igoriss

The more experienced that you get with investing, particularly when it comes to individual companies, the better you tend to get a handle on what their value should be and what direction shares should eventually move. It’s not a perfect process and everybody will make mistakes. But one company that I have had a pretty solid track record with so far is Gentex Corporation (NASDAQ:GNTX). For those not familiar with the company, it operates as an automotive supplier, offering customers a wide array of digital vision, connected car, and dimmable glass products. It also sells some fire protection products.

From the time I first rated the company a ‘buy’ in April of 2022, shares are up 35.9%. That’s far better than the 19.5% seen by the S&P 500 over the same window of time. However, by December of 2023, I ended up downgrading the company to a ‘hold’ to reflect my view that the stock should perform more or less along the lines of the market moving forward. Since then, that is approximately what has transpired. Shares are up 11.4% since the publication of that article. That’s only marginally better than the 10.3% rise seen by the index. After a further increase, the question needs to be asked of whether the stock deserves any additional skepticism or, with new data now out and guidance pointing toward a rather robust 2024 fiscal year, whether now might be the time to upgrade the business once again. Based on my own view, I would argue that the former should still apply.

Holding steady despite positive expectations

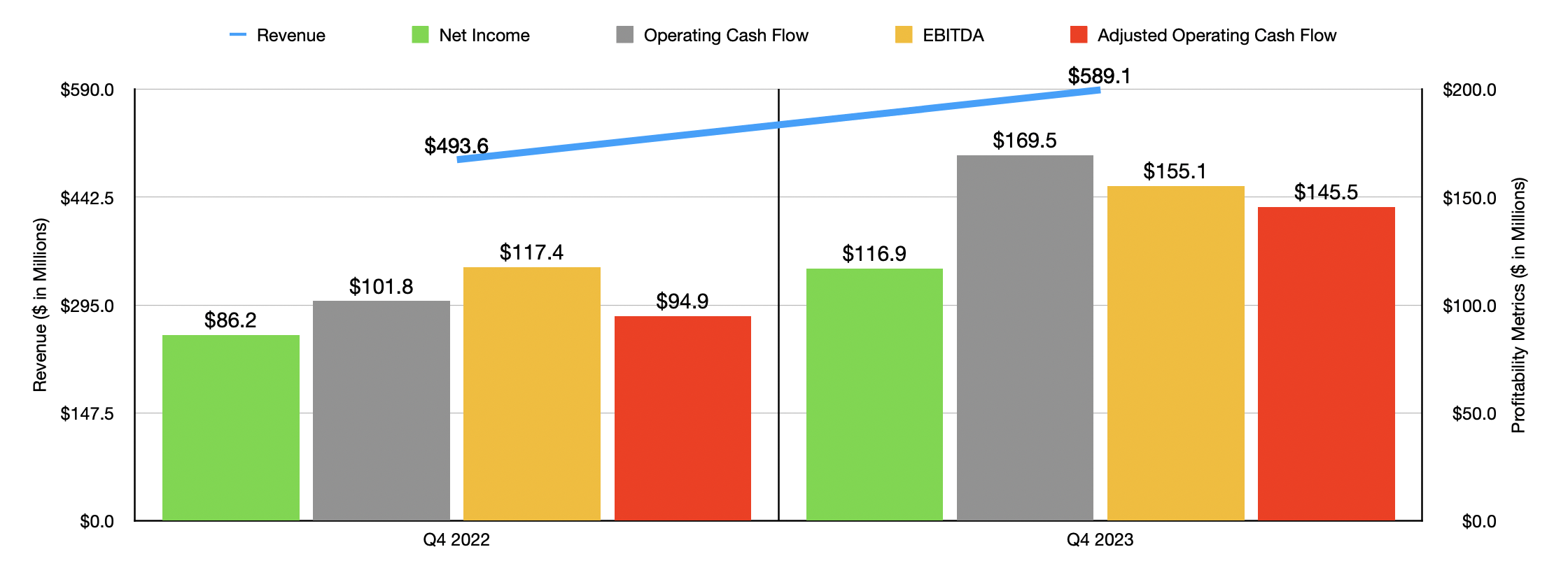

