ilbusca

The Adidas Investment Thesis

In June of last year, I wrote an article about Adidas AG (ADDYY / ADDDF) in which I argued that its competitors had better long-term prospects. And I continue to believe this as Nike, Inc (NKE) continues to deliver higher returns on capital and better margins and is well positioned for the future.

Nevertheless, Adidas is worth keeping an eye on after the guidance hike, as a successful turnaround story often offers opportunities for extraordinary returns. If Adidas can pull off the turnaround, there should be plenty of upside left.

Adidas Q1 2024 Earnings Review

Last week, Adidas announced its preliminary results for the first quarter of fiscal year 2024. And at the same time, they have raised the guidance for the full year. First quarter sales were up 8% year-over-year and the company is targeting an operating profit of €700 million for the fiscal year 2024, up from the previous target of €500 million.

Contributing to the strong results was the recent Yeezy line, which generated revenues of € 150 million and an operating profit of € 50 million. In the past, the brand’s nine-year relationship with Kanye West and his Yeezy collection was a huge success before the partnership ended. In 2019, for example, Yeezy alone generated more than $1 billion in revenue. For this reason, the temporary suspension of sales of Yeezy products has had a significant impact on sales in the past.

However, with some of the guidance increase likely due to strong Yeezy sales, it will be interesting to see how things play out once the remaining inventory is sold off. Because it used to be assumed at Adidas that the Yeezys were not going to contribute to the bottom line.

However, according to the latest news, the Yeezy models will only be available until the end of the year, so next year’s sales will not have the boost from the Yeezy sales. This year, however, the European Football Championship in Germany and the Olympic Games in Paris are two international events that could drive sales.

The Battle For Athletic Stars Between Adidas And Nike

It is a constant battle between the two sportswear giants to sign the biggest sports stars and give them signature shoes or even their own brand, as they are important brand ambassadors. And right now, Nike definitely has the edge, having signed both Victor Wembanyama and likely Caitlin Clark, the two potential faces of women’s and men’s basketball in the future.

And the story that Giannis Antetokounmpo told in the Thanalysis show also shows that Adidas missed the chance to sign him because they did not offer a contract to his brother on the same day.

I was also surprised that the German national soccer team changed its sponsor from Adidas to Nike after more than 70 years. This is all the more surprising given that Adidas is a German company and soccer is the number one sport in Germany.

In soccer, they still have perhaps the best player of all time under contract in Messi, but he is in the late autumn of his career, and rising stars like Erling Haaland and Kylian Mbappe are with Nike. And surprisingly, Puma has managed to sign stars like Grealish or Neymar. But all in all, Nike has the best roster at the moment.

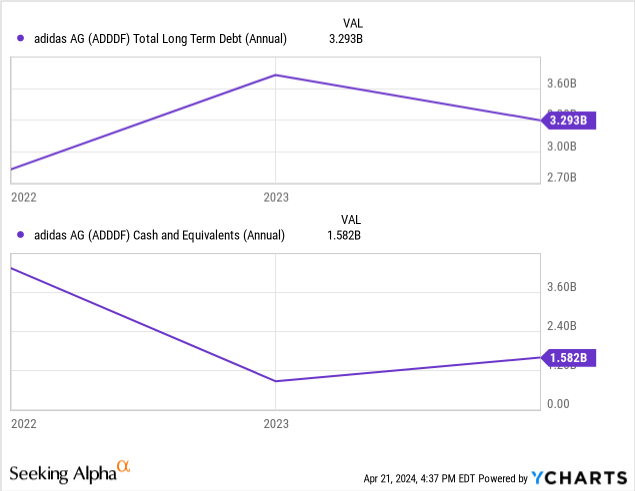

Adidas Balance Sheet

Adidas has been able to pay down some of its long-term debt, as we can see in the picture above. However, they still have about $3.2 billion in LT debt remaining. This is offset by approximately $1.5 billion in cash and cash equivalents. However, this figure has declined significantly in recent years. There have been times when Adidas had more cash than long-term debt. So you could say that the balance sheet has been healthier in the past.

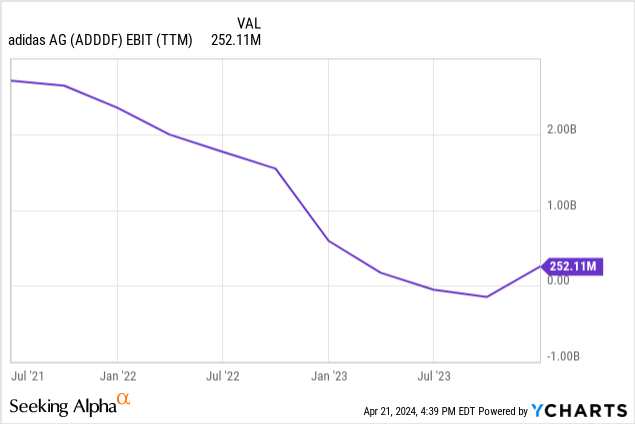

And so the declining EBITs have led to Adidas no longer being in the range that I think is very robust, which is when LT debt is not higher than four times TTM EBIT. But with EBIT on the upswing, I think Adidas could get back into that range. But for the time being, the balance sheet situation still has room for improvement.

