bopav

Introduction

In my quest to find income funds that focus on asymmetric risk and reward situations, I stumbled upon the Defiance NASDAQ 100 Enhanced Options Income ETF (NASDAQ:QQQY). I covered its first 60 days back in November 2023.

This article will serve as a follow-up to my previous conclusion, which was:

I will try to cover QQQY again…to see how the strategy changes and evolves…Until then, I have to rate the fund a hold as I don’t believe we have the data to say how this investment will act and I don’t see it having a place in my income portfolio currently.

Six months later, now April 2024, we have more data. Let’s take a look again at QQQY and see if it can show its strengths.

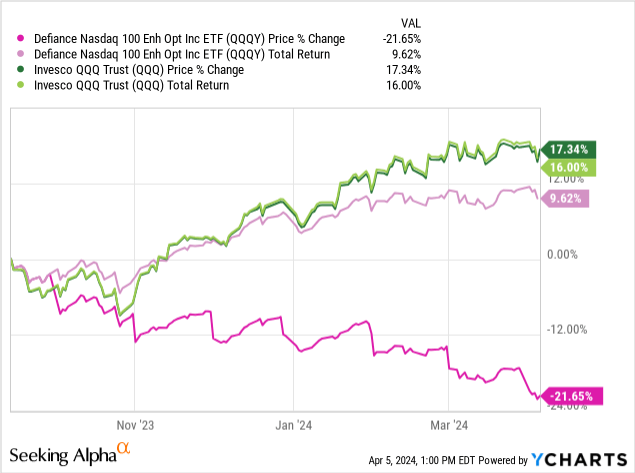

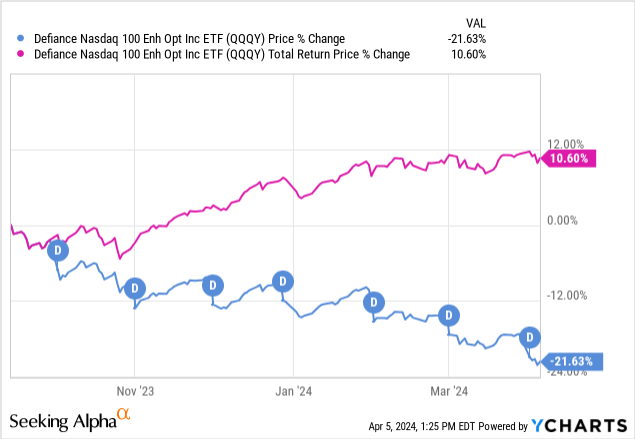

Here are the price and total returns for both QQQY and its underlying index, QQQ.

Overview

QQQY is unique in its offering among options-selling ETFs, as it seeks to sell 0DTE ITM put options. For those not in the know, this means that the fund writes options against QQQ expiring the same day they are written, and they are written at strikes that are likely to be exercised at expiration.

Typical options-based ETFs sell calls against their holdings, which come with very different P/L possibilities and risk profiles.

Because the ETF is writing options, it can secure its options with margin. This allows the cash in the portfolio to be deployed into bonds and assets with positive yields to help the overall yield.

Defiance offers an explanation of their strategy as well.

QQQY aims to achieve consistent and outsized monthly yield distributions for investors coupled with equity market exposure to the Nasdaq-100. QQQY is an actively managed exchange-traded fund (“ETF”) that seeks enhanced income, constructed of treasuries and Nasdaq-100 index options. The strategy’s objective is to generate outsized monthly distributions by selling option premium on a daily basis. The fund uses daily options to realize rapid time decay by selling in the money puts with 0DTE.

The Fund’s primary investment objective is to seek current income. The Fund’s secondary investment objective is to seek exposure to the performance of the Nasdaq 100 Index (the “Index”) subject to a limit on potential investment gains.

