JHVEPhoto

Investment Thesis

IBM (NYSE:IBM) is set to announce their earnings report for the first quarter of this year, on Wednesday, April 24th, next week, after market hours.

Big Blue reported a strong full-year FY23 earnings report in the previous quarter, which showed a re-acceleration in their core business segments, Software and Consulting aided by strong growth due to AI. Its Consulting business reported strong growth as well, defying the general weakness that was seen through last year, including its consulting peers like Accenture (ACN).

Last quarter, management did well to restore further confidence in the strength of their business as they invested and launched new products and features, especially in AI. Next week, I expect management to build on this momentum to illustrate the progress of their Software and Consulting segments, as well as the revenue impact from AI.

Over the long term, I believe it still offers investors attractive entry points at current levels. I had previously covered IBM, where I had issued a Buy rating, and I will continue to recommend a Buy for IBM stock.

Summarizing IBM’s Q4 Performance and Key Management Commentary

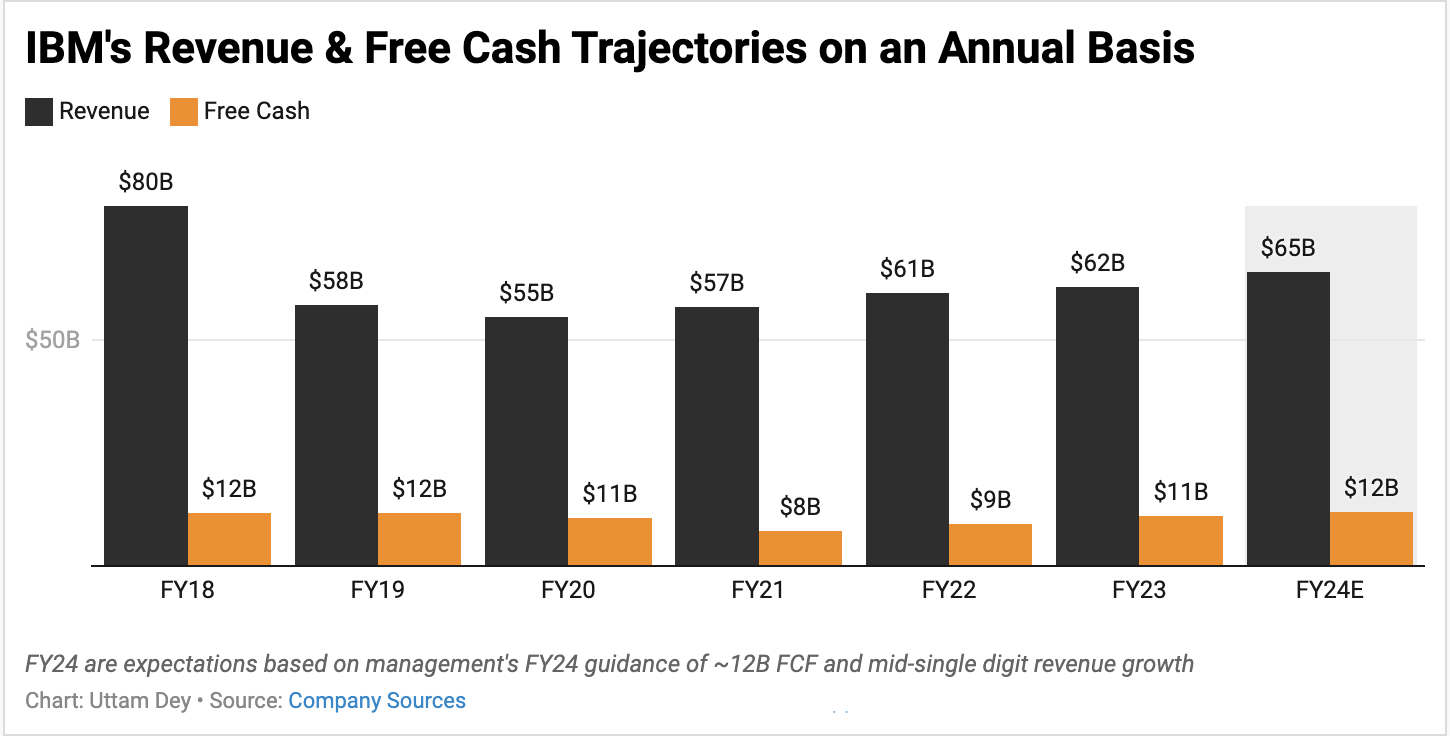

For the full year FY23, IBM’s revenues grew 3% to $62 billion, as seen in the chart below, led primarily by a 5% increase in Software revenue and over 6% in Consulting. In addition, the company reported strong growth in its free cash of ~$11 billion through FY23, but what baked the cake for the market was management’s strong guide on free cash of $12 billion projected by the end of this year.

IBM’s revenue and free cash trends since 2018 including management’s own guidance for FY24 (Company sources)

On the call to discuss its stellar Q4 earnings, management pointed to the platform-based approach they were using to drive inter-segment synergies between IBM’s Software and Consulting segments. IBM’s 2019 acquisition of Red Hat continues to drive accretive gains for IBM’s software platform, which is built on top of Red Hat infrastructure.

