MF3d

Lam Research (NASDAQ:LRCX) is the stalwart backbone of the semiconductor industry producing the wafer fabrication equipment required to produce semiconductors worldwide. While it doesn’t have the monopoly status of ASML Holdings (ASML) with its advanced EUV lithography machines, it is an integral and essential part of the semiconductor food chain, without which most of the industry would not survive.

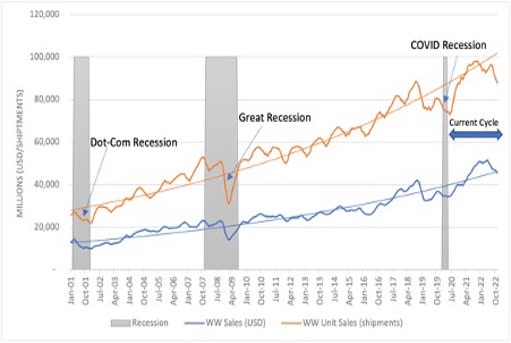

I own it and had planned to recommend it several times but often baulked at the cyclical, commodity nature of capital machinery and equipment for the semiconductor industry that usually has over-capacity in all its segments foundry, logic, and memory. The semiconductor industry has gone through cycles as we can see from the charts below for the industry and for the memory segment.

Semiconductor Market (SIA and WSTS) Semiconductor Memory Market (Onida)

Lam Research itself has gone through two revenue dips in the last decade, a 13% drop in FY2019, and more recently a forecasted post pandemic indigestion 15% drop in FY2024. Too often it’s difficult to catch the bottom and too easy to overpay, expecting good times to continue.

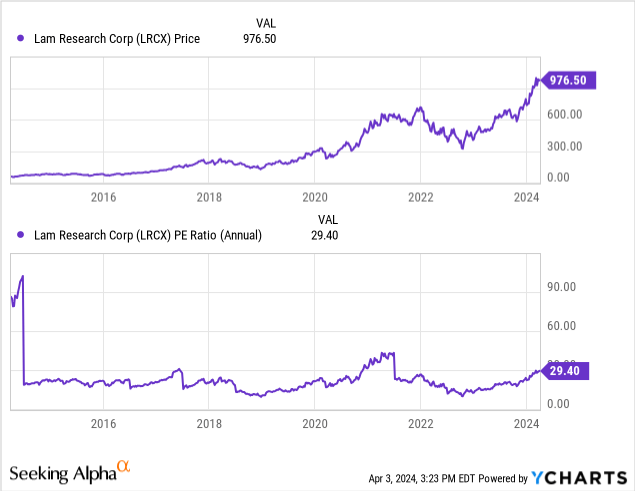

That said, Lam Research has already shot up 90% in the past year, on surging high bandwidth memory demand for GPUs from the likes of memory supplier Micron (MU).

Lam Research is expensive at 34x FY24 estimated earnings of $30 per share and could very well see sideways movement throughout the year, but given the growth and demand ahead, I would add more on declines and specially if there is a pullback in the overall market.

Let’s take a look at what makes it tick.

Strong demand and growth

Given the demand for the next three years on artificial intelligence capital expense buildouts, the wafer equipment industry is expected to grow at 8.4% per year from 2022-2027.

I also expect demand to stay strong and elevated through 2027 based on Nvidia’s extraordinary estimated growth for FY 2025 through FY 2027 on AI GPUs, and on Taiwan Semiconductor’s, the world’s largest semiconductor foundry, (TSM) growth. TSMC alone expects its share of AI revenue to increase from 6% to the low teens by 2027.

DRAM chip spending, which benefits from artificial intelligence buildouts and strong demand out of China plays to Lam Research’s strengths, as do smaller advanced nodes.

Here are revenue projections of two large Lam Research customers for the next three years, indicating the Lam Research is likely to get continued demand from its largest customers. Micron, which is one of the largest memory chip producers in the world is slated to grow a CAGR of 36% from its trough in FY2023. Taiwan Semiconductor, the most valuable semiconductor foundry in the world is also forecasted to grow 18% for the next three years.

