Tak Yeung

Investment Thesis

I believe that T-Mobile US Inc. (NASDAQ:TMUS) is a hold at the current stock price. The continued growth in across the top and bottom line, coupled with optimistic future forecasts, suggests to me that T-Mobile is well-set for continued success. Its strategic investments in 5G technology have not only made it an industry leader but also helped with customer acquisition and loyalty. These advancements provide T-Mobile with a solid foundation for a strong 2024 and I expect that to continue into the future too. With that in mind, a discounted cash flow (DCF) analysis indicates a hold based on the anticipated return which is I do not believe is high enough to offset the added risk of investing in TMUS instead of the S&P 500.

Introduction

Being that I’m an investor aiming to pick stocks that will outperform the market, my approach is to choose understandable companies which have a clear and sustainable advantage over its competitors. This is because, I believe this will allow management to better reinvest back into the business, compounding the returns to shareholders over time which should ultimately grow my portfolio.

Personally, I’m drawn to the stability and growth potential, dividend investing offers. It aligns with my investment style by providing a source of passive income whilst still compounding returns and lowering overall risk.

A company that has come on the radar for many dividend investors like myself in the past few months is T-Mobile. As part of their Capital Return Program, the company announced on September 6, 2023, that the Board authorized a shareholder return program of up to $19.0 billion through December 31, 2024, which, for the first time in its history, included the payment of a quarterly dividend. This announcement got me wondering if T-Mobile would make a good dividend opportunity and whether dividend investors should consider it as an investment.

Company Profile

T-Mobile is a wireless network operator in the United States, based in Bellevue, Washington. Known previously as VoiceStream Wireless PCS the company dates back to 1994 and became T-Mobile USA in 2001 following acquisition by Deutsche Telekom AG. T-Mobile is currently the third-largest wireless carrier in the US, with 119.7 million customers as of the end of 2023. The company’s services include mobile telecommunications and wireless broadband under both the T-Mobile and Metro by T-Mobile brands. More recently, the company merged with Sprint Corporation which has significantly expanded T-Mobile’s subscriber base and service capabilities as well as increased its revenue streams.

Thanks, its strong financial performance over the past decade, the company has seen its stock price rise considerably. In the last 10 years, T-Mobile shareholders have seen a (CAGR) of 18.7% in the stock price which has been a massive overperformance compared to the broader markets and has resulted in many investors flocking to stock in the hopes of achieving similar returns in the future, something I could see myself doing if the opportunity is right.

Dividend Discussion

Dividends are a key indicator of a company’s financial health in my opinion, and as someone keen on securing financial freedom through sustainable dividend investing, I pay close attention to them. Typically, when assessing a company’s dividend, I look at the company’s dividend paying track record, this gives me an understanding as to whether the company is likely to maintain or raise a dividend through all economic conditions, however, of course in the case T-Mobile this isn’t possible. That being said, I believe T-Mobile’s recent move to start paying a dividend shows that the management is confident in the financial position of the business and have identified a dividend as one of the best ways to return value to shareholders.

Currently, T-Mobile’s dividend is $1.30, yielding about 0.81% at a share price of $160.90 which is below the S&P 500 average of 1.35% and has a payout ratio of approximately 9%, which in my opinion is very sustainable. When compared to competitors like AT&T (T) and Verizon (VZ), T-Mobile’s dividend yield is considerably lower, with T and VZ offering 6.4% and 6.3% dividend yields respectively. Although, it’s important to note two things when comparing T-Mobile’s dividend with its competitors. Firstly, the payout ratio of AT&T and Verizon are far higher and not as sustainable and secondly, the trailing twelve month (TTM) dividend numbers only account for two quarterly dividends from TMUS, and thus if we were to include the next two quarterly dividends which are expected to remain at $0.65 per quarter, the yield and payout ratio double, although these metrics still considerably lower than T-Mobile’s competitors.

