Sydney James/DigitalVision via Getty Images

Investment Thesis

McCormick & Company (NYSE:MKC) reported results on the 26th, March, beating on revenues and EPS so the share price jumped over 10%. MKC was founded in 1889 and is a dominant player in selling spices and seasonings to the food industry. They sport a wide moat, however, food inflation has increased cost of sales and the company has experienced a significant drop in margins. I am initiating a Buy on MKC as I see margins recovering as inflation reduces.

Background

MKC is a dominant player in the global spices and herbs market. They sport 20% market share in this category which is four times their closest competitor, and the market is forecast to grow at 4.67% CAGR to 2029. Their suite of intangible assets and strong relationships with retailers allows for a wide moat over the competition. And they are one of the only company’s to offer private label as well as branded spice products.

In the Consumer segment their brands reach 170 countries and form 57% of revenues. It is in this category where they sell spices, seasonings and condiments. Under the Flavor bracket they sell a wide range of flavoring products to food manufacturers and it forms the remaining 43% of revenues.

MKC’s Consumer segment is benefitting from a global increasing in demand, especially in Europe. As developing nations adopt a healthier lifestyle of living. Herbs and spices are associated with wellness which is becoming increasingly adopted by first world countries. Major importers of herbs and spices include Germany and the UK.

The Flavor segment is being driven by blended spices which are used in savory snacks, beverages and sauces. With the rise in immigration comes different tastes, so ethnic groups are driving demand for spices from their native countries which is aiding MKC revenues. Also, since the pandemic, consumers prefer to dine at home rather than in restaurants, so find themselves picking up spices from the shelf and making homemade recipes.

As a result of the drive to include more spice in your life, it is essential that manufacturers keep innovating and finding new blends. Various studies have found that the US consumer is very open to trying new spices, with 50% opting they would try something new.

Investor Presentation

CCI and GOE Programs

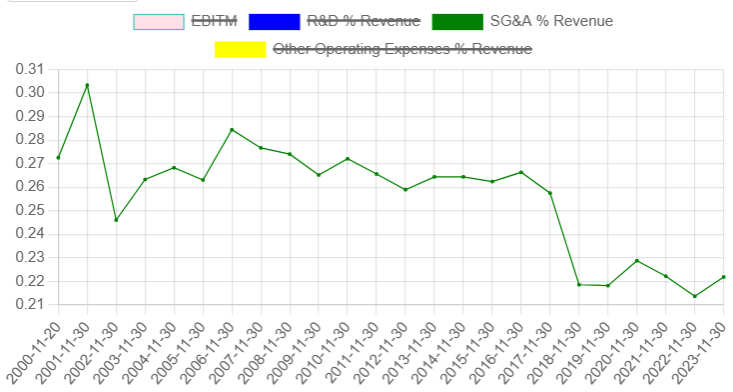

In 2009 MKC announced the they are fueling investment into their CCI and GOE programs. The CCI program aims to improve productivity and reduce costs by investing in brand marketing and growth initiatives, and the GOE program was based on a voluntary retirement plan.

So has it worked? Yes. SG&A Margins dropped 390 basis points in 2018 and have remained steady ever since. This is a result of efficiencies across the organization and a reduction in the number of employees in 2023 following the GOE program. It has also been reported that MKC recently partnered with Cognizant to improve their technology infrastructure through AI. Which I believe will drive further efficiency gains.