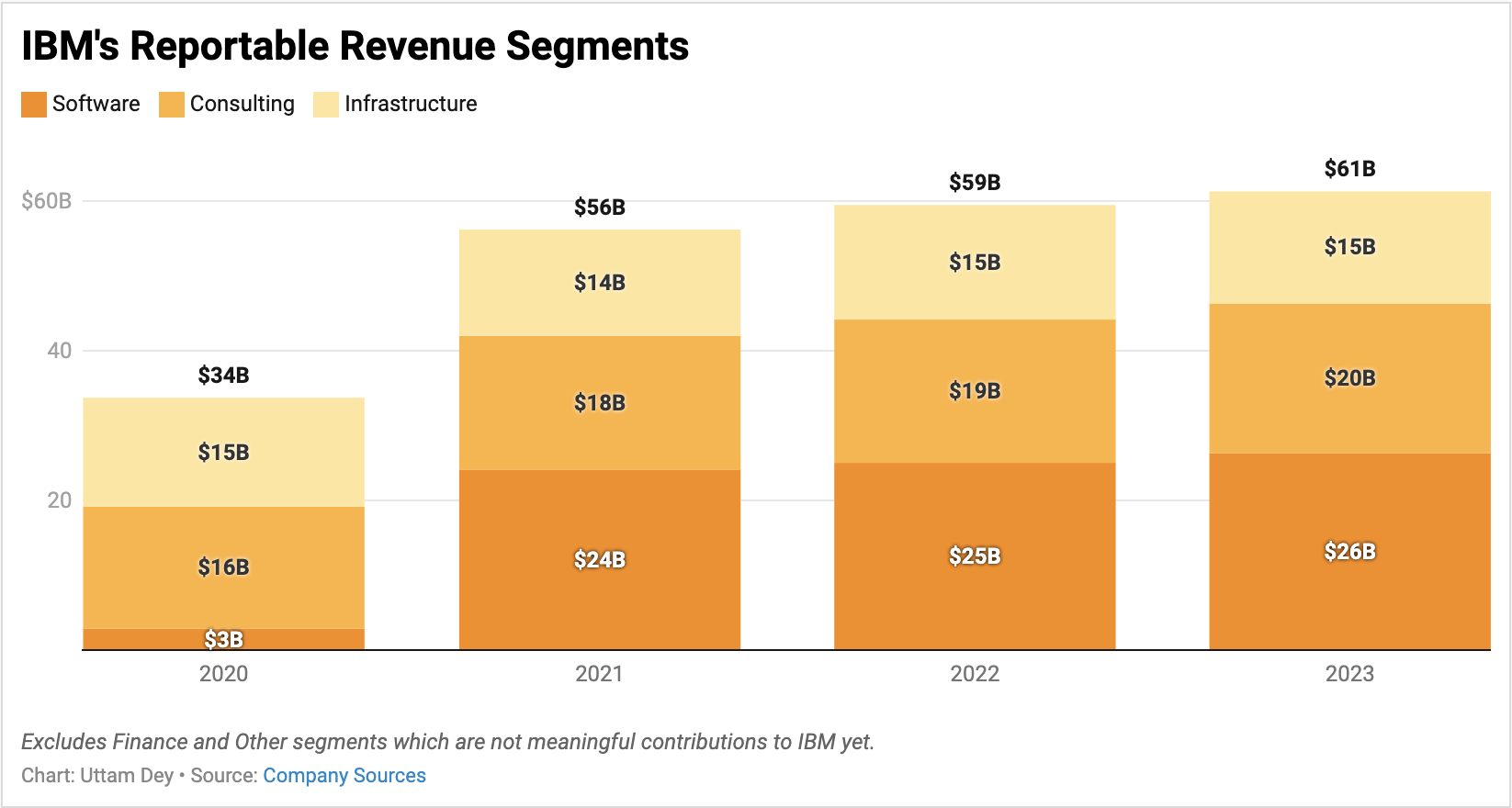

Software and Consulting segments now account for approximately 75% of IBM’s total revenues, up from 73% in FY21, as can be seen below. These two segments combined have grown at a compounded growth rate of 4.7% since FY21, strong by IBM’s standards, in my opinion, given its history of pre-pandemic no-to-low single digit growth.

IBM’s reportable revenue segments from FY20 to FY23 (Company sources)

In my previous coverage on IBM, I had observed how AI was now starting to play a key role since the launch of several initiatives last year, which I will briefly summarize here.

For example, IBM’s AI-accelerator-based hybrid cloud service, z16, meant for mission-critical workloads, launched two years ago, is finally starting to bear fruit for the company. I noted how IBM’s Infrastructure business grew revenues by 2% in Q4 FY23, aided by strong growth in z16 due to AI demand. In addition, IBM also launched its watsonx AI & data platform last year. Management announced that their “book of business” due to generative AI doubled sequentially, which helped spur growth in a number of lucrative deals in Software and Consulting.

I’ve added some commentary from IBM’s management in their previous earnings call, which I felt summed up their Q4 earnings:

Since 2021, we delivered average revenue growth for IBM and for each segment at or above our model. The overall trends we are seeing reinforce our views of the future. We are confident in achieving our midterm revenue model, and the strength of our diversified business model allows us to make progress each quarter.

We entered the year intent on enhancing our Software portfolio and strengthening our Consulting position. We have done both. Mid-last year, we launched watsonx, our flagship AI and data platform, and we are excited by the traction we are seeing. Consulting has delivered durable revenue growth through the year despite an uneven macro environment.

