J Studios/DigitalVision via Getty Images

Introduction

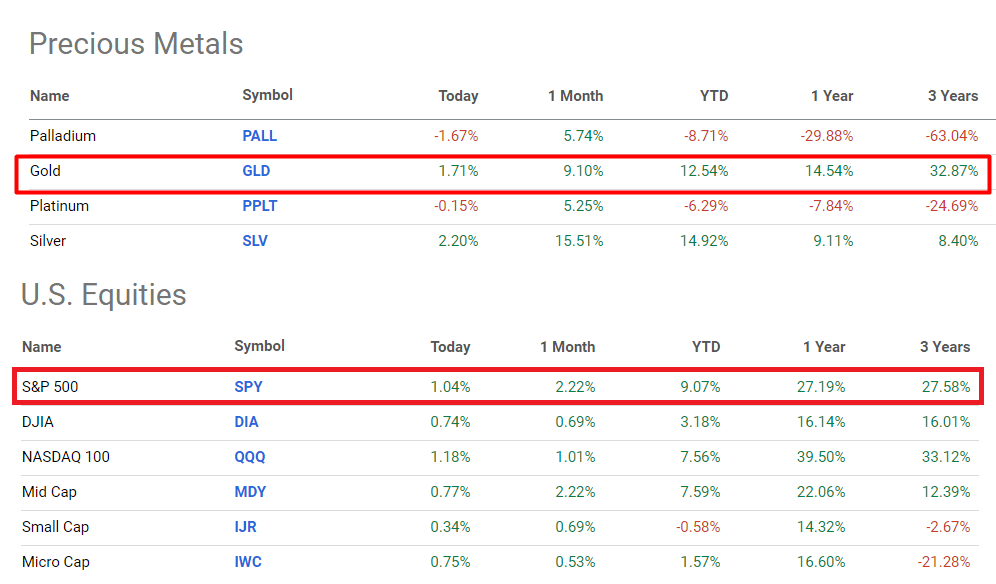

Looking at recent market trends, it is easy to overlook the fact that the price of gold has suddenly shot up after many years of stagnation and has outperformed the majority of other assets over the past few months:

Seeking Alpha, author’s notes

There might be various arguments why the gold is going up so much:

- expectations of increased government spending, exemplified by the Biden administration’s proposed $7.3 trillion budget for fiscal 2025;

- a greater willingness from central banks to tolerate higher inflation;

- favorable financial conditions (peaking Fed’s tightening).

Whatever the reason, the gold price could rise further to $2,600 per ounce if long-term real interest rates continue to weaken, write the analysts at Jefferies in their latest note (proprietary source). But they also add that there are concerns about the operating outlook for gold miners, including doubts about project spending, operational execution, and geopolitical risks. Moreover, some investors are skeptical about multi-year company guidance and fear upcoming Q1 2024 results. With this in mind, I decided to take a look at Newmont Corporation (NYSE:NEM) – the largest gold mining company in the world – and try to assess the stock’s growth prospects.

Newmont’s Recent Financials And Prospects

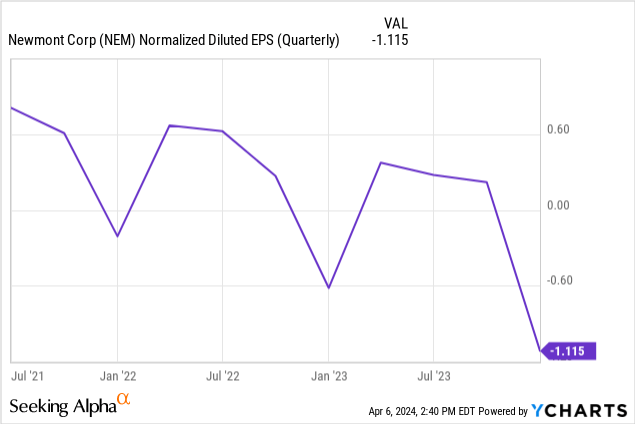

The company reported for its Q4 FY2023 on February 22, 2024, beating the consensus estimates both in terms of revenue and EPS figures, showing a YoY growth of 23% in sales. Despite that top-line expansion, Newmont remained vigilant about managing expenses: Its adjusted EBITDA amounted to ~$1.4 billion while the margin slightly narrowed to 34.9%. Hence we see the deterioration in terms of absolute EPS number:

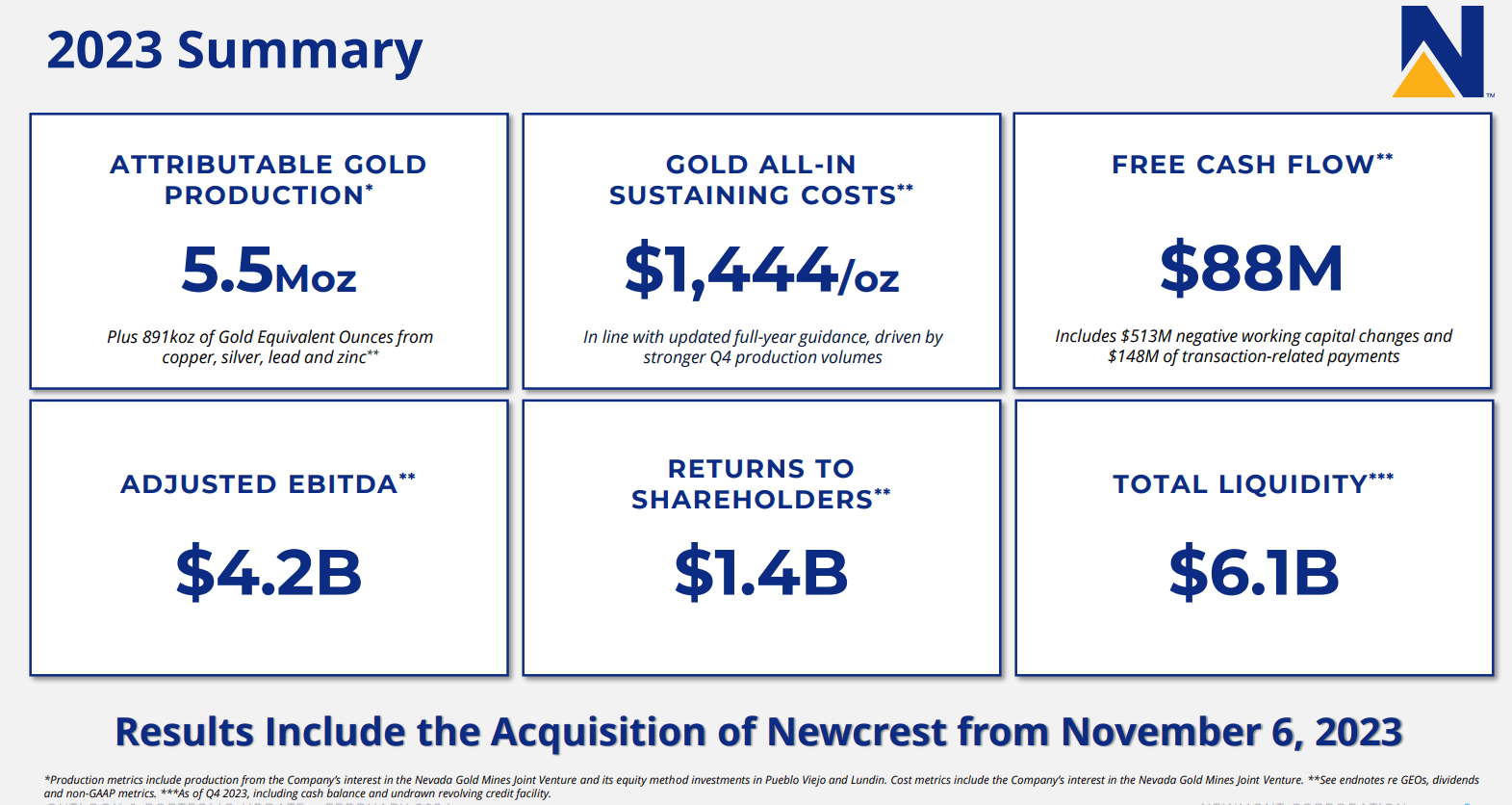

The financial results for the full year 2023 are quite straightforward and are clearly presented to investors in the latest IR presentation:

NEM’s IR materials

Since NEM’s revenue is almost 90% dependent on selling gold, its financial results are closely linked to trends in gold production and pricing. As an example: according to the press release, Q4’s revenue growth was primarily fueled by a 7% increase in gold production, totaling 1.74 million ounces, and also the uptick in the average realized gold price reaching $2,004 per ounce (+14% YoY).

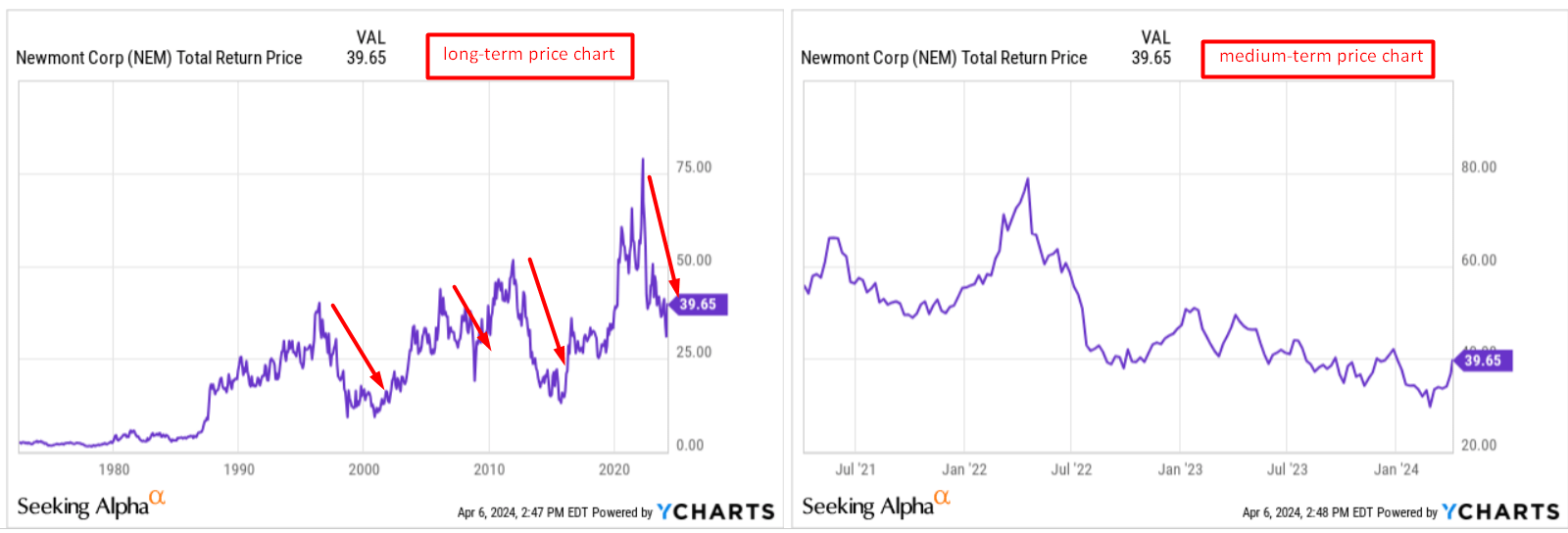

Gold remains a safe-haven asset, now trading above $2,000 per ounce due to ongoing geopolitical tensions (Israel-Palestine, Russia-Ukraine, etc.) and prospectively lower U.S. interest rates – logically, this is a very positive sign for NEM. But the stock price reacts almost in no way to this catalyst, if we do not look just at the short-term time frames (1 week – 3 months) but at the medium and long-term price charts. From a cyclical perspective, NEM is at its local lows, as in previous decades:

YCharts, author’s notes

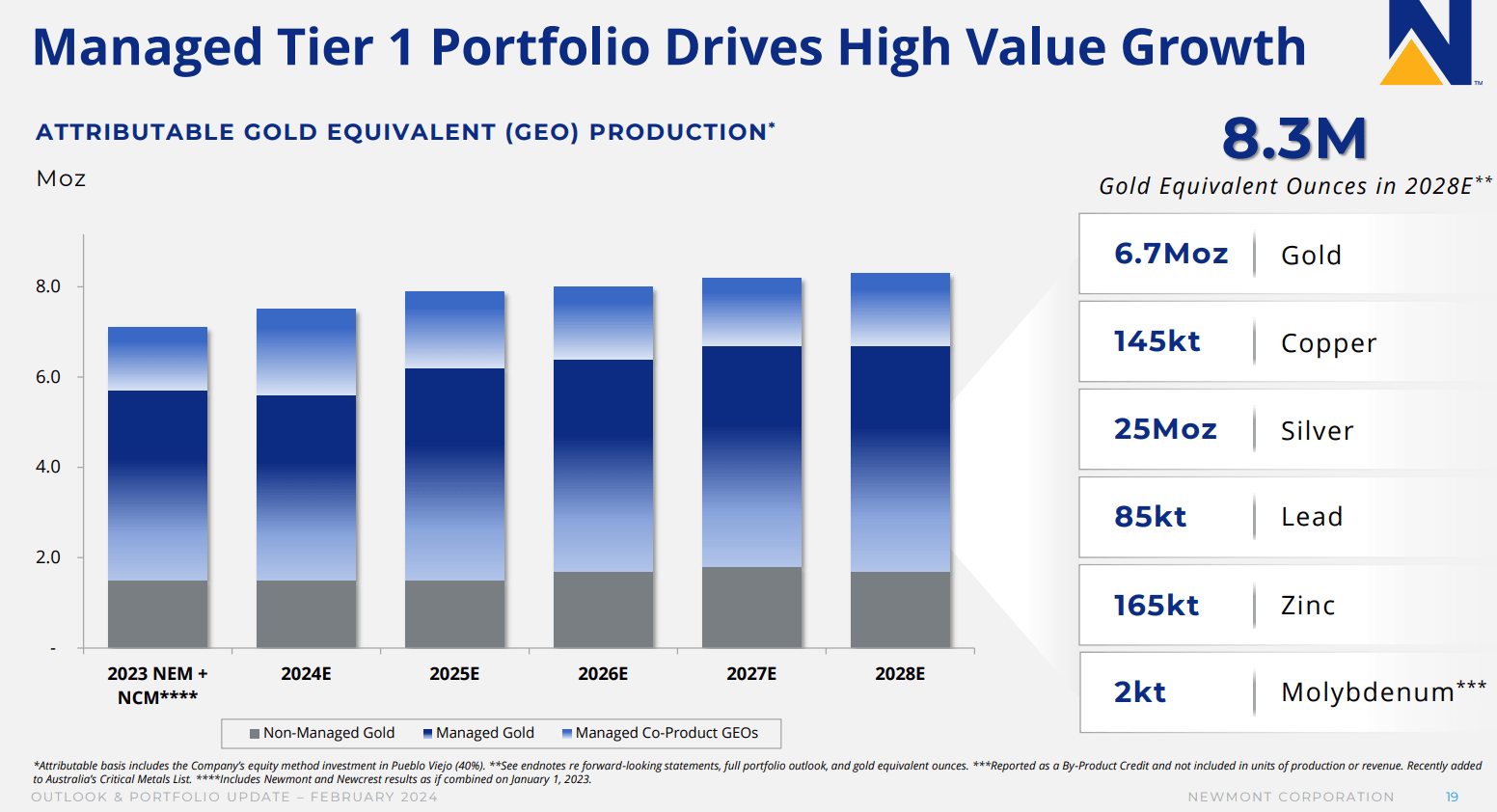

I believe that if gold prices stay above $2,000 per ounce for some time (right now it’s heading to $2,350), Newmont should see better margins once operational conditions normalize and the company’s business development initiatives unfold. As part of management’s strategy, according to the latest earnings call, NEM wants to divest 6 non-core assets, concentrating more efforts on maximizing returns from its Tier 1 copper and gold projects.

