Adam Gault

By Elisa Mazen, Michael Testorf, CFA, & Pawel Wroblewski

Repositioning for an International Revival – Market Overview

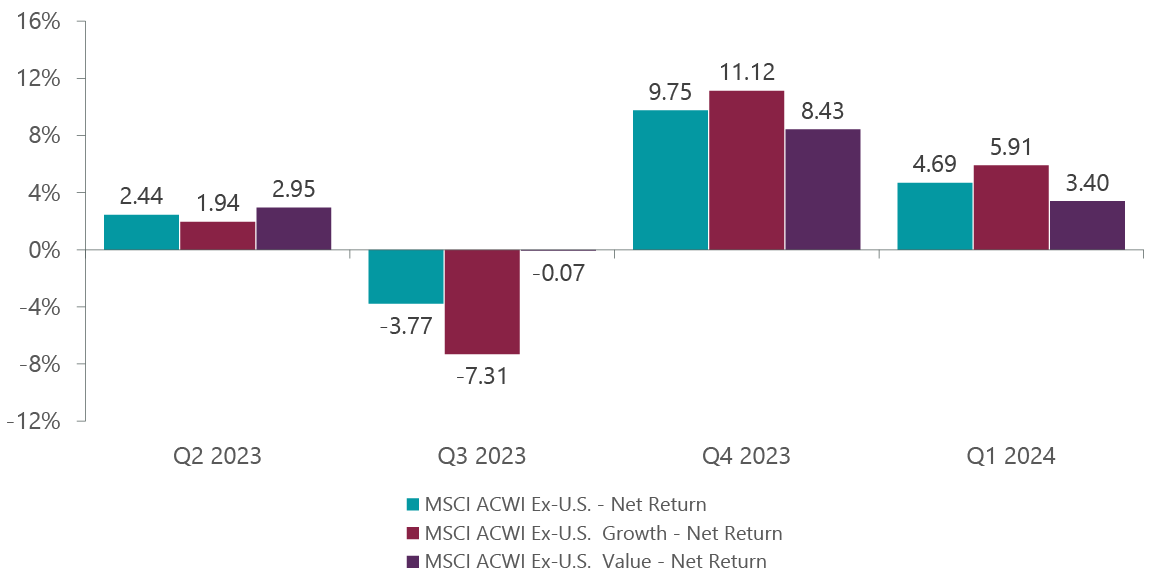

International equities continued to climb in the first quarter, supported by improving investor sentiment, better economic data in the U.S., rate cuts beginning in Europe and confidence in a Japanese economy that is seeing improved corporate governance. The benchmark MSCI All Country World Ex-U.S. Index advanced 4.69%, while the MSCI Emerging Markets Index added 2.37% and the MSCI ACWI Ex-U.S. Small Cap Index gained 2.21%.

Growth stocks surged to start the year, buoyed by optimism that bond yields would continue to ease off their 2023 peak. Switzerland became the first major developed market to reduce rates in March, the U.S. Federal Reserve communicated its plan for three 25 basis point (bps) rate cuts this year and the market is pricing in 90 bps of easing from the European Central Bank. Against this backdrop, the MSCI ACWI Ex-U.S. Growth Index rose 5.91% for the quarter, outperforming the MSCI ACWI Ex-U.S. Value Index by 251 bps (Exhibit 1).

Exhibit 1: MSCI Growth vs. Value Performance

As of March 31, 2024. (Source: FactSet.)

The ClearBridge International Growth ACWI Ex-US Strategy outperformed its benchmark for the quarter, led by holdings in cyclical sectors including materials, information technology (IT) and industrials as well as the more defensive health care sector. We were encouraged that stock selection in these areas worked, as did active positioning that expresses our growth style, with an overweight to IT proving the most beneficial to performance. We believe international growth equities will remain in favor this year as rate cuts in Europe appear to be ahead of the Fed, European economic data has been weak and credit flows in the eurozone are rising, both on the corporate and consumer side, which is often a leading indicator of GDP growth.

