Hispanolistic

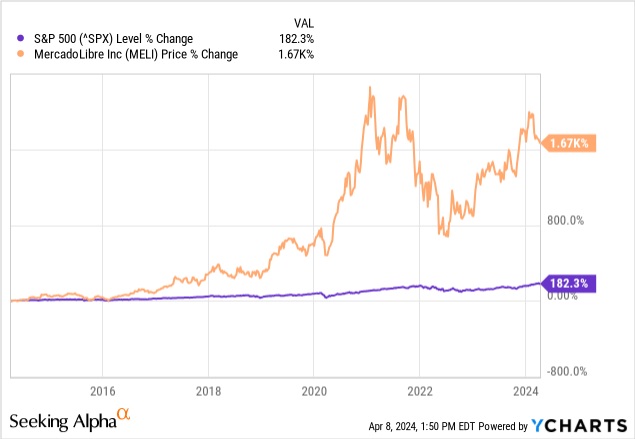

MercadoLibre (NASDAQ: MELI) is a Latin American company that is one of the world’s largest e-commerce and fintech companies. The best part is that it still has additional revenue growth opportunities beyond e-commerce and fintech with its growing digital advertising business in the region. Management’s excellent governance of its growth and profitability opportunities has made the stock one of the better market performers over the previous ten years, substantially beating the S&P 500 returns.

The company reported fourth-quarter 2023 earnings on February 22, 2024. Although top-line growth was satisfactory, as the company beat analysts’ consensus revenue estimates by $130 million, investors were worried about several items, including shrinking margins and missing analysts’ GAAP earnings-per-share (“EPS”) estimates by $3.71. The stock dropped 10% the day after the earnings report and is still down around 18% from its February 22 closing price as of April 8, 2024. Although the market may still overvalue the stock based on many valuation ratios, its intrinsic value may warrant growth investors putting it on their list of potential stocks to buy. If you are an investor with a long-term mindset willing to withstand short-term volatility, the stock’s pullback may be an ideal time to invest.

This article will discuss investor concerns with the recent earnings report, examine its competitive advantages and why the company is still on track for long-term growth, and delve into its digital advertising business, which is a new potential growth driver. We’ll also examine its current valuation and why the recent stock decline might not adequately reflect MercadoLibre’s long-term value. I rate the stock a strong buy.

One of the primary investor concerns

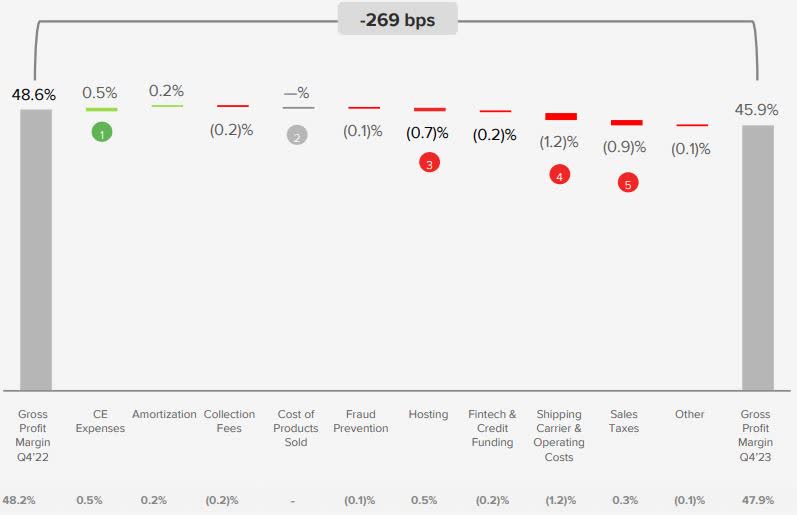

One of the most prominent issues investors became concerned about in the fourth quarter earnings report is margin compression. MercadoLibre’s fourth quarter 2023 gross margin was 45.9%, down 269 basis points (“bps”) from the previous year’s comparable quarter, which was 48.6%. Two major reasons for the fall in gross margins were higher e-commerce shipping expenses and one-time costs from management losing two lawsuits.

