Sundry Photography

With the S&P 500 continuing to show no slowdown in momentum, there’s a growing argument to be cautious with our portfolios. I have more than 30% of my holdings socked away in short-term bonds and cash, waiting for a better time to deploy the capital back into equities: and within the stocks that I’m holding, I’ve been cautious to prune off recent winners that have grown into outsized valuations.

Nutanix (NASDAQ:NTNX) is one of these names. The hyperconverged infrastructure software company has been on a tear this year, aided by AI tailwinds. Year to date, shares of Nutanix have jumped more than 40% as the company signs GPT-related deals to fuel its growth trajectory.

I last wrote a bullish opinion on Nutanix back in December, when the stock was then hovering near $40 per share. I had cited strong deal momentum and a reasonable valuation as the core reasons to be bullish on Nutanix at the time. I also cheered the company’s buildup in ARR (annual recurring revenue) and high margin profile.

However, my price target on the stock was $57, a level Nutanix has now blown past. At current share prices, I see more of a balanced bull and bear case for Nutanix and can’t justify being purely bullish.

Here’s what remains of the bull case of Nutanix:

-

AI is fueling more workloads and deals. Nutanix management believes AI applications will run where the data is housed. Already, the company has signed on major deals involving AI and GPT-related use cases. These use cases, as well as IT departments’ growing focus on building out the infrastructure to support automation and AI, will continue to provide positive tailwinds for Nutanix’s pipeline.

-

Prioritizing profitability. The company hit pro forma profitability for the first time in FY23 and is eyeing further gains ahead in FY24 on the back of a ramping gross margin profile. The company’s recurring revenue deals are a big component of operating leverage, as Nutanix doesn’t need to stretch itself on resources just to renew and upsell existing clients.

At the same time, however, we do have to be cognizant of a number of risks for the company:

- Public cloud isn’t going away. Nutanix strives to create an efficient and cloud-like environment for IT infrastructure, but it is not the public cloud. More and more companies are shedding their datacenters in favor of fully offloading to public cloud services. How Nutanix will coexist with this long-term trend remains to be seen.

- Slowing growth rates. Despite AI tailwinds, Nutanix is experiencing a slowdown across most of its top-line metrics, including revenue, ARR, and ACV billings. This may call into question the stock’s more expensive valuation multiple.

Nutanix’s newfound valuation remains one of the core reasons I’m now neutral on this name and shying away from holding it in my portfolio. At current share prices near $66, Nutanix trades at a market cap of $16.12 billion. After we net off the $1.44 billion of cash and $1.22 billion of debt on the company’s most recent balance sheet, Nutanix’s resulting enterprise value is $15.90 billion.

For the upcoming fiscal year FY25 (the year for Nutanix ending in June 2025), meanwhile, Wall Street analysts have pegged a revenue growth target of $2.50 billion (+17% y/y) for the company. This puts Nutanix’s valuation multiple at 6.4x EV/FY25 revenue.

For a company whose revenue growth has slowed down to the mid-teens, I’d prefer to lock in gains here and retreat to the sidelines until a better price avails itself.

Q2 download

Nutanix recently released fiscal Q2 (December quarter) results at the tail end of February, which already showed a slowdown across the top line. Take a look at the Q2 earnings summary below:

Nutanix Q2 highlights (Nutanix Q2 earnings release)

Revenue grew 16% y/y to $565.2 million, ahead of Wall Street’s expectations of $550.4 million (+13% y/y) but decelerating versus Q1’s 18% y/y growth rate. We note as well that Nutanix’s preferred gauge of deal momentum, ACV billings, also showed a slowdown in growth to 23% y/y, from 24% y/y growth in Q1 – and it’s looking to get worse before it gets better.

