Andersen Ross Photography Inc/DigitalVision via Getty Images

We’re seeing the fruits of the Warner Bros. merger with Discovery that led to the current company Warner Bros. Discovery, Inc. (NASDAQ:WBD). With FY 2023 results out in February to show how well this merger has gone, the market doesn’t seem too happy about it.

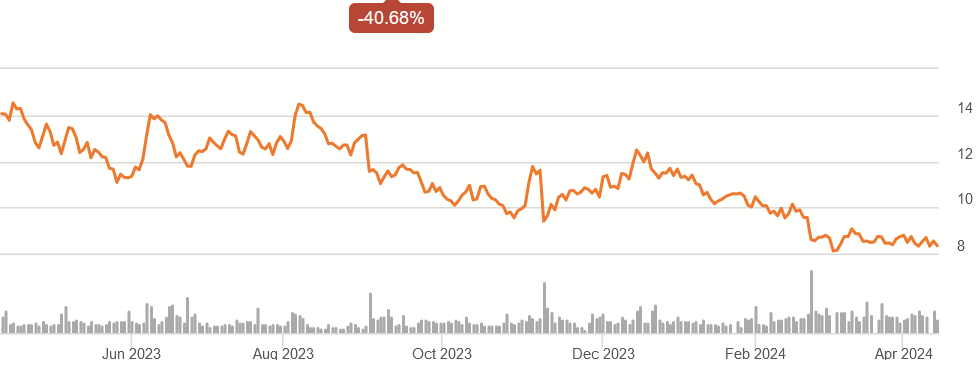

WBD 1Y Price History (Seeking Alpha)

The shares are about the lowest that they have been since the merger. This is interesting to me because I felt that the news for 2023 was good. I’m going to review the historical financial data, talk about the combined company’s strengths, and explain why I think it’s a Buy at this valuation.

Recent Financial Data

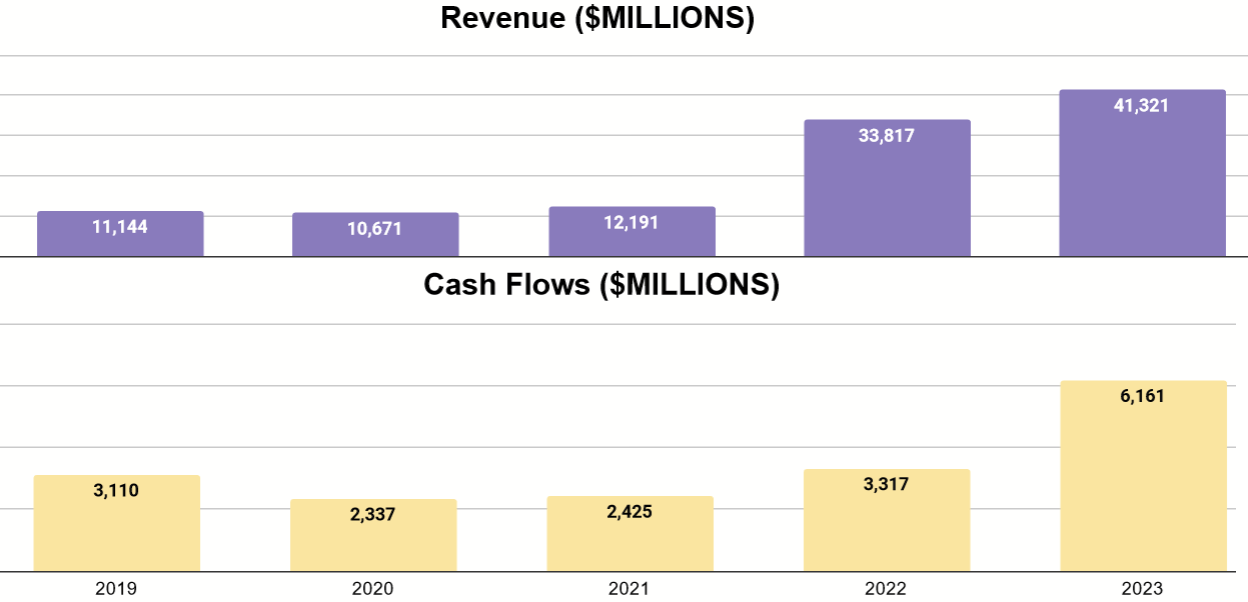

The data from the last five years show how the financials changed for Discovery once it merged with Warner Bros., both in terms of revenue and free cash flow.

