antorti

Opportunity Overview

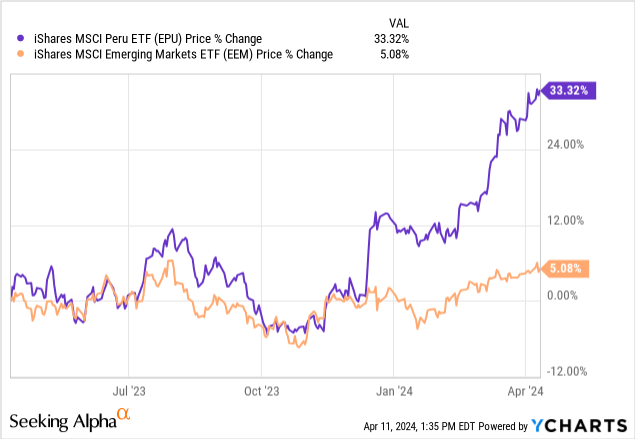

Equities in Peru have massively outperformed emerging market equities in the past year. Growth has recovered substantially, and the market could benefit from increased copper demand from economies like the United States and China. Peru may be one of the better ways to gain access to emerging markets this decade.

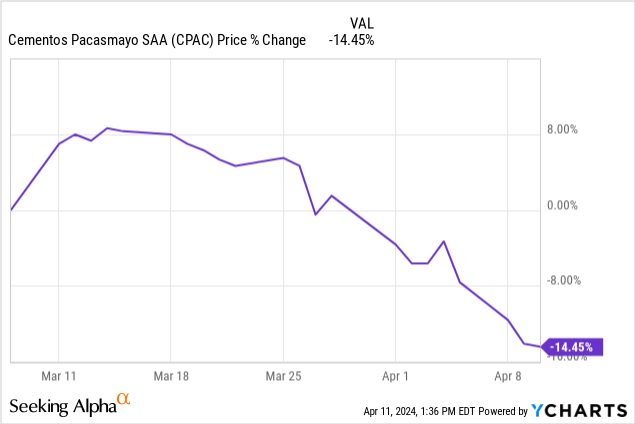

I originally covered the iShares MSCI Peru ETF (EPU) around a year ago and mentioned how this ETF was a convenient way to gain access to the market. However, I think it could be a good time to look at Cementos Pacasmayo (NYSE:CPAC), as this month looks like a solid entry point due to the short-term sell-off. Shares of Cementos Pacasmayo have declined by 14.5% in the past month following its disappointing 2023 results.

While concerns over the slower growth are relevant, it looks like shares of Cementos Pacasmayo are oversold and that 2024 is a solid entry point. I am planning to monitor the share price and to accumulate on any dips if the share price drops below $5. I think there could be an additional short-term sell off due to broader geopolitical risks, or company-specific events such as lackluster quarterly results in 2024. The company has a solid market share throughout Peru, and has a lot of pricing power, which can help it maintain favorable margins even if its revenue growth rate declines.

Peru’s Economy

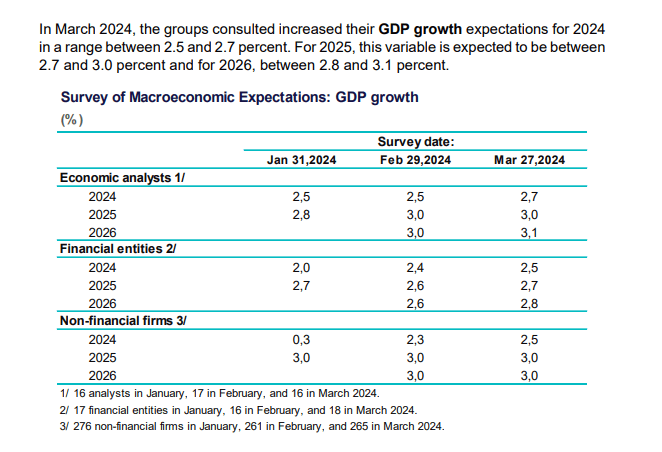

Peru’s economy is beginning to bounce back, but it is still likely months away from considering rate cuts to fuel additional growth. Peru’s Central Bank recently decided to keep rates steady due to inflation exceeding expectations. However, the country’s Central Bank has successfully brought inflation down from 8% to 3% and may be able to lower its current benchmark interest rate of 6.25% if inflation remains near 3%.