Positions tied to generative AI and diabesity, two relatively recent but key growth themes that have dominated global markets over the last 15 months, drove performance for the second straight quarter. Semiconductor equipment makers Tokyo Electron (OTCPK:TOELY)(OTCPK:TOELF) (Japan), a repurchase during the quarter, and ASML (ASML) (Netherlands), two companies which manufacture equipment critical to the development of the GPUs that power large language models, as well as contract chip manufacturer Taiwan Semiconductor (TSM), were top contributors. Enterprise resource planning software maker SAP (SAP) was also a standout. We recently wrote about the large and growing opportunity in diabetes and obesity treatment where Novo Nordisk (NVO), a leading developer of GLP-1 pharmaceutical treatments for these conditions, continues to execute well. Emerging biotechnology company Zealand Pharma (OTCPK:ZLDPF), a new purchase during the quarter, is making progress in clinical trials for a new therapeutic for liver disease and obesity with very promising results.

Consumer spending, both local and global, is a key part of our allocations, leading us to favor luxury goods over most auto makers as they have less operational volatility over an economic cycle. We saw resurgent results from high-end apparel and spirits group LVMH ( OTCPK:LVMHF) and iconic auto maker Ferrari (RACE), as well as continued excellent results from our longtime holding in apparel retailer Inditex, offering further proof of its business model.

These positive drivers offset weakness in financials, where our meaningful underweight to banks and consumer discretionary stocks tied to Asia and travel weighed on performance. While Chinese equities remained pressured by economic uncertainty, Japan was the best performer regionally in the benchmark, with Japanese equities rising following the Bank of Japan’s (BOJ) decision to end its negative interest rate and yield control policies. This move reflects Japan’s confidence that it has achieved price stability by removing deflation as a major risk to its economy. The BOJ will, however, maintain accommodative policies. Combined with ongoing corporate reforms and a weakening yen, we believe the outlook for Japanese stocks should continue to improve.

Portfolio Positioning

We were active during the quarter, initiating 11 new positions while eliminating 10 others. While Strategy positioning was slanted toward more defensible and self-help business models through the monetary tightening regime, our new purchases represent a mix of secular, structural and emerging growth companies reflecting a more balanced market environment.

In the secular bucket, our largest addition was French electrical and industrial automation supplier Schneider Electric (OTCPK:SBGSF)(OTCPK:SBGSY). We believe the company’s revenue growth will be faster than expected as it is well-positioned to participate in several secular demand drivers: a reshoring of supply chains and manufacturing production in the U.S. and EU; energy and power management needs to support AI and cloud growth; and accelerating demand for electrification across economies. Schneider should also see higher than forecasted margin expansion due to faster growth in software and system sales compared to lower-margin device sales. We also repurchased U.K.-based hygiene and pest control provider Rentokil (RTO) after its risk-reward became more attractive due to delayed synergies from a recent acquisition.

Among structural growth names, we initiated a position in French advertising holding company Publicis Groupe (OTCQX:PUBGY). The company has unique assets in Epsilon (EPSN) and Sapient that give it unmatched and difficult to replicate advantages in winning new business, retaining existing clients and transitioning to an AI-driven business model. We also added EQT AB (OTCPK:EQBBF), a Swedish alternative asset manager that helps reduce our financials underweight.

In the emerging growth bucket, we initiated a position in monday.com (MNDY), which offers front office software-as-a-service that enables organizations to build custom applications and solutions for project management, customer relationship management, marketing and software development. The company has low cross-selling penetration across its existing customers and stands to expand as its platform broadens. monday.com is fundamentally sound with best-in-class free cash flow margins.

To make room for these new names, we exited several holdings that either reached our price target, as was the case with Canadian exploration and production company Suncor Energy. Hong Kong Exchanges & Clearing was closed due to China equity market weakness driving down exchange volumes, as well as part of our general reduction in Hong Kong to bring our exposure to more index neutral levels. China travel and reservations software maker TravelSky Technology (OTCPK:TSYHF)(OTCPK:TSYHY) and Japanese cosmetics maker Shiseido (OTCPK:SSDOF)(OTCPK:SSDOY) were sold due to tepid travel and tourist spending by Chinese consumers.