Source: Author’s Calculations

Financials

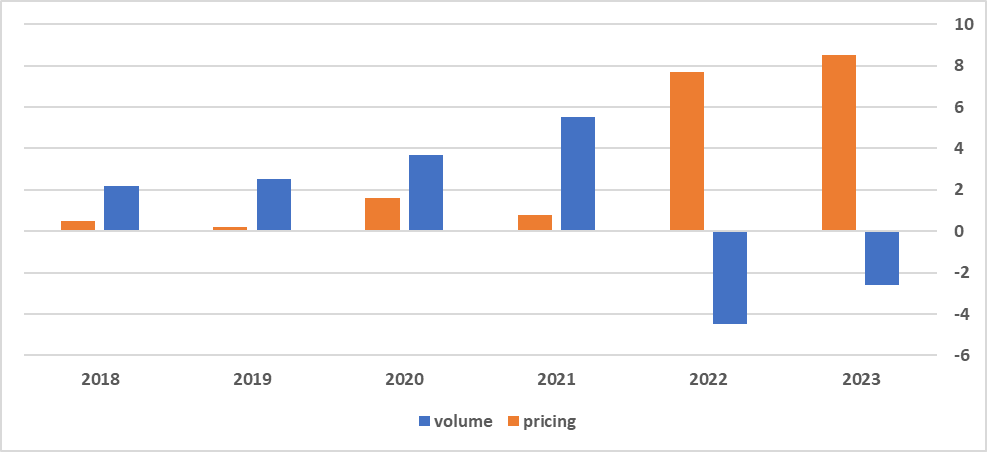

MKC has trailing revenues of $6.70 billion with a 5-year CAGR of 4.72%, which places it towards the median of the industry. Prior to 2022 the company gradually increased prices and volumes grew which bolstered sales by a growth of 5.9% CAGR between 2018 and 2021. But with the increase in raw material costs MKC has significantly increased prices in a bet to soften the impact on margins, and I believe this has impacted volumes. In the latest quarter MKC raised prices 3% offset by a 1% decline in volumes, indicating that prices are moderating and volumes are returning. Investors will welcome the return in volumes, because the current rise in prices isn’t sustainable over the long-term and will result in market share losses.

Source: Author’s Calculations

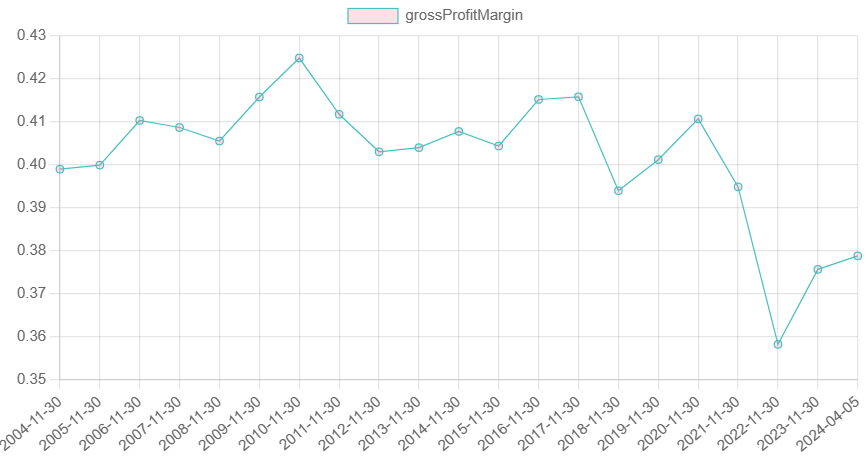

Despite the increase in prices, inflation has taken its toll on gross margins which contracted 370 basis points in 2022. We have since seen a recovery but they remain well below historical standards. I believe with inflation coming down we should see a full recovery here.

