Timon Schneider/iStock Editorial via Getty Images

Orient Overseas International logo (Orient Overseas International)

Investment Thesis

Six months ago, we downgraded Orient Overseas (International) Limited (OTCPK:OROVY) (OTCPK:OROVF) from a Hold stance to a Sell, on the back of a weakening freight environment and expectations of more pain to come.

Bear in mind, this was before the war started in the Middle East. The day after our previous article on OROVY, Hamas attacked Israel, and on the 19th of November last year, Houthis hijacked a commercial ship in the Red Sea. This has been followed by rockets and drone attacks on several maritime vessels.

On the 21st of March this year, OROVY came out with their 2023 financial results, which is a good time to reassess their performance.

2023 FY Financial Results

As expected, the profit for the year was much weaker than the year before. That was also the main reason for our earlier downgrade.

Despite transporting 209,000 more TEU Y-o-Y, the net profit for FY 2023 was 86% lower, coming in at only $1.4 billion, as opposed to $10 billion in 2022.

Their freight revenue per TEU came down from $2,619 in 2022 to $1,027 in 2023.

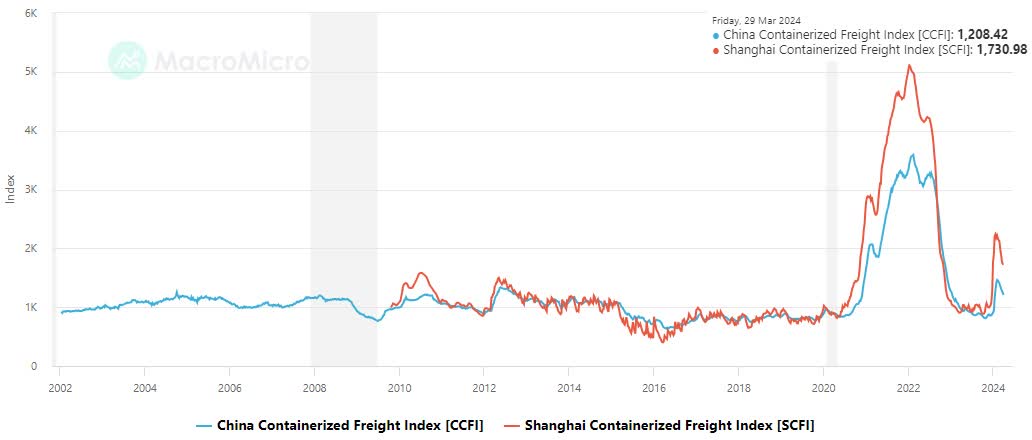

The market did spike when shipowners decided to reroute their vessels away from the Red Sea. However, it came down again in a fairly quick manner.

China Containerized Freight Index – 29 March 2024 (MacroMicro)

OROVY is an ADR that constitutes 5 ordinary shares. In the calendar year of 2023, OROVY paid out a dividend of $22.75 in July and another dividend in October of $4.25

The next proposed dividend of US$0.145 per ordinary share and a second special dividend of US$0.036 per share, should mean that owners of the ADR would get about $0.905. This should be payable in June this year.

As such, the TTM dividend yield becomes 8%

They have also decided to revise their dividend policy for the next three years.

The new dividend policy is set as a target payout ratio of 30% to 50% of the consolidated net profit attributed to the shareholders of the Company in the financial years 2024 up to and including 2026.

Valuation

The share price is not expensive when we look at past EPS, P/B and balance sheet strength.

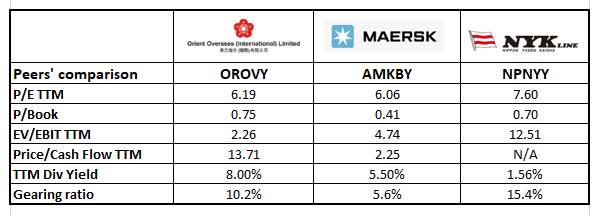

Valuation comparison to peers (SA)

Of the three peers we chose, we believe A.P. Møller – Mærsk A/S (OTCPK:AMKBY) has the strongest fundamentals of the three. Their cash of $6.7 billion is larger than the LTD of $4.2 billion, and more importantly, they have assets like vessels with a book value of 65.2 billion. That is far greater than their peers.