Outlook

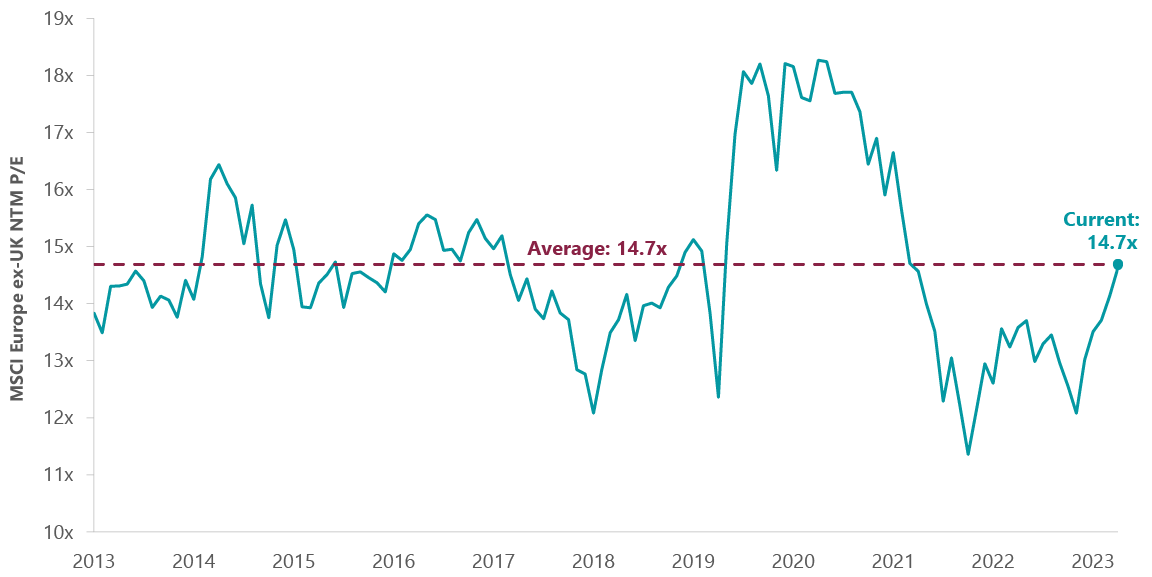

Recent results validate the need for investors seeking international exposure to include growth equities in their portfolio. While the macro picture in Europe, the Strategy’s largest exposure, remains muddled with Germany in particular showing weakness, markets appear to be looking past recent disappointing GDP growth in the region as evidenced by improvements in the Citi Economic Surprise Index. Investor flows into Europe are also demonstrating green shoots after an extended period of outflows, with a pickup in share buyback activity being a catalyst.

Exhibit 2: European Equities Trading at Lower Relative Valuations

NTM P/E: P/E based on next twelve-month consensus earnings expectations. Data as of March 31, 2024. (Source: FactSet, MSCI.)

We continue to believe international growth equities in general, and European stocks in particular, look quite attractive compared to their U.S. peers. Judging by forward P/E multiples, the eurozone is trading at less than two-thirds the U.S. – its cheapest relative levels since before the COVID-19 pandemic. Given an improving rate environment and the resilience companies there have shown through the Russia-Ukraine war and an inflation scare, we maintain confidence in our European and U.K. holdings.