Financial Discussion

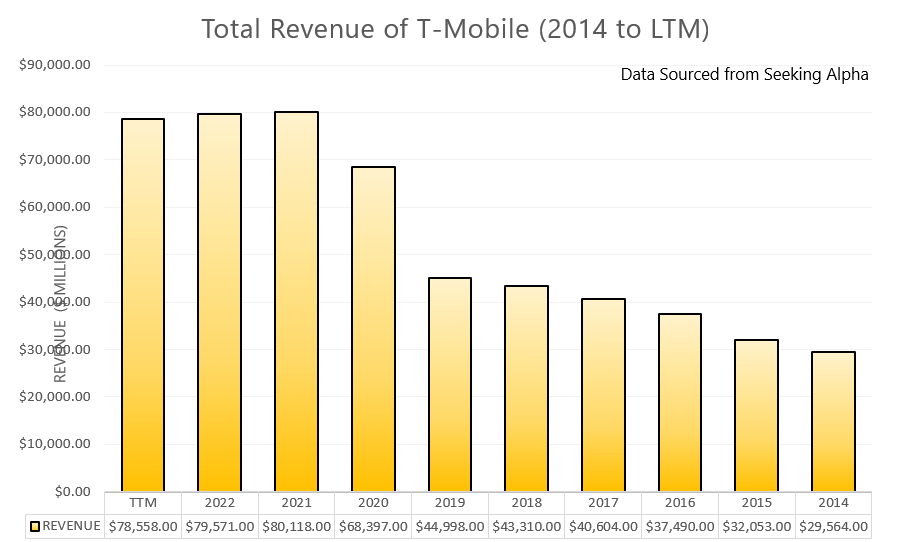

T-Mobile has significantly outperformed its primary rivals over the last decade, marked by a strong top line growth. Revenue during this period grew from $29.16 billion in 2014 to $77.38 billion in the (TTM), which is approximately 11.5% (CAGR). This great revenue growth has made its way through to key profitability indicators, specifically the Earnings Per Share (EPS). (EPS) has seen even more impressive growth than revenue, in 2014 EPS was $0.30 compared to the (TTM) where it is $6.93 which translates to a very strong (CAGR) of roughly 41.8%. It’s worth noting that in terms of (EPS), 2023 was a particularly good year for T-Mobile thanks in part to well managed expenses and a reduction in costs associated with merger and restructuring and I don’t expect this kind of growth rate to be maintained in the long-term.

T-Mobile’s revenue summarized (Division One Dividend)