Source: Author’s Calculations

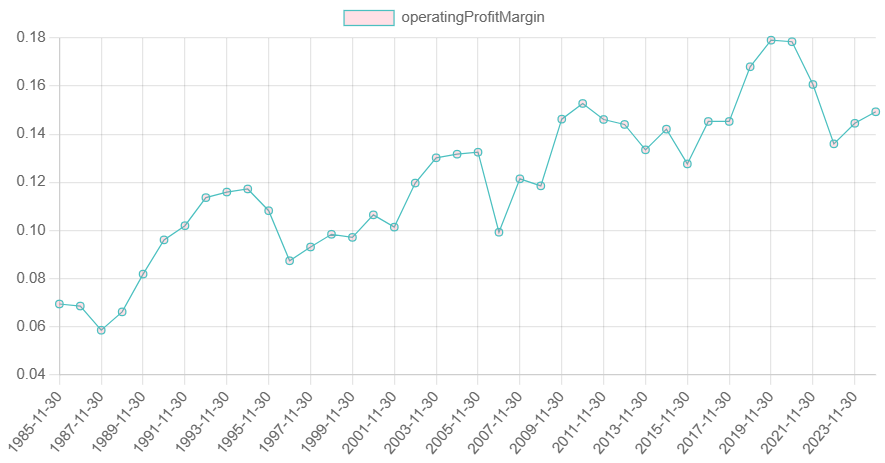

The cost reductions plans discussed above have helped mitigate the impact of inflation further. EBIT Margins declined 250 basis points in 2022 as SG&A Margins fell to record levels. They have since recovered but have a way to go before reaching pre-COVID levels. Below you can see the significant affects of the cost reduction plans on EBIT Margins between 2017 and 2020. And note the long-term uptrend.

Source: Author’s Calculations

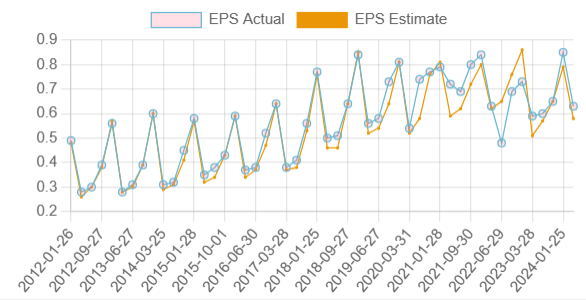

The company’s capital allocation strategy has changed over the years. They have always paid a consistent dividend, which stands at a yield of 2.4%, invested for organic growth and made the odd acquisition. But since 2017 the company has cut its share repurchase program. Between 2013 and 2016, the company spent on average 5 cents for every dollar of revenues repurchasing shares. But that has since dropped to below 1 cent for every dollar. This will be hindering bottom line growth, which is evident as EPS has consolidated since calendar Q3 2018.

Source: Author’s Calculations

MKC has trimmed its Net Debt to Sales ratio but it still stands at a level of 50%. They have upcoming principals this year of $250 million, in 2025 of $500 million and 2026 of $750 million. Their current cash balance is $180 million and they have produced on average $680 million in Free Cash Flow over the last 4-years. This is a bit tight, but the company should have sufficient funds to service these principals.

Total company sales increased 3% from a year ago, and 2% at constant currency. This was driven by a 3% increase in pricing offset by a 1% decline in volumes. Operating leverage improved on an adjusted basis by 5% and EPS came in at $0.62, reflecting a 7% increase. The Consumer segment increased 1% with prices increasing 3% and volumes declining 2%. Some of the decline in volumes was due to MKC exiting lower margin businesses. The Flavor category increased 2% constant currency with volumes increasing 1% and prices also increasing 1%.

In terms of guidance, MKC expects constant currency sales in the range of -1% to 1% driven by further pricing actions and a return to volume growth. They also expect adjusted EBIT to expand between 3% and 5% driven by gross margin expansion.

Revisions

Most future year revenue revisions are down around 5% over the last 6-months. But some far out years have moved up in the last month. Similar story for EPS over the last 6-months, but all years have seen upgrades in the last month.

EPS revisions (Seeking Alpha)

Similar to other packaged food and meat companies MKC is facing a challenging macroeconomic backdrop, especially in China, where sales growth is forecast to remain flat on 2023. Consumers are feeling the pressure on pockets and are being choicely in their purchases. Also, restaurant traffic remains low. But with the company forecasting EBIT Margins of $963 million and flat sales growth it equates to a margin of 14.5% which is flat on 2023. This guidance factors in less of a recovery than competitors such as Tyson Foods so there could be room for upgrades in future quarters.