MercadoLibre Commerce Executive Vice President Ariel Szarfsztejn highlighted four reasons for shipping expenses rising higher in the fourth quarter on the company’s fourth quarter 2023 earnings call:

- The company relaunched a loyalty program named Meli+ in Brazil and Mexico, which introduced a new free shipping program named MELI Delivery Day (MDD). The company’s fourth quarter 2023 shareholder letter described MDD as “a shipping option that enables subscribers of the program to schedule a day of the week on which they can access free shipping on items from approximately $6 (vs. the standard free shipping threshold of approximately $15)“. The free shipping benefit for customers translates to higher shipping costs for MercadoLibre’s logistics operations. The fourth quarter was Meli+’s first full quarter of operation.

- The rapid expansion of MercadoLibre’s first-party (“1P”) sales on its e-commerce website increases shipping expenses. On the fourth quarter earnings call, Ariel Szarfsztejn explained the increased 1P shipping costs: “The growth of 1P in our business, whose GMV [Gross Merchandise Value] was 50% higher quarter-over-quarter in dollars, also acts as a headwind basically because there are no sellers paying for shipping revenues given that we are the sellers in the case of 1P.“

- Management decided to remain competitive in Argentina by not passing on the high inflation costs to buyers.

- The fourth quarter, the Christmas season, has the highest e-commerce sales, requiring the company to temporarily increase spending on more workers and additional shipping capacity to meet the increased demand.

Although investors never like seeing costs go up, the above additional expenses should benefit MercadoLibre’s e-commerce operation in the long term. The following chart from the company’s fourth quarter 2023 investor presentation shows the difference between MercadoLibre’s gross margin in the fourth quarter of 2023 and the fourth quarter of the previous year. The following image comes from the company’s fourth quarter 2023 earnings presentation.

MercadoLibre Fourth Quarter 2023 Investor Presentation.

Let’s discuss the two court cases that lowered gross margins. The first court case was the company’s battle with Brazilian Federal tax authorities about whether the government can tax payments MercadoLibre sends from its Brazilian subsidiaries to its Argentine subsidiaries for IT support. The company argues that the Brazilian government is double taxing the business. The Brazilian government disagrees. Management seems to believe they are about to lose the tax case and has booked a $58 million provision in the gross margins for the expected court loss, which is point three on the chart above, under hosting. MercadoLibre’s operating margin also shrank 600 basis points (“bps”) from 11.6% to 5.6%, primarily due to the company provisioning $261 million in product development expenses for this same expected court loss to Brazilian Federal tax authorities.

The second issue that wound up in court is point five in the image above. MercadoLibre lost this second court case in Brazil’s highest court over sales taxes. After paying the disputed taxes from April to December 2022, the company now pays that sales tax as an ongoing expense. As a result of the court loss, it charged a $31 million expense on the cost of revenue line.

The combination of all the above costs harmed the bottom line in the short term. The company produced a fourth-quarter GAAP earnings-per-share of $3.25 when analysts expected almost twice that number. News outlets blared headlines like “Earnings Miss” and “Profit Shortfall,” with market sentiment turning negative toward MercadoLibre. However, a decent chunk of the margin compression was mainly a one-off event from the court cases in the fourth quarter, and the higher e-commerce expenses should pay off in increased market share and revenue in the longer term.

Other risks and things to watch

Investors are concerned with more than just the e-commerce portion of the company. Since the fintech portion, MercadoPago made up approximately 43% of the revenue in 2023; investors are rightly concerned about anything that could negatively impact MercadoPago. MercadoLibre launched MercadoPago in 2004 as a payments network and later added different functionality, like lending money to consumers and businesses, by establishing MercadoCredito in 2016.

