Thomas De Wever/iStock Editorial via Getty Images

Overview

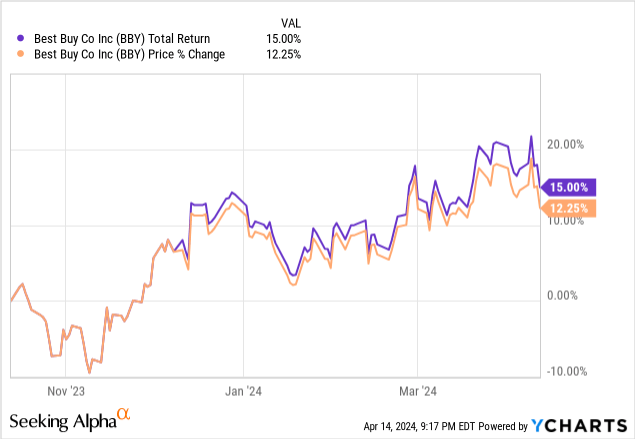

Best Buy (NYSE:BBY) has outpaced the S&P 500 (SPY) in total return since my initial coverage of the stock back in November of 2023. While I still remain unimpressed by the company’s fundamental business model, I am, however, impressed by the upward price movement over the last 6-month period. The price movement can likely be attributed to the last earnings report, where revenue and EPS came in stronger than expected. The price spike led me to this point of creating follow-up coverage in response. Is Best Buy still a good stock to own in 2024? I don’t believe so due to their shrinking sales revenue, slow adaptability, and current overvaluation.

While the dividend yield also remains attractive at 4.8%, I stay cautious of the overall vulnerability of their business structure. I fail to understand what makes Best Buy a stand-out experience compared to peers like Amazon (AMZN), which is awfully more convenient and flexible when it comes to pricing. On my last coverage, some comments responded by letting me know that the customer service experience is far more superior as you are able to physically speak with someone to inform you about a product. While this is true in nature, I don’t see it as a compelling enough reason to get me out of my house to buy some tech that I probably already researched beforehand.

In addition, the recent price movement upward makes BBY even less attractive than it was at prior levels. My prior valuation calculation resulted in an estimated fair value of $70.49 per share. As you can see, the price now sits above this level, so I will be conducting another valuation method by using a dividend discount model this time around. First, though, I would like to cover the vulnerabilities that BBY faces at the moment.

Vulnerabilities

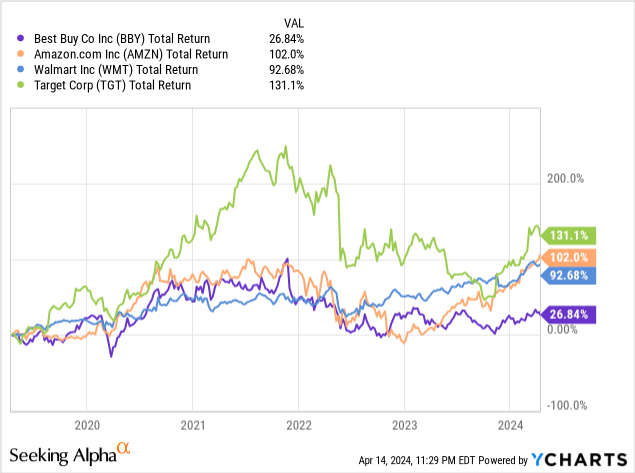

There are clear vulnerabilities here when it comes to the future of Best Buy. Their online presence isn’t quite yet able to compete with the likes of Amazon, Walmart (WMT), or Target (TGT). You can essentially buy 75% of the same products at these peers and as a result, BBY is losing more and more market share every year as they depend on their physical locations to carry the bulk of the sales. The reliance of physical locations is really something that brings down the potential for BBY. BBY has confirmed the closure of 10-15 stores this year.

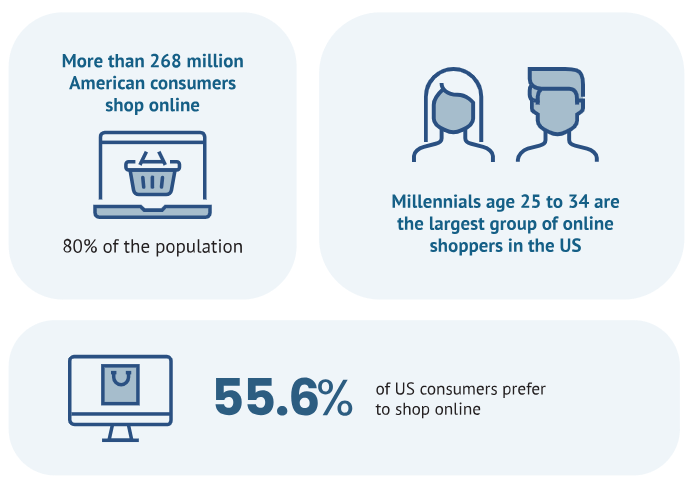

In addition, the e-commerce threat to BBY is something they struggle to compete with as sales continue to decrease over time. 55.6% of the population prefer to do their shopping online, and my assumption is that this rate percentage will continue to increase. Millennials are the largest age bracket that prefers to shop online, and this problem is running the course to become more prevalent as the data supports the fact that Gen Z also prefers to shop online.

