Sharkyjones/iStock Editorial via Getty Images

Note:

I have previously covered Diamond Offshore Drilling, Inc. (NYSE:DO), so investors should view this as an update to my earlier articles on the company.

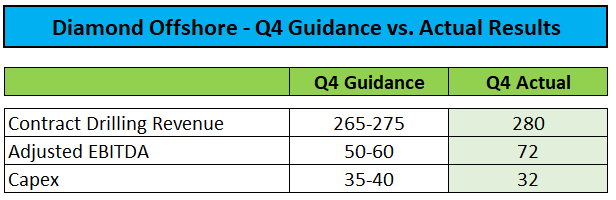

In late February, Diamond Offshore Drilling (“Diamond Offshore”) reported better-than-expected Q4/2023 results, with contract drilling revenues and Adjusted EBITDA coming in above previously communicated expectations:

Company Press Releases / Conference Call Transcripts

Please note that the company only guides for contract drilling revenues, which do not include reimbursables. Adjusted EBITDA was boosted by a $8 million GAAP accounting benefit related to the required deferral of contract preparation costs.

Company Press Releases / Regulatory Filings

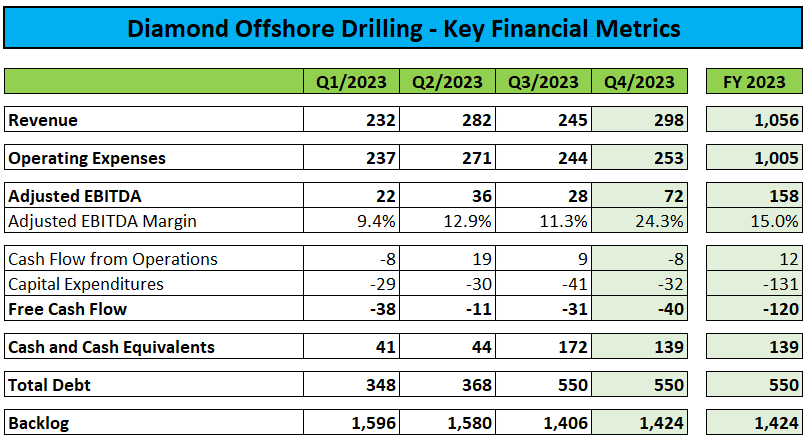

However, free cash flow continued to be negative. Diamond Offshore ended the year with $125 million in unrestricted cash and cash equivalents, as well as $550 million in debt. The company continues to have access to its undrawn $300 million revolving credit facility.

Backlog at the end of 2023 amounted to $1.42 billion (including $118 million attributable to managed rigs), up slightly on a quarter-over-quarter basis but down from $1.79 billion (including $308 million attributable to managed rigs) at the end of 2022.

Subsequent to year-end, Diamond Offshore reported two-year contract extensions with BP (BP) for the high-specification drillships Ocean BlackLion and Ocean BlackHornet at decent terms with an aggregate backlog addition of $700 million.

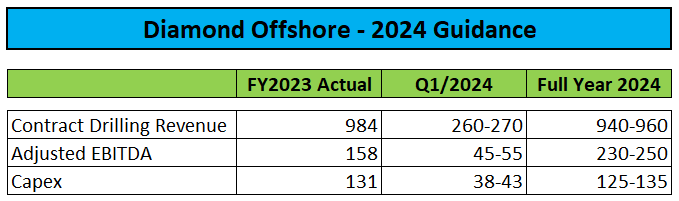

On the Q4 conference call, management provided guidance for Q1 and FY2024, which was roughly in line with muted expectations:

Company Press Releases / Regulatory Filings / Conference Call Transcripts

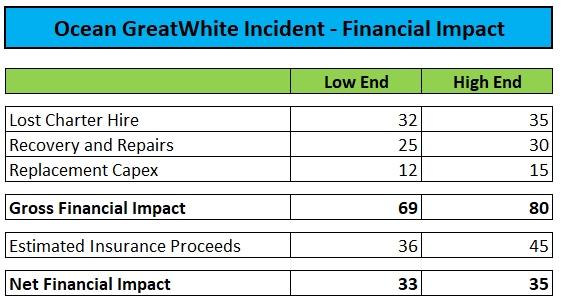

However, the outlook does not include the impact from the recent incident on the semi-submersible rig Ocean GreatWhite:

As previously reported, on February 1, 2024, the Ocean GreatWhite, a semisubmersible drilling rig owned by a subsidiary of Diamond Offshore Drilling, Inc. (the “Company”), reported that the rig’s lower marine riser package (“LMRP”) and deployed riser string unintentionally separated from the rig at the slip joint tensioner ring and the LMRP and riser dropped to the seabed while located approximately 200 km to the west of the Shetland Islands. Since the incident, the Company has been working closely with its customer and local authorities in response and has pursued efforts to recover the equipment and replace missing or damaged equipment. The Company has successfully retrieved the LMRP to the rig and removed the blowout preventor (“BOP”) from the secure well and raised the BOP to the rig. The rig has departed the location of the incident and is currently in transit to a repair facility, where the Company plans to repair the LMRP and complete related work.

