GrandviewGraphics/iStock via Getty Images

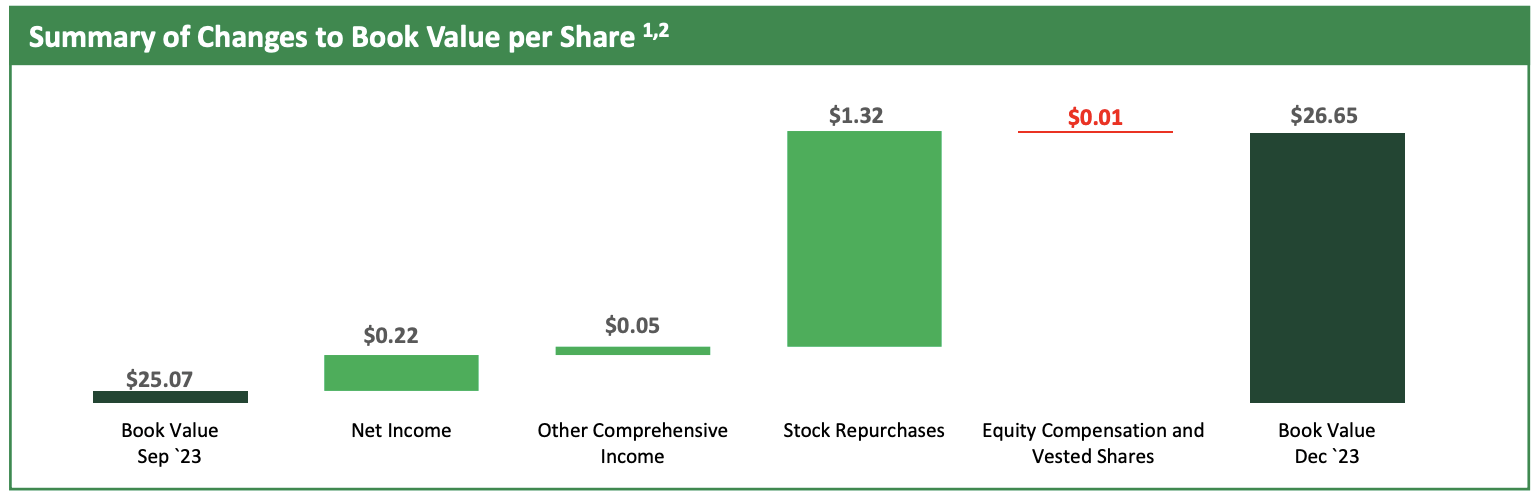

ACRES Commercial Realty’s (NYSE:ACR) remarkable discount to its book value remains steep even after its 50% 1-year rally. The commercial mortgage REIT last reported a GAAP book value per share of $26.65 at the end of its fiscal 2023 fourth quarter, this was a sequential increase of $1.58 per share primarily on the back of the mREIT’s stock buyback program that saw its weighted average number of outstanding shares end the fourth quarter dip 2.78% year-over-year to 8,566,058. ACR at its current $14.09 stock price is swapping hands at a significant 47% discount to book value. The program has roughly $9.8 million left after the buyback authorization was expanded by $10 million in November.