Perhaps the best place to start when it comes to revisiting Gentex would be to cover the financial performance of the company during the most recent quarter for which data is available. That would be the final quarter of the 2023 fiscal year. In that window of time, revenue for the company came in at $589.1 million. That’s 19.3% above the $493.6 million generated only one year earlier. It is worth noting that about $5 million of the amount of revenue generated in the final quarter of 2023 came from one time cost recoveries. So if we exclude this from the equation, revenue would have risen a slightly more modest 18.3%. This growth was driven by a 6% increase in light vehicle production in the primary markets in which the company operates. These markets would be North America, Europe, Japan, and South Korea.

Author – SEC EDGAR Data

On the bottom line, the picture also improved rather nicely. Net income jumped from $86.2 million to $116.9 million. Of course, other profitability metrics performed well also. Operating cash flow, for instance, managed to grow from $101.8 million to $169.5 million. If we adjust for changes in working capital, we get a rise from $94.9 million to $145.5 million. Over the same window of time, EBITDA for the business managed to grow from $117.4 million to $155.1 million. It is worth noting that the increases that the company saw from a profit and cash flow perspective were driven not only by the increase in revenue, but also by an expansion in the firm’s gross profit margin from 31.2% to 34.5%. The aforementioned cost recovery certainly helped. That would have had a 100% profit margin or somewhere off they close to that. However, the company also benefited from price increases that it was able to levy onto its customers. Even given the one-time nature of the cost recovery, management believes that the gross profit margin for the company will improve even more in 2024, coming in at between 35% and 36%.