Valuation

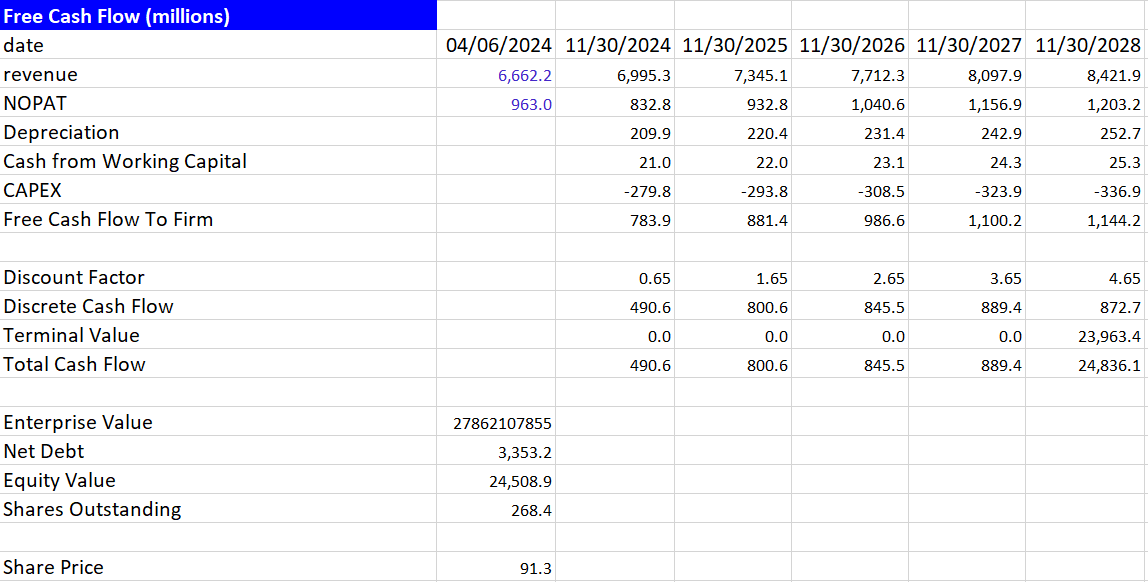

Source: Author’s Calculations

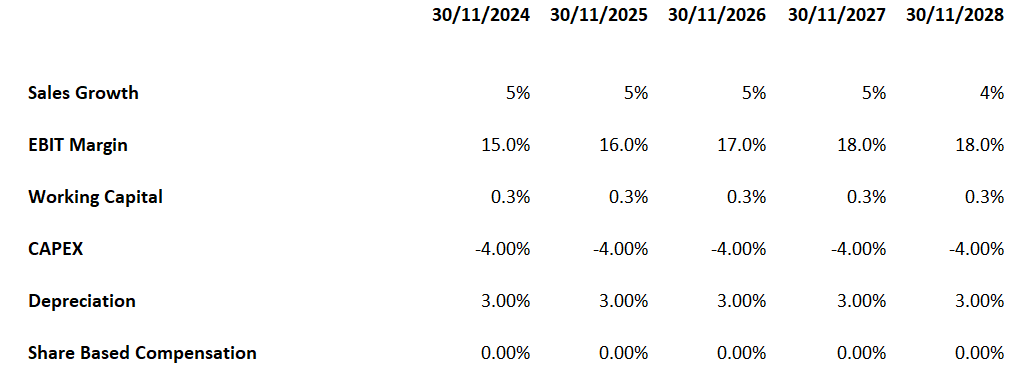

To arrive at my share price target of $91 I have used the 10-year P/FCF median multiple of 27x with a WACC of 6% (gurufocus). I have EBIT Margins expanding from current levels to 18% by 2027, as I believe inflation will moderate and the company will keep finding efficiencies.

The company delays payments to suppliers, which produces a large balance of accrued liabilities so I have working capital incrementing sales by 0.3% and have CAPEX running and the long-term median of -4%.