E-commerce sales are expected to grow 10.5% in 2024 and will continue to increase through 2027. In addition, most online shopping is down from mobile devices and Best Buy is not he best optimized to support this. There are tons of shopping apps on mobile devices where building a user-friendly interface and design comes top of mind. Most important, most shoppers have changed their habits due to the shape of the economy; 73% to be exact.

Fit Small Business

High inflation, higher housing costs, increasing groceries, and the overall cost of living increases have people looking to save a dollar wherever they can. Where’s the best place with the best odds to find a deal on something you really want? Online, where you have an abundance of different avenues to find the lowest price possible. With a current US market share less than the competitors, I do not feel confident in their ability to grow since there are no known growth initiatives, stores are closing, and the outlook looks weak.

Financials

BBY’s Q4 earnings report beat estimates, but I believe that the overall sentiment was negative because revenue was down and the outlook for the next fiscal year was poor. Revenue came in at $14.64B, which was down -0.7% from Q4 of the prior year. This can be attributed to the fact that comparable sales were declined 4.8%, with the largest drivers of this within the home theater, appliances, mobile phone, and tablet categories. This loops me back to the first problem I have with Best Buy: all of these categories are things that people prefer to buy online now. There is virtually no longer a benefit of buying these products from Best Buy as opposed from their respective manufacturers.

If I want a new Samsung tablet, I would just buy it from Samsung’s site where I can also trade in a previous device, pay for a warranty, or maybe even use a discount code. Ordering from the manufacturer’s site also likely has a free shipping policy and a flexible return policy. There is no added benefit of taking the drive to Best Buy to get a product.

People may argue that BBY has the physical appeal of getting to see your product out in person before purchasing. Speaking from experience, though, there have been many times where I see an item in store and then ultimately end up buying it from another source because I found it for a cheaper price. I believe that this e-commerce vulnerability will ultimately lead to Best Buy’s continued downfall in store sales and flat revenue.

Next, I believe that the slow adaptability has also been a cause for the decrease in profits. Management stated that the decrease in sales caused by the categories I previously mentioned was offset by the gaming category, where sales increased. The gaming sector has exploded since the pandemic, with revenues expected to grow from $262B in 2023 up to $312B in 2027. If this is the case, why doesn’t BBY take the time to invest in this category to make it a more fleshed out experience. Best Buy’s gaming aisles are so outdated with older titles and very limited in selection. They also lack the variety in gaming related hardware as well, and I believe this to be a huge missed opportunity.

BBY Q4 Results

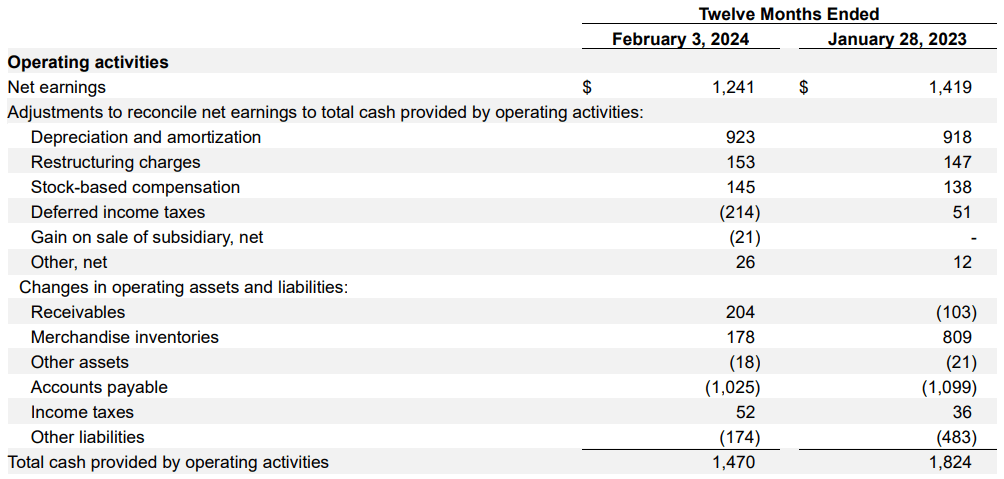

Domestic online revenue was $5.1B, and this was a decrease of 4.8% on a comparable basis. We can see how operating activities saw a decrease and resulted in a lower level of cash flow. Management’s guidance for FY25 is that they expect revenue to come in at around $42B. This would be an additional decrease from the most recent revenue of $43.4B.

With this negative growth in mind, I do not see a light at the end of the tunnel for Best Buy unless they make some changes to adapt to the current environment better. While their balance sheet remains solid with $1.47B in cash from operations, the revenue growth has been lackluster. The revenue has actually decreased by 6.15% YoY. In terms of valuation, I believe the stock to also be overvalued at these levels since there are no growth catalysts at the moment.