According to the latest projections from BCRP, Peru’s economy will only likely grow by around 2.5-2.7% this year and 2.7-3% in 2025.

BCRP

Any favorable commodity price movements, particularly in the price of copper, could help growth exceed current projections. The price of copper recently reached a 14-month high and could be headed higher if supply issues persist. However, it has still pulled back strongly from its 2022 high and could have a lot of room to run this year.

Copper Price

Macrotrends

Peru’s economy can benefit from a rebound in manufacturing in China and the United States, which could boost the demand for copper. These two countries are Peru’s largest export destinations.

The mining sector accounts for around 11% of GDP and 57% of its exports. Peru’s economy may be moving towards a new growth phase, following its record growth in 2021 and decline in subsequent years. Annual growth in infrastructure spending rose by a record 38% in 2021, following the slowdown in 2020, but is unlikely to sustain this growth rate. Peru’s construction industry will only likely have moderate growth, slightly above its GDP growth rate.

Cementos Pacasmayo Overview and Outlook

Cementos Pacasmayo is a leading cement company in Peru, with a strong market share in the Northern part of Peru. The company has diversified operations, providing cement products for residential real estate, infrastructure projects, and other industries. Furthermore, it has a favorable product mix (91% bagged cement), which allows it to sustain higher selling prices and consequently enjoy favorable margins. This setup has been particularly helpful in recent quarters, where the company has been able to boost its margins amid slower industry growth.

CPAC

Most of its customers include retail customers, who are between the ages of 25-55. Many of these customers, particularly in the North of Peru, may prefer to buy products from nearby companies to save on transportation costs. Its remaining revenue is derived from providing products to various private sector clients and infrastructure projects. One of its main infrastructure projects includes its work on the Chiclayo Airport. It also has a lot of larger private sector clients, including companies that are constructing shopping centers, supermarkets, and housing complexes.

Recent Performance and Outlook

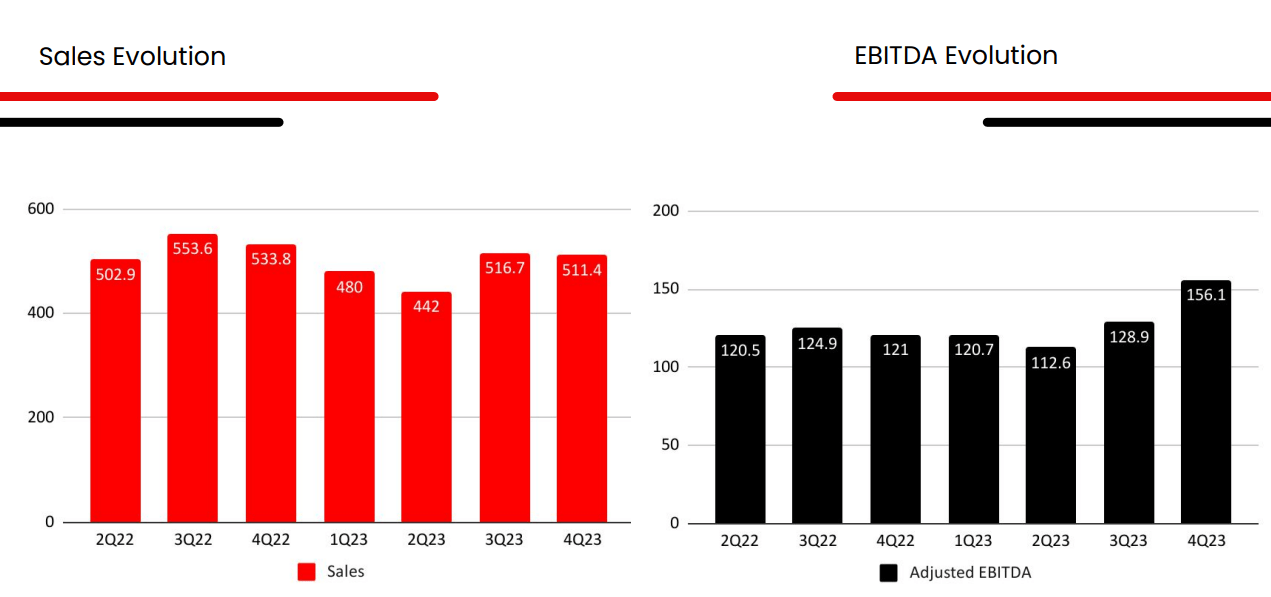

Cementos Pacasmayo had weaker performance in recent quarters, which has put pressure on its share price in March. Its cement, concrete, and precast shipments declined by 10.3% YoY last quarter. The company’s quarterly revenue has not surpassed the previous high of Q4 2022, as demand for cement in Peru has been weaker relative to 2021 and 2022.