ACRES Commercial Realty Fiscal 2023 Fourth Quarter Presentation

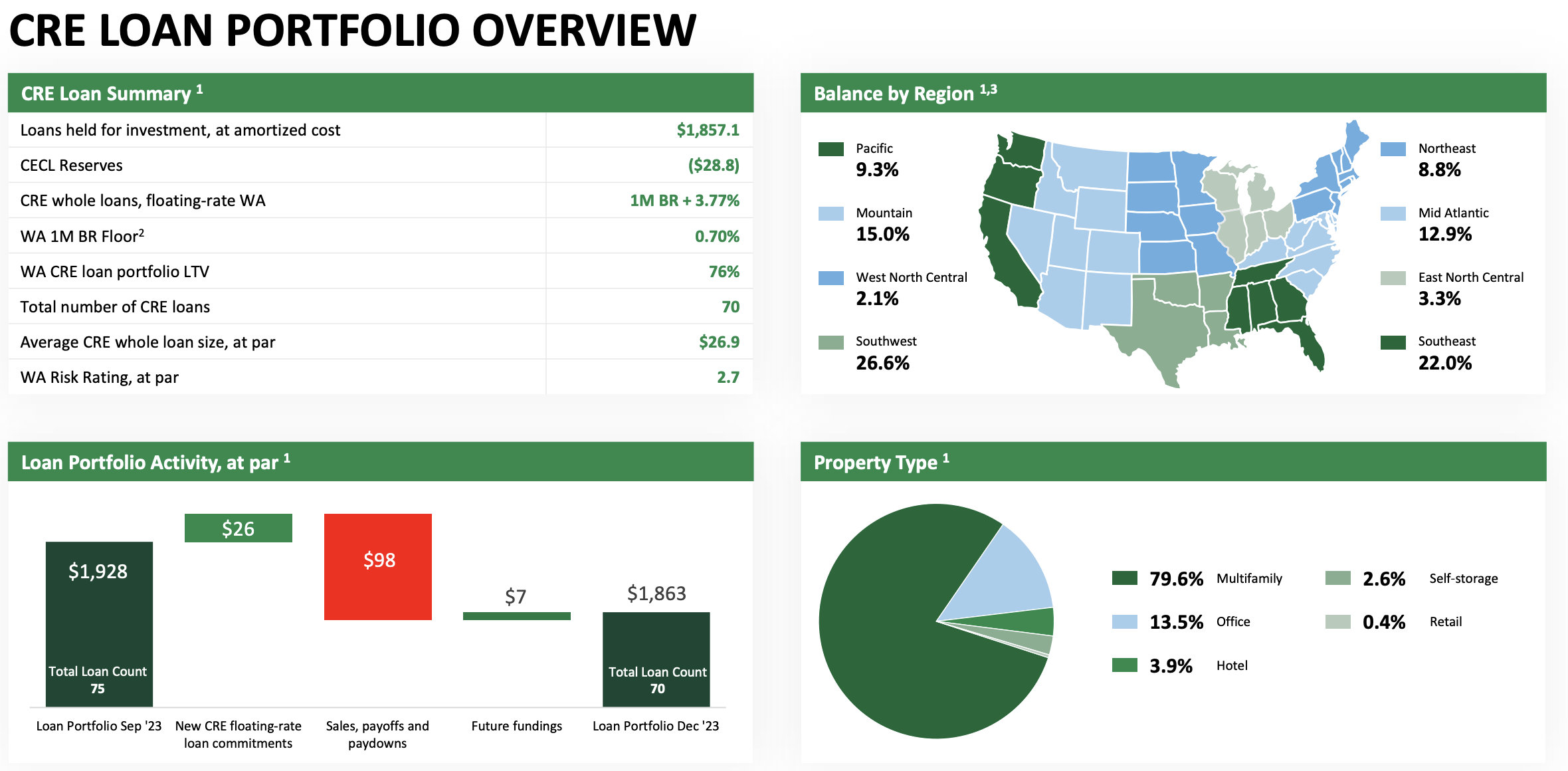

ACR’s loan portfolio at the end of the fourth quarter stood at $1.86 billion before a $28.8 million allowance for credit loss. The mREIT is heavy on multifamily loans which constitute 79.6% of its CRE loan portfolio with office loans the second largest segment at 13.5%. There’s also broad US geographic diversification with 70 loans at the end of the fourth quarter priced at 3.77% over the one-month benchmark rates. The investment play here is that ACR will be able to close the discount to book value on the back of strong underwriting quality, its buyback program, and the continued growth of book value per share. Keeping allowance for credit losses and nonperforming loans low will form critical tenets of the bull case.