Author – SEC EDGAR Data

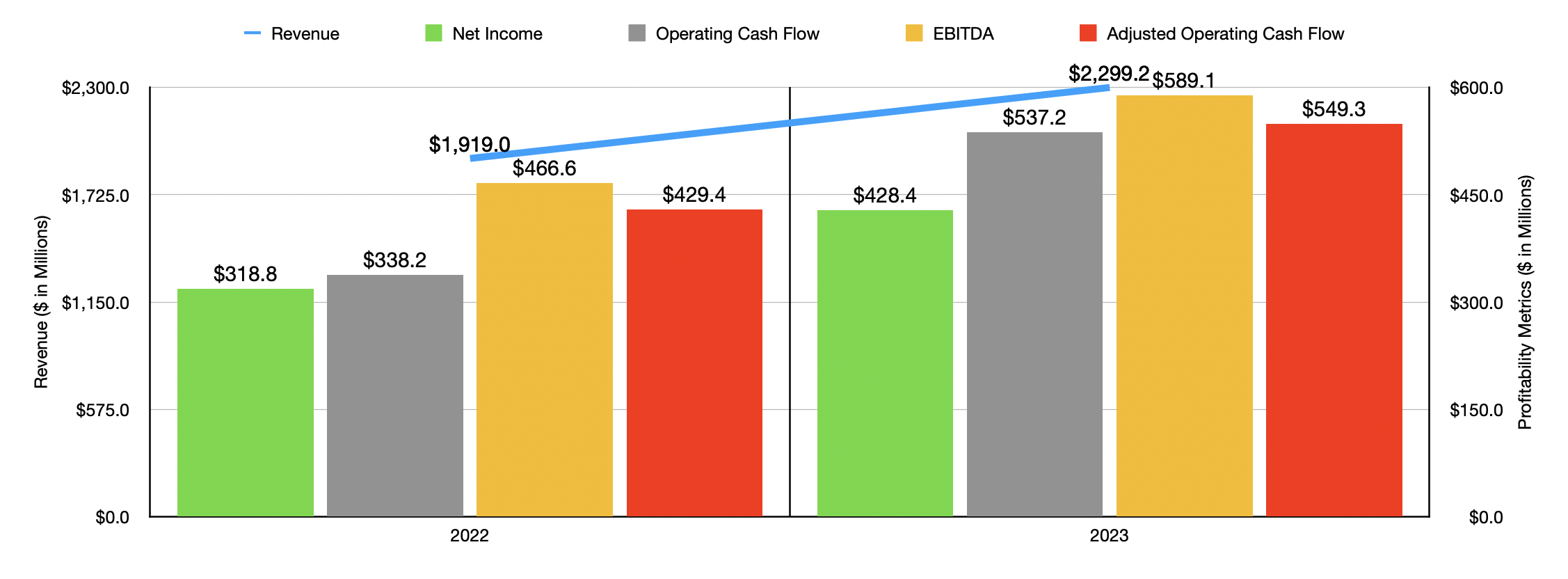

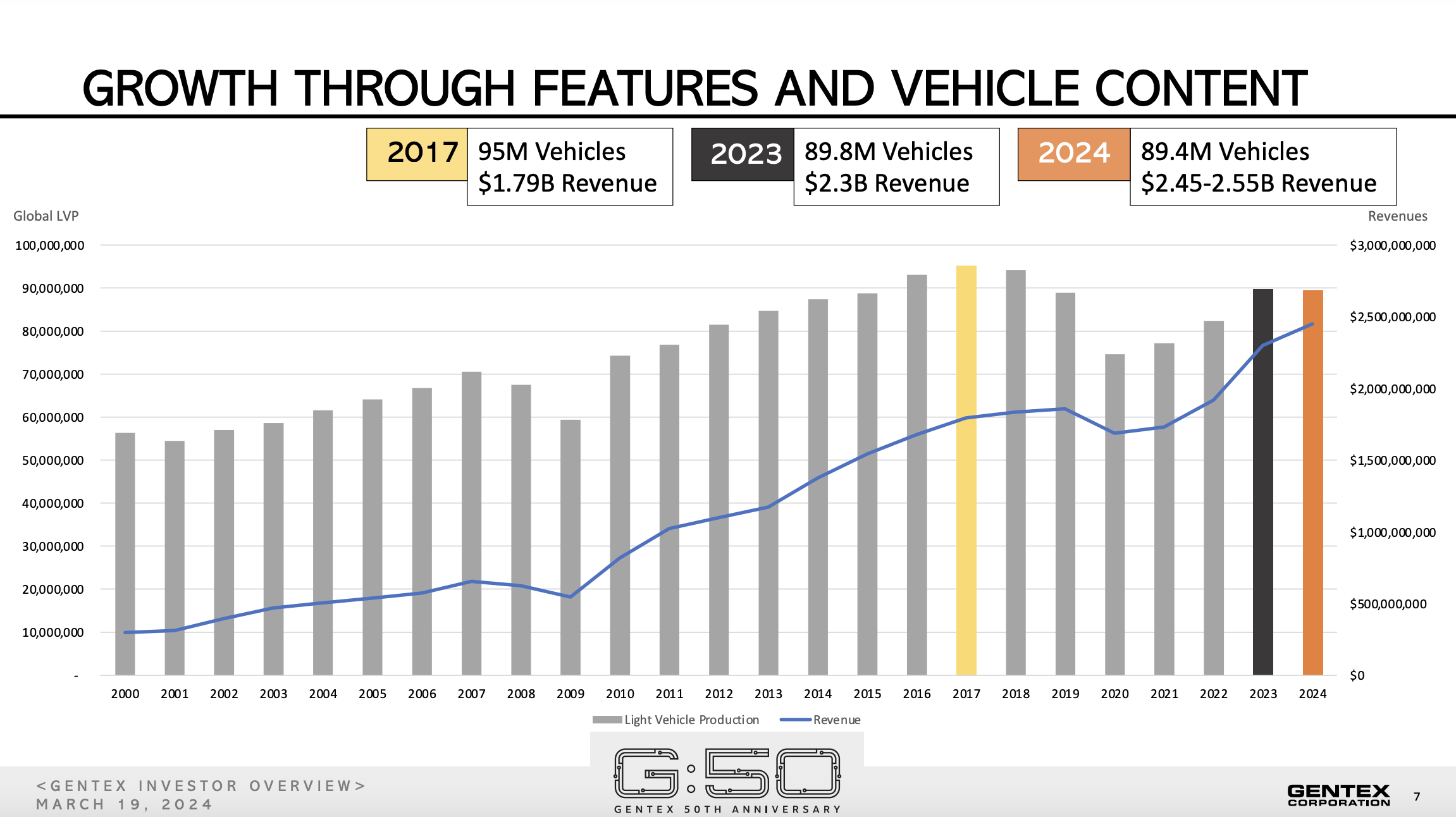

As you can see in the chart above, financial results for 2023 as a whole were rather robust compared to what was seen in 2022. The same factors that helped out during the final quarter of the year were largely helpful for the year in its entirety. However, I would like to talk about some improvements that the business is making. As I mentioned already, management is targeting a gross profit margin this year of between 35% and 36%. For 2023 as a whole, it was about 33.2%. This improvement will likely be driven by further price increases that should push sales higher. Consider, for instance, the revenue picture. Management anticipates sales of between $2.45 billion and $2.55 billion for 2024. At the midpoint, that would be 8.7% above what was seen in 2023. You might normally think that this would be because of an increase in demand. However, due to supply chain issues, a continued chip shortage, labor shortages, and other factors, global light vehicle volumes are expected to be rather low. This year, the company anticipates 89.4 million such vehicles being produced. That’s down from the 89.8 million reported for 2023 and it compares to the 95 million seen back in 2017.

Gentex

When revenue rises because of price increases, profit margins usually expand. This is likely why management is forecasting profits, at the midpoint, of around $466.9 million. That would be up nicely from the $428.4 million reported for 2023. Guidance also seems to be pointing toward adjusted operating cash flow of $587 million and EBITDA of $629.5 million. Management did forecast even further into the future, with revenue expected to rise to between $2.65 billion and $2.75 billion in 2025. But because we don’t know what to expect on the bottom line, I will instead stick to the 2024 fiscal year.

