dani3315/iStock via Getty Images

TG Therapeutics Inc. (NASDAQ:TGTX), saw its multiple sclerosis drug BRIUMVI approved by the FDA at the end of 2022 and the launch began in January 2023. There was no shortage of results in the same year, and new partnerships were consolidated for marketing outside the US. Based on the results achieved in 2023, the revenue and earnings growth hypotheses are very encouraging for 2024, and although, to date, the share price may be overestimated, if future growth hypotheses are realized, an investment today could bring excellent results.

Regarding competition, it should be noted that some barriers to entry are evident and could protect the product by allowing significant growth in 2024 and 2025. Hedge funds have begun to reinvest in TGTX as they did in 2020 and 2021.

The risk is high, but the yield could be just as good.

Business Overview

TG Therapeutics, Inc. is a biopharmaceutical company primarily engaged in the development of drugs for multiple sclerosis.

As we can read from the TG therapeutics business update:

Relapsing multiple sclerosis [RMS] is a chronic disease of the central nervous system [CNS] and includes people with relapsing-remitting multiple sclerosis [RRMS]. RRMS is the most common form of multiple sclerosis [MS] and is characterized by episodes of new or worsening signs or symptoms (relapses) followed by periods of recovery. It is estimated that nearly 1 million people live with MS in the United States, and approximately 85% are initially diagnosed with RRMS.

The company also identifies and acquires promising new drugs and technologies for the treatment of B-cell diseases (Follicular Lymphoma, Chronic Lymphocytic Leukemia, Mantle Cell Lymphoma as well as Relapsing Multiple Sclerosis). As for R&D, it conducts clinical studies to evaluate the safety and effectiveness of its products in patients with various pathologies and collaborates with research and clinical centers around the world to accelerate the development of its drugs.

TG Therapeutics markets its approved products directly (in the US) or through licensing agreements, as in the recent agreement with Neuraxpharm Group for marketing in the EU

Investment Buy Thesis

My buy investment thesis is based on some upside points that could lead the company to perform well in the coming months. These are based on expected revenue and profitability growth in 2024, significant entry moats, favorable financial strength, and recent movements regarding share purchases. A less favorable point (but which nevertheless has elements of interest) could instead be seen in the existing pipeline. In the end, the share price seems expensive today, but seen from the perspective of future growth, appears to have high investment return potential.

Each aspect is analyzed in detail below.

BRIUMVI launch and 2024 perspective

2023 was a turning point for TG Therapeutics: following the approval of the BRIUMVI drug, the company immediately started with the commercial launch of the product with excellent feedback from the market, which recorded $90M in net revenue in the US. In 2023, the company also obtained approval from the European Commission [EC] for the treatment of adult patients with relapsing forms of multiple sclerosis [RMS] and this marked a further milestone for marketing in the European market.

In terms of market sizing, as we can hear in the latest earnings call:

We estimate there are approximately 40,000 patients going on a CD20 therapy each year, or about 10,000 patients per quarter. And in the fourth quarter of 2023, we had approximately 1,000 prescriptions come into the TG Hub, which would reflect approximately a 10% market share if all these patients were infused.

We could hypothesize that from 2024 onwards, there is still a 90% penetration rate that the company can attack, it would seem, in the best possible way.

If we analyze these data, which indicate a potential market upside of 90% which should be entirely incremental compared to the $90M of revenue already achieved, in my opinion, the new revenue target for 2024 of between $220M and $260M should be achieved.

If we add to the above target the potential development in the EU which should obtain the first results in 2024, I believe that 2025 could mark the turning point also with regard to the growth of profitability in terms of EPS.

BRIUMVI today, appears to have a solid moat

The company seems to have the goal of becoming a market leader in the anti-CD20 monoclonal antibody sector, and this necessarily requires, in addition to the effort of the entire company team, also a structural condition that allows the achievement of this ambitious objective.

In this case, the elements that differentiate the product on the market and make it unique concern primarily its administration, which requires only one hour of infusion every 6 months. This element which has a great advantage compared to competitors allows it to bring a benefit to the patient, which reduces the time spent carrying out the therapy. On the other hand, also allows the structures that practice the infusion to optimize the routes of care also reducing operating time.

