Andrey Semenov

Earnings Preview

No one on Wall Street predicted the meteoric rise of Super Micro Computer (NASDAQ:SMCI) thus far in 2024. Super Micro closed the first day of trading in January of 2023 at $83.86 and closed December 31st, 2023 at $284.26. The stock closed the year up 238.97%.

Little did we all know that this gain would be dwarfed in the beginning months of 2024. The year set off with a bang when Super Micro pre-released earnings on January 18th, showing extremely strong YoY growth and an increase in sales guidance. The stock opened that day at $311 and closed the following day at $423. The company then released official earnings on January 29th and beat the January 18th guidance. The stock closed on January 29th at $495 and ran to $1,004 by February 15th. I subsequently covered this, calling it a stellar report. The stock is up 89% since that article, versus the 6% gain in the S&P.

The stock peaked on March 13th at $1,188 following the March 1st announcement that the company would be added to the S&P 500 in the March 31st rebalancing.

Management then took a strategic move of a public stock offering, utilizing these sky-high prices to raise $1.75b on a stock price of $875, which sent the stock back below $900. The stock is trading around $950 at the time of writing.

What a year it has been so far for Super Micro management and shareholders. Long gone are the days of drastic undervaluation that I discussed in my initial coverage. The stock was trading at $166 at the time and I rated it a Strong Buy, noting that even using absurdly conservative growth metrics (which have been blown out of the water in reality), the stock was underpriced. The market was asleep at the wheel throughout 2023 but woke up in a major way the first quarter of calendar year 2024.

Now the investment case is much more nuanced. Let’s discuss.

Financials

Super Micro posted impressive results in the FY Q2 report in January, highlighted by strong growth across the board:

- Net sales of $3.66 billion versus $2.12 billion in Q1 FY 2024 and $1.80 billion in the same quarter of last year.

- Net income of $296m versus $157m in Q1 FY 2024 and $176 million in the same quarter of last year.

- Diluted EPS of $5.10 versus $2.75 in Q1 FY 2024 and $3.14 in the same quarter of last year.

- Non-GAAP EPS of $5.59 versus $3.43 Q1 FY2024 and $3.26 in the same quarter of last year.

In the upcoming quarter, the company guided for continued growth raising FY 2024 revenue outlook to $14.3b to $14.7b, up from the previous $10b to $11b previous guidance range.

For Q3 FY 2024, the company expects net sales of $3.7b to $4.1b, GAAP EPS of $4.79 to $5.64 and non-GAAP EPS of $5.20 to $6.01. The company’s projections for GAAP and non-GAAP net income per diluted share assume a fully diluted share count of 60.1 million shares for GAAP and fully diluted share count of 61.0 million shares for non-GAAP. This will be closer to 62.1 and 63 million shares due to the recent stock offering. This would translate to GAAP EPS guidance of $4.64 to $5.46 and Non-GAAP to $5.03 to $5.82.

Meanwhile, Wall Street has only been revising EPS and revenue guidance upwards. Wall Street analysts expect Non-GAAP EPS of $5.76 and revenue of $3.94b for the quarter.

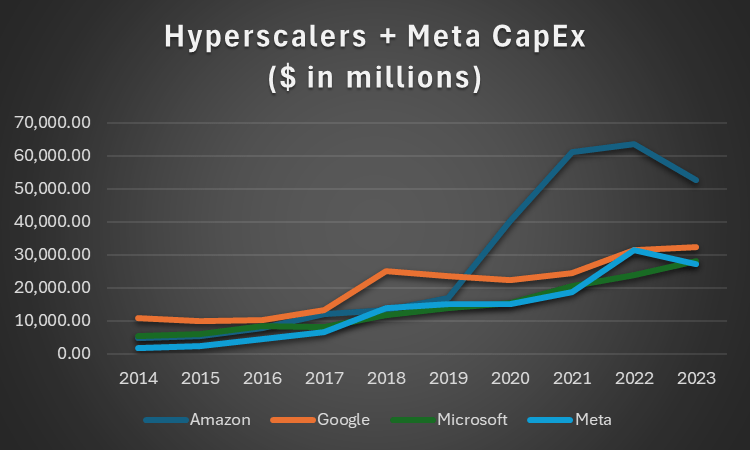

I see no reason why the company guidance and Wall Street estimates will be missed. End market demand has shown no signs of stopping, with hyperscaler cloud service providers continuing strong CapEx spend. Meta (META), Super Micro’s largest customer, also follows this CapEx trend and CEO Mark Zuckerberg commented earlier this year that the company will be a major buyer of Nvidia (NVDA) H100 GPUs.

Analyst’s Creation, Company Reports

Purchases of H100’s were hamstrung in 2023 by a shortage caused by Taiwan Semiconductor Manufacturing Company’s (TSM) CoWoS packaging process. I discuss this in detail in a previous article. TSMC has expanded CoWoS capacity significantly in 2024, so there’s some likelihood that the strong 2023 revenue growth of SMCI and Nvidia (NVDA) will be overshadowed by even stronger growth in 2024. There could still be latent demand from the 2023 shortage. Further, Nvidia’s recent release of the next-gen B100 GPU could stoke further demand.

There is risk in the Osborne effect rearing its head though. This could erode current H100 demand as CSP’s opt to wait for B100 commercialization and could harm Super Micro in the short run. This is not a long-term threat though, as the sales would simply shift out a few quarters until the B100 is ready for shipment.

Given the company’s recent performance, I believe they will provide results in line with expectations and reiterate FY 2024 revenue guidance of just under $15b.