Author – SEC EDGAR Data

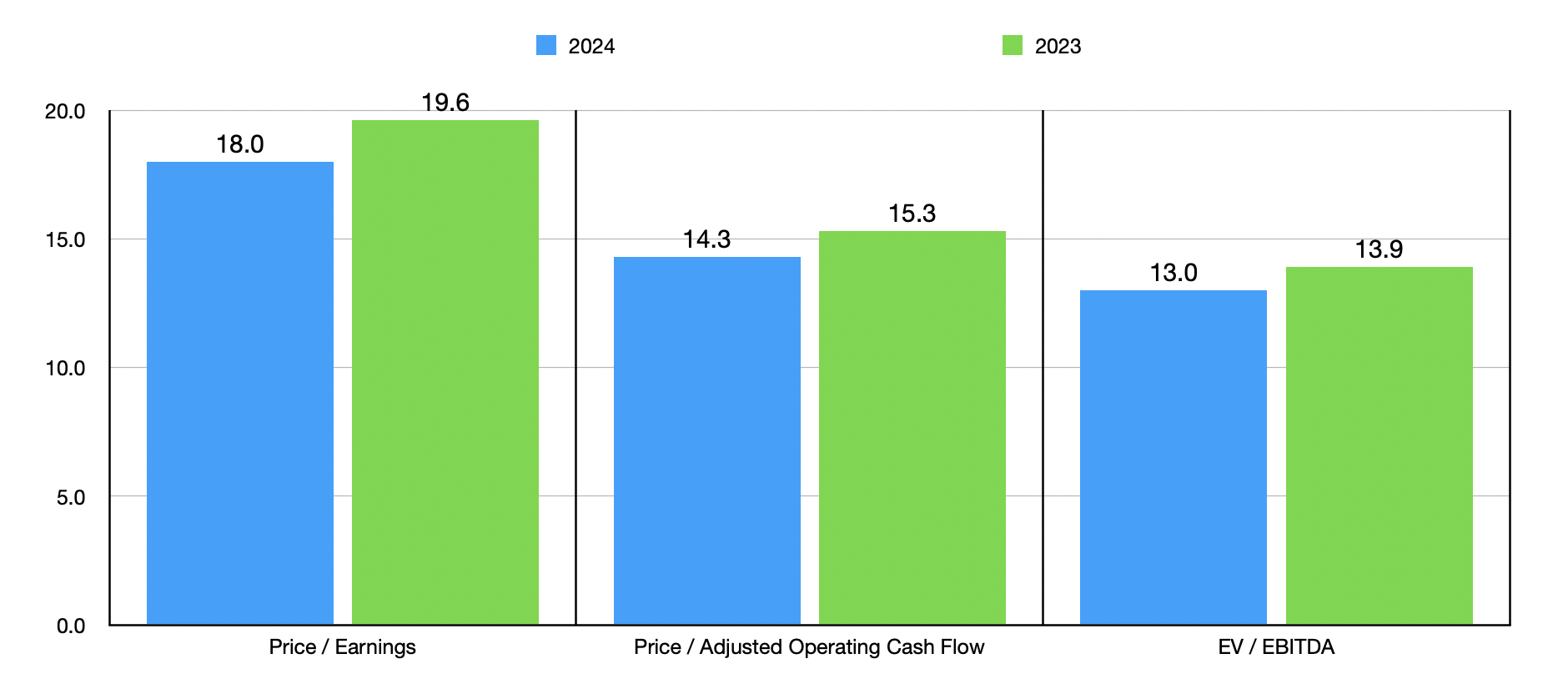

Using the 2024 estimates and the historical results from 2023, I was able to value the company as shown in the chart above. Shares do get cheaper on a forward basis. But I wouldn’t exactly call them cheap. Instead, I would say that we are looking at a firm that is more or less fairly valued. Relative to other firms, however, the stock does look a bit expensive. In the table below, you can see precisely what I mean. On a price to earnings basis, two of the five companies ended up cheaper than Gentex. But this number increases to four of the five when using both the price to operating cash flow approach and the EV to EBITDA approach.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Gentex Corporation | 19.6 | 15.3 | 13.9 |

