Hiroshi Watanabe

More than half a year ago, I wrote an article on the Amplify CWP Enhanced Dividend Income ETF (NYSEARCA:DIVO), outlining a rather bullish thesis on how the combination of relatively relaxed covered call strategy (i.e., distant option strikes from the prevailing market price) and exposure to large-cap names provides an opportunity for investors to capture enticing yields without sacrificing too much on the upside potential.

At the same time, I also underscored the potential opportunity risk that stems from the embedded covered call strategy; here is a short excerpt from the article:

DIVO, however, should not be viewed as an investment which could deliver alpha in the scenario of upwards trending markets. It should also not be viewed as a pure play protection mechanism during declining equity markets since the current covered call strategy does not encompass a significant part of the portfolio.

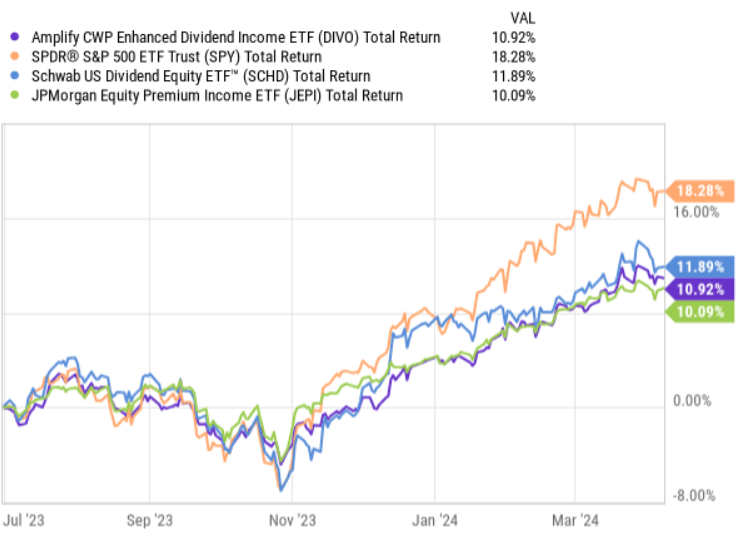

Since then, DIVO has performed very much in line with the rest of the dividend-focused vehicles (including covered call strategy ETFs) that carry a notable exposure toward the S&P 500 or U.S. large-cap names.

Ycharts

After the relatively weak performance (albeit somewhat decent returns on an absolute basis) and considering several recent broader market dynamics, in my view, there is a stronger basis now to go long DIVO.

Here are the two main reasons why I think that investors should pay more careful attention to DIVO and consider going long here.

Thesis update

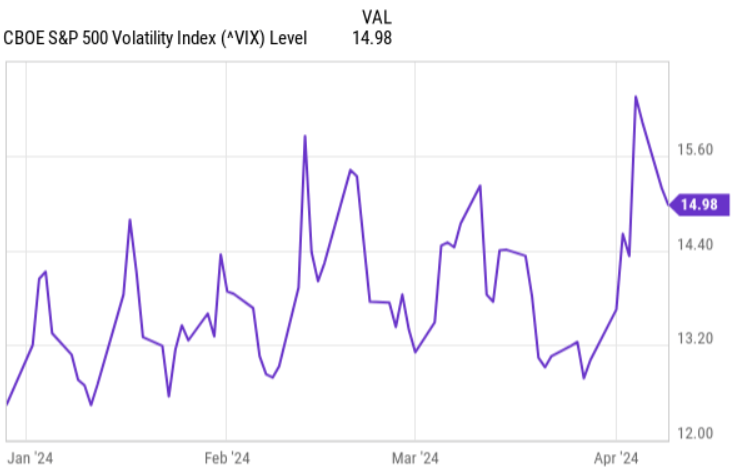

First, the VIX has risen to more favorable levels for covered call funds to extract juicer yields from the sold options positions. On a YTD basis, the VIX has advanced by 20% and, more importantly, from the chart below it seems that “higher level territory” is quite sticky, thus offering a more sustained base for option richness.

Ycharts

There are many reasons behind the increased volatility here, but the major driver is obviously the uncertainty around the interest rate path. Based on the recent commentary by the Fed and seeing how the market slowly but surely prices in delayed interest rate cuts, it is clear that we will most likely be facing prolonged conditions of interest rate uncertainty.

Such an environment provides strong support for the overall market volatility, which in DIVO’s case comes in handy as it per definition increases the option prices across the board. This means that the pocketed premiums from the call writing strategy (and thus limitation of the underlying stock price appreciation) bring in more sizeable cash flows that DIVO can further distribute to its unit holders.

Second, the fact that the probability of experiencing a notable drop in the interest rates this year has been dropping for quite some time sends a strong message for yield-seeking investors to revisit their underlying holdings that currently produce abnormal yields.

Namely, whenever equity products offer yields that are really above the norm, it is often that the companies trade at relatively steep discounts and carry unhealthy loads of debt on their balance sheets. When we entered 2024, the consensus was that these companies would do just fine as the Fed would manage to cut the rates in a notable fashion so that when debt rollovers take place, the increase in cost of financing would not be that dramatic.

Now with higher for longer assuming momentum (even with 25 – 75 basis points of cuts), aggressive equities and high yielding products have become subject to an elevated financial risk. Given this, it pays off to focus on current income that is underpinned by inherently more defensive constituents or strategies.

In DIVO’s case, we have three supportive dynamics in place:

- DIVO isolates ~25 large-cap companies, which have gone through a discretionary screen by the fund, where a focus is put on high quality, stable dividends (i.e., ample dividend coverage) and earnings durability.

- The presence of a covered call strategy allows the Management (or rather ETF) to not go far up in the risk curve to offer attractive yields as the pocketed premiums complement nicely the dividends paid by the underlying companies.

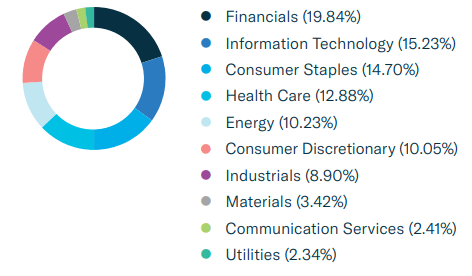

- The sector diversification, which is not that biased towards sectors that are overly CapEx intensive and requiring huge loads of debt (reflected below) with the tilt towards defensive companies, introduces an additional layer of safety.

Amplify ETFs

The bottom line

In my opinion, the attractiveness of DIVO has increased meaningfully since I published my article on it back in July, last year. The key driver here is the sustained uncertainty around the direction of interest rates that has triggered higher volatility (i.e., VIX) levels and an increased probability of distress among debt-heavy corporates and/or high yield, that are often the key elements supporting abnormal yields. For DIVO, however, such conditions are supportive in the context of yield generation and its relative attractiveness to other income-producing alternatives. Higher VIX renders options more expensive, which allows DIVO to pocket more from the covered call strategy. Also, from the fundamental perspective, DIVO holds truly defensive names (e.g., large-cap, already cash and dividend-generating that are nicely distributed across different, and not overly debt-focused, sectors), which should protect the underlying positions from rising volatility and more expensive debt for longer.

For all of the above reasons and DIVO’s current (attractive) yield of 4.5%, this ETF is a buy for me now.

Q2 2024 Earnings Call Transcript")