A further element of competitive advantage is inherent in the protection of BRIUMVI in terms of patents: to date, the United States Patent and Trademark Office has issued 4 patents protecting the product with time coverage until 2042. This allows the company to have a sufficiently broad time horizon to be able to manage the business in the best possible way, as underlined by CEO Michael Weiss

…there’s a lot of detail in those patents, but I think the sum in some sense is that in addition to a new composition of matter patent that covers the glycosylation profile of BRIUMVI plus some use patents within that, we feel good about the 2042 patent protection. So we feel that we’ve got a really nice runway here, but the forms are issued, they are out there. People can read them. But the overriding concept is that it’s a composition of matter plus some use patents. 2042 is a nice new place for our exclusivity to run to.

From a technical point of view, it has also been verified that BRIUMVI is the only anti-CD20 monoclonal antibody to achieve an annualized relapse rate of less than 0.1 in Phase 3 studies and this represents a further fundamental element for the use of the drug in long period.

Financials

2023 saw the company close with an impressive track record of total revenue of $233.7M. This revenue, however, includes an important one-off ($140M) related to the license purchased by Neuraxpharm in July 2023 for the marketing of BRIUMVI outside the US territory. The impact of this revenue allowed the company to have a positive EBIT of $20.6M and a diluted EPS of $0.09.

These latest data, regarding company profitability, will be difficult to replicate in 2024. If we assume that the direct production costs ($14.1M in 2023) which impact 15.5% on BRIUMVI’s revenue of $90M in 2023 remain constant in incidence also in 2024, this determines a possible gross profit on a revenue estimated by the company at $220 M (conservative model) equal to $185.8M. If we subtract all other operating costs (which we could also estimate to be constant) equal to $198.9M, we obtain a negative operating profit of approximately $3M (estimate for 2024).

To achieve a positive operating result, given the above assumptions, revenue must be greater than $240M. In my opinion, the target could be reached in 2025 and this would lead to a probable positive EBIT and consequent growth in EPS.

Ultimately, the company records in Q4 -23 a $217.5M in cash and equivalents. If we compare this data with the operating costs recorded in 2023 ($189M) we can indicate with some certainty that the company has sufficient liquidity in its coffers capable of guaranteeing business continuity for at least one year. This data also underlines the company’s financial stability in the medium term.