Semiconductor growth catalysts (Seeking Alpha)

Strong, secular and durable growth in the past: Lam Research has done extremely well even without the AI jump and memory bump, and even with two revenue declines, the 10-year revenue CAGR has been 16% growing from $4.6Bn in FY2014 to $17.4Bn in FY2023 and EPS CAGR has been an extremely strong 28%, during the same period. And that has rewarded the shareholder very well, Lam Research’s 5 year return has been 405% and 10 year total return was 1,734%. Why am I even calling this a cyclical? These are truly secular growth company returns if one didn’t panic and held through the troughs. Lam Research’s revenues are a function of global chip volumes and overall chip complexity, and while cyclicality should continue in the former, but given the emphasis on AI GPUS, there should be more durable growth for the latter.

Market Leadership

The etch and deposition packing equipment markets, where Lam Research has more than 50% market share is forecasted to grow at 8% per year through 2031.

Strong chip manufacturing expertise, R&D and switching costs also give it competitive advantages.

R&D spend, which grew at a CAGR of 10% from 2014 to 2023, at an average 12% of sales is holding steady around $1.7Bn and doesn’t reduce even with lower sales. Since it is further downstream it doesn’t have to use as much CAPEX as Micron – it uses its capital far better. CAPEX spending totaled $2.9Bn in the last 10 years.

The AI factor

We’re seeing how well Micron has done with a stock price return of 93% in the past twelve months. I had recommended Micron in June 2023, mentioning that memory chips would be a key factor in AI expansion, and that Micro’s management was very confident that they were at the bottom of the cycle with significant improvements in average selling prices and demand growth. I should have gone further downstream and bought Lam Research as well, but I believe that the next three years will still have excellent growth. I too am surprised how strongly AI has contributed to demand trends, which indicate rising layer counts in 3D NAND chip and demand high-bandwidth memory DRAM chips for artificial intelligence. Demand should also increase for gate all-around transistors and advanced packaging for the same reasons.

Risks

Geopolitical: While the US government has targeted the high end of the market, namely Nvidia’s H100’s and also ASML’s EUV equipment to restrict China sales, the pressure on Lam Research for export restrictions is far less. Lam Research has a 40% exposure to China, far more than any other region or country, and it will remain a contingent threat.

Patterning gaining strength over etching: Within semiconductor wafer equipment, there seems to be a shift from etch and deposition equipment, which are Lam Research’s strengths to patterning, a segment led by ASML, which gained market share in 2023.

Capex and R&D intensive: Lam Research has to plough back cash for R&D and Capex, and in the past ten years spent $12Bn for R&D, and $2.8Bn on Capital Expenses. Lam Research is about 65% the size of Applied Materials, (AMAT) its largest competitor, and constantly needs to invest in R&D and Capex to keep and hold its market share. Still R&D grew at a much lower CAGR of 10% per annum over the last ten years, as compared to 28% earnings growth.

Large exposure to memory demand cyclicality – While Lam Research’s December 2023, quarter sales rose 8% sequentially to $3.76 billion, it was a 29% drop year over year, and NAND flash chips took a nosedive in 2023.

Competition

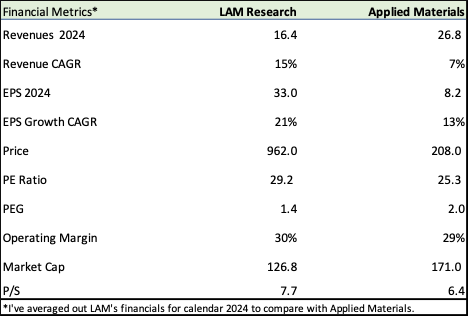

Lam Research and Applied Materials (Seeking Alpha, Lam Research, Applied Materials, Fountainhead)

Lam Research does stack well against its much larger competitor Applied Materials. Its forward revenue growth at 15% is double that of Applied’s 7%, Its EPS growth of 21% is also vastly superior to Applied’s 13%. Not surprisingly, it does sport a higher multiple of 29x earnings compared to 25 for Applied, but again is way better when it comes to Price Earning Growth, its PEG ratio a mere 1.4 to 2 for Applied Materials. Both have excellent operating margins at 30% and 29%.

