jetcityimage

Investment Thesis

Wayfair Inc. (NYSE:W) is set to report its results for fiscal Q1 2024 on 2 May, premarket. And I believe that the stock is primed for a selloff.

At its core, we have a business that is barely growing its top line. Indeed, after the fiscal Q1 easy comparable quarter, the remaining quarters of fiscal 2024 will be up against much tougher comparable quarters.

Furthermore, the business is barely generating any free cash flow. And the free cash flow it does generate will struggle to make a meaningful indentation on the debt on its balance sheet, which reaches approximately $1.8 billion of net debt.

Consequently, I declare that over the next twelve months, investors will look back to $62 per share as a high price to aspire towards.

Rapid Recap

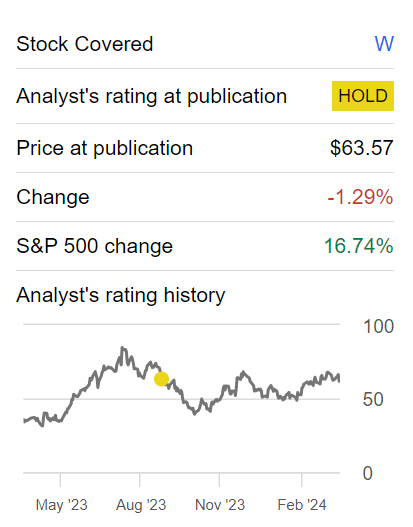

Last September, I wrote questioning whether Wayfair’s stock was already fairly valued,

Despite Wayfair’s outstanding outperformance in the past few months, I can’t help but feel a sense of uncertainty about the stock’s true value. While Wayfair has improved its financials, I question whether its stock isn’t already fairly valued?

Author’s work on W

Since that time, the stock has hardly budged, even though the market as a whole has been rampant, with the S&P 500 (SP500) up +16% in the same time period. But now I’m not neutral on W. Now I believe this stock is overvalued. Here’s why.

Wayfair’s Near-Term Prospects

Wayfair is an e-commerce company specializing in furniture, offering a vast selection of products. As an online retailer, Wayfair is focused on delivering an easy shopping experience and provide a one-stop destination for customers furnishing needs.

While Wayfair has implemented solutions to mitigate supply chain disruptions, increased shipping times and rising container prices are likely to impact its near-term profitability (more on this soon).

Additionally, the volatility of the macroeconomic backdrop, including softness in the home category and inflationary pressures, poses challenges to revenue growth and margin expansion in the near term. As a point of reference, consider Lovesac’s (LOVE) recent results.

Moreover, as the market continues to evolve, maintaining market share gains and sustaining customer loyalty will require further investment in customer experience and competitive pricing strategies.

What’s more, the company’s capital structure, including its convertible notes, adds complexity to the bull thesis. Thus, given this background, let’s now discuss its financials.

