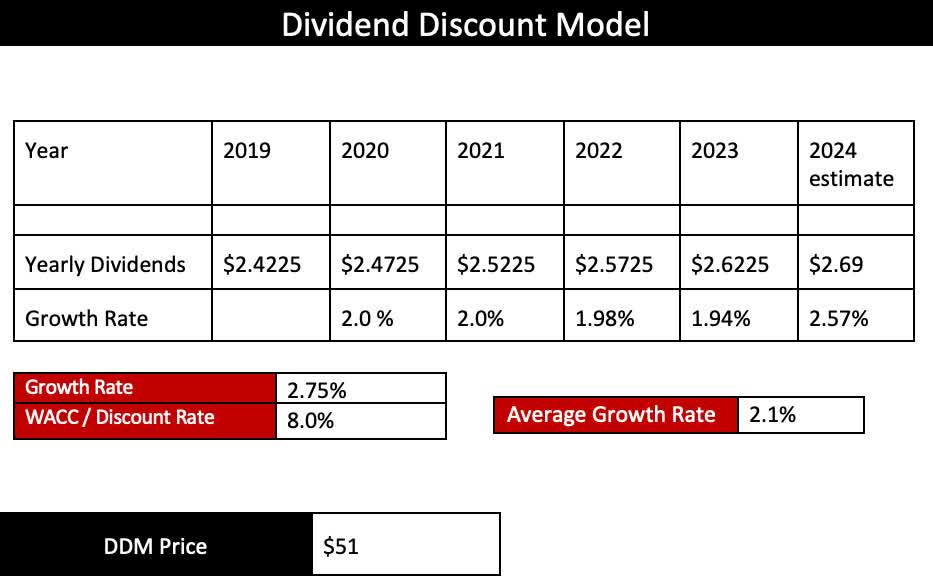

At the current price of less than $40 a share, I think investors have the potential to see minimum $45 a share by the end of the year, but of course, this is all centered around interest rates. If they remain here, I expect the stock to trade between $40 to $42 a share. Using the Dividend Discount Model, I have a price target of $51, slightly less than the $54 price target Morningstar has for the telecom giant. Either way, you get a nice yield and the potential for double-digit upside.

Author DDM

Bottom Line

Despite the stock selling off for what appeared to be disappointing Q1 earnings, Verizon is still on track to continue making improvements in 2024 as a result of lower CAPEX and debt than last year. The company has been making a concerted effort to improve the business fundamentals and turning the ship around. And although cash from operations declined, free cash flow was up double-digits, further strengthening the company’s dividend.

This in turn may give the company more sentiment for larger dividend increases in the near future. And this coupled with lower interest rates could boost investor sentiment, increasing the share price in the near future. Because of the company’s continued improvements to grow their free cash flow, stronger balance sheet, and AI implementation, I continue to rate the telecom company a buy.

Q2 2024 Earnings Call Transcript")