Financials and Valuation

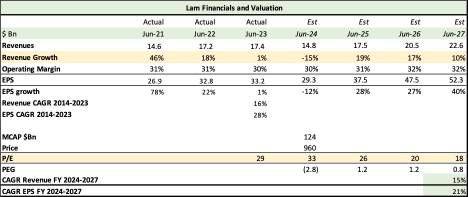

Lam Research Financials (Seeking Alpha, Wall Street, Barron’s, Fountainhead, Lam Research)

Lam Research did fairly well in the cyclical semiconductor industry, with only two periods of revenue drops in the last ten years, dropping 13% in FY June 2019, and is forecasted to drop 15% for FY June 2024.

Smoothening it out over 10 years, Lam Research has actually grown from $4.6Bn in FY14 to $17.4Bn in FY23 – that’s an impressive revenue CAGR over these 10 years of 16%.

Similarly, in FY2019, EPS dropped 13% but over 10 years it grew at a humongous pace of 28%, clearly operating leverage and better margins boosting earnings at almost twice the pace of revenues. For an equipment maker subject to peaks and troughs in semiconductors, this is excellent for a cyclical and gives me a lot of confidence that Lam Research can bounce back from bad times very strongly.

Lam Research is slated to drop FY24 EPS by 12% to $29.26, that too after barely eking out a 1% gain in FY23. However, based on analysts’ consensus and my estimates earnings should rebound strongly by a CAGR of 21% in the next three years to $52 per share. As we can see from the table FY23 and FY24 were periods of indigestion from the heady pandemic growth of 78% and 22% in FY21 and FY22 respectively.

The good part is operating margins have stayed above 30% consistently even in the current down year – Lam Research is fairly disciplined in reigning in costs.

Going forward, revenues should grow at a CAGR of 15% in line with its long term CAGR of 16%, and EPS should grow at 21% from a higher base.

Lam Research’s significant shareholder returns have been funded with its heady cash flow, cash generation has been exemplary with $24.7Bn in the last 10 years and $18.7Bn worth of buybacks have led to share count reducing by 22% from 175Mn to 135Mn shares.

The big hump to getter over is the price – Lam Research has already risen 90% in the past twelve months like its cyclical peer Micron, some of the forecasted earnings growth for the next three years is already priced in.

I would conservatively value Lam Research at 25 times earnings, at 33x it is way above its average as we can see from the chart.

Lam Research Total Return and P/E (Seeking Alpha)

Data by YCharts

At 25x 2027 earnings of $52, the stock is worth $1,300 in three years, 35% higher or a return of 10% per year + dividends. So, returns will be muted and not even close to the 90% price appreciation made in the past year. Ideally, this should be bought in the $900- $910 range to make a decent go of it.

I own it, I was late in buying it and will be looking to accumulate more at lower levels. I also believe that Lam Research could get a better multiple and that’s scope for further upside for the following reasons:

- The anticipated growth in semiconductors from AI requirements and buildouts.

- Market leadership in etching and deposition.

- Phenomenal cash generation, which has rewarded shareholders well with a lot of buyback potential left.

- The past 10 year EPS CAGR of 28% is testament to Lam Research’s ability to surmount cyclicality so much better than its peers and achieve secular growth type returns.

If Lam Research gets a P/E multiple of 29, the stock would be worth $1,450 with a total potential return of 50% or 14% per year.

Q2 2024 Earnings Call Transcript")