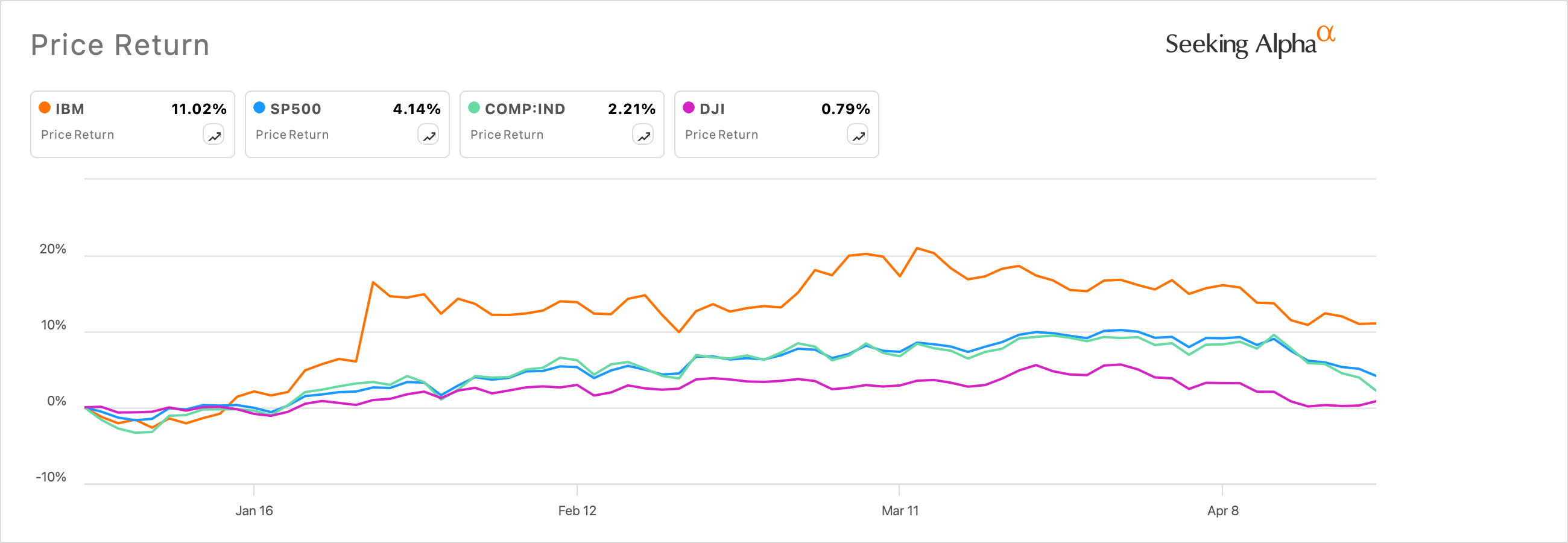

I believe these results were strong enough for IBM to be one of the top performers, not just in the Dow 30 index (DJI) but also in the S&P 500 index (SPX).

IBM’s stock performance YTD (sa)

Changes in Q1 that will impact IBM’s earnings next week

Through the quarter, IBM has been busy launching products and features across its product suite, as noted below. In addition, the company also announced some key changes in their reporting segments, which is important to factor in as an investor. I’ll start with the change in reporting segments announcement.

IBM will be slightly changing their reporting segments starting Q1 FY24 (Company sources)

Starting in the Q1 FY24 quarter, I will expect IBM to start reporting its revenue split by business and segments based on the structure I