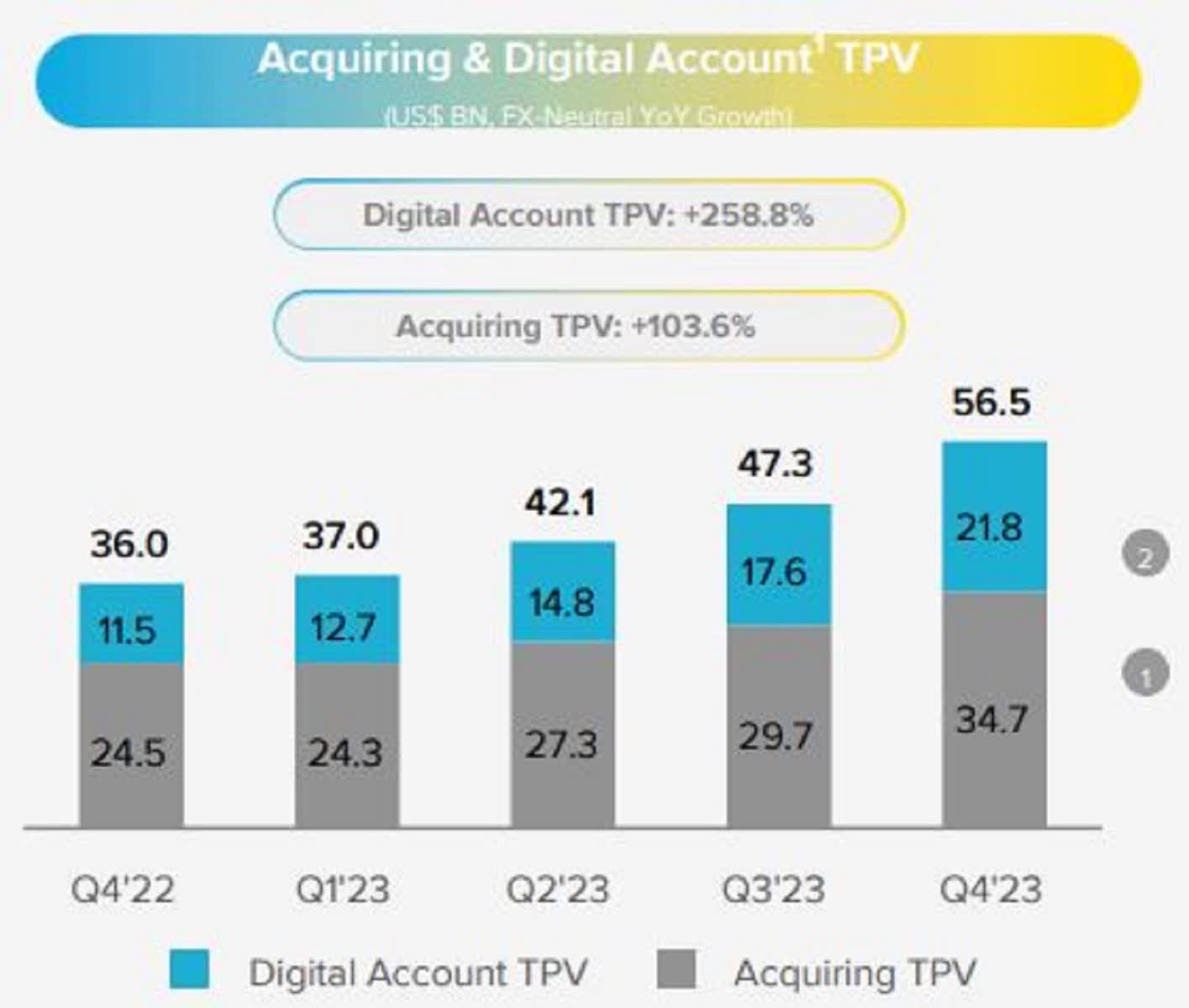

One of the most important things to consider with MercadoPago is its Total Payment Volume (“TPV”), which measures the total value of payments processed through a payment platform. MercadoPago reports two separate categories of TPV. The first is Acquiring TPV, which is the total monetary value of all payment transactions paid for using the MercadoPago platform. The second is Digital Accounts TPV, which involves credit products, debit cards, savings, investments, and insurance product transactions. The following image shows that its Acquiring and Digital Account TPV produced healthy growth in the fourth quarter.

