Klaus Vedfelt/DigitalVision via Getty Images

I published my ‘Strong Buy’ thesis for Uber (NYSE:UBER) in January 2024, highlighting their improvement in the take rate and operating margin. I continue to view Uber’s stock price as undervalued, and the market has not fully appreciated Uber One membership growth and their potential for margin and FCF growth. Therefore, I assign a ‘Strong Buy’ rating with a fair value of $103 per share.

Uber One Membership Growth

Uber offers Uber One subscription services, priced at $9.99 per month or $99.99 per year. Members can enjoy $0 delivery fee on food and groceries, 5% discount on eligible deliveries and pickup orders and some other benefits for rides.

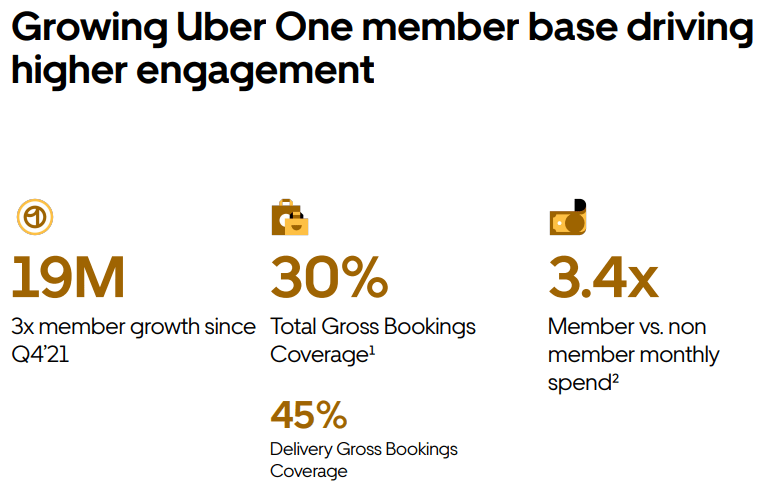

Since Q3 FY21, Uber has tripled the total number of members, reaching 19 million in Q4 FY23. As indicated in the slide below, members spend nearly 3.4x more frequent than non-members, and currently, members contribute more than 30% of total gross bookings, and 45% of total delivery gross bookings.

Initially, Uber tried to provide monetary incentives such as free trials to attract new members, and now they are shifting towards non-monetary incentives like customized services and matched rides to enhance retention rate and improve margin.

Uber Investor Presentation

I think Uber One is pivotal to Uber’s future success. As Uber owns both ride sharing and delivery services, their platform can provide a variety of services to their members. They are still in the early stages of expanding their member base. For comparison, Costco (COST) has 128 million members, and Amazon (AMZN) has approximately 167 million Prime members. Despite being launched just three years ago, Uber One has 19 million members now. I think they have a huge runway for future growth, especially when comparing to Costco and Prime members.

Additionally, Uber One can enhance the engagement with their platform and services. For members, the more frequent they use Uber’s services the greater the value they derive from their membership. In order to improve the value proposition, Uber needs to continue to expand the range of services in both rides and delivery markets. I am encouraged to see Uber launching new services such as Uber Reserve, Uber for Business, and grocery delivery among others.

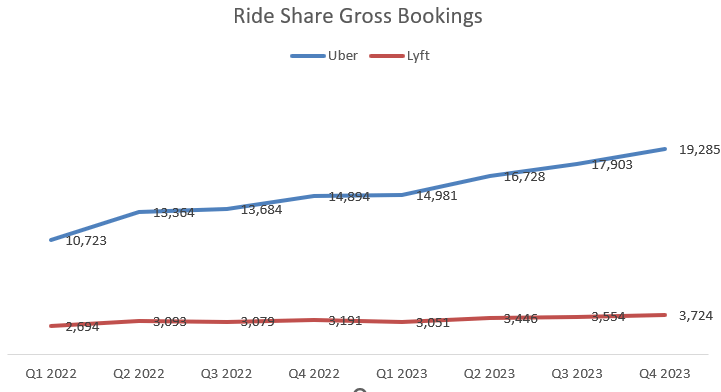

As depicted in the chart below, Uber’s mobility business has experienced strong growth in the gross bookings, while Lyft (LYFT), the main competitor, has been growing much slower.