| Autoliv (ALV) | 21.2 | 10.6 | 10.5 |

| Lear Corp (LEA) | 15.0 | 6.9 | 6.6 |

| Fox Factory Holding Corp (FOXF) | 17.6 | 11.9 | 12.4 |

| Standard Motor Products (SMP) | 21.9 | 5.2 | 6.9 |

| Modine Manufacturing (MOD) | 22.5 | 23.6 | 17.6 |

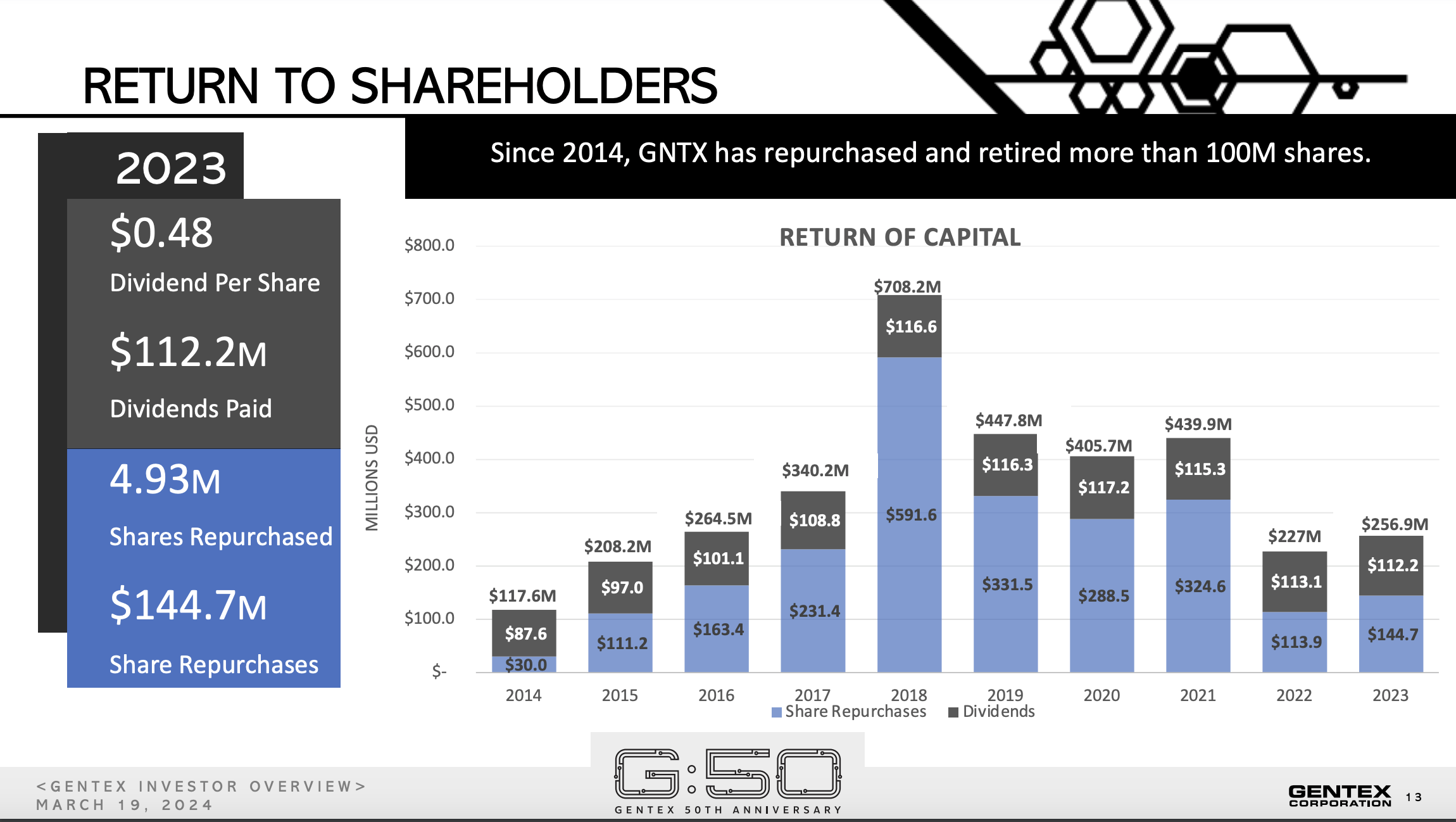

Even though shares are expensive, it doesn’t mean that the company is bad. Already, I pointed out that growth is on the horizon. Of course, growth doesn’t come cheap. Management plans to allocate between $225 million and $250 million toward capital expenditures each year, much of which will go toward growth initiatives. In fact, the firm is completing three new projects, two of which are expansions on existing facilities, this year alone. And between this year and next year, they are opening a childcare facility at another location. This does not mean that the company has ignored returning capital to shareholders. Over the past several years, management has done just that. In 2023 alone, the company spent $112.2 million on dividends, on top of the $144.7 million towards share buybacks. And since at least 2014, there has not been a single year where both dividends and buybacks were ignored.

Gentex

Takeaway

From what I can tell, Gentex is and likely will remain a solid business in the space in which it operates. Management has done a fine job up to this point and shares have deserved a lot of the upside experienced so far. However, all good things must come to an end. And while I will not say that shares are overvalued by any means, they do look pricey relative to similar firms while being more or less fairly valued on an absolute basis. Sure, shares could rise further from here. But as a value investor that prioritizes the existence of a large margin of safety in my investment decisions, I believe that there are better opportunities that can be had today.

Q2 2024 Earnings Call Transcript")