MercadoLibre Fourth Quarter 2023 Shareholder Letter

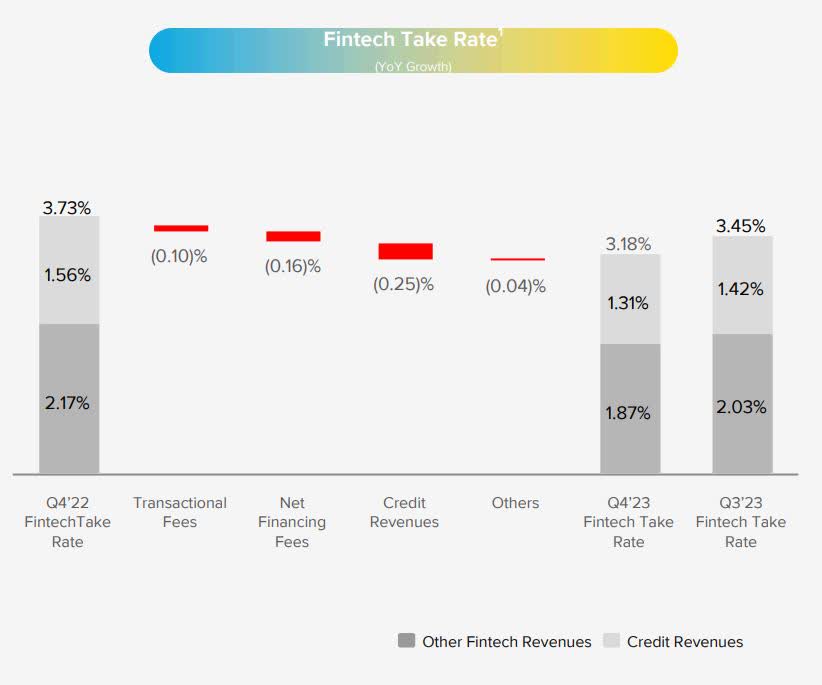

The other important metric to follow in its fintech segment is the take rate, which the company defines in the following image as “Fintech Revenues as a % of Total TPV,” or in other words, the money MercadoPago generates from the monetary value of transactions taking place on its platform. The company’s take rate trends can tell an investor a lot about competition within the fintech market. A rising take rate indicates increased profitability of the platform. A downward take rate could indicate increased competition, a mix shift to lower fee transactions, or increasing promotions to generate more TPV.

MercadoLibre Fourth Quarter 2023 Investor Presentation.

The above image shows that MercadoPago’s fourth quarter 2023 total fintech take rate declined 55 bps year-over-year and 27 bps sequentially to 3.18%. MercadoLibre should report its first quarter 2024 earnings on May 2, 2024. Investors should observe whether the take rate trends continue to lower or stabilize. If the take rate trends lower, you should try identifying the reason. The light gray area on the chart also represents the credit take rate, which shows a 25-bps year-over-year decline and an 11-bps sequential decline to 1.31%. A declining take rate in the credit portion of the business could indicate that the loan environment is becoming increasingly competitive, or that MercadoCredito might be making riskier loans.