noted earlier. This change has no material impact on IBM, in my opinion. I see this change being made to reflect IBM’s divestiture from the Weather Company.

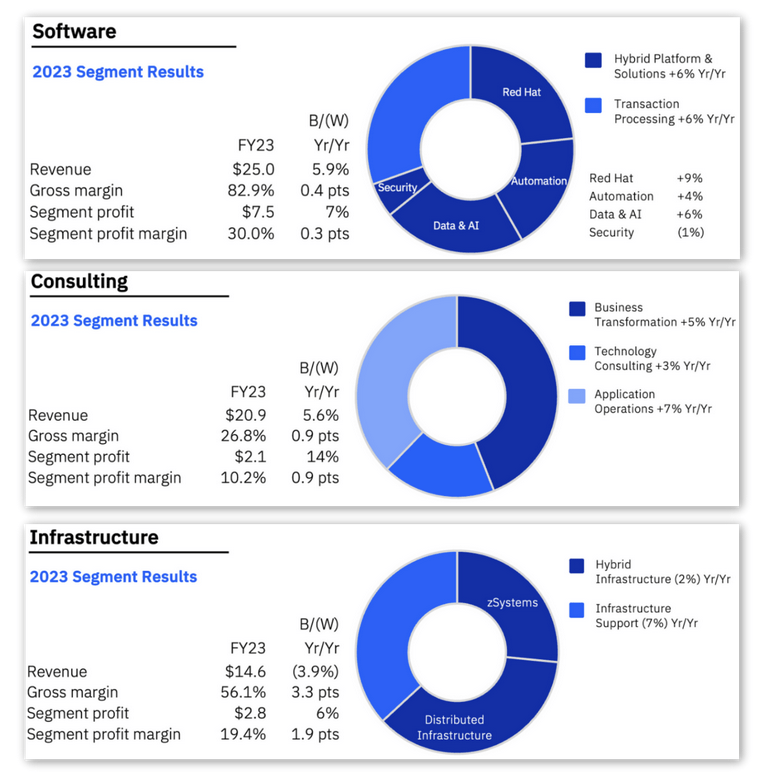

In addition, IBM will now be reporting its Security Services within its Consulting business under the new reorganization. I actually believe this may be beneficial to the company. I had noted in one of my previous coverages that cybersecurity peers such as SentinelOne (S) and Palo Alto Networks (PANW) were also seeing elevated levels of demand for their Managed Security Services solutions. I believe moving Security Services to IBM’s Consulting business will be a long-term advantage for the company, given the positive shifts in demand for IBM’s Consulting services as well as the overall demand for Managed Security Services.