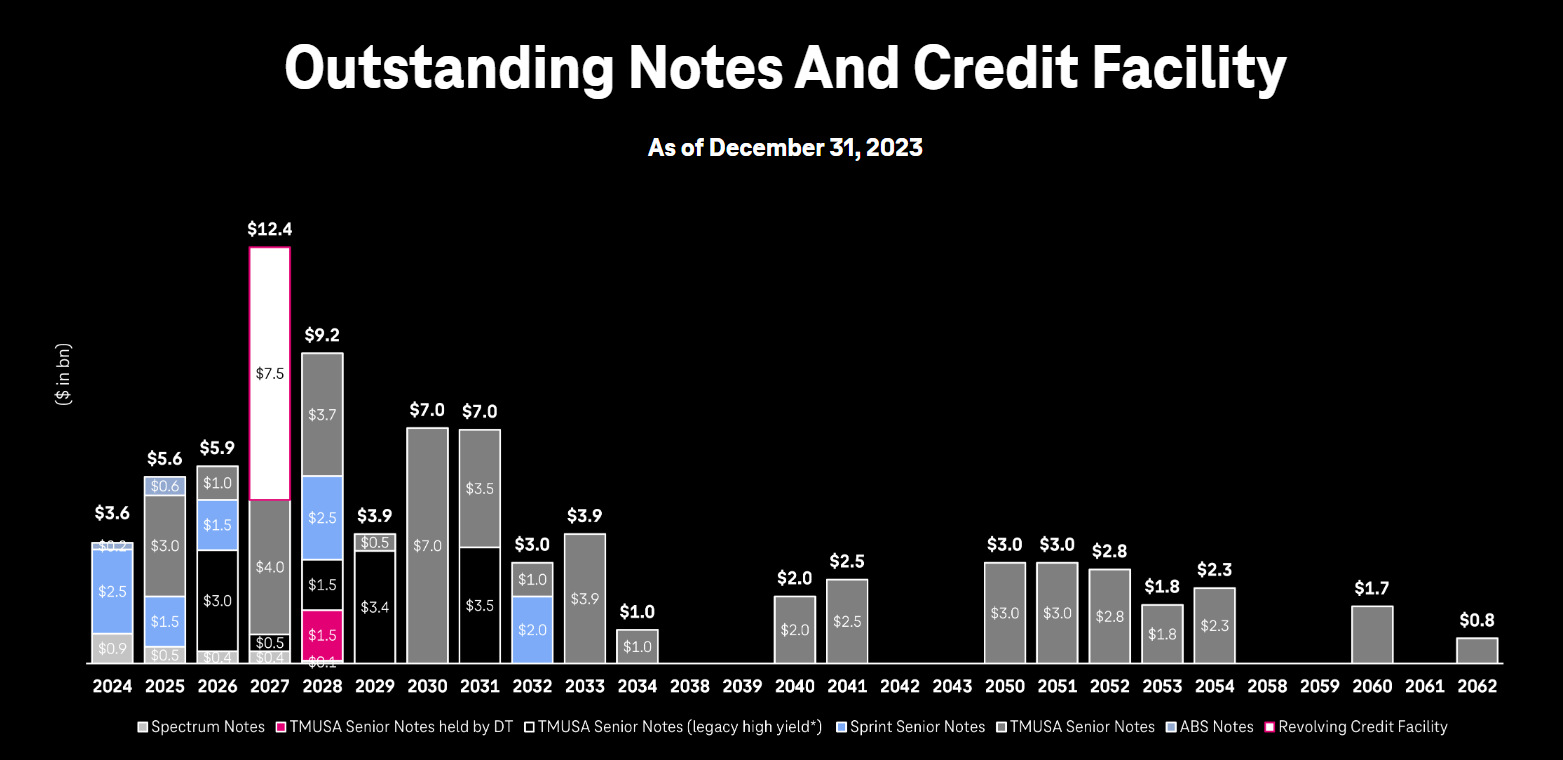

Owing to the nature of the telecommunications industry, businesses like T-Mobile often finds themselves with a tremendous amount of debt, which for many investors is a concern as it could impact the return they receive. Looking specifically at TMUS, the company has a net debt position of $108.51 billion. This is a considerable amount of debt, beyond what I would typically consider healthy, although T-Mobile has accumulated this debt in order to acquire assets which will promote growth over the long-term. Additionally, the company’s debt has been spread across multiple decades all the way through to 2062 and has secured relatively low interest rates thanks to their favourable credit rating. Despite this, I expect repayment obligations to somewhat reduce overall shareholder returns in the long-term, hence my reduced projected growth rate compared to analysts.

T-Mobile’s debt repayment schedule (T-Mobile)

Looking to more recent financial discussion of T-Mobile, in particular the latest quarterly earnings, which were released on 25 January 2024, the company has seen 1.27% decline in revenue compared to the previous year whilst EPS more than tripled from $2.06 to $6.93 thanks in large part to the reduced expenses as I previously mentioned. On a quarterly basis, service revenue grew 3% compared to the previous year thanks to increase in Postpaid service revenues. On the other hand, Equipment revenues decreased 6% because of lower lease revenues and a lower net number of devices and accessories sold due to lower postpaid upgrades. On the dividend front, the company announced another quarterly dividend of $0.65 which will be payable on the 13 June 2024.