Valuation

In terms of valuation, BBY sits at a price to earnings ratio of 13.08x. While this is slightly below the 5-year average PE of 13.23x, it sits well-below the sector median of 15.78. In addition, the current average Wall St. price target sits at $86.11 per share. This represents a potential upside of 10.4%. However, these metrics don’t automatically mean that BBY remains undervalued.

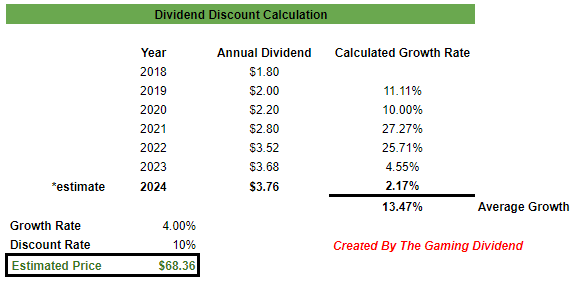

Compiling all of the prior years’ dividend data can help us determine an estimated share price by using a dividend discount model. Compiling this data starting in 2018, we can see that the dividend has grown by an average CAGR of 13.47%. There were two large raises in 2021 and 2022 following the rise in consumer spending. The effects of the pandemic, increased unemployment benefits, stimulus payments, and remote work fueled spending to higher levels which enabled such strong dividend raises. However, that period is now done, so the raises have tempered down, resulting in a very modest raise of 4.55% in 2023 and a slight bump of 2% to start 2024.

Author

Management’s forward-looking guidance states an expected comparable sales decrease of -3%. However, the operating income is expected to grow at approximately 4%. Therefore, we come to an estimated fair value of $68.36 per share. This means the price is currently trading at a premium of about 12.5%. For what it’s worth, Seeking Alpha’s Quant also rates Best Buy as a Hold at these levels.

Despite the price trading at a premium and sales figures looking bleak, I think there is still value here with the high dividend yield. As much as I doubt the future profitability of the business model here, the current high-yield and excellent dividend growth rate have admittedly returned shareholders lots of value over the years.

Dividend

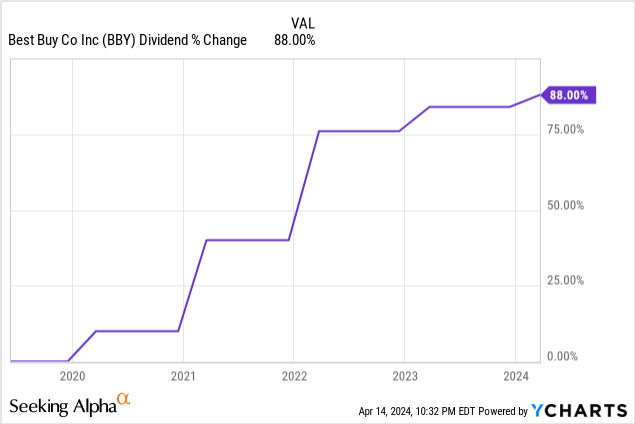

The dividend was recently raised by 2.2% in March. The new quarterly dividend is $0.94 per share, which brings the current yield up to 4.8%. All of the high raises from 2020-2023 has resulted in a dividend yield that trades significantly above the 4-year yield of 3.45%. Best Buy has done a great job with their dividend growth and has managed to grow their dividend for 13 consecutive years.

The dividend growth has been impressive, with a dividend CAGR of 14.87% over the last 5-year period. Even zooming out to a 10-year basis, the dividend increased at a double-digit CAGR of 18.46%. In fact, the dividend has increased by a total of 88% since the pandemic. With a current payout ratio of 58%, the dividend should remain relatively safe for the future. However, this payout ratio does sit well-above the BBY’s average payout ratio of only 37.7% and the sector median payout ratio of 32%.

However, I can’t help but think that this dividend growth comes from the lack of reinvestment back into growth avenues. Best Buy has announced the closure of 10-15 stores this fiscal year. It seems like a counterproductive move to reward shareholders with additional capital when store performance has slumped. Not to mention the previous earnings and outlook metrics, sales are still expected to be down for the year. There’s a sneaking suspicion that BBY is dishing out this extra capital towards dividend payments because they do not have an efficient place to put that cash that would further enable growth.

While the recent dividend increases have been large, we can already see the growth rate slowing down, with the two single digit raises as of most recently. While I don’t expect management to ruin their dividend streak altogether yet since they still have the cash to cover, I do anticipate the continued shrinking of the dividend growth rate when we take these negatives into consideration. Therefore, I will pass on a position, even though the high dividend yield remains tempting.

Takeaway

Best Buy is potentially overvalued here at this price level, but the dividend yield of 4.8% is still providing value to shareholders. The dividend growth rate has averaged double-digit rises, but I anticipate this growth to slow since sales aren’t keeping up with the distribution raises. However, BBY has been slow to strategically adapt to changing markets and take advantage of areas that are actually profitable, such as the gaming category. In addition, the combination of store closures and a weak outlook for the next fiscal year makes this hard to recommend. For now, I rate this as a Hold because I think there is still time to turn the business around and make necessary changes to better capitalize within the ecommerce space.

Q2 2024 Earnings Call Transcript")