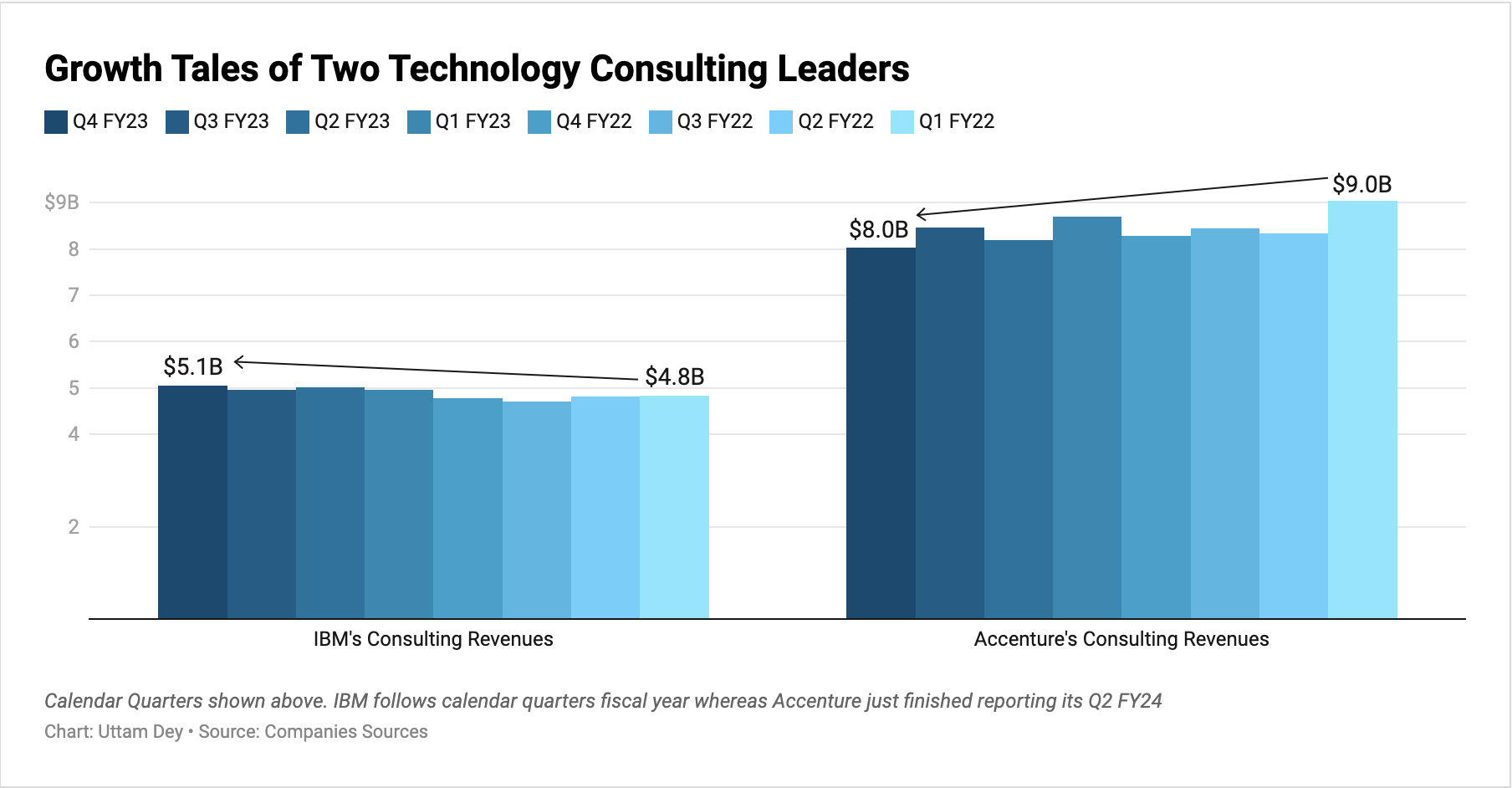

Continuing the train of observations with IBM’s Consulting, I noticed some weakness continues to persist within the broader Consulting market. Accenture cut its annual revenue forecasts, whereas McKinsey has been slashing jobs as demand wanes for Consulting services. However, as noted in the chart below, I see that IBM defies those trends.