Uber, Lyft Quarterly Earnings

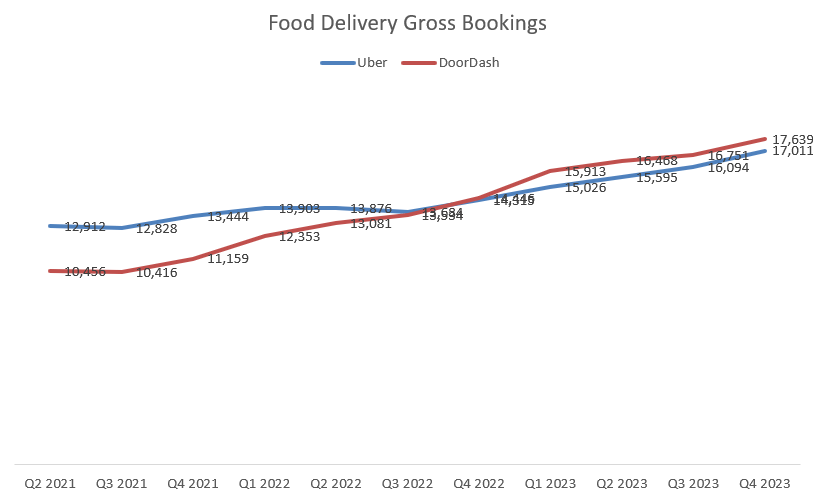

DoorDash (DASH) is the current leader in the food delivery market, with Uber steadily closing the gap. Both companies have achieved similar levels of gross bookings. In my opinion, Uber possess a competitive advantage in offering both ride share and delivery services on a single platform, and there is no other companies can copy this model.

Uber and DoorDash Quarterly Earnings

Improving Monetization

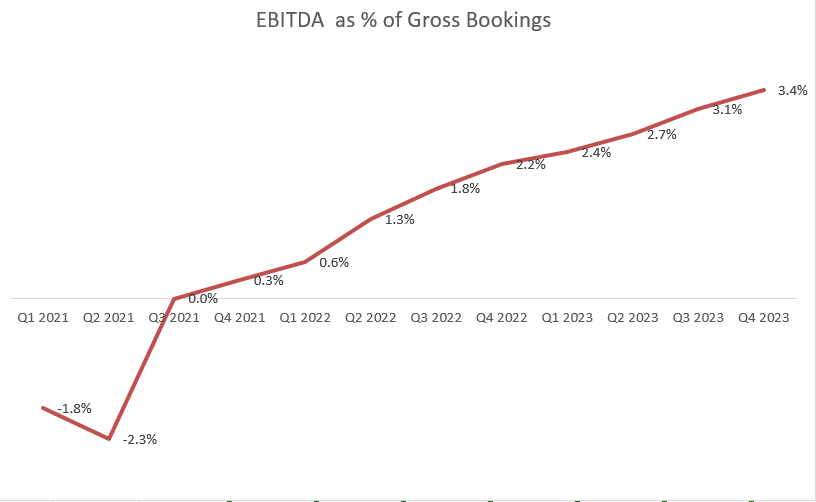

To better understand the take rate, I encourage investors to monitor Uber’s EBITDA as a percentage of gross bookings. As shown in the chart below, the monetization margin has steadily improved over the past few quarters. The enhancement in monetization explains Uber’s strong margin improvement and free cash flow growth.

Uber Quarterly Earnings

In my view, several factors contribute to the improving monetization rate.