ACRES Commercial Realty Fiscal 2023 Fourth Quarter Presentation

Underwriting Quality, Risk, And Liquidity

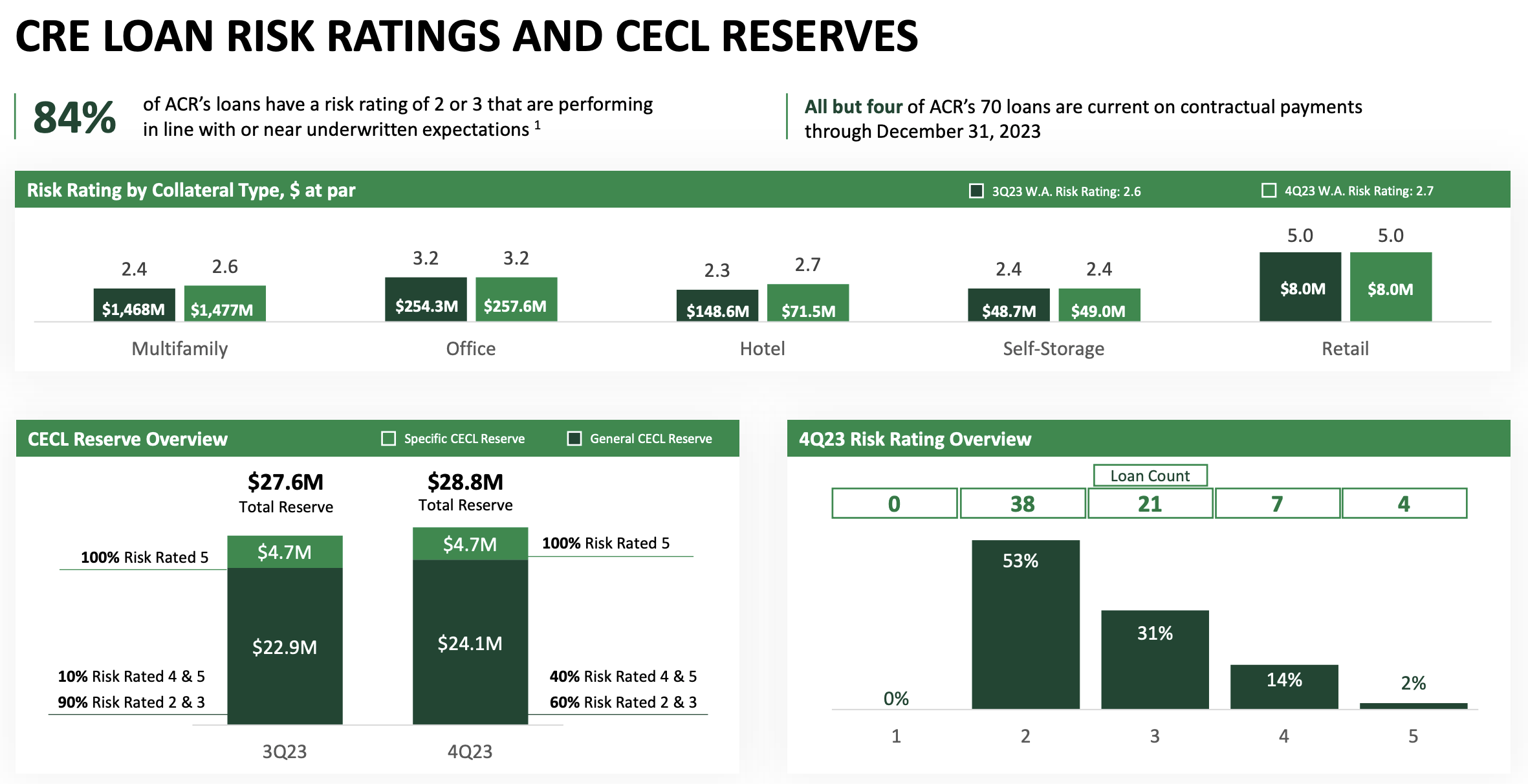

The market has discounted ACR by 50% because of uncertainty over the direction of US CRE. This part of the economy has become the stock market boogeyman and according to bears the harbinger of doom for the entire US financial system. However, ACR’s intrinsic focus on multifamily loans means its portfolio is better shielded from the uncertainty wrought by the rise of work-from-home office vacancy rates. Roughly 84% of ACR’s loans had a risk rating of 2 or 3 at the end of the fourth quarter with four loans not performing in line with contractual obligations. This was a sequential deterioration from 92% of loans with a risk rating of 2 or 3 at the end of the third quarter.