Adidas Capital Allocation

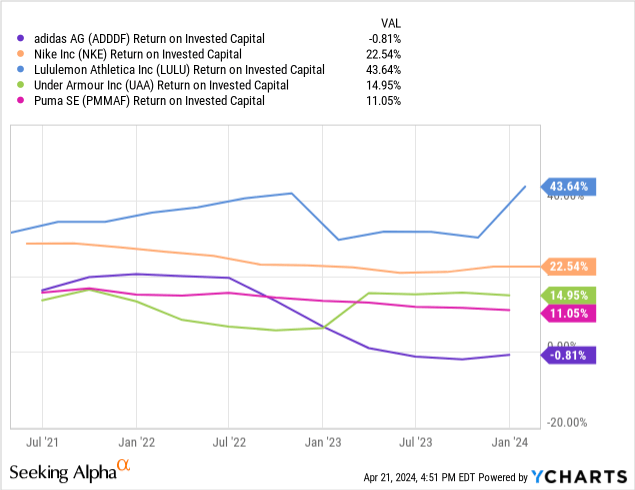

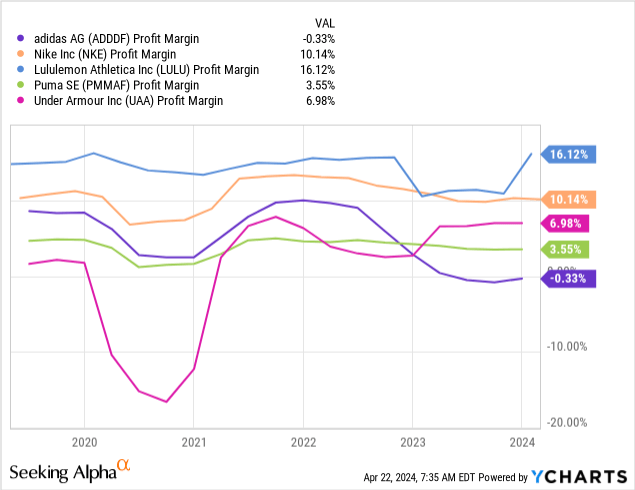

And because I firmly believe that ROIC is one of the most important metrics, because in the long run, returns are going to get closer and closer to ROIC. Therefore, a peer comparison can be helpful in assessing the competitive situation. And unfortunately, Adidas has the lowest ROIC in the peer group I looked at here. The downtrend that started around July 2022 has stopped, but with a current negative ROIC, the ROIC-WACC spread will also be negative.

Adidas still has tremendous name recognition and a strong brand, which is normally a great competitive advantage, but the apparel market is highly competitive and constantly changing. Trends come and go quickly.

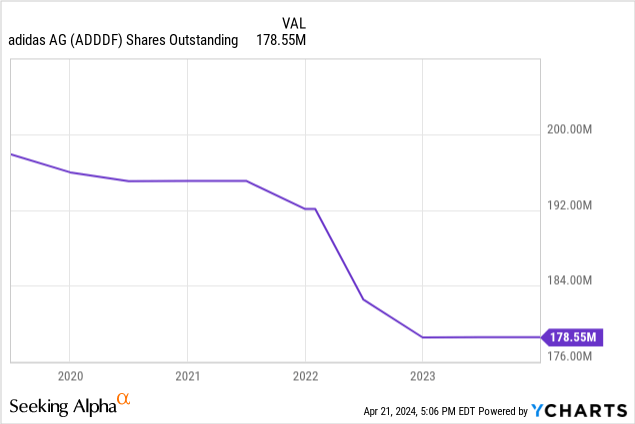

On a positive note, Adidas is not diluting shareholders as many companies do these days, because the number of shares outstanding has been steadily decreasing over the last 5 years. If earnings improve in the future, the number of shares could be reduced again. This should have a positive effect on EPS, which would also benefit shareholders.

The peer comparison of profit margins also shows that Adidas is currently in a transitional phase. But even as they return to their old strength, their closest competitor, Nike, has historically had the edge in both margins and ROIC.

Adidas Reverse DCF

Author

As 2023 was a transition year, we can expect Adidas to earn $3 of diluted EPS on a normalized basis in 2024. The guidance for 2024 is € 700 million in operating income, and they achieved that in FY22 with a diluted EPS of $3.58. So I think the $3 for FY24 is a conservative but realistic assumption.

Using this assumption and performing a reverse DCF, we find that the market is pricing in 16% EPS growth over the next 10 years. Historically, however, EPS growth is much lower, as diluted EPS was already at $2.84 in FY14.

EBIT also shows a negative 10-year CAGR of -13.78%. Therefore, and also due to the fact that Adidas is in a turnaround phase, I think the stock is overvalued at the moment.

Conclusion

The days of reselling exclusive sneakers on platforms like StockX for a multiple of the purchase price are over as demand has dropped. Nevertheless, the most popular list on StockX is a good representation of which sneakers are currently popular. And here you can clearly see that Adidas has broken Nike’s dominance a bit. While Nike’s Jordan and Dunk Low dominated for a while, Adidas’ Campus and various Yeezy models are also currently among the most sought-after models. However, should the Yeezy line be discontinued, it can be expected that Nike will once again dominate the sneaker segment.

Turnarounds, when successful, offer great opportunities, but they are often also associated with risks. This is especially true as Chinese sportswear companies enter the market and new European and American companies enter the market. Social media in particular has helped many companies position themselves well and build great brands in a short period of time, especially in the gym and fitness industry.

Therefore, I am looking forward to seeing how Adidas performs and whether the turnaround story will continue in the remaining quarters of this fiscal year. If Adidas can continue to grow strongly in the future without the Yeezy collections, I would think about raising the rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")