Author’s display of 10K data

We can see that the combined entity is capable of generating significantly more revenue, but free cash flow is more of an open question, with 2022’s results being more disappointing, while 2023’s were better. What was happening here?

Income Statement (2023 Form 10K)

A major contributor was the reduced operating expenses in 2023, combined with increased revenues. Almost $3 billion in costs related to the merger in 2022 did not recur into 2023.

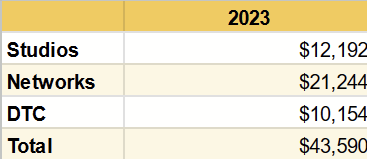

This new company now consists of three main segments: Studios, Networks, and DTC. The chart below shows how their share of revenues. (A few minor items make this a different total than the last chart).

Segment Revenues in Millions (Author’s display of 10K data)

Studios relates mainly to their films, TV, and games, Networks to cable TV, and DTC to streaming.

If we return to the valuation of WBD, that’s a market cap of about $20B currently, and that gives a Price/FCF multiple of 3.3, surprisingly low. Of course, there’s a reason for that, the amount of debt on their balance sheet.

Debt Situation

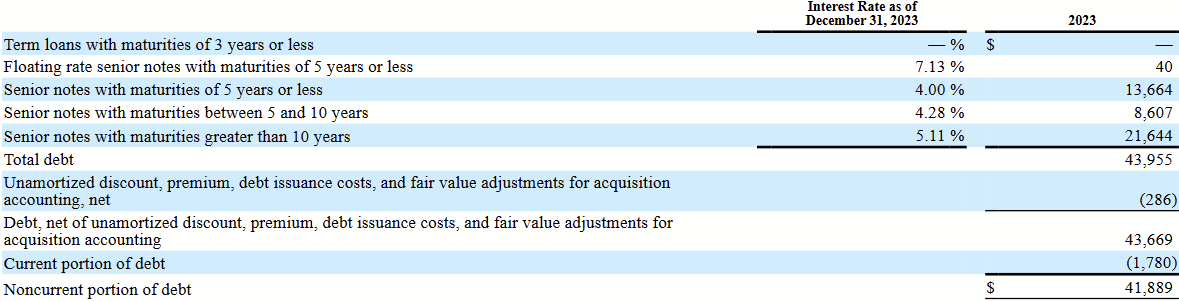

In their 2023 Form 10K, WBD reported $41.9B in long-term debt, double the current market cap. Yet, if we look at the interest and maturities, the picture is not as bleak as the market might have you think.

Debt (2023 Form 10K)

Most of the interest is less than short-term rates today, and the maturities are staggered, with most due ten years later or more.

Principal Due, Next 5 Years (2023 Form 10K)

As such, it’s conceivable that WBD should be able to repay this remaining principal, but it complicates a typical Discounted Cash Flow model. Moreover, we need to see what a normal amount of free cash flow is going forward. Let’s turn to recent comments by management.

Recent Conference Calls

Here, I’ll be referencing remarks from Q4 2023 earnings and a subsequent call in March.

CEO David Zaslav explained their approach to the debt in Q4 earnings:

We said we would be less than 4 times levered, and we are. We paid down $5.4 billion in debt for the year for a total of more than $12.4 billion since the deal closed. We’re now at 3.9 times and expect to continue to de-lever in 2024.