ACRES Commercial Realty Fiscal 2023 Fourth Quarter Presentation

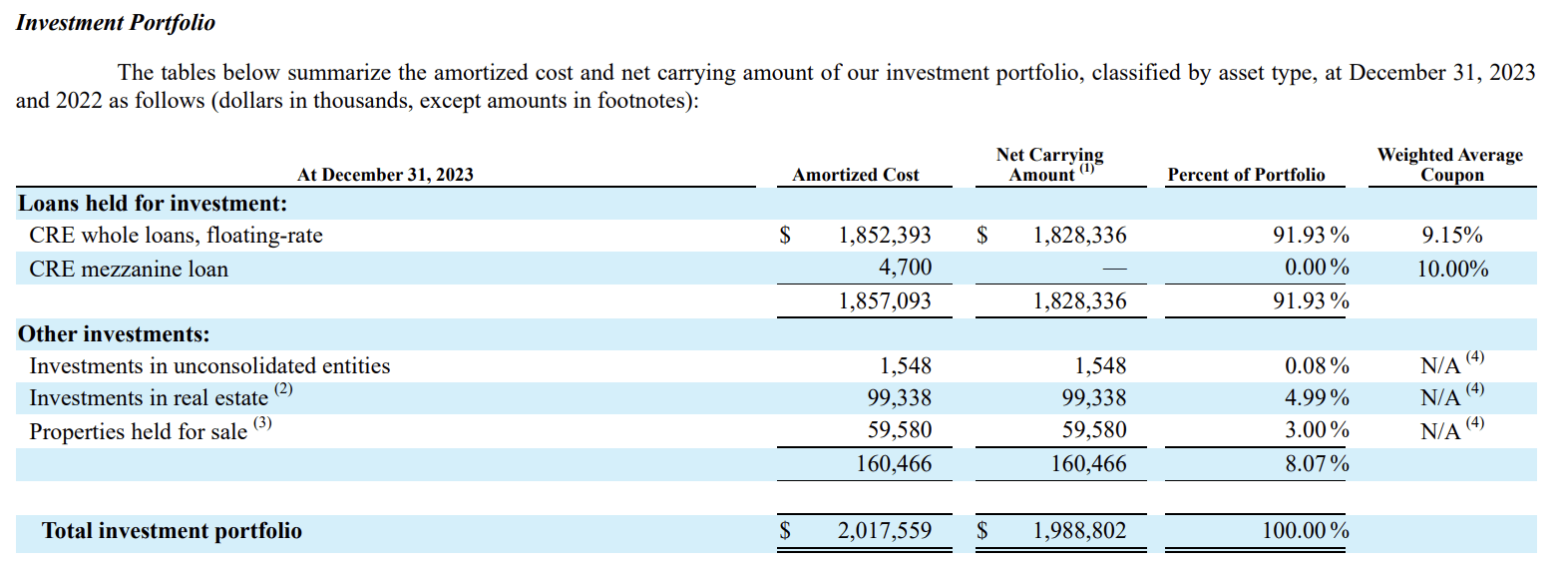

ACR’s CECL reserve at $28.8 million was up $1.2 million from the third quarter as the risk rating of its multifamily loans worsened slightly, rising to 2.6 from 2.4 at the end of the third quarter. However, CECL reserves at just 1.55% of ACR’s loan portfolio highlight the benefits of the mRETI’s focus on multifamily properties and healthy underwriting standards. ACR’s total investment portfolio stood at $2.02 billion at the end of the fourth quarter, up marginally sequentially with the mREIT holding $158.9 million in net investments in real estate and properties held for sale. Available liquidity at the end of the fourth quarter stood at $108 million, formed from $83 million of cash and $25 million of projected financing available on unlevered assets.

ACRES Commercial Realty Fiscal 2023 Form 10-K

The Preferreds And The Fed

| Preferred series | Discount to liquidation price ($25) | Annual distribution | Yield on cost % | Floating date |

| 8.625% Fixed-to-Floating Series C Cumulative Preferreds (NYSE:ACR.PR.C) | -3% ($24.20) | $2.16 | 8.91% | 7/30/2024 |

|

7.875% Series D Cumulative Redeemable Preferreds (NYSE:ACR.PR.D) |

-14.2% ($21.45) | $1.96875 | 9.18% | N/A |

ACR has two outstanding preferreds (ACR.PR.C) and (ACR.PR.D) offering healthy investment profiles. The Series D is trading at a double-digit 14.2% discount to their $25 per share liquidation value and currently pays a $1.96875 annual coupon for what works out to be a 9.18% yield on cost. I’m heavily leaning toward the Series C here though. The discount to liquidation is lower at 3% but they’re floating rate from the end of July. This will be at a rate equal to three-month SOFR plus a spread of 5.927% per year and subject to a floor of 8.625%. Three-month SOFR is currently at 5.34775% with an additional 0.26161% adjustment to be added as the preferreds were initially priced using LIBOR. Hence, the aggregate coupon assuming no Fed rate cuts by this date would be 11.5%.