CPAC Q4 Presentation

Cementos Pacasmayo’s revenue declined by 4.2% compared to the same period last year and dropped by 7.8% annually in 2023. The company cited various issues that resulted in weaker performance, including lower public and private investments and the negative impact of Cyclone Yaku. Moreover, this demand weakness also strongly impacted its self-construction segment, which is a key revenue contributor. The market has responded negatively to this circa 10% drop in demand, which was recently announced in February. However, there appears to be a silver lining, as margins improved this quarter due to its strong position in the market.

Cementos Pacasmayo has been substantially improving its margins in recent quarters. Even though the company’s revenue declined considerably, its EBITDA still rose by 29%. Given its strong market share in the country, particularly in Northern Peru, Cementos Pacasmayo may have a lot of pricing power in the coming years, which could help offset cyclical lows. Moreover, the company also mentioned how its lower production costs at its new Kiln in Pacasmayo helped it improve its margins last quarter. Based on current data, the company currently offers a circa 10% dividend yield, but this may be difficult to sustain due to its slower growth and increasing debt.

CPAC Q4 Presentation

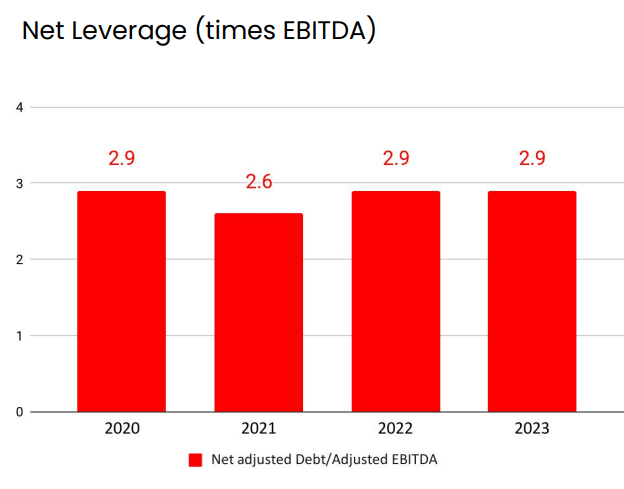

As of the end of 2023, the company’s debt to adjusted EBITDA was nearly 3x. The company’s debt has increased by nearly 30% since 2020, and its cash and short-term deposits recently declined by more than 50% compared to Q3 2023.

Global Peers

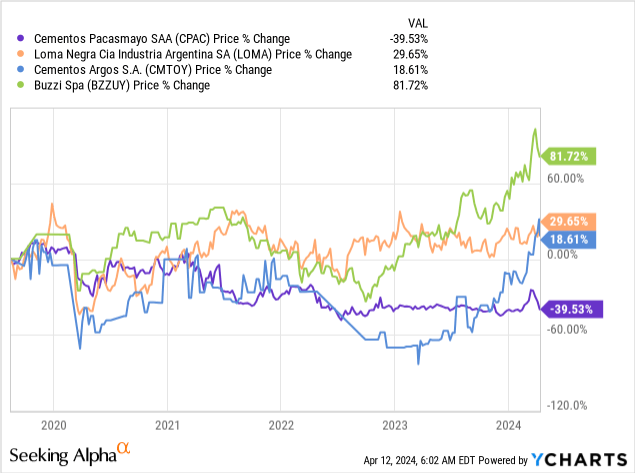

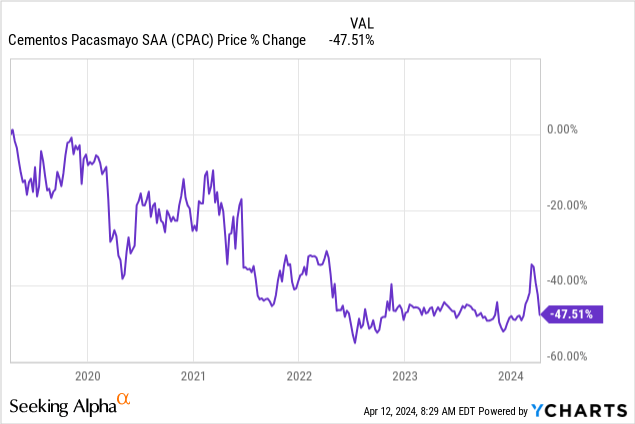

Cementos Pacasmayo has significantly underperformed many global cement companies in the past five years. This may largely be due to political and economic risks in the country rather than company-specific fundamentals, although a less dramatic sell off does seem befitting due to its 2023 results.