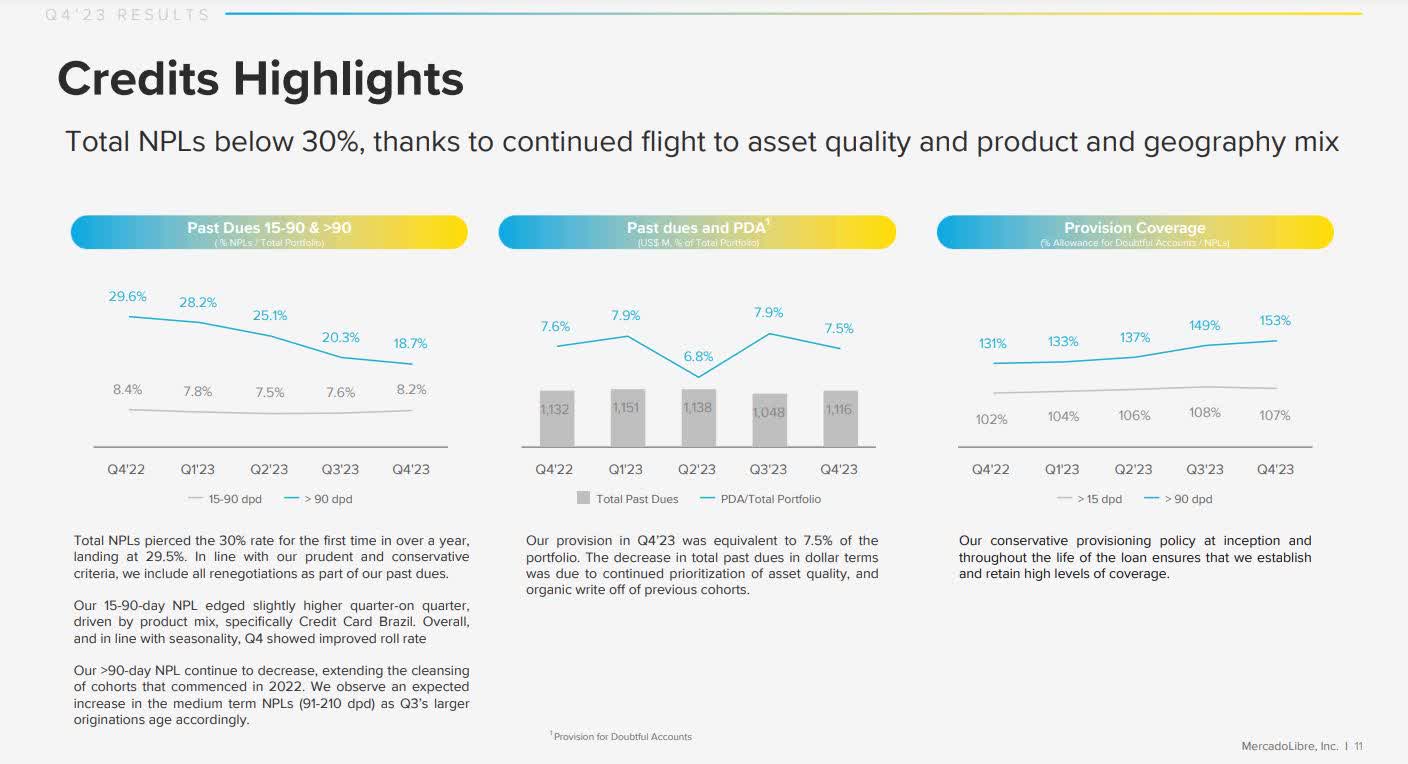

Let’s look more closely at the company’s credit portfolio. The chart below shows MercadoCredito’s non-performing loan ratio in the left-hand column. A >90 NPL is a loan that is 90 days past due, which the banking industry views as a non-performing or bad loan. A 15-90 NPL is a loan between 15 days and 90 days past due, which the banking industry views as a leading indicator of a loan becoming non-performing. The image below shows that >90 loans have dropped from 29.6% to 18.3% year-over-year, a sign that fewer loans have turned sour in the fourth quarter of 2023 than in the previous year’s comparable quarter — a good thing. A potential concern is that the 15-90 NPL jumped from 7.6% in the third quarter to 8.2% in the fourth quarter, signaling that more loans will likely become non-performing in the future, especially if this metric trends up.

MercadoLibre Fourth Quarter 2023 Investor Presentation.

At least one Wall Street analyst has his eye on more loans potentially turning bad. In response to a question by UBS analyst Kaio Prato about what made the company comfortable in raising credit card loan originations in an environment where non-performing loans (“NPLs”) have risen, MercadoLibre’s Commerce Executive Vice President Ariel Szarfsztejn said the following on the earnings call:

With regards to what makes us more comfortable, we first launched credit cards in Brazil three years ago, and we have been iterating the models we use to score grades. We have done many iterations, several every year. And each iteration we do, we get better results. We saw the credit situation overall in Brazil worsened a year and a half ago, two years ago. So, we were more cautious. And now, throughout last year, we started feeling more and more comfortable, and we have been increasing the amount of origination in Brazil. And also, we launched a credit card in Mexico, and we’ve been, I would say, aggressive in rolling it up. When we look at, as we say in the shareholder letters, when we look at total payment volume for our credit card, year-over-year, it has grown well above 100%. So, we have been aggressive with regards to that.

Source: MercadoLibre Fourth Quarter 2023 Earnings Call.

Right now, there is no reason to be alarmed. Still, the market might become concerned if the 15-90 NPL continues increasing in the coming quarters and > 90 NPL sharply rises. The other two charts in the image convey that the company has positioned itself conservatively, and management has likely adequately prepared for more loans turning sour. The company sets aside a certain percentage of its portfolio to cover bad loans, which is called the loan loss provision in accounting. Its fourth quarter 2023 loan loss provision was 7.5% of the loan portfolio.