NEM’s IR materials

In addition to the synergy effects of the Newcrest Mining acquisition, the CEO said they plan to deliver ~$500 million in annual cost and productivity improvements by FY2025 – it’s like saving almost a whole quarter of today’s operating costs.

Newmont is also targeting a $1/sh. annual base dividend and announced a new $1 billion share buyback program – all of which adds up to a dividend yield of ~2.52% and a buyback yield of ~2.18%, for a total shareholder return of just over 4.7%. Not bad, in my view.

Full-year 2024 Newmont expects to increase gold production to 6.9 million ounces while aiming to manage costs effectively, as mentioned above, forecasting an average gold price of $1,900 per ounce for the year. As you can see, it’s much lower than what the gold price has shown in recent weeks. I assume that the management team wanted to hedge their bets because according to the 10-K, the average gold price for FY2023 was $1,941 per ounce. Nevertheless, to me, it’s clear that the market is offering Newmont a chance for much stronger growth than what management initially foresaw, and even compared to what Wall Street predicted just a month ago.

Given the top-notch quality of the company’s portfolio and its global importance in the gold mining industry, I expect that the actions planned by management to cut operating costs and focus on the core Tier 1 assets will likely lead to a significant uptick in revenue, EBITDA, and net profit in 2024-2025. But the stock’s prospects should also depend on the valuation. Let’s take a closer look there.

Newmont Stock’s Valuation Analysis

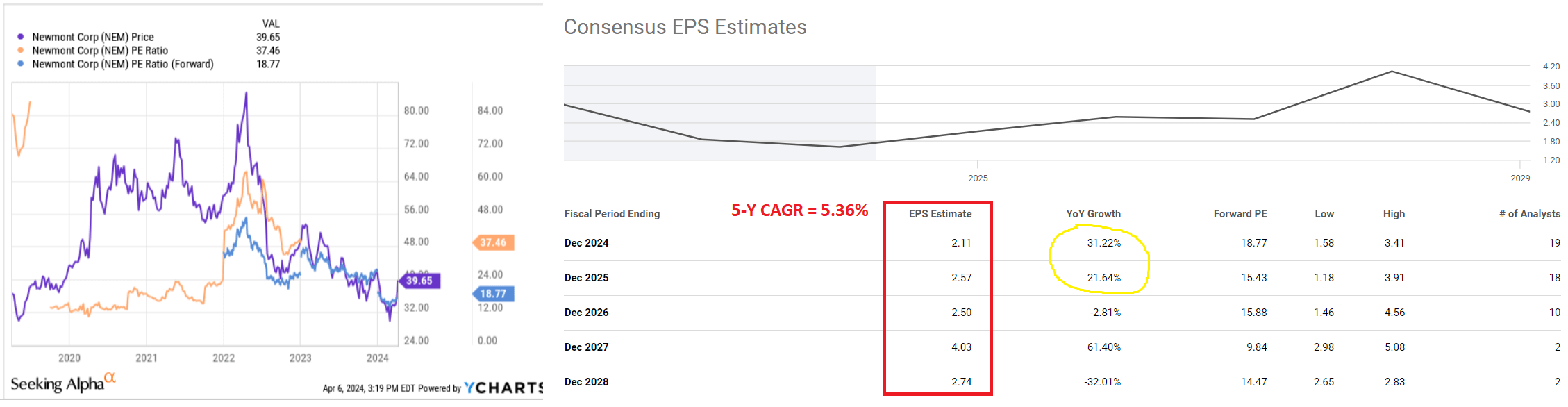

Initially, I considered assessing Newmont shares using the traditional DCF valuation model, but I quickly realized that attempting to predict the price of gold 5-6 years forward is quite a risky endeavor. Instead, I find it wiser to concentrate on the current or next-year valuation multiples and a discount (or a premium) the market is pricing in right now – especially considering the recent dynamics in gold prices and their anticipated trajectory.