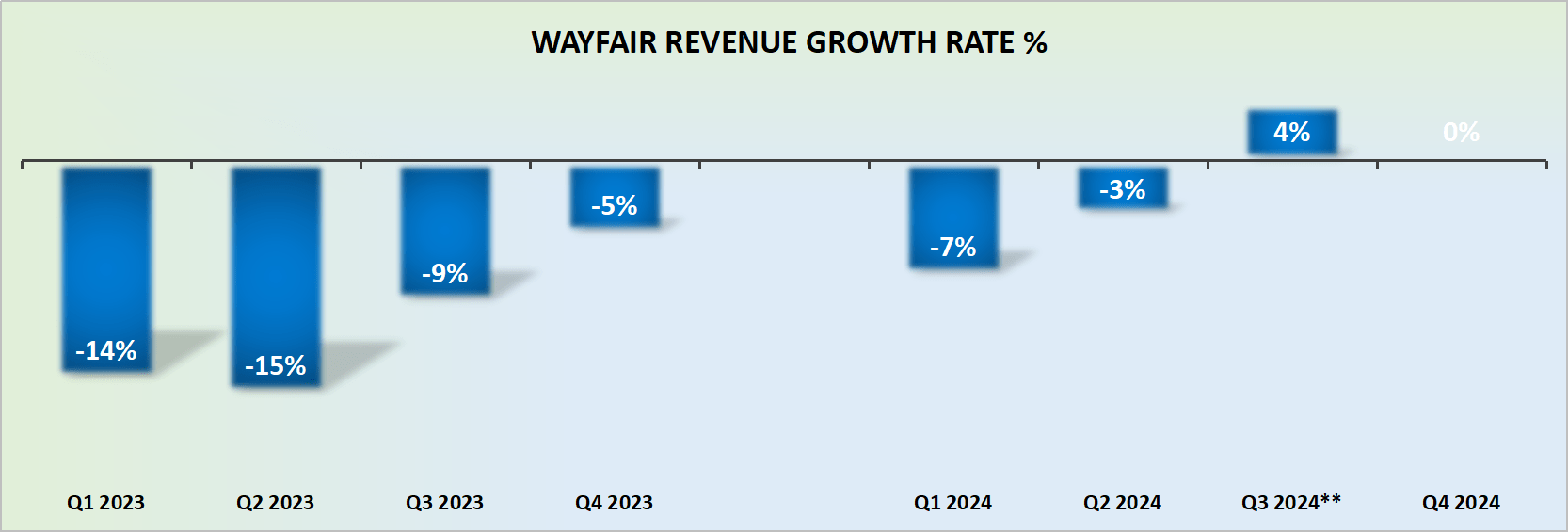

Revenue Growth Rates Don’t Reflect a Growth Company

W revenue growth rates

Wayfair’s recent financial performance raises questions about its status as a growth company.

Wayfair’s results may have stabilized of late, but there’s no way this is a growth company today. The best that investors can hope for is fiscal Q1 2024 delivering around 2% to 4% top-line growth, given that fiscal Q1 of the prior year offered Wayfair an easy hurdle to compare against.

But as the remaining quarters of fiscal 2024 come into view, Wayfair’s revenues are likely to once again deliver no top-line growth. Therefore, this stock should be afforded a premium commensurate with a growth stock.

In fact, Wayfair was once heralded for its meteoric rise in the e-commerce furniture market, but now it faces too much fierce competition from online players, for example, from Amazon (AMZN), but others too.

While Wayfair may have initially capitalized on a niche market, its massive success has become its downfall. Indeed, the relentless competition in the online retail space from discounted players such as Ikea has also taken its toll.

But it’s not only Amazon and Ikea that Wayfair has to contend with, and perhaps that’s the problem. Because there are numerous smaller companies, which are all vying for market share, which has intensified the competitive landscape, squeezing margins for Wayfair and complicating its path to sustained growth.

Moreover, the company’s aggressive expansion strategies, including hefty investments in marketing and infrastructure, have yet to yield commensurate returns in terms of profitability, and investors are notoriously impatient, something we turn to discuss next.

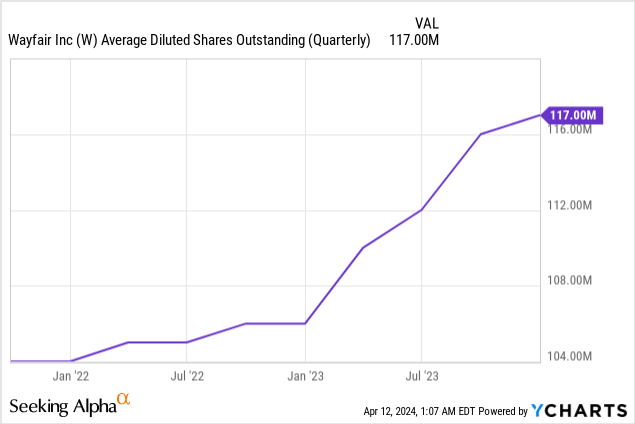

W Stock Valuation — Too Richly Priced

When it comes to investing, the fact that the share count is increasing, see above, doesn’t bother investors, provided that they are seeing a steady and consistent increase in profits and cash flows.

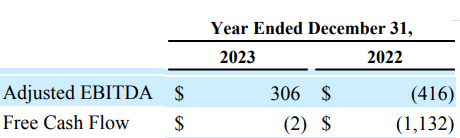

But when one focuses on Wayfair’s free cash flow line, one is reminded that despite a strong improvement in free cash flows in fiscal 2023, the business simply broke even on its free cash flow line.

W Q4 2023

What’s more, despite reporting $306 million of adjusted EBITDA in fiscal 2023, we have to keep in mind that more than $600 million of this EBITDA line was made up of stock-based compensation.

To put it more starkly, it’s not only that the business is barely breaking even on its free cash flow line, but that this business is not only delivering ephemeral revenue growth, but it’s just plainly unprofitable.

And moreover, Wayfair still has to contend with an overleveraged balance sheet that carries $1.8 billion of net debt. This business carries too many hairs on it.

The Bottom Line

In conclusion, I firmly believe that Wayfair’s stock is poised for a selloff, as the company faces significant challenges in the near term.

With stagnant revenue growth and minimal free cash flow generation, compounded by a heavily leveraged balance sheet carrying approximately $1.8 billion in net debt, the outlook for the stock appears bleak.

Despite recent stability in financial performance, Wayfair’s status as a growth company is called into question, particularly as it contends with intense competition in the e-commerce furniture market.

Additionally, uncertainties surrounding supply chain disruptions, inflationary pressures, and macroeconomic volatility further exacerbate Wayfair’s challenges. As investors reassess the stock’s true value, I anticipate a downward trajectory for Wayfair’s shares in the coming months, with $62 per share serving as a high price to aspire towards.

Q2 2024 Earnings Call Transcript")