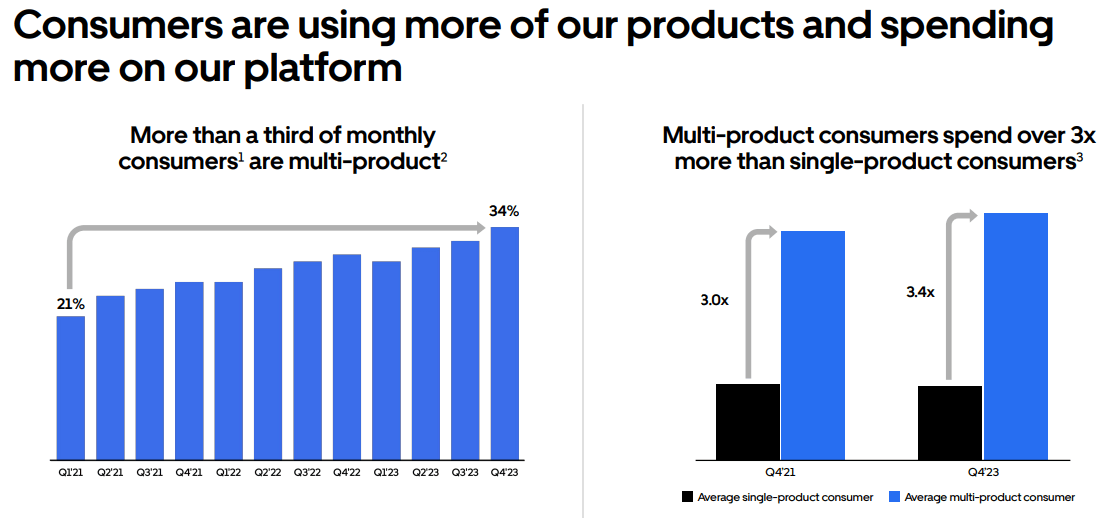

As disclosed during the investor call, consumers are increasingly utilizing multiple products offered by Uber and spending more on their platform. Specifically, average multi-product consumers spend 3.4x more than single-product consumers.

Uber Investor Presentation

As client initial acquisition costs are pretty much fixed, Uber can derive higher profitability from customers who use multiple services. To maximize profitability, Uber has done a great job to engage these customers by providing more relevant services. As disclosed, 50 million consumers used two or more of Uber’s products every month.

Additionally, Uber has been encouraging customers to switch from monthly to yearly subscription, which could significantly enhance the retention rate. A lower churn rate would make a substantial impact on their monetization rate, as Uber wouldn’t need to pay additional acquisition costs for existing customers.

Recent Result and FY24 Outlook

Uber announced their Q4 FY23 result on February 7th with 13% constant revenue growth and 21% gross booking growth. For the full year, they achieved a positive reported operating margin, marking the first time in their history. On the balance sheet, they have $6.2 billion in cash and cash equivalent and $9.45 billion in debt, with a net debt leverage of 1.7x.

Uber 10Ks

For FY24 growth, I am considering the following factors:

-Uber One Member Growth: As discussed previously, Uber One only has 19 million members so far, and Uber has a huge potential for their membership growth in the near future. As members use Uber’s service more frequently than non-members, the member base growth would contribute more to Uber’s gross booking growth compared to non-members.

-Mobility Business: The business growth is primarily driven by three variables: number of consumers, trips per consumer and gross bookings per trip. Uber offers different price-range services, including low-cost Uber XShare, standard UberX and Comfort, and premium Reserve, Black etc. The variety of services enables Uber to potentially increase both trips per consumers and number of consumers. Assuming 2% growth in number of consumers, 3% growth in gross bookings per trip ((CPI related)) and 3% growth in rips per consumer, the Mobility business is forecasted to grow by 18% annually.

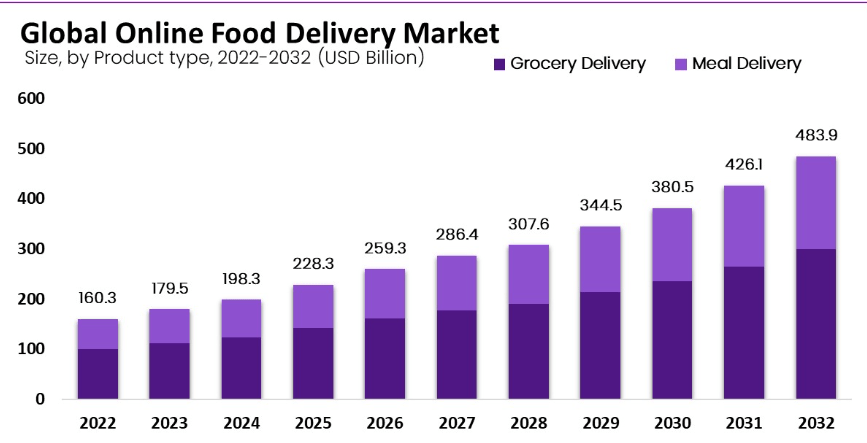

-Delivery Business: Market.us predicts that the global online food delivery market will grow at a CAGR of 12% from 2024 to 2033. Uber is well positioned in both grocery delivery and meal delivery markets. They have achieved an annual run rate of around $7 billion in grocery delivery, with 40%+ year-over-year growth, as disclosed in the earnings call. Given Uber and DoorDash’s leading positions, I anticipate both companies to grow faster than the overall market growth.

