The MLP has been on a red-hot run over the past year.

Energy Transfer (ET -0.85%) has gone on a strong run since the start of 2023. The master limited partnership (MLP) has rallied more than 25%. That’s a big move for a relatively slower-growing pipeline company.

The MLP’s rally likely has some investors wondering if it’s too late to buy. Here’s a look at whether the pipeline stock is about to run out of fuel or has plenty left in the tank.

What has fueled Energy Transfer’s rally?

A big driver of Energy Transfer’s recent run is its growing earnings. The MLP has grown its adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) from $13.1 billion in 2022 to $13.7 billion last year, about a 5% increase. It expects earnings to grow to $14.5 billion-$14.8 billion this year, a 7% to 8% year-over-year increase.

Powering Energy Transfer’s growth has been a combination of organic expansion and acquisitions. It invested $1.6 billion on expansion projects last year and expects to spend $2.4 billion-$2.6 billion on growth capital projects in 2024. Meanwhile, the company paid $1.5 billion to buy Lotus Midstream and $7.1 billion for fellow MLP Crestwood Equity Partners in deals that closed last year.

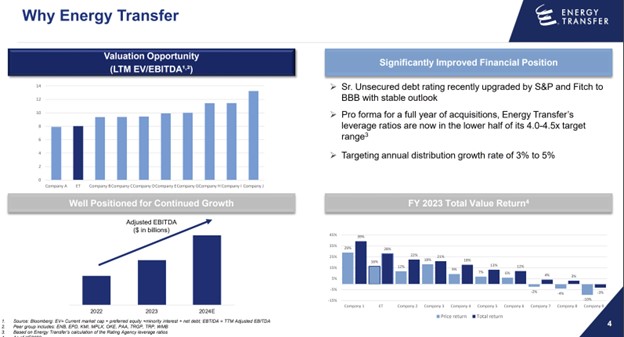

The company’s growing earnings are giving it the fuel to increase its already attractive distribution (currently yielding over 8%). The MLP aims to expand that payout by 3% to 5% annually. Its earnings growth has also helped drive down its leverage ratio, which it expects will be toward the low end of its 4.0-4.5 times target range this year.

That lower leverage recently gave two credit rating agencies the confidence to upgrade Energy Transfer’s credit rating to BBB with a stable outlook. That higher credit rating gives it greater access to lower-cost capital. It used that access earlier this year to issue new notes and used the proceeds to redeem all its outstanding Series C and Series D preferred units.

Is there any upside left?

Energy Transfer’s sharp rally last year made it the second-best-performing energy midstream company in its peer group. It delivered 16% unit price growth and a 28% total return when adding in its high-yielding distribution. However, it still trades at a bottom-of-the-barrel valuation despite that rally:

Image source: Energy Transfer.

As the graph in the upper left-hand corner showcases, Energy Transfer trades at the second-lowest enterprise value–to-EBITDA multiple in its peer group based on its earnings over the last 12 months. It’s even cheaper based on its forward earnings. That low valuation alone suggests it’s not too late to buy the MLP since it has plenty of upside as its valuation multiple expands toward the peer group average.

One looming catalyst that could help boost its valuation is the potential for the MLP to repurchase some of its common units this year. The company expects to produce about $7.5 billion in annual distributable cash flow, $4 billion of which it will distribute to investors. That leaves it with about $3.5 billion of excess free cash flow. Its long-term plan is to reinvest $2 billion-$3 billion into high-return capital projects while using the remaining balance ($500 million to $1.5 billion) to pay down debt and repurchase units.

With capital spending tracking toward the middle of its range this year, the company will have about $1 billion in excess free cash flow. Given that its leverage ratio is already toward the lower end of its target range, the MLP will likely start prioritizing unit repurchases in the coming quarters.

In addition to those upside catalysts, Energy Transfer still offers a very attractive income stream. The MLP currently yields 8.3%, several times higher than the S&P 500‘s dividend yield (1.4%). That already high-yielding payout should continue heading higher as the company delivers on its plan to increase its payout by 3% to 5% per year. While MLPs come with some tax complications (including sending a Schedule K-1 to investors each year), the lucrative tax-deferred income can make them worth the hassle.

It’s not too late to lock in an enticing total return

Despite its rally, Energy Transfer remains relatively cheap compared to other pipeline companies. Because of that, it’s not too late to buy. The company has a clear catalyst on the horizon (unit repurchases) and still offers a very attractive income stream. Because of that, it could continue producing strong total returns.

Matt DiLallo has positions in Energy Transfer. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")