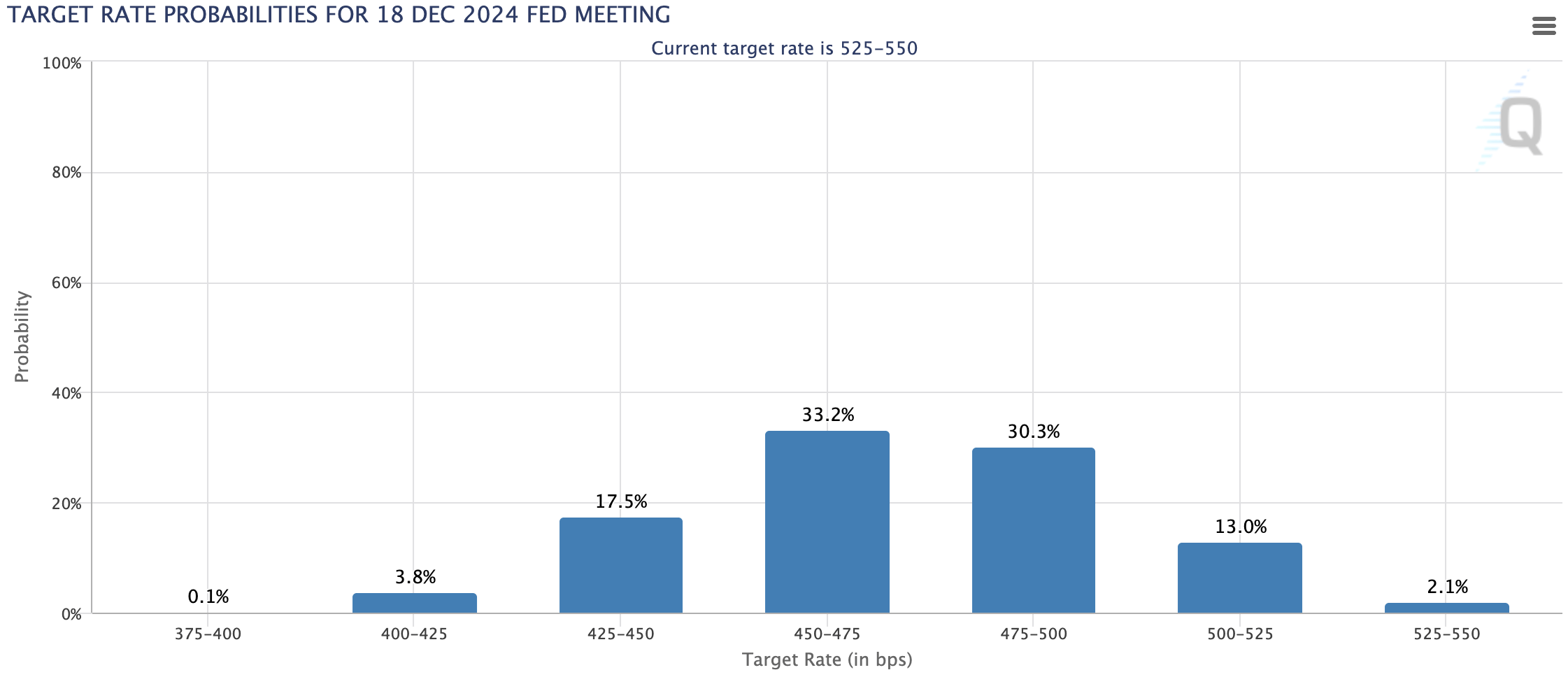

CME FedWatch Tool

The Fed is anticipated to cut rates by at least 75 basis points through 2024 with the CME FedWatch Tool pricing in base interest rates at 4.50% to 4.75% at the end of the year. Hence, this floating coupon on the Series C should still be double-digit at the end of the year with the potential discount also closed as a result of the positive duration effect of pending Fed rate cuts. I’m rating both the commons and the preferreds as buys here and I’ll look to take a position in the Series C sometime in April. The near 50% discount to book of the commons is far too steep for ACR’s multifamily heavy portfolio and the market has sold off the stock too cheaply in what can only be classed as an overreaction to CRE angst.

Q2 2024 Earnings Call Transcript")