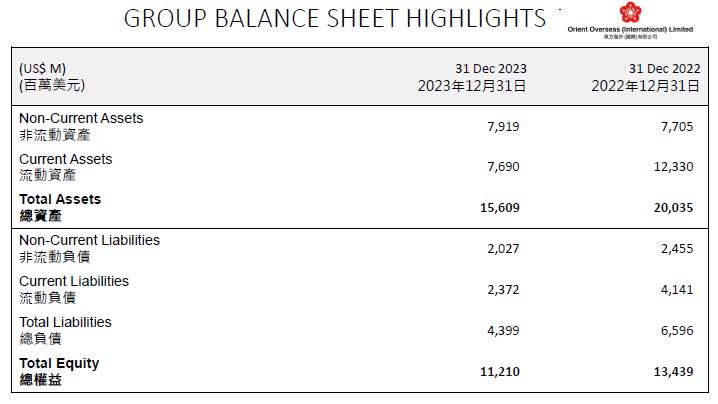

Fortunately, companies like OROVY and many of their peers, such as AMKBY, used the good times around 2021 and 22 to improve their balance sheets. It has made them more resilient and able to withstand low freight rates for some time.

OROVY – Group balance sheet 31 Dec 2023 (OROVY)

Business development

The problems in the Red Sea caused many liner companies, such as AMKBY and others, to divert their containerships around Africa when going to and from Europe and Asia. That adds roughly 10 days to the sea passage, which otherwise would have been about 26 days from Rotterdam to Singapore.

That is what caused the spike that took place recently, as we just showed in the previous graph. Without this diversion, we believe the continued addition to the fleet would have resulted in even lower freight rates than what we saw prior to 19th of November last year.

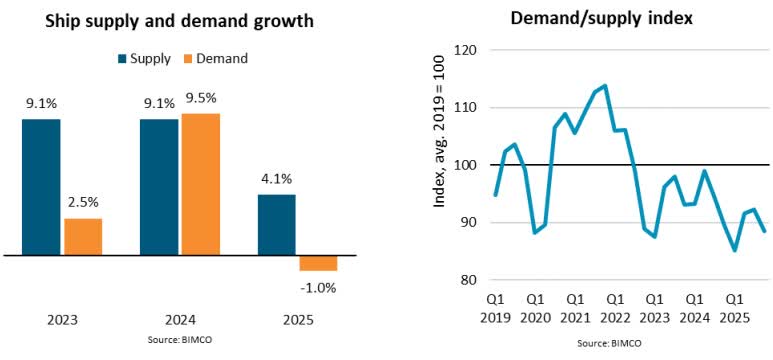

We would like to remind our readers about the negative supply/demand dynamics.

Container vessels – Supply and demand (BIMCO)

Risk to the thesis

Nobody knows how long the Houthis will be able to disrupt the normally safe passage through the Red Sea. One would think that the mighty military capacity of the rest of the world would solve this problem quickly, but clearly, that is not the case.

Our sell thesis is built upon a lower freight rate because of the huge new supply of large vessels. Under normal circumstances, it would take years to absorb this extra supply.

Conclusion

The positive thing that should help liner companies like OROVY to survive is their excellent balance sheet.

OROVY’s cash is $6.72 billion against LTD of only 1.44 billion.

However, when we look at their net cash-to-equity ratio of 0.47:1 at the end of 2023, compared with a ratio of 0.68:1 at the end of 2022. That is a reduction of 30.9% in just one year. They can afford to burn cash now, but this will only last another two years at that rate. A prolonged period of low freight rates would become troublesome.

They can also reduce some costs by delivering vessels which has been chartered in at higher costs. As of 1st January 2024, they had 25 vessels chartered in. This will fall to 20 vessels over the next two years.

All in all, it is still our opinion that now is not the time to buy OROVY.

The main reason is that we believe the extremely high dividend yields in the past will evaporate in this freight market. This will lead to a lower share price. It is not its valuation that will drag down the share price – it is the lack of earnings power and ability to remunerate shareholders with high dividends.

Our Sell stance remains.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")