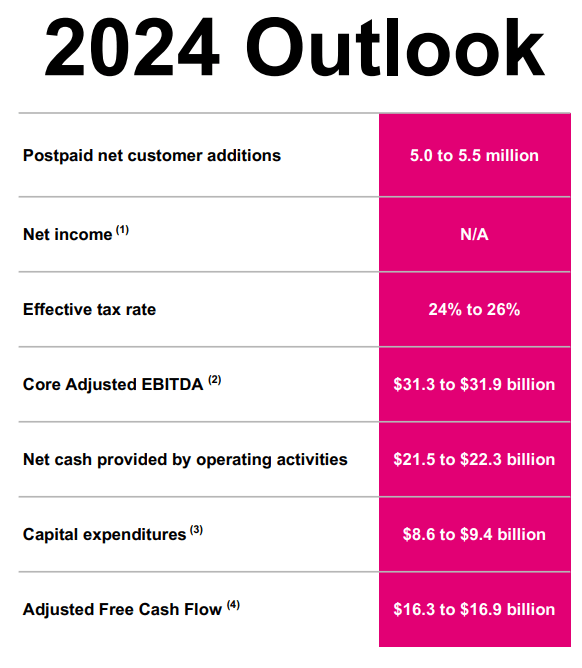

Additionally, management also provided guidance for their upcoming quarterly earnings, in which they stated that they expect to add another 5 to 5.5 million postpaid customers which will help to grow Core Adjusted EBITDA to between $31.3 and $31.9 billion and Adjusted Free Cash Flow to roughly $16.3 to $16.9 billion. Meanwhile the company also expects to continue to trend of reducing capital expenditure which I believe showcases a transition in focus away from aggressive expansion toward a focus on shareholder returns. I anticipate the company will, given their recent track record of raising guidance, meet their 2024 expectations and expect the company to raise their dividend toward the end of the year. I generally expect that T-Mobile will continue to perform strong financially and outperform its closest competitors thanks to its heavy investment in its 5G network and more favourable debt situation.

T-Mobile’s earnings guidance (T-Mobile)

Massive Investments Drive Market Leadership and Customer Growth

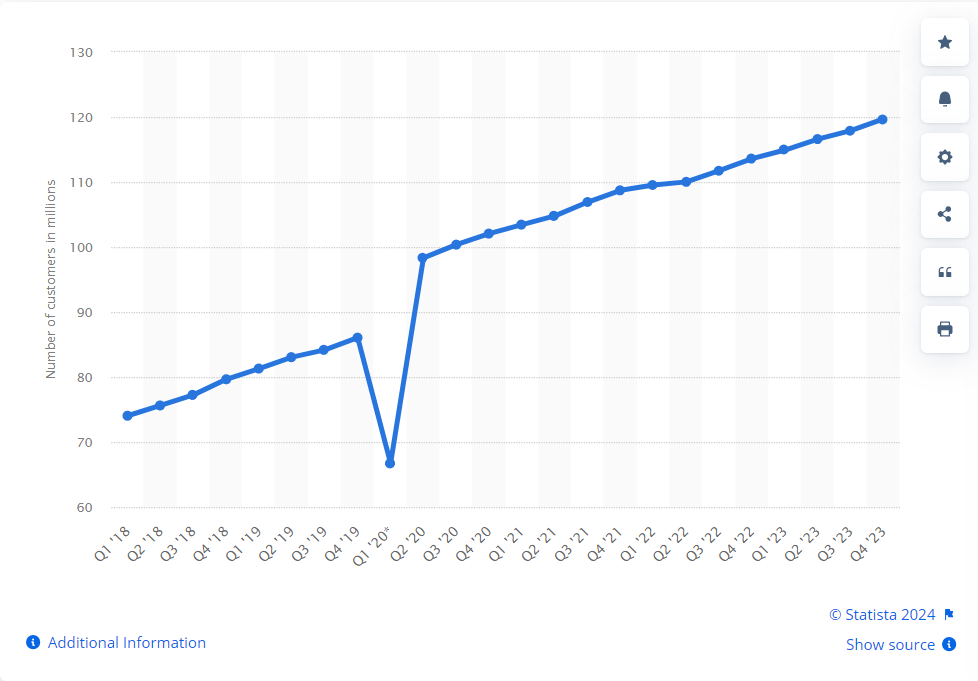

A few years back, when 5G was emerging as a promising technology in the telecommunications space, T-Mobile saw an opportunity and invested heavily into establishing infrastructure across the US. I believe that this foresight not only secured T-Mobile a favourable position to capitalize on the demand for reliable wireless internet but also helped in differentiating T-Mobile from its competitors and helped to position it as a leader in the telecom space. The expansion into broadband services, has been underscored by significant increases in both postpaid and prepaid High-Speed Internet customers, which has fuelled strong growth in their overall customer numbers.