Seeking Alpha analyst Heavy Moat Investments has identified “bad credit risk” as a significant threat to cash flow in this linked article in October of 2023. Raising the loan loss provisions can reduce net income and free cash flow (“FCF”), which is a vital consideration for investors using bottom-line metrics like earnings-per-share (“EPS”) or FCF to value the stock. Some investors may have turned away from the stock because they expect loan loss provisions to rise and dampen EPS and FCF growth. Suppose you invest in MercadoLibre; it would be wise to watch for whether management makes loans to too many risky borrowers in an attempt to pursue credit card growth, which would eventually show up in NPL rising and potentially a substantial rise in loan loss provisions.

MercadoLibre has many moving parts and bells and whistles. I have only included a small portion of the risks of investing in this company. If you decide to invest, you should thoroughly investigate more of the company’s risks, which it lists in its 10-K.

It has solid competitive advantages

Despite the company’s risks, it has several competitive advantages that should help it maintain growth for years to come. MercadoLibre is Latin America’s number one e-commerce platform and is the eighth-largest e-commerce platform in the world, right behind Walmart (WMT), according to eDesk. Marcos Galperin founded MercadoLibre in 1999. It was among the first companies to build an e-commerce marketplace in the Latin American market, giving it a similar first-mover advantage that Amazon (AMZN) commands in the U.S. markets. As time passed, the company added everything online merchants needed to run an online business effectively. The company’s platform consists of six interwoven services:

- An e-commerce marketplace.

- A payment and credit solution.

- A logistics service.

- Advertising.

- Online classifieds.

- A way to build online storefronts.

Although e-commerce has a low barrier to entry, very few of its competitors have all the services MercadoLibre offers to merchants. By providing an array of services that save merchants time and money setting up an online store, the company attracts more and more merchants to its platform. As consumers see more products on the platform from an increasing number of merchants, the company increases its number of buyers on the platform. The growing number of buyers attracts more merchants to the platform, and the cycle begins again — a network effect competitive advantage.

With each new customer, the company gains a data advantage over new market entrants, allowing MercadoLibre to personalize the consumer shopping experience by recommending relevant products. Additionally, more data enables it to improve its e-commerce and fintech products or create additional services for consumers or merchants, making it harder for competitors to catch up. For instance, MercadoLibre is in the process of building a significant advertising platform in Latin America.

The company has a substantial potential upside in advertising

Although some people are just now paying attention to it, the company started its digital ad business, MercadoAds, in 2009. There are two reasons that the ads business is beginning to catch the market’s eye. First, MercadoAds is becoming a digital advertising force in Latin America. Statista said it generated approximately “48.5% of Latin America’s digital retail media advertising revenue” in 2023, up from 38% in 2022. So, its ad business is rapidly increasing and taking market share.

Second, MercadoAds reached a milestone and finally exceeded 1% of annual Gross Merchandise Value (“GMV”) in 2021. It later reached annual GMV of 1.3% and 1.6% in 2022 and 2023, respectively. It’s a rapidly growing, high-margin business. The company’s fourth quarter 2023 Shareholder Letter stated that the ad business’ growth “remained above 70% on an FX-neutral basis for the seventh successive quarter in the fourth quarter of 2023.” Several years ago, in the company’s fourth quarter 2021 earnings call, old Chief Financial Officer Pedro Arnt estimated MercadoAds’ gross margins to be around 70%.

MercadoLibre started getting really serious about its ad business in 2022. The company doubled the number of engineers assigned to the advertising business that year to revamp its ad technology stack from brand awareness solutions in display and video ads to adding performance advertising product ads focused on converting ad views into sales. One of its first improvements in 2022 was deploying a proprietary ad server, a software platform that automatically manages, targets, and inserts ads in display advertising. Later, the company announced in a video released after its first quarter 2023 earnings call that it had launched a new programmatic ad platform. Global brands and agencies now have an automated display buying platform that leverages MercadoLibre’s first-party data, enhancing the platform’s ability to target users. The new platform offers advertisers accurate real-time bidding models, live reports, and analysis. Management recently wrote:

We welcomed almost 50,000 new advertisers to our Ads platform in 2023, which we believe is an indication of its importance to sellers, and the strength of our product. This is particularly the case amongst the small and medium-sized sellers that make up a majority of our marketplace, and use our advertising platform on a self-service basis. We are also excited to have launched technology that facilitates advertising on our platform for big brands and the agencies that work on their behalf, and we look forward to its continued maturation in 2024 and beyond.