IBM continues to defy the odds in of a slump in the broader market Consulting Revenues (Companies sources)

Through my previous analysis, I observed that IBM has been very successful in moving into niche market segments such as DevSecOps & AIOps. All these market segments are emerging areas for IBM to grow while leveraging its AI and Red Hat-based software platform, which also feeds into its Consulting business.

On the AI front this quarter, I observed that IBM is widening the scope of its AI solutions, building on product launches last year. IBM recently announced the availability of Microsoft-backed (MSFT) Mistral AI’s LLM model on their watsonx platform. I see IBM has been consistently ramping up the availability of multiple LLM models as part of their multi-model strategy.

For example, Meta’s (META) Llama2 LLM models were already made available on watsonx last year. I believe IBM has been moving the needle by quite a bit to make the impact, which will continue to provide the observed tailwinds over the long term for the company.

IBM’s Outlook and Valuation

In terms of my outlook, I note that IBM has projected revenues to grow by ~5% y/y to $65 billion, while free cash is projected to grow by ~7% y/y to ~$12 billion for FY24. I noticed that consensus FY24 revenue projections have slightly dipped to $63.6 billion as of writing. I believe this would be due to the rise in the US dollar (DXY), which has risen ~2.5% since IBM reported its Q4 earnings in January.

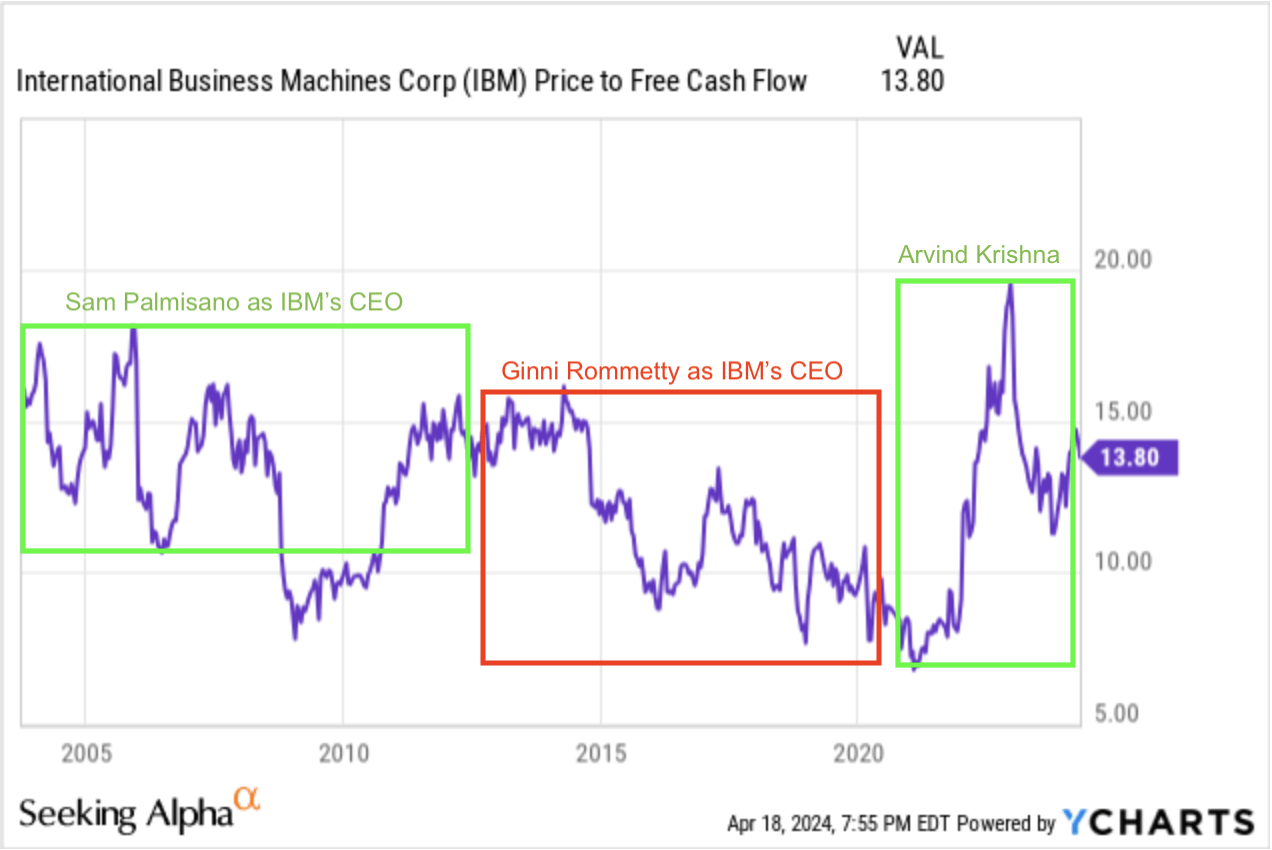

However, given IBM’s momentum in product launches and services that I noted in the earlier section through the first quarter, I believe the company will keep its projections unchanged. Given these views, I estimated IBM to be trading at 14x forward free cash. I believe these valuation multiples are still overlooking the growth in free cash that IBM has demonstrated since 2018, as I noted in a chart at the start of this post. From that chart, I observed that IBM’s free cash has grown by 19% CAGR since 2018, which is very impressive in my opinion. It easily gives room for the forward free cash multiple to expand to a multiple of 15x, as last seen during the times of Sam Palmisano, a previous CEO of IBM, as shown below.