Consistent with previous reports, there continues to be no reports of damage to seabed infrastructure and no known environmental impacts or lower hull damage to the rig from the incident. It remains too early for the Company to reliably predict the future financial impact of the incident. Based on the facts known to the Company to date, including the impact of weather delays on the recovery process, the Company currently estimates that recovery and repair activities will result in the Ocean GreatWhite being off rate for approximately 120 to 130 days from the date of the incident and currently estimates that the rig will return to earning rate under its current contract by late May or early June 2024.

Based on the company’s most recent estimates, total financial impact after insurance proceeds will be in a range of $33-$35 million:

Regulatory Filing

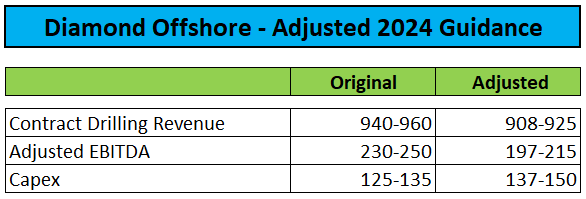

Adjusted for the estimated impact of the Ocean GreatWhite incident, Diamond Offshore’s adjusted FY2024 guidance would look like this:

Conference Call Transcript / Regulatory Filing

Taking into account the company’s interest payment obligations, 2024 might very well be another year with limited or even negative free cash flow generation.

However, I would urge investors to look beyond mediocre near-term prospects and rather focus on the earnings inflection widely expected for next year and beyond.

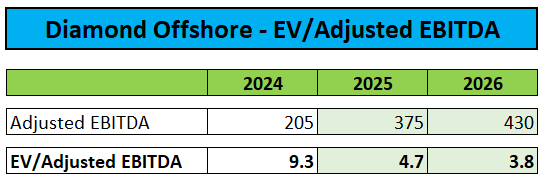

While the Ocean GreatWhite incident has caused me to lower my Adjusted EBITDA projections for this year, I have actually raised my expectations for 2025 and 2026 due to a combination of the above-discussed drillship contract extensions and further evidence of dayrates for high-specification assets holding up well despite a recent lull in deepwater contracting activity:

Author’s Estimates

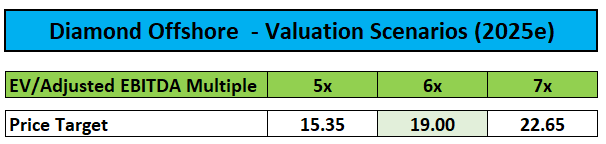

With Adjusted EBITDA expected to increase by more than 80% next year, Diamond Offshore should finally start generating substantial free cash flow, thus paving the way for returning capital to shareholders in the form of share buybacks and/or dividends.

Assigning an unchanged EV/Adjusted EBITDA multiple of 6x would result in a slightly increased $19 price target for the stock:

Author’s Estimates

Even after the most recent rally in offshore oil service stocks, the company’s shares are still providing for substantial upside relative to peers:

Author’s Estimates

Consequently, I am reiterating my “Buy” rating on the shares while increasing my price target from $18 to $19.

Bottom Line

Diamond Offshore Drilling reported better-than-expected Q4/2023 results and guided Q1 and FY2024 largely in line with muted expectations. Unfortunately, the recent Ocean GreatWhite incident is likely to result in the company falling short of its projections.

On a more positive note, Diamond Offshore Drilling managed to secure two-year contract extensions for two of its high-specification drillships in the U.S. Gulf of Mexico at decent rates.

Consequently, I have raised my Adjusted EBITDA projections for 2025 and 2026 and would urge investors to look beyond the company’s mediocre near-term prospects and rather focus on next year’s earnings inflection.

However, following the most recent rally in offshore oil service stocks, I wouldn’t chase the shares aggressively and rather wait for a near-term pullback.

I am reiterating my “Buy” rating on the stock, with an increased price target of $19.

Q2 2024 Earnings Call Transcript")