YCharts, Seeking Alpha, the author’s notes

Looking at the company’s TTM price-to-earnings of around 37.5x, we see that next year, Newmont is expected to trade at almost 19x. This multiple contraction is based on the consensus view that the EPS will grow at a CAGR of 5.36% over the next five years, while the bulk of this growth is going to come in FY2024 and FY2025 (and also FY2027). While the overall EPS momentum may appear somewhat volatile, the consensus for this year and next may be close to the truth as 19-18 analysts form the consensus.

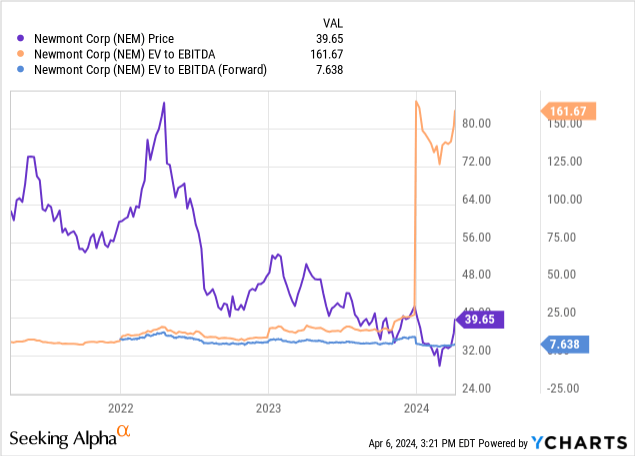

A similar picture emerges based on other multiples – below is the example for TTM and FWD EV/EBITDA:

So, what does this mean in my view? In the long term, the company’s EPS should grow by over 5% annually based on the consensus data. Remember, the management plans to reward investors through dividends and buybacks at ~4.7% in 2024. Looking at the historical chart of where the company’s P/E multiple typically resides, it seems to hit a local bottom right now (similar to what we’ve seen in 2020 or 2021). Considering all this input data, it appears to me that Newmont stock is currently undervalued. I estimate a fair multiple at ~25x by the end of 2024, which leads me to believe that Newmont’s stock could reach around $52.75 in a matter of months, assuming the current consensus of $2.11 in EPS for FY2024 holds true. This indicates a potential upside for NEM of ~33%, not factoring in the dividend and buyback yields (so the overall investor return could surpass 35%). However, this growth potential will only remain, in my opinion, if management succeeds in turning its cost management plans into reality and the gold price has enough strength to stay above $2,000 per ounce. Here lies the risk, among many others.

Where Can I Be Wrong?

One risk to my conclusions is tied to the price of gold – it’s evident from the chart below that the current price is quite overheated (take a look at the RSI indicator). We may be on the verge of a correction, and the duration of this correction remains uncertain.

Source: Refinitiv [shared by the TME newsletter]![Source: Refinitiv [shared by the TME newsletter]](https://static.seekingalpha.com/uploads/2024/4/6/49513514-17124326129178503_origin.png)

Furthermore, while the market has been factoring in fewer rate cuts this year, as I mentioned in my recent macro article, any shift in expectations regarding rate cuts could potentially impact the movement of gold.

Another significant risk lies in management’s ability to effectively steer the current situation in a positive direction. By this, I mean in particular the plan to reduce operating costs, which is to be implemented by 2025. If Newmont’s margins don’t increase as I expect today, there is a possibility that the stock price will stagnate or even fall further.

Summary Thesis

Despite the myriad risks surrounding Newmont today, I firmly believe that the company has great prospects and its stock is too undervalued to ignore. We all understand that Newmont Corporation embodies a cyclical narrative. I think that today, various macro, industry, and idiosyncratic factors suggest that the cycle for Newmont is once again turning bullish. Considering that the company’s shares are trading at only 15-18 times forwarding net earnings, I believe we can deem them as inexpensive. Anticipating growth in net profits over the next couple of years, I assign a “Buy” rating today.

Thank you for reading!

Q2 2024 Earnings Call Transcript")