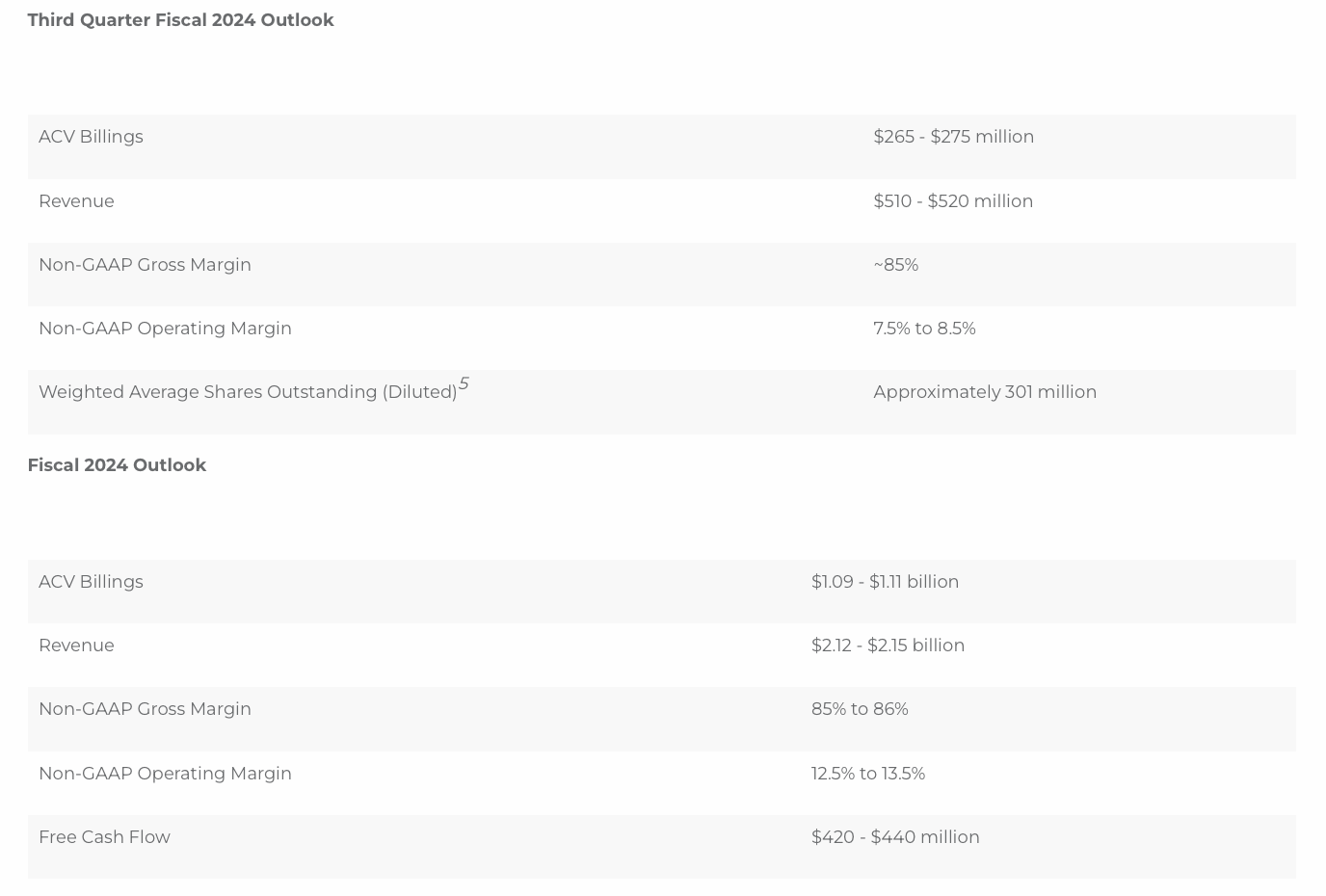

The company’s Q3 outlook is shown below: compared to $240 million in ACV billings in the third quarter of FY23, the company’s guidance of $265-$275 million implies a slowdown to a growth range of just 10-15% y/y growth.

Nutanix outlook (Nutanix Q2 earnings release)