Hedge Funds Shareholders

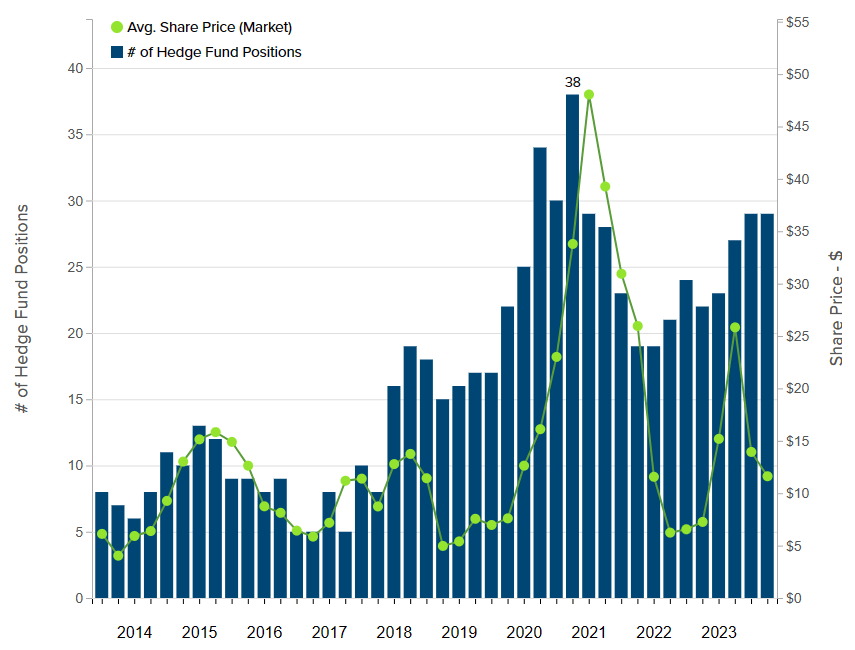

Insider Monkey

The graph above shows the trend in the number of hedge funds holding shares in the company. We can see how in 2020 and 2021 the hedge funds increased to reach the number of 38, and we can also see how a similar trend (growth in the number of funds) occurred in 2023 and is still underway. The current number is equal to 29 funds, the growth trend is a significant positive element and if confirmed also in Q1 – 24 this could represent a further element of confidence from the market in considering a future appreciation of the share price.

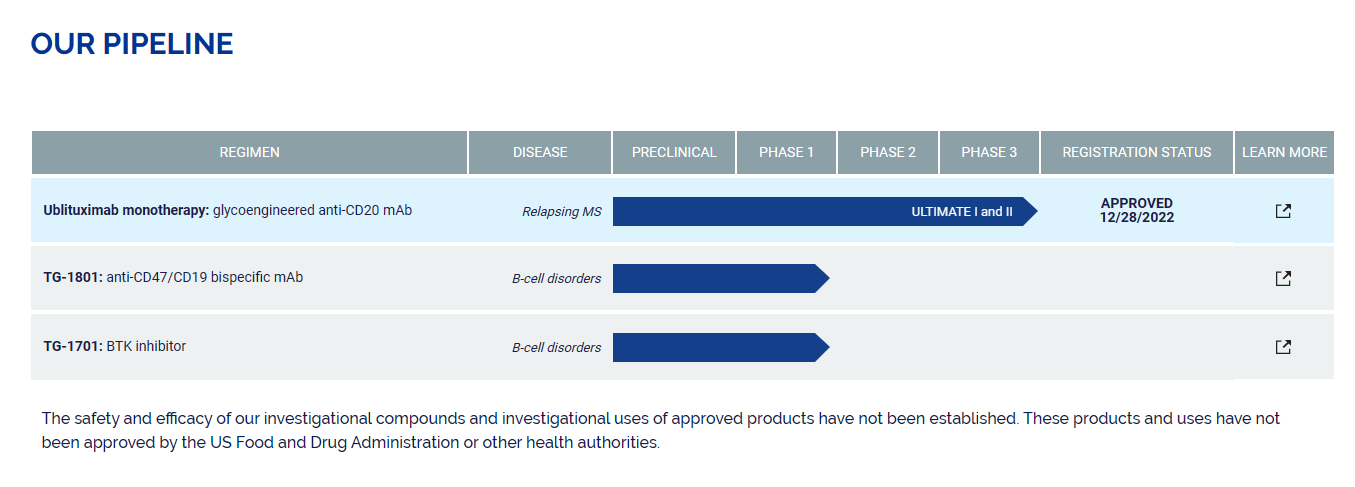

Pipeline and future developments

The first chapter already in progress concerns the commercial agreement with the partner Neuraxpharm relating to the development of BRIUMVI in Europe. The first and most promising country is Germany, but during the year, development should also take place in all the main European countries as well as subsequently in the rest of the world. This commercial agreement represents an element of possible advantage for the company, which will be able to count on a support partnership for development beyond national borders.

TGTX Web Sites

Regarding BRIUMVI, in addition to studies for expansion into fields other than MS, a further area of intervention is represented by the development of subcutaneous administration, which seems to be an activity that will be followed as a priority in 2024. The preliminary data from the Phase 3 study demonstrated that BRIUMVI SQ is non-inferior to BRIUMVI IV in the prevention of VTE (venous thromboembolism). Also, in this case, BRIUMVI SQ, if approved, could represent an important innovation in the treatment and prophylaxis of thrombosis and could represent a further commercial boost in the short term.

Worth mentioning that Phase 1 projects TG Therapeutics and Precision BioSciences have partnered to develop azer-cel, a CAR-T cell therapy, for the treatment of autoimmune diseases and other non-oncology indications. This agreement could potentially open new avenues for this cell therapy and therefore new business opportunities for the company in the long term.