This is reassuring, given what I just mentioned, but this easier to accomplish if they can grow FCF. What clues have they given on that? CFO Gunnar Wiedenfels stated:

For D2C, which clearly is the top priority here from a growth perspective for us, we’re committed to maintain profitability, but as we said last time we spoke to all you guys, is we’ve restructured the business. $2.2 billion of profit improvement in 12 months. From here, the priority is going to be different. We’re not going back to subs at all costs, but we want to fuel profitable top line growth, and that’s going to be guiding us as we go through this year and beyond.

Zaslav also added:

Free cash flow is a key metric for us. And we said we’re going after it to have generated the $6.2 billion, but also just the 60% conversion, this company — in a year where we held back dramatically on selling our content to third parties, where you saw — I think it was almost $1 billion in difference year-over-year in terms of the content that we sold.

Both of these statements indicate that they believe there is room for growth of FCF, particularly as there were forces even in 2023 that created extra costs or forced them to miss out on revenues. Some of these were related to getting the merger done. Some were related to the writer’s strike. The point is that more upside exists than recent years suggest.

Focusing on DTC, this is their targeted area of growth going forward, and it’s undoubtedly one where investors are focused because streaming is king nowadays. Given the strength of streamers like Netflix (NFLX), how does WBD get in on that opportunity?

WBD’s Streaming CEO, JB Perrette, mentioned the following in the March call:

We had to launch and design a new tech product with the launch of Max, which took us some time, which we did in the U.S. last May. We finally started globalizing the product a week ago when we launched in Latin America successfully, and we’re launching in Europe. But the growth piece of it — so the profitable growth piece of it, the growth piece of it is now right in front of us.