The main divergence in performance took place in 2022 when political risks in Peru were arguably much higher. The weight of political risks, slower macro conditions, and its recent earnings announcement have resulted in a strong sell-off.

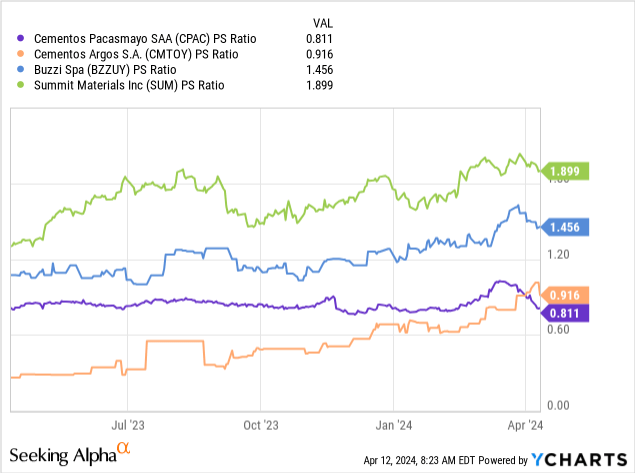

Shares of CPAC trade at a notable historical discount to other global players and even at a slight discount to Cementos Argos (OTCPK:CMTOY), its Colombian peer. However, this is one of the first months that this company begin to trade at a discount to Cementos Argos.

Final Thoughts

Shares of Cementos Pacasmayo look very cheap, especially because the company improved margins amid weaker demand. The company has a lot of pricing power in the country, particularly in the North, and should be able to endure any short-term economic setbacks in Peru. The company has a wide moat in the Northern region of Peru, where it can sell directly to consumers. However, the company also has the potential to increasingly branch into infrastructure and private sector projects, which currently only account for around 27% of its revenue. This investment thesis may become more enticing if Cementos Pacasmayo can capture some of the growth of infrastructure spending in Peru, and further diversify its revenue sources.

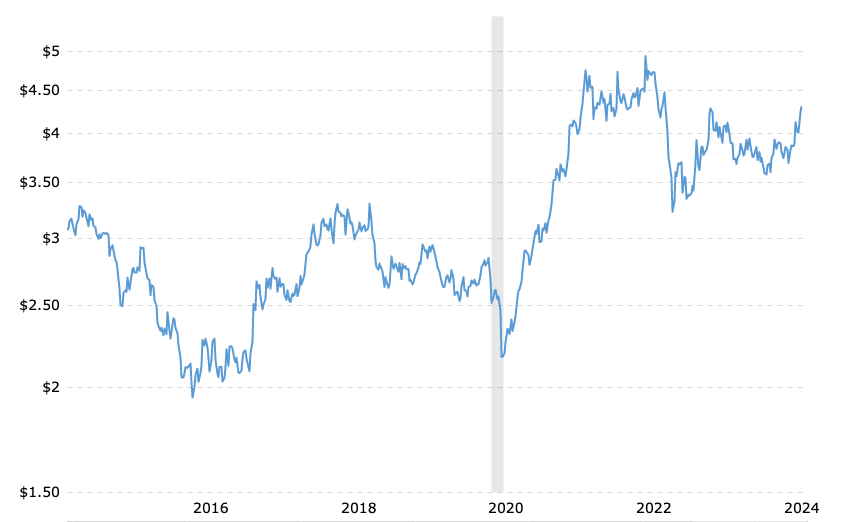

The concerns over the company’s rising debt, as it relates to its ability to maintain its dividend, are very reasonable. However, the greater value may lie in capital gains potential, as shares could double if they move back toward their pre-covid high. This company looks like an even better buy in the $4-5 range, especially if this is driven by economic/political news or any news related to the company potentially cutting its dividend.

I’m taking a wait and see approach, as I do not see any near-term improvements ahead, and I want to find out more information about its dividend yield. But I think this company is still worth holding on to at its current price and accumulating during any subsequent dips. I think it is reasonable for the company to trade at its annual revenue this year, which would result in around 25% upside in the short term.

Q2 2024 Earnings Call Transcript")