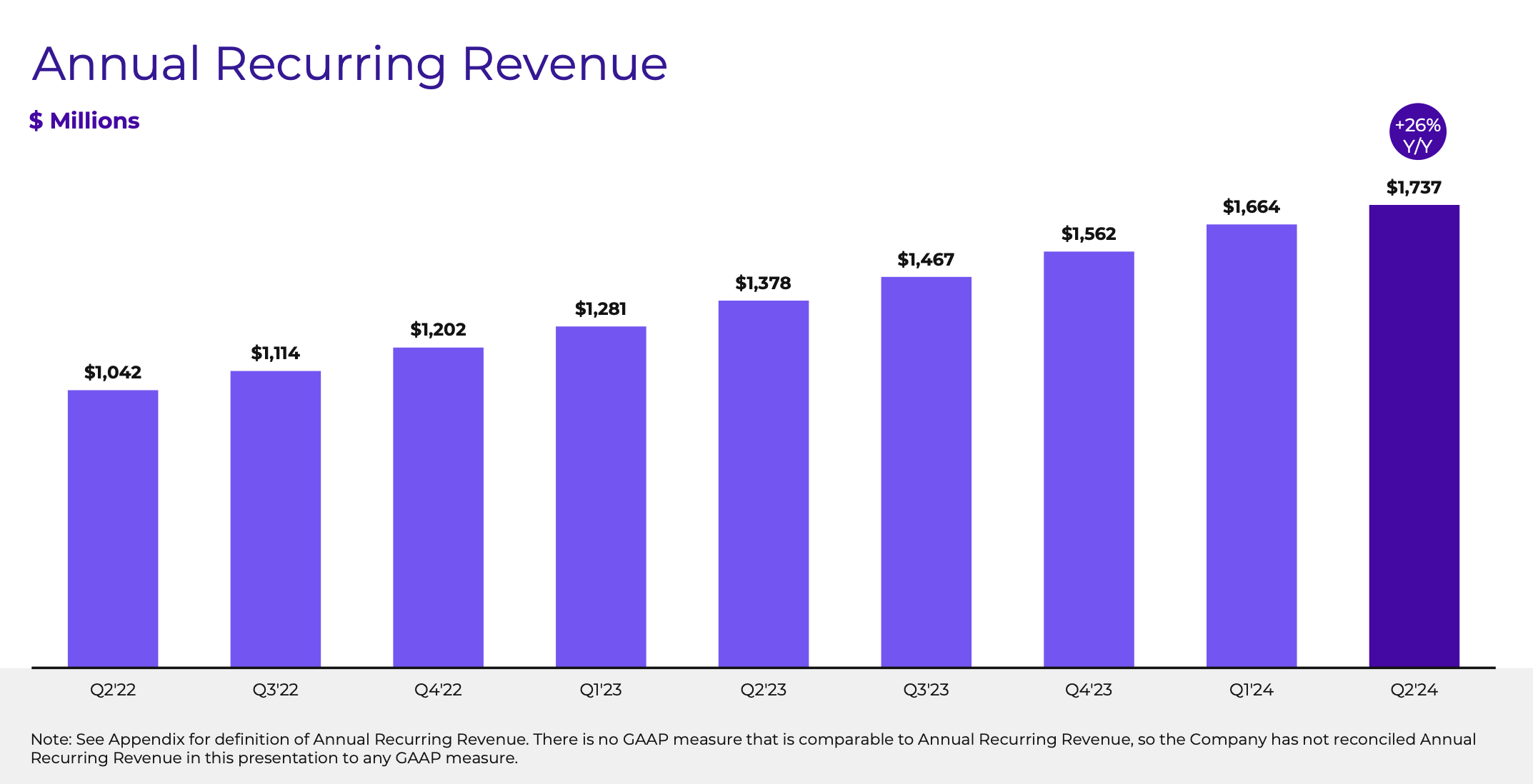

ARR, too, has also shown signs of weakening. The company added just $73 million in net-new ARR in the second quarter, versus $102 million added in Q1; while y/y growth slowed from 30% y/y in Q1 to 26% y/y in Q2.

Nutanix ARR trends (Nutanix Q2 earnings release)

Note that the December quarter tends to be the largest quarter for deal closings and ARR growth, as IT departments try to exhaust their budgets before the end of the calendar year. In the prior December quarter, Nutanix had added $97 million of ARR on a sequential basis – showing that deal closings are either slimmer or that upsells are waning. And again, this is despite the company citing AI tailwinds as a driving force for deal closings.

Rukmini Sivaraman, Nutanix’s CFO, noted on the Q2 earnings call that macro pressures have continued to cause deal cycles to elongate:

I will now provide some commentary regarding our updated fiscal year ’24 guidance. First, we are seeing continued new and expansion opportunities for our solutions despite the uncertain macro environment. However, as we mentioned previously, we have continued to see a modest elongation of average sales cycles relative to historical levels. Our fiscal year ’24 new and expansion ACV performance outlook assume some impact from these macro dynamics. We are also seeing a higher mix of larger deals in our pipeline, which is driving greater variability in the timing of our new and expansion business.

Second, the guidance assumes that our renewals business will continue to perform well. Third, the full year guidance continues to assume that average contract duration would be flat to slightly lower compared to fiscal year ’23, as renewals continue to grow as a percent of our total billing. Fourth, a reminder that the full year ACV billing is not the straight sum of the ACV billings of the four quarters due to contracts with duration less than one year. We expect full year ACV billings to be about 5% to 6% lower than the sum of the four quarters ACV billings.”

This being said, we are impressed at the company’s continued profitability growth, as pro forma operating margins improved 750bps y/y to a sky-high 21.9%, nearly putting Nutanix in the so-called “Rule of 40” alongside its 16% y/y revenue growth. Large operating margin increases are always a nice salve alongside slowing top-line growth, which we hope Nutanix can continue to achieve heading into the back half of its FY24.

Key takeaways

With Nutanix calling for key growth measures to moderate in Q3, it’s a good time for us to lock in gains after a 40%+ rally since the start of the year. Keep this stock on your watch list, but rotate your portfolio toward more value-oriented names.

Q2 2024 Earnings Call Transcript")