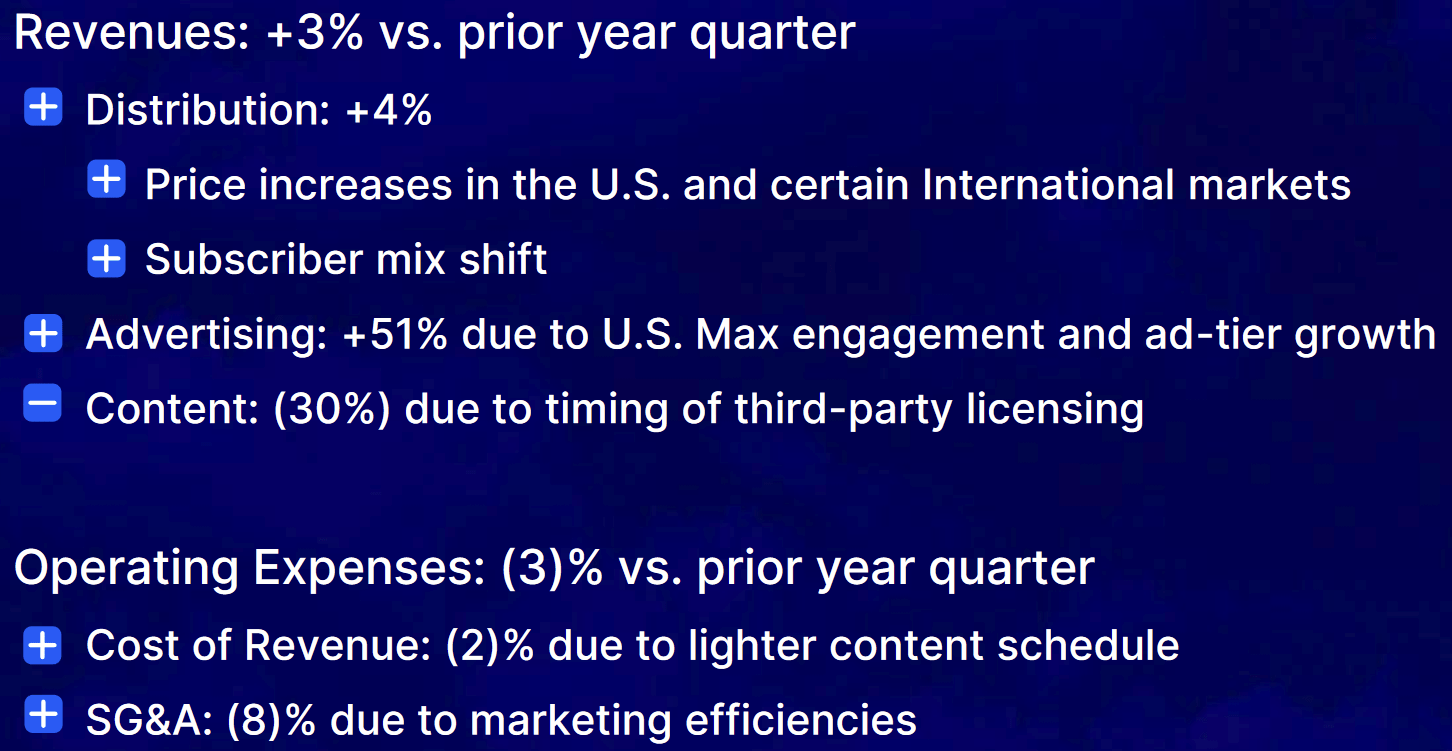

Q4 2023 Company Presentation

The slide above shows how some of these trends to grow DTC’s FCF began in 2023, with lower costs, price increased, and more revenue in advertising (benefiting from more time spent using Max).

I believe the DTC segment can continue to grow with many of the problems of 2022 and 2023 behind it.

Valuation

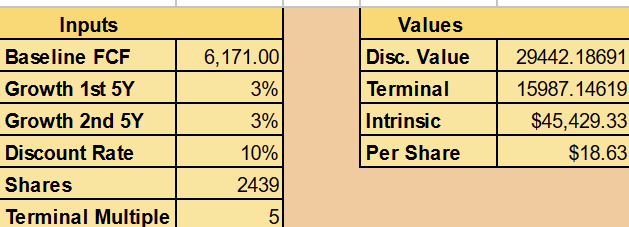

With the information we have, I think we can do at least a conservative valuation. I’ll make the following assumptions:

- $6,171M as baseline FCF

- 3% average annual growth

- Terminal multiple of 5

My baseline FCF is 2023’s number. Seeing as how there were things weighing down FCF in 2023, I think it’s reasonable to use that as a launching point. Plus, they have durable brands and assets behind that cash flow: DC Comics, Looney Tunes, Lord of the Rings, Harry Potter, Game of Thrones, Dune, Barbie, Cartoon Network and more.

I’m assuming 3% growth to keep it conservative, but given that DTC’s revenues were up 3% with lower costs and the room there is for global expansion, along with the profitability of the two lines and shrinking interest expense, I think this is doable. A terminal multiple of 5 is factored in to allow for continued market caution about the debt.

Lastly, I have modified the valuation of future cash flows to subtract the principal repayments on that debt, using the repayment schedule that was shown earlier.

Author’s calculation

These inputs suggest that a fair value of the company, even taking into account the debt, should be about $45 billion and at least $18 per share. As such, I think we’re getting an established media empire at a surprisingly attractive discount.

Risks

The main risk is what we already discussed: the debt. 2027 in particular has one of the largest maturities, at about $4.7B. If there is a bad year for WBD, namely that year, it could find itself in a liquidity pinch if FCF dips too low.

Additionally, while the streaming service is capital-light, the studios segment is not, and films that flop at the box office are painful. In the earnings call, they mentioned their plan to start more DC films, with James Gunn making the next Superman. The superhero content market is heavily saturated, and folks are debating if they will have that consistent appeal that started with the Iron-Man and the first Avengers films. Disappointments here may not result in losses but could be a drag on FCF growth.

Conclusion

Warner Bros-Discovery is not Disney (DIS), and it has a lot of debt. To the broader market, this is reason to price it at just a few years’ FCF. Yet, I think WBD is still a decent business on its own and has reasonable means to repay what is rather cheap debt, with 2023 showing the seeds of that starting to sprout.

While an especially bad year would be riskier for them than other companies, they are also priced well below intrinsic value, even if you take out the principal repayments. For these reasons, WBD isn’t just a Buy. It’s stupidly undervalued.

Q2 2024 Earnings Call Transcript")