IBM’s FCF Multiple History Since Two Decades (yCharts)

If I use reverse DCF to value IBM, I see that there is still tremendous upside. My assumptions here are:

-

Discount rate is 9% higher than market estimates.

-

IBM’s sustained growth in the business will stabilize FCF growth closer to its long-term midpoint growth model over the long term.

Author’s Valuation Using reverse DCF (Author)

Based on my model, I believe IBM still has room to grow from its current levels. Markets are experiencing heightened volatility, which may impact IBM, but I believe any pullbacks in this stock can be bought.

5 Key Factors to look for in IBM’s Q1 FY24 earnings report

I wanted to emphasize a few things that I think are important to look for in IBM’s earnings report next week:

-

AI: Now that we are in the second full year of AI since the ChatGPT euphoria began, what are the revenue impacts AI is having on IBM’s top and bottom lines? I expect management to add more color to bookings and segments or expand more on their “book of business” comments made in the previous earnings call.

-

Consulting Business: Can IBM sustain the momentum it has enjoyed over the past 8 quarters, as I had noted in an earlier chart? With Accenture and other peers underperforming, what is management’s +FY24 outlook on Consulting? Especially when Gartner projects Consulting/IT Services to improve by 290 basis points in FY24. I believe the momentum should continue and IBM should be on track to guide towards the 6-8% growth range for Consulting in FY24.

-

Software Business: Can IBM sustain the momentum in its Software segment as well? If IBM’s Red Hat division grows in double digits, that would further boost its outlook. My take on Software is slow to start in FY24, but plays catch up in the back half to eventually grow ~6-7% in FY24.

-

Any further revisions to the prior FY24 and long-term midpoint growth operating models? Prior FY24 guidance was recently reiterated at the TMT Conference last month.

-

Any incremental headwinds seen from the rise in the dollar in Q1 FY24? Or other headwinds?