Source: Author’s Calculations

Risk

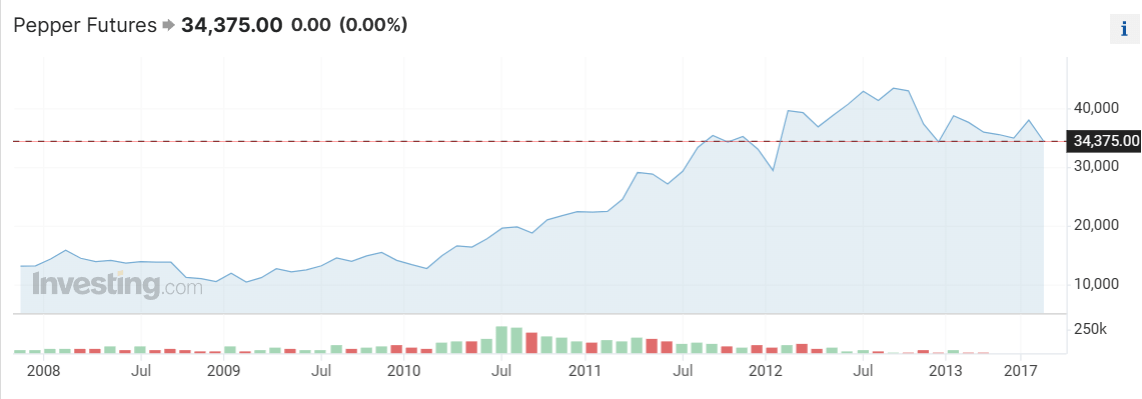

Because MKC produces and distributes spices and seasonings, its cost structure is heavily affected by commodity prices. To illustrate, Pepper prices quadrupled between 2009 and the summer of 2012. This is a key raw material for MKC and Gross Margins contracted 130 basis points over the period.

Pepper price (Investing.com)

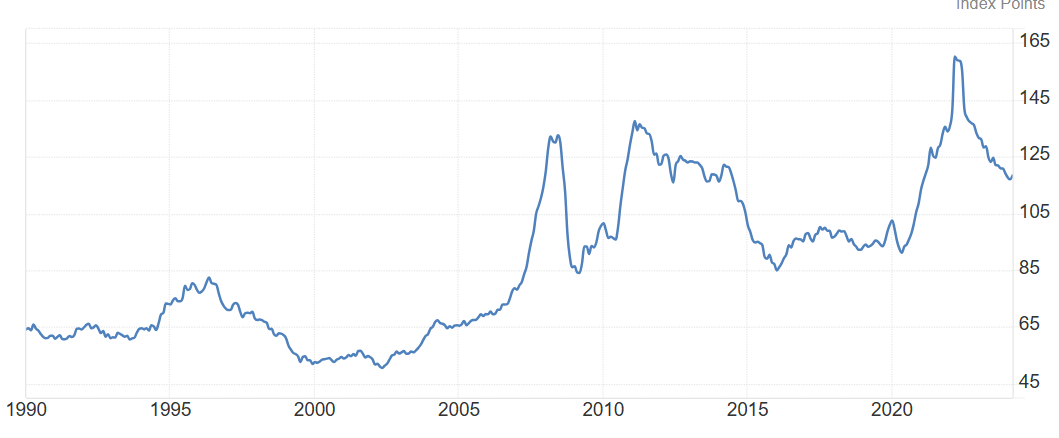

World Food prices remain elevated but have reduced on the highs of 2022. They increased in March and the risk is that they increase further, once again asserting pressure on MKC margins.

World Food Price Index (Trading Economics)

Another risk is the trend in volumes. MKC has been grappling soft volumes for over 2-years and there is a risk these remain subdued as interest rates squeeze consumers. That being said they should benefit from their private label sales, however, this might hinder a full recovery in margins.

Conclusion

MKC has a commanding leadership, boasting the highest market share in the spices and seasoning market. They continue to source out productivity and efficiency gains across the organization, all while investing into brand initiatives and R&D. I spoke on Tyson Foods (TSN) at the beginning of March, which also stands to benefit from a recovery in margins. MKC is a similar play, so I am recommending a Buy on the company with a share price target of $91.

Q2 2024 Earnings Call Transcript")