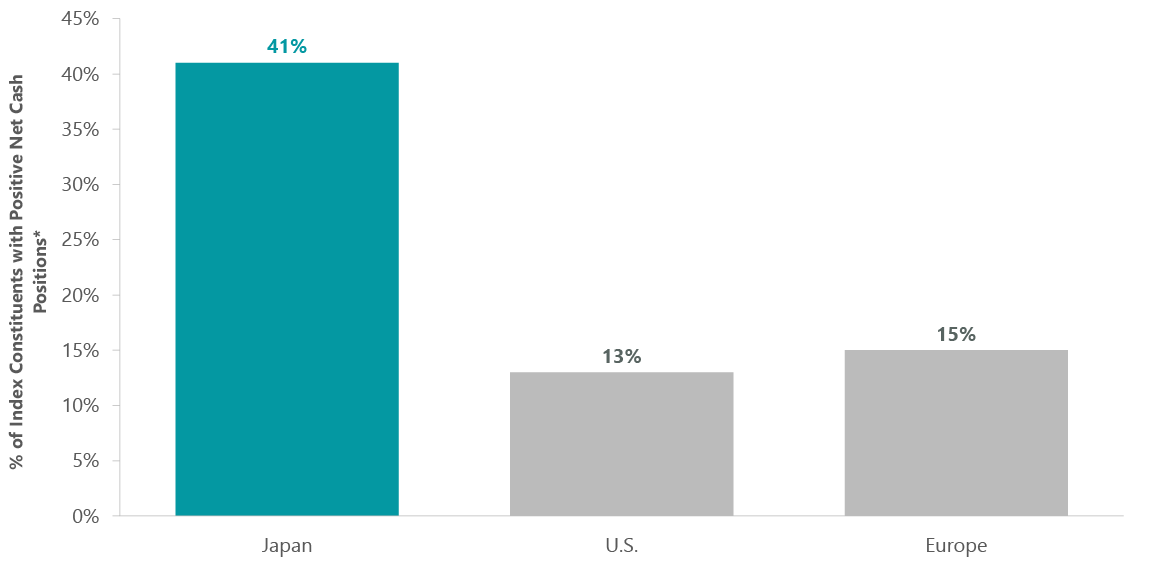

Meanwhile, in Japan, the actions taken by the government and exchanges to improve corporate returns and encourage greater equity ownership are beginning to flow through to better earnings. Companies are also sitting on high cash levels that can be directed to shareholder-friendly activities such as buybacks and dividends.

Exhibit 3: Corporate Japan Flush with Cash

*Positive net cash positions ex-financials. U.S: S&P 500, Europe: MSCI Europe, Japan: MSCI Japan. Data as of March 31, 2024. (Source: FactSet, MSCI, S&P)

To capture these opportunities, we remain committed to our valuation approach to growth and diversification across the different types of growth companies represented by our buckets.

Portfolio Highlights

During the first quarter, the ClearBridge International Growth ACWI Ex-US Strategy outperformed its MSCI ACWI Ex-U.S. benchmark. On an absolute basis, the Strategy experienced gains across seven of the 10 sectors in which it was invested (out of 11 total), with the IT, industrials and health care sectors the primary contributors while the financials sector was the main detractor.

On a relative basis, overall stock selection and sector allocation contributed to performance. In particular, stock selection in the materials, IT, industrials and health care sectors and an overweight allocation to the IT sector aided results. Conversely, stock selection in the financials, consumer discretionary and utilities sectors detracted from performance.

On a regional basis, stock selection in Europe Ex U.K., the U.K. and North America and underweight allocations to emerging markets and Asia Ex Japan supported performance while stock selection in Japan and emerging markets proved detrimental.

On an individual stock basis, the largest contributors to absolute returns in the quarter included ASML, Taiwan Semiconductor, SAP and Tokyo Electron in the IT sector and Novo Nordisk in the health care sector. The greatest detractors from absolute returns included positions in TravelSky Technology in consumer discretionary, HDFC Bank (HDB) and AIA Group (OTCPK:AAGIY)(OTCPK:AAIGF) in financials, EDP in utilities and Zai Lab (ZLAB) in health care.

In addition to the transactions mentioned above, we initiated positions in Daifuku (OTCPK:DAIUF) in the industrials sector, Givaudan (OTCPK:GVDNY) and John Hardie Industries in the materials sector and SoftBank Group (OTCPK:SFTBY)(OTCPK:SFTBF) in the communication services sector. In addition, we exited positions in Amadeus IT Group (OTCPK:AMADF)(OTCPK:AMADY) in the consumer discretionary sector, Edenred (OTC:EDNMF)(OTC:EDNMY) in financials, Sumitomo Metals Mining (OTCPK:SMMYY)(OTCPK:STMNF) in materials, Computershare (OTCPK:CMSQF)(OTCPK:CMSQY) in industrials as well as Schott Pharma and BioNTech (BNTX) in health care.

Elisa Mazen, Managing Director, Head of Global Growth, Portfolio Manager

Michael Testorf, CFA, Managing Director, Portfolio Manager

Pawel Wroblewski, CFA, Managing Director, Portfolio Manager

|

Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Morgan Stanley Capital International. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance is preliminary and subject to change. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Further distribution is prohibited. |

Q2 2024 Earnings Call Transcript")