Source: MercadoLibre Fourth Quarter 2023 Shareholder letter

Lastly, MercadoLibre took a page out of Amazon’s book and established Meli+, which I mentioned earlier in this article. Similar to Amazon Prime, Meli+ offers its users access to a free streaming platform. Management named its streaming platform MELI Play. The company monetizes MELI Play through advertising, providing a potential new video ad revenue stream.

Valuation

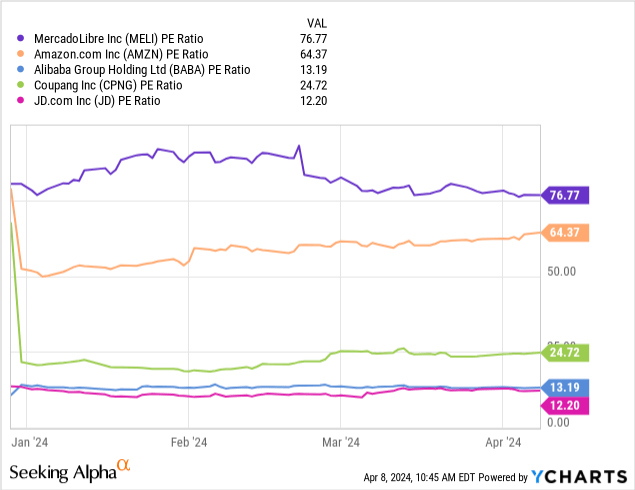

Using most ratio-based valuation metrics, the company looks overvalued. Seeking Alpha’s Quant rates the value as D-. MercadoLibre has a price-to-earnings (P/E) ratio of around 77, well above its sector median P/E ratio of 17.48. Its P/E is also the highest among several large regional e-commerce platforms.

Usually, when a forward P/E exceeds analysts’ growth estimates, the market may overvalue that stock. In contrast, the market may undervalue a stock when a forward P/E is below analysts’ growth estimates. Using that standard, MercadoLibre’s forward P/E of 45.77 may indicate overvaluation. However, its one-year forward P/E 33.57 may indicate undervaluation. If MercadoLibre traded at a one-year forward P/E that is in line with its one-year forward growth rate of 36.33%, the stock price would be $1625.04, around 9% above its April 9, 2024 closing price.

| Fiscal Period Ending | Analyst’s Year-over-Year Growth Estimates | Forward P/E | # of Analysts |

| December 2024 | 43.66% | 45.77 | 13 |

| December 2025 | 36.33% | 33.57 | 14 |

Data Source: Seeking Alpha

The following reverse discounted cash flow (“DCF”) model shows the implied FCF growth rates over the next ten years for MercadoLibre’s closing price of $1,495.01 on April 9, 2024.

Reverse DCF

|

The fourth quarter of 2023 reported Free Cash Flow TTM (Trailing 12 months in millions) |