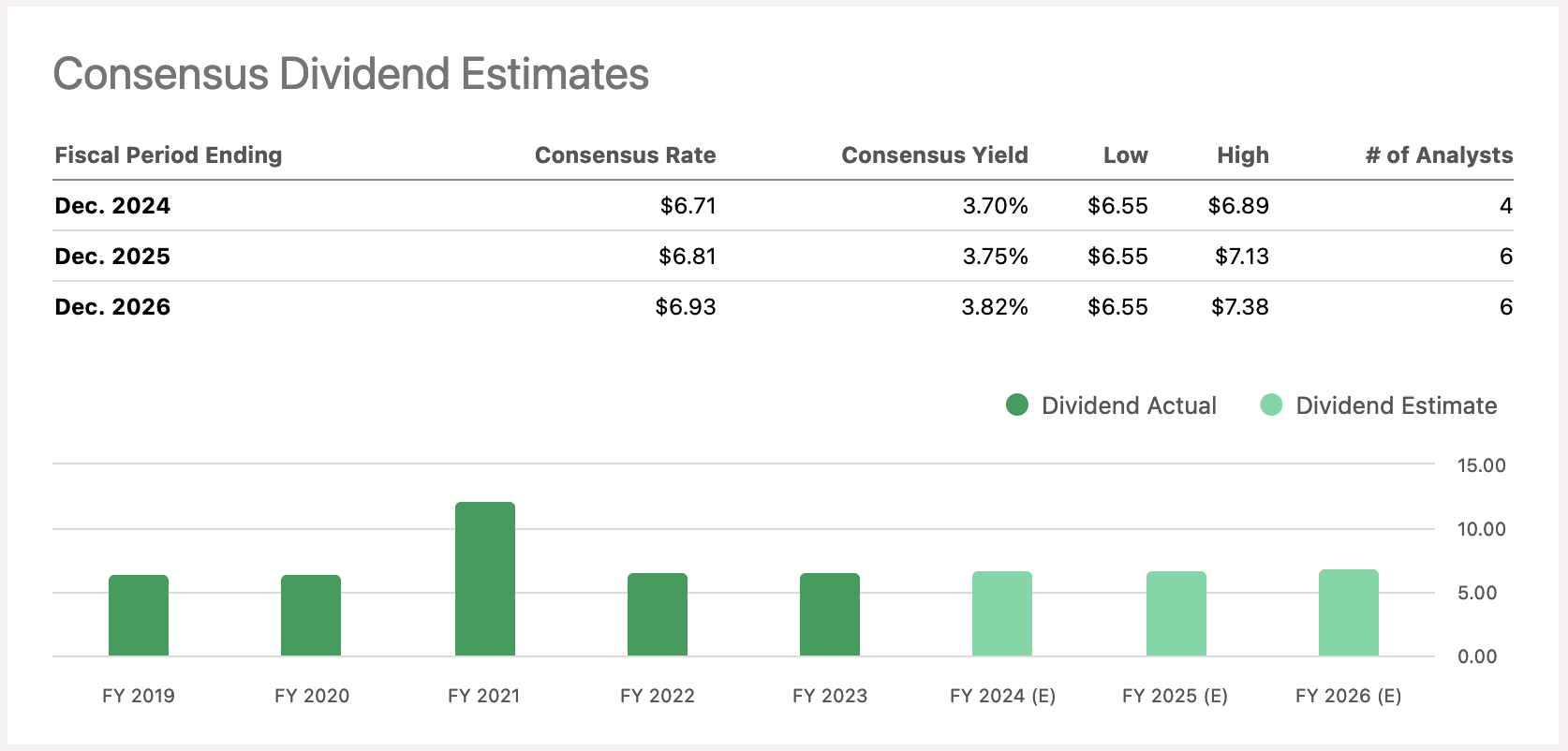

In addition to the capital appreciation, many investors benefit from IBM’s dividend yield. Here are the consensus estimates so far. Any changes in cash, free cash will affect dividend payouts, but I don’t expect material changes to dividends here as well in Q1.

IBM’s Expected Dividends Per Consensus Estimates (SA)

Conclusion

IBM continues to stand at a pivotal time in FY24, as it needs to demonstrate to investors that the Big Blue can sustain the momentum that it has seen over the past year. I have stated in my coverage earlier how I have been impressed by IBM’s rapid turnaround in developing & deploying AI products and solutions, while also reaching across the board and striking key partnerships with peers and critical stakeholders in the industry. I believe the company is pulling the right levers, and this company definitely holds long-term value for shareholders.

I recommend a Buy rating on IBM.

Q2 2024 Earnings Call Transcript")