In essence, for the near future, the company is strongly focused on its core product with possible further market expansion, but in the long term, there are currently no solutions in the pipeline that could lead to further developments of significant impact.

Price share valuation

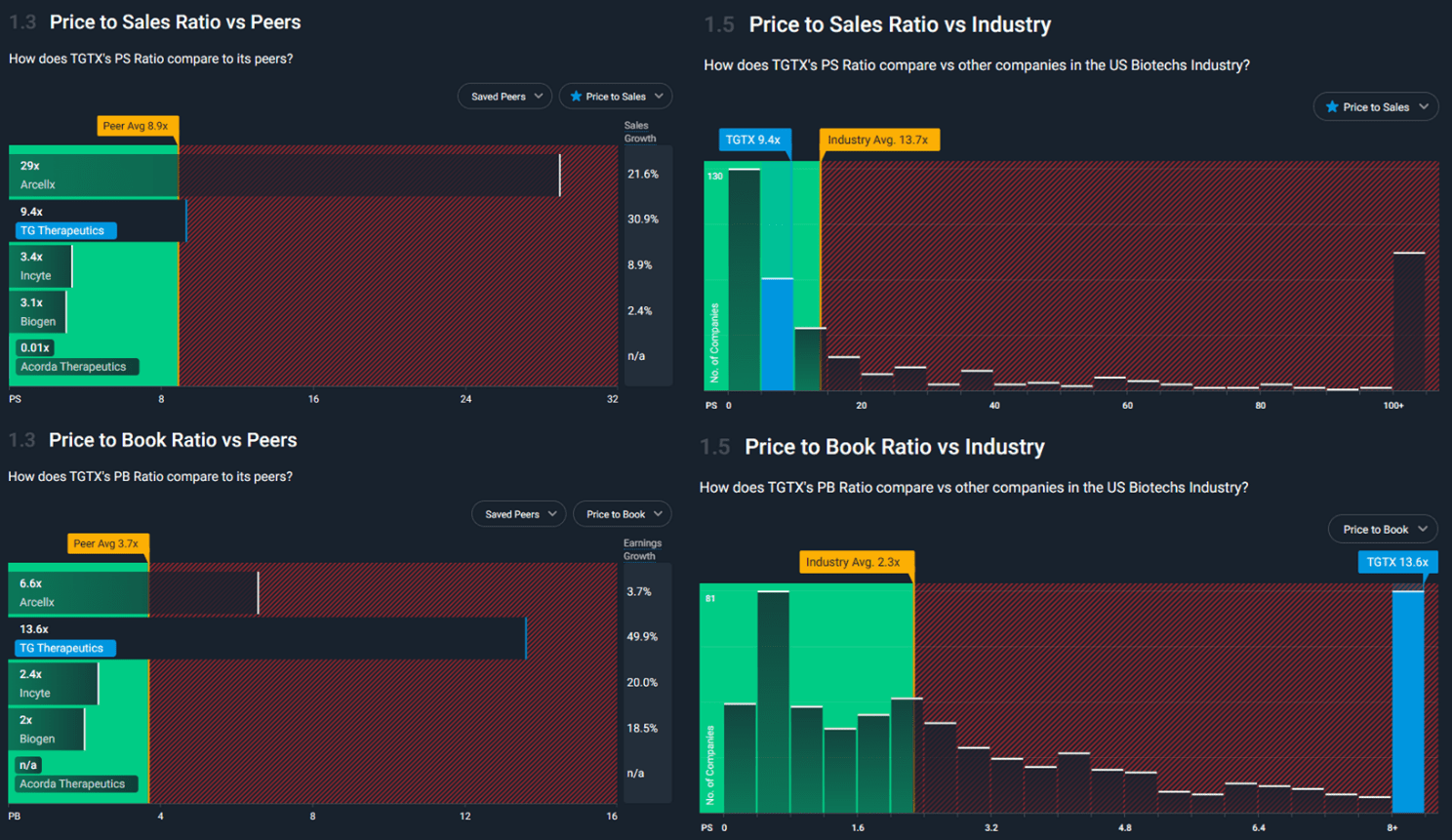

Using fundamental parameters such as P/S and P/B for a comparison, we note how TGTX has a P/S of 9.4 which is lower than the reference industry parameter (13.7) and quite in line with the identified peers (8.9). In terms of the P/S ratio, the price of TGTX appears to be in line with the market or even cheaper. The result changes significantly if we move on to the P/B ratio (13.6) which is a particularly high figure both when compared with the industry (2.3) and with peers (3.7). This last comparison makes us understand how the company has particularly restrained management about the book value, i.e. a very low value of total assets, and the same indication, in terms of management, is obtained if we consider the capex (equal to 0) and depreciation (almost zero). The company invests very little in capex assets. This could be seen as a wake-up call for the stability of the business in the long run.

Author Graph

Wanting to test a more objective evaluation based on current earnings, we use the EPV (earnings power value) model:

The method starts with EBIT. The second step is to add depreciation and amortization and then subtract stay-in-business CAPEX. The result is the Cash Trading Profit. I then subtract the taxes by calculating the amount using the actual tax rate that the company pays. The result is the After-Tax Cash Trading Profit

At least to calculate the total company enterprise value, I divide the After-Tax Cash Profit by the interest Rate I define as fine for this kind of Company (according to a study made by NYU, the cost of capital for Biotech is 9.05%)