$4,631 |

| Terminal growth rate | 3% |

| Discount Rate | 10% |

| Years 1 – 10 growth rate | 4.4% |

| Stock Price (April 9, 2024, closing price) | $1,495.01 |

| Terminal FCF value | $7.377 billion |

| Discounted Terminal Value | $40.410 billion |

| FCF margin | 32% |

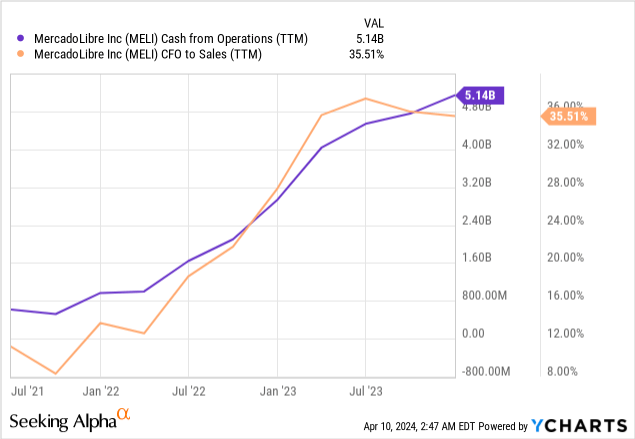

According to the assumptions I made in the above reverse DCF, the company only needs to grow its FCF by 4.4% over the next ten years to justify today’s stock price, which I think it can easily achieve. Based on analysts’ estimates, revenue should grow 30.75% annually to $72.32 billion over the next ten years. The company has also grown very efficient in converting sales into cash over the last three years, with cash from operations exploding higher, as the chart below shows.

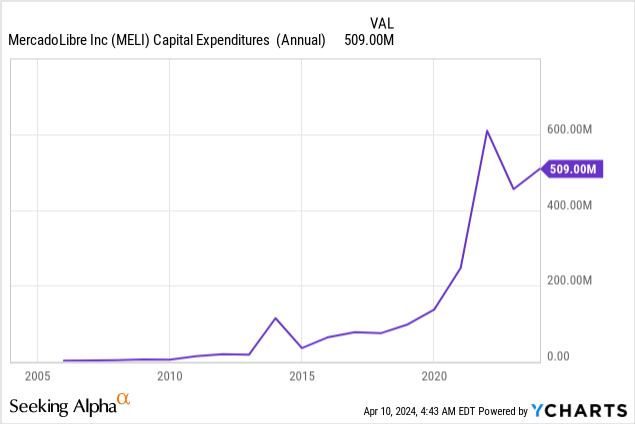

One factor that could reduce FCF is capital expenditures (“CapEx”). The company has recently started investing heavily in its logistics network and Information Technology (“IT”) for its e-commerce and fintech platform. In 2023, MercadoLibre spent $225 million on IT assets and $233 million on the shipping and warehouse network, which is approximately 90% of the $509 million spent in CapEx last year.

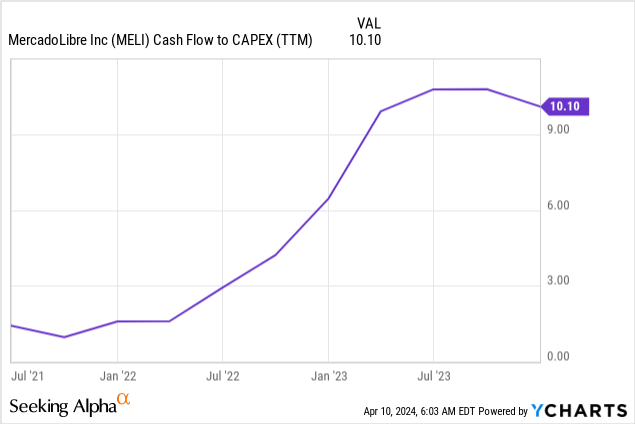

The good news is that MercadoLibre is growing its operating cash flow substantially faster than CapEx, as shown in the chart below.

Suppose the company can maintain high efficiency in converting sales into cash flow and maintain a revenue growth rate of between 20% and 30% over the next ten years. In that case, MercadoLibre should be able to easily grow its FCF above 4.4% over the next ten years, especially if management prevents the loan loss provisions from exploding higher by making good lending decisions. Suppose management can conservatively reach a FCF growth rate of 6%; the stock’s intrinsic stock price is $1677.92, up 12.23% from the April 8 closing price of $1495.01. If you believe the FCF growth rate can reach 8% over the next ten years, the intrinsic stock price is $1949.91, up 30.42% from the April 8 closing price.

MercadoLibre is an excellent buy at current prices

It is rare that MercadoLibre’s stock pulls back enough to provide investors with a good entry point. Now is one of those times. In the past, when investors bought this company on a pullback, the stock’s eventual rise rewarded the buy decision. If you are looking for a solid growth investment over the next five to ten years, look at MercadoLibre and consider buying a few shares. I rate the stock a Strong Buy.

Q2 2024 Earnings Call Transcript")