Total number of customers/subscribers of T-Mobile in the United States from 2018 to 2023, by quarter (Statista)

Not only has the company’s heavy investment in high-speed internet increased T-Mobile’s customer numbers but it has also improved customer satisfaction and, given the increasing reliance on internet for work, education, and entertainment, increased the points of contact for consumers with T-Mobile products which provides further opportunities for the business to up-sell in my opinion. I also think this is good news for customer retention as I believe having more devices connected to the T-Mobile network makes it more of a hassle for consumers to switch.

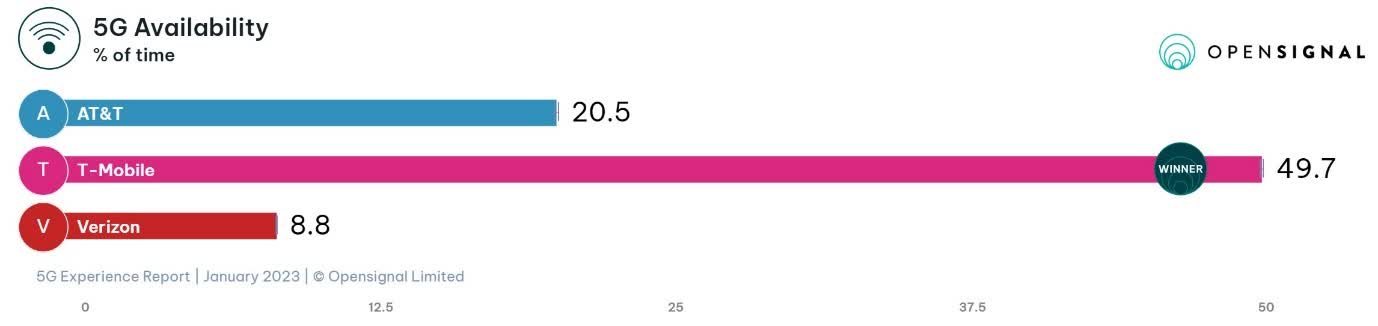

Of course, the investment into high-speed internet and its acquisition of Sprint, came at a significant cost, the company took on a lot of debt and had a capital expenditure which often exceeded cash from operations. However, in my view the investment has begun to pay itself off as according to Opensignal T-Mobile can now offer a superior internet experience in terms of speed, latency, and reliability. This combined with the fact that the company is citied as having the best 5G coverage in the US, makes me believe that the company will continue capture market share within the industry as it continues to obtain new customers at a faster rate than its competitors. The increasing market share within a growing industry leads me to believe that T-Mobile is poised for continued revenue and profit growth for the foreseeable future, however the rate at which they can grow will be dependent on T-Mobile’s ability to maintain its lead across key connectivity metrics such as availability and speed as well as the company’s ability to manage costs, something they have done well so far.

5G Availability of Major Providers (Opensignal)

Valuation

T-Mobile’s previous decade of growth has been impressive in my opinion and suggests that the business has successfully leveraged debt to become a market leader in a fast-growing industry. While T-Mobile is clearly a high-quality business with an excellent source of reoccurring revenue in my opinion, the current Seeking Alpha valuation grade of a D indicates that the business may be overvalued. This rating isn’t reflected by Wall Street which has assigned a buy rating, whilst its current (PE) ratio also indicates the stock is slightly undervalued given that its below its 5-year average.