The result is the Total Company Earnings Power Value. Dividing the result by the total number of shares, we find the value per single share. The table below shows the calculation for TGTX:

|

EPV |

|

|

EBIT |

20.60 |

|

Dep & amort |

0.20 |

|

CAPEX |

0.00 |

|

Cash Trading Profit |

20.80 |

|

TAX |

3.00% |

|

TAX |

-0.624 |

|

After TAX cash profit |

20.18 |

|

Interest Rate |

9.05% |

|

EPV |

222.94 |

|

Share in issue |

141.80 |

|

EPV per share |

1.6 |

$1.6 represents the actual share price evaluated according to the EPV model.

The company is growing rapidly, and this value does not take into account future growth prospects. But it represents what the company could be worth today if the cash profit remained constant over time, and provides us with an indication of how much the share may be overvalued in today’s price.

To consider the growth prospects of company profits, I use another model.

I think that this method (EPS growth model) may be more representative in the coming months because it considers the EPS growth parameter, while the previous method assumes that EPS remains constant over time.

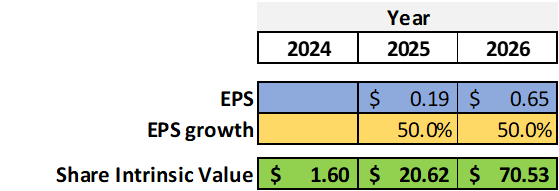

EPS Growth Model

Wanting to be conservative, let’s consider the lowest EPS estimate made by analysts for the years 2025 ($0.19) and 2026 ($0.65). These EPS estimates can be achievable (assuming an incidence of operating costs equal to 2023 and 2024) if we consider an increase in Revenue of $265M in 2025 and $345M in 2026. These revenue objectives could, in my opinion, be achievable considering the 90% further market penetration as seen in the previous paragraph ‘BRIUMVI Launch and 2024 perspective’.

Based on these conservative estimates, we also use an EPS growth parameter of 50% which is also conservative: EPS growth from $0.19 to $0.65 predicts an increase of $0.46 which related to $0.19 implies a potential increase of 242% (=0.46/0.19). In this model, I want to be more conservative and assume a maximum growth of 50%, which in my opinion, could be achievable.