Valuation

Super Micro’s forward PE of 43 is materially above its 5-year average 13, but the 0.87 PEG suggests slight undervaluation considering growth prospects. Therefore, management’s guidance of future growth will significantly impact the stock’s reaction.

Assuming net margin remains consistent at about 9%, the lower end of Super Micro’s revenue target of $14.3b yields an estimated net income of $1.27b. My valuation model is a bit more conservative, estimating $991m of net income for FY 2024. The company experienced gross margin erosion in the recent quarter due to the rapid expansion in customer base, so net margin could also erode in the coming quarters. It’s likely that the company received larger orders and offered better prices to attract customers, which pressured margins.

Regardless, using this conservative starting base of $991m FY 2024 net income and modeling for 15% earnings CAGR through 2033 and 2% annualized stock outstanding growth (~78m shares outstanding in 2033) the stock is worth about $1100-$1150 using a terminal PE of 20. I discounted future cashflows at 5%.

The 5-year historical average PE is 16.77, so I believe a terminal multiple of 20 is fair considering we are entering a higher growth era fueled by AI spend. Accordingly, I believe the stock is trading slightly below its fair value, but this is assuming that management’s ambitious growth targets are attainable.

This is a somewhat conservative model. It is possible earnings will grow above a 15% CAGR, so using a 20% CAGR instead (all other assumptions the same), the stock is worth upwards of $1,500. Still, from a starting base around the current $950 price range, this suggests lackluster performance over a 10-year time frame. Growing from $950 to $1,500 over 10 years represents a return of below 5% annually.

I believe caution is warranted. The stock is extremely volatile and the semiconductor industry is very cyclical. Although Super Micro is growing rapidly now, there’s no certainty this growth is sustainable. More risk-loving investors could see opportunity, but cautious investors may find it wise not to chase the stock. Even a minor miss on guidance or earnings in the coming quarters could send the stock back down to the mid-hundreds.

I suggest looking for a price closer to the $800 range before considering a position. Granted, if the company comes out and beats estimates this quarter or raises guidance, my target price will increase. I will pin a comment to this article following the earnings call with an updated price target based on the results.

What to watch for: Super Micro 4.0

The most important discussion to monitor in the upcoming call is any comments on Super Micro 4.0. For context into this discussion, I suggest reviewing my prior articles.

In my initial article, I discussed Super Micro’s business model and demand drivers. It details what I believe to be the core of Super Micro’s competitive advantage: fast time to market, high flexibility in configurations, and industry leading total cost of ownership.

Next, I reviewed Super Micro’s position in the wider server OEM industry. I presented a comparative analysis of Super Micro against the two industry leaders Dell (DELL) and HP (HPE) and gave a more macro focused viewpoint. I discussed the advantage of being a white-box server provider (offering industry standard rather than proprietary components) and end-market growth trends.

In my recent earnings review I highlighted the company’s evolution from Super Micro 1.0 to Super Micro 3.0. CEO Charles Liang mentioned the next phase of this evolution in the call, stating that the team is working on the Super Micro 4.0 strategy.

The company dubs Super Micro 3.0 as “Total IT Solutions”. This means server racks, networking, and software support for customers. The next leg of growth will be dictated by the shift to Super Micro 4.0.

For a while, I believed this was a shift to AI-enabled consumer electronics. This thought has changed.

I believe Super Micro 4.0 will be a shift from server racks to rack clusters. Shortly after Nvidia’s announcement of the Blackwell architecture, Super Micro announced a host of new products using B100 and related configurations. Included in this is a new class of products for the company: the Generative AI SuperCluster.

If you visit Super Micro’s website today, the very first thing you see is this:

supermicro.com

The company is marketing the SuperCluster front and center on its website leading up to the earnings call.

Super Micro could move further up the value chain by selling clusters of server racks networked together. These will command higher prices, especially when sold with liquid cooling capabilities. Leading edge GPU’s capable of running AI at scale require more power than ever, and Blackwell will continue this trend. With more power comes more heat. Air cooling is sufficient with current server configurations, but the path is leading increasingly to liquid cooling. Nvidia all but confirmed this in the recent GTC conference with its mention of Vertiv Holdings Co. (VRT), a leader in liquid cooling technology.

I believe Super Micro 4.0 will be a strategic shift from a simple server OEM to a partner in data center infrastructure design. They can provide entire server clusters of AI-enabled racks and help data center operators with floorplans, installation, and ongoing maintenance of the systems. In the age of AI, data center operators are met with increasingly complex floor planning decisions between legacy CPU servers and AI-enabled GPU servers.

Super Micro 4.0 could be the shift from Total IT Solutions to Complete Data Center Partner.

Investor Takeaway

While Super Micro has had an astounding run year-to-date, there still looks to be plenty of growth left in the tank. Despite the positive growth outlook though, caution is warranted as much of this growth is priced into the stock. I believe the company will meet analyst estimates in the upcoming call, so future guidance will be a key takeaway for me.

Finally, more detail on the Super Micro 4.0 strategic shift commands utmost attention from investors. If my speculation is correct and Super Micro is moving more toward server clusters, it would be very bullish for the company long-term. Liquid cooled server clusters will command much higher average selling prices and Super Micro could turbocharge its next leg of growth as a result.

I rate SMCI a Hold at current prices because I find it unwise to sell a company with such compelling growth prospects, but also believe caution is warranted with a stock that has the valuation that SMCI has.

Q2 2024 Earnings Call Transcript")