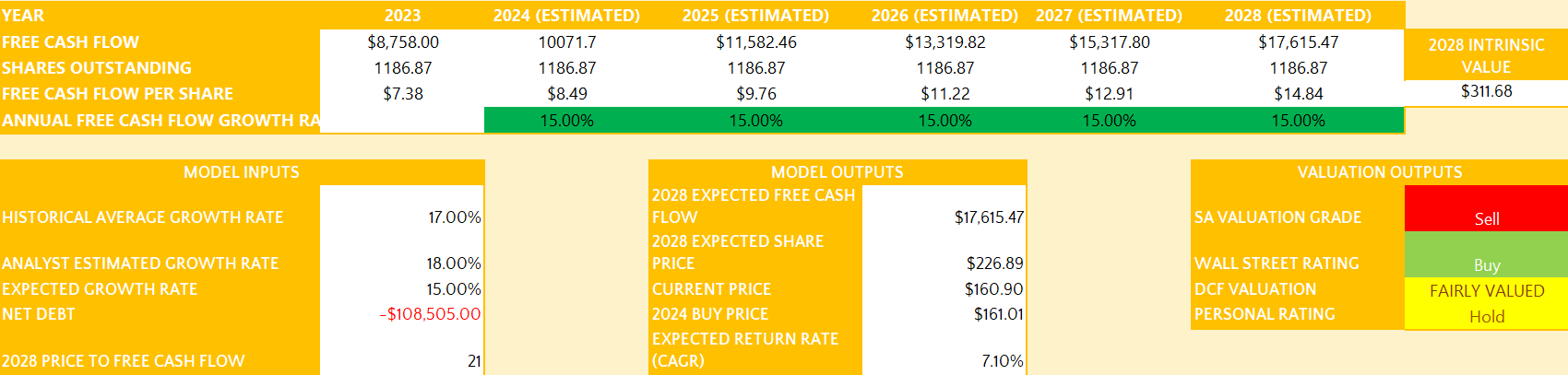

For me to determine the valuation of T-Mobile I have decided to use a (DCF) analysis. T-Mobile’s free cash flow (FCF) for 2023 was reported at $8.758 billion. If we assume a constant growth rate of 15%, which is less than both analyst and historical growth estimates, T-Mobile’s (FCF) is estimated to be $17.62 billion by 2028. I believe this growth projection, seems reasonable given T-Mobile’s large expansion into high-speed internet services, its leading position in the 5G space, and its cost management.

The estimated share price in 2028, considering a Price to (FCF) ratio of 21 would therefore be around $311.68. This suggests that a (CAGR) of 7.1% is possible for investors if buying at today’s share price. Based on the expected return from the (DCF) model and considering the outlook of the business and the potential risks, I believe that at the current price of $160.90, TMUS is a hold.

DCF Valuation (Division One Dividend)

Risks To Consider

In my opinion, while T-Mobile’s growth strategy and investments in its network infrastructure have put it in a leading position in the telecommunications sector, it has come at a massive cost, most of which has been funded by debt. The debt taken on to achieve their growth goals is what, I believe, is the biggest risk to consider when investing into TMUS and is my biggest concern for the business going forward. The company’s large debt position, resulting mostly from its merger with Sprint and other major investments, is a massive commitment for the company and there are several scenarios I see which could harm T-Mobile’s ability to pay off this debt.

Firstly, a significant reduction in subscriber growth or customer retention issues, perhaps due to service quality concerns or more attractive offerings from competitors, could negatively affect revenue. To stay ahead of competition, T-Mobile needs to continue to invest in its network and try to remain as the leader in terms of connection speed and availability. This is expensive and failing to do so will see Verizon and AT&T take customers away from T-Mobile in my opinion and will reduce overall growth of the business. Additionally, should we enter a recession or some other financial crisis, customers may look to living expenses, which may see them seek cheaper alternatives.

If this were to play out, it is likely revenue and profitability would decline or growth would slow considerably, and T-Mobile might face liquidity constraints. This could potentially lead to credit rating downgrades, higher borrowing costs, and the need to commit a larger portion of cash flow to debt servicing. Ultimately, this would restrict cash available for investment and growth and I believe this could also lead to a re-evaluation of its dividend policy, affecting shareholder returns and likely causing a decline in stock price.

Takeaway

The introduction of a dividend by T-Mobile has excited me like many other dividend investors I imagine. The company’s strong revenue and (EPS) growth, set the company up well for continued success. Its investment in network infrastructure has established it as a market leader while also helping to improve customer growth and customer retention, even when factoring in the high costs. This is what I believe gives T-Mobile a strong performance outlook for 2024 and beyond. While a (DCF) analysis leads me to apply a hold rating based on the expected return, the overall narrative of T-Mobile is one of a company capitalizing on its investments, with prospects for sustained growth.

Q2 2024 Earnings Call Transcript")