Using the formula by popular investor Benjamin Graham: Intrinsic value per share = EPS x (8.5 + 2 g)

Where

EPS = earnings per share

g = EPS growth rate = 50%

Author Graph

Example of calculation for 2025:

Intrinsic value per share = EPS x (8.5 + 2 g) = 0.19x(8.5+2×50) = $20.62

Based on the above models, the current price of $14.7 seems to be overvalued if compared to the EPV model ($1.6) which in my opinion represents the estimate of the share value with current revenue and EPS conditions. The current price incorporates within a future growth factor that could be evaluated through the second model used (which considers the EPS growth estimate over the years) and which foresees for 2025 (if the growth hypotheses are satisfied) a share price of $20.62. This last price is, in my opinion, a price target that could be reached in the coming months and could lead to a return on investment of about 40%.

Peers

To compare the potential investment in TGTX, I propose a comparison with the following companies operating in the same reference market:

- Biogen Inc. (BIIB): Focused on developing drugs to treat neurodegenerative diseases such as Alzheimer’s and Parkinson’s and is developing new drugs to treat multiple sclerosis and psoriasis.

- Incyte Corporation (INCY): develops and commercializes therapies for hematological and oncological diseases, as well as inflammation and autoimmunity.

- Arcellx (ACLX) is a clinical-stage company developing CAR-T cell therapies for the treatment of solid tumors. Their lead product is CART-T BCMA, being tested for multiple myeloma.

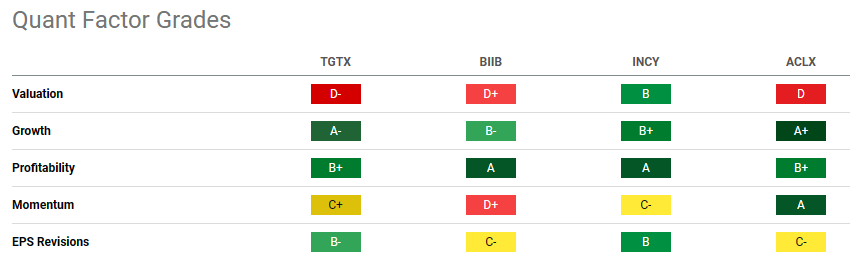

Using the Quant Rating of Seeking Alpha, we can see INCY is the only one to have a Buy rate today. All the other companies are rated a Hold.

Seeking Alpha

The main reason, which seems to penalize TGTX compared to INCY and also to other peers seems to be precisely the valuation. All peers have a good rating in terms of growth and profitability, while on Momentum and EPS Revision, there are contrasting grades.

Ultimately, TGTX does not seem to be the best solution when compared with INCY from these metrics. The main reason could be related to the valuation grade, which for INCY is a ‘B’ while for TGTX it has a ‘D-‘. We have seen in the previous paragraph how the current price seems to be overestimated (compared to current conditions and this is in line with the D-) but we have also seen how if future growth hypotheses are satisfied, in the coming months and 2025 the current price could become cheap. Precisely this last aspect makes me lean towards choosing TGTX also in comparison with the peers mentioned above.

Seeking Alpha

Risks

TGTX is certainly a high-risk investment, and the stock will most likely suffer from a lot of volatility in the coming quarters.

The biggest risk I see is related to the failure to reach the revenue targets set for 2024. If problems are encountered on the market that do not allow the company to reach the $220/260M of revenue confirmed in the latest earnings call, then the entire castle could fall quickly, and it would take a long time to regain confidence in new growth in the share.

The revenue and consequent profits are also linked to the commercial agreements for the distribution of the product outside national borders, and on this aspect TGTX has its hands tied or is completely entrusted to the work of Neuraxpharm. This aspect could also represent a possible risk not dependent on the company’s actions, and it would be almost impossible to recover lost sales in the short term if the commercial partner did not prove reliable.

From a long-term perspective, the development of new products seems to be at a standstill or very slow currently and this represents, in my opinion, a further risk element should there be any problems with BRIUMVI.

Conclusion

TGTX represents an interesting biotechnology company with an approved flagship product with a one-year history. This allows us to have some confidence in the possibility that revenue forecasts can be achieved. The share price already incorporates these prospects and stands at a very high value to date, but which could bring interesting results in 2025 and 2026. Hedge funds have begun to increase their holdings and this could be a further sign of positivity. The risk is high, but the return could be too. My rating is a Buy.

Q2 2024 Earnings Call Transcript")