Market.us

As such, I assume the Mobility business will grow by 18% in FY24, and Delivery will grow by 15% year-over-year, and the combined revenue growth rate is projected to be 15% in FY24, as per my calculations.

Valuation Update

I estimate Uber will deliver 15% revenue growth in the near future as discussed above. They spent $1.8 billion in stock-based compensation in FY22 and $1.9 billion in FY23. The high SBC payout has led to dilution of their shares outstanding, with the total number of shares increasing by 4.2% in FY22 and 3.2% in FY23. Given the absence of any plans for share repurchasing, I forecast the total number of shares outstanding will continue to grow by 3% annually.

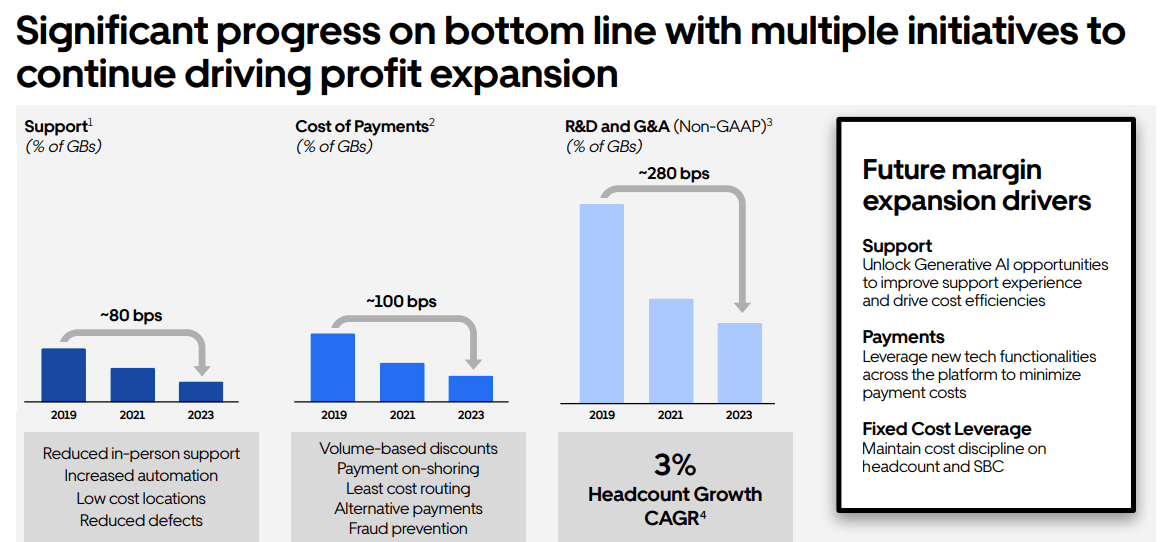

On the margin side, Uber has maintained a disciplined approach towards headcount growth. As illustrated in the slide below, the total headcount has only grown by 3% annually, significantly lower than their topline growth. In addition, Uber has been investing in back-office automation, leading to a significant reduction in in-person support over the past few years. As a result, their operating and support expenses as a percentage of revenue has dropped from 17.7% in FY19 to 7.2% in FY23.

Lastly, I think Uber has already passed the peak of investment in sales and marketing to build up their brand. The sales and marketing expenses as a percentage of total revenue have decreased dramatically over the past few years. In summary, I forecast Uber will deliver 50bps gross margin expansion, 30bps leverage from sales and marketing, 10bps leverage from supports and 20bps from G&A savings.

