Pgiam/iStock via Getty Images

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the last week of March.

Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the closed-end fund (“CEF”) markets for perspectives across the broader income space.

Market Action

Preferreds underperformed this week, primarily due to REITs, but the broader space still managed to eke out a positive total return over March. Over the month, all but one sector (the single-issuer BDC sector) were up.

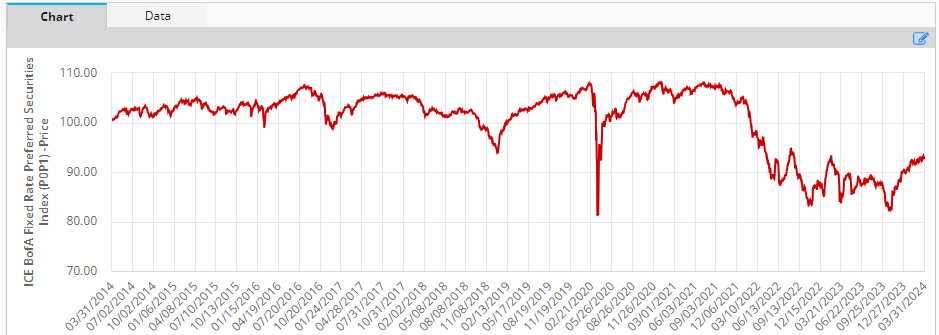

Systematic Income

The preferreds sector has enjoyed the longest rally since 2021 but remains well off its 2021 high in price terms. This highlights that yields are still significantly above their 2021 levels.

ICE

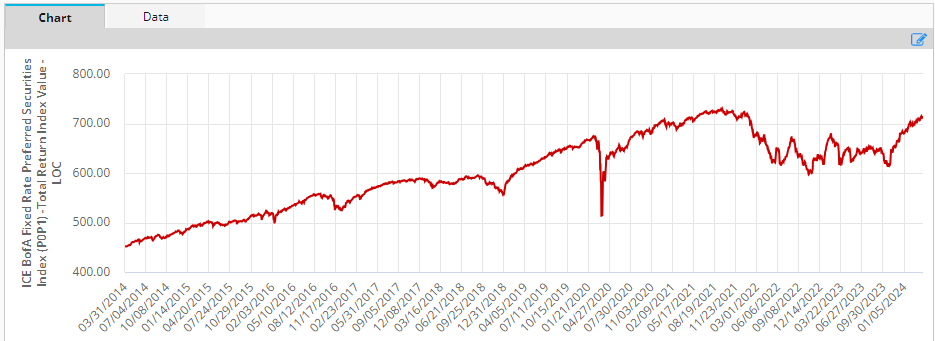

From a total return perspective, preferreds have nearly reclaimed their 2021 highs, owing to substantial dividends earned in the last 2-3 years.

ICE

Market Themes

Two recent issues have illustrated the common pattern of new issuance coming in cheaper, i.e., at higher-yields than existing securities of the same issuer. The reason for this is fairly intuitive – if new issuance were more expensive it wouldn’t attract much demand. And two, a higher yield to existing issuance gives the bookrunners a margin of safety to place the security.

There were two examples this week of issuers pricing securities above the yields of their existing ones. First was the CLO CEF Eagle Point Income Company (EIC). It is issuing an 8% 2029 preferred (EICC). The fund has two other preferreds outstanding – EICA and EICB with 2026 and 2028 maturities respectively and yields of around 7.7%.

EIC is a lower-octane CLO CEF than something like OXLC, ECC and OCCI because of its sizable CLO Debt allocation. This is one reason why EIC preferreds (as XLFT.PR.A) tend to trade at a lower yield than the preferreds of CLO Equity CEFs.

The second example was a bond issued by the BDC Trinity Capital (TRIN) which announced a new 7.875% 2029 bond (TRINZ) with a first call in 2026. The company’s other baby bond – the 7% 2025 TRINL – has been trading at much lower yields, currently at 7.08%, rarely dipping below par. This 0.8% yield pick-up over an existing issue is one of the largest we have seen.

The use of proceeds mentions redeeming the KeyBank credit agreement and possibly the 2025 bond. Refinancing the credit facility probably makes sense as it costs around 0.65% more than the new bond and it has additional covenants which the new unsecured bond does not. Refinancing the 2025 bond is a bit odd given its 7% coupon which has another 10 months to run. Maybe the company is looking at the tight credit spreads and thinks this is as good as it’s going to get for issuance even if Treasury yields are not all that low.

Between these two issues, we would consider adding TRINZ not much above par as it’s likely to rally to a comparable yield as TRINL, particularly if TRINL is partly or fully redeemed. As far as EICC, we continue to favor OXLC bonds in the broader CLO CEF senior security sector given their yields comparable to EIC preferreds with a much stronger asset coverage profile, despite the higher-beta nature of the OXLC CEF.

The key takeaway here is that investors ought to keep an eye on new issues both as tactical opportunities as well as a way to upgrade their existing holdings.

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the BDC, CEF, OEF, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis – sign up for a 2-week free trial!

Q2 2024 Earnings Call Transcript")