Uber Investor Presentation

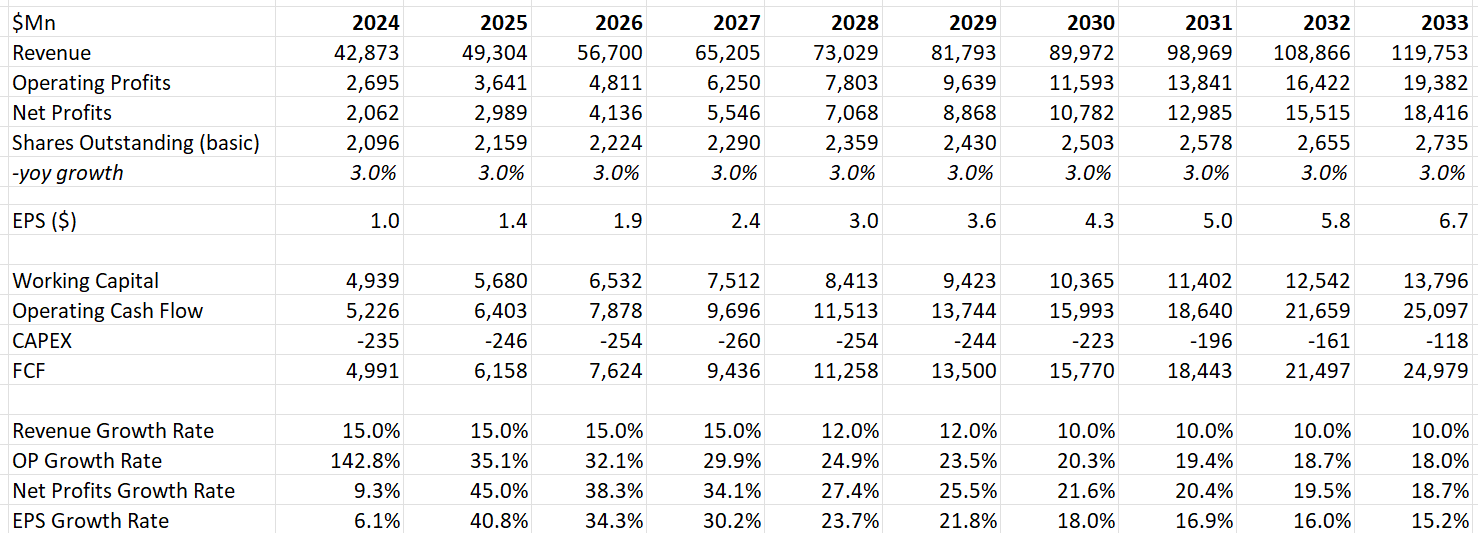

With these assumptions, the financial summary of my DCF model can be found below:

Uber DCF – Author’s Calculation

The WACC is calculated to be 10% with the following assumptions:

-Risk free rate: 4.25% ((U.S. 10-Y Treasury Yield))

-Beta: 1.25 ((SA’s DATA))

-Equity risk premium 7%; cost of debt 7%

-debt $9.5 billion; equity $11.2 billion

After discounting all the free cash flow, the enterprise value is calculated to be $209 billion in total. Adjusting the total cash and debt balances, the fair value of Uber’s stock is estimated to be $103 per share.

Key Risks

Insurance Costs: As communicated by Uber’s management, auto insurance cost increased by 20% year-over-year as insurance companies raise premiums to offset rising input costs. Uber is able to pass through the increased insurance costs to passengers; however, the pass-through would impose additional burdens on consumers, potentially impacting the total number of rides. It’s unlikely that insurance costs will decline in the near future as insurance companies have to raise premium to offset the rising costs of replacement parts and repair services.

Oil Price: The oil price has climbed by almost 15% in 2024 caused by concerns over suppliers and geopolitical risks. The rising oil price could potentially reduce the affordability of consumers, leading to reduced consumptions in dining orders, travelling and recreational trips. A high oil price environment is detrimental to Uber’s business growth in my view.

Conclusion

I think the market and investors haven’t full appreciated Uber One’s member growth potential, and Uber’s capability for margin expansion and free cash flow growth in the near future. Uber One could leverage both mobility and delivery services to enhance customers’ engagement with Uber’s platform. I give a ‘Strong Buy’ rating with a fair value of $103 per share.

Q2 2024 Earnings Call Transcript")