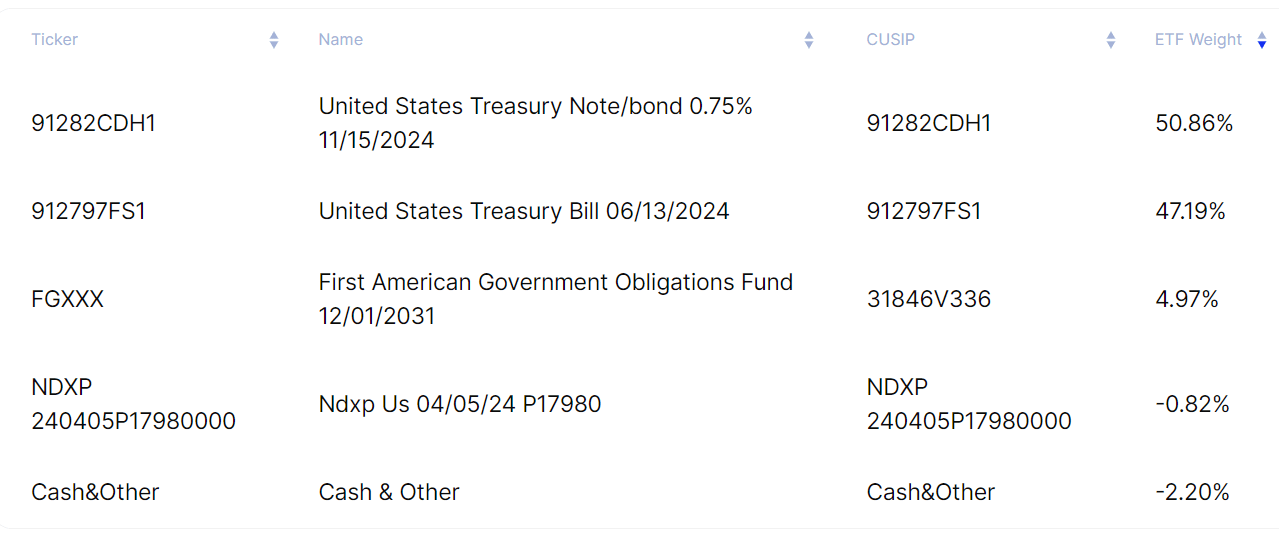

Check out QQQY’s current holdings here, as they change daily. Depending on when you read this, the options may look radically different.

Figure 1 (Defiance ETFs)

Those who read my first article will note that the fund has now deployed all of its cash, going from 29% cash in November to a negative cash balance now.

This is a good sign for the ETF, as it means that it has no “spun up” its operations and have fully deployed their cash into treasuries and a money-market fund that acts as their liquid capital to close trades with.

The yields on the treasury notes are low because they were purchased at a steep discount, allowing them to be sold for a capital gain instead of taking most of the gain in the form of dividend income. This allows the fund to primarily distribute its options income instead of UST distributions.

Distributions

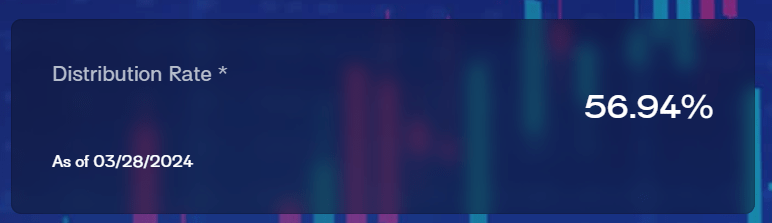

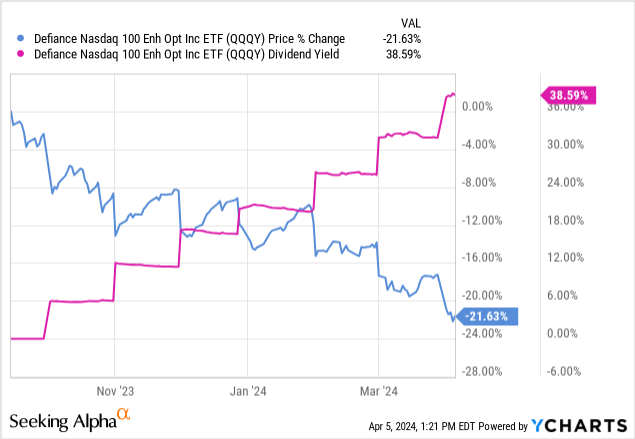

QQQY has been keeping an eye-watering distribution rate going for some time now, far longer than I would’ve expected a fund to make it distributing over 50%.

Figure 2 (Defiance ETFs)

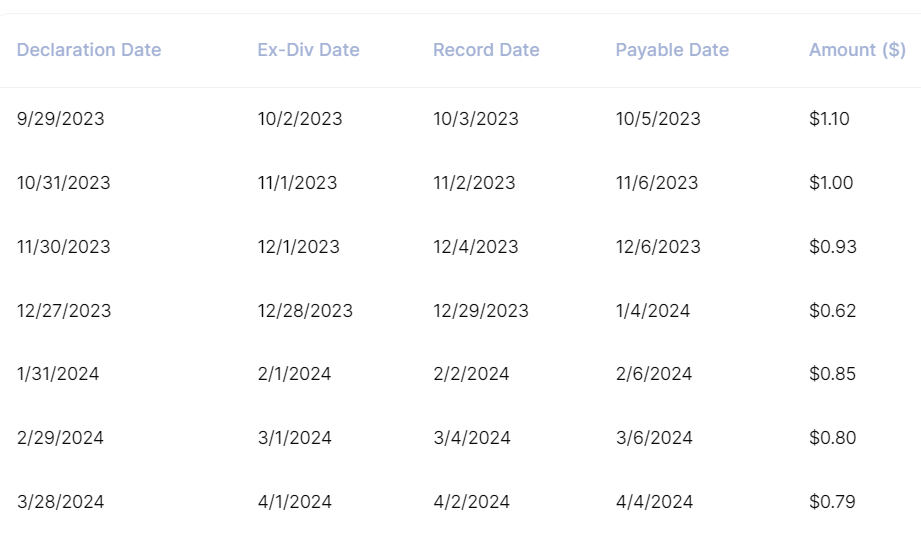

The distributions themselves have been on a decline, but since the price is falling, the rate stays high.

Figure 3 (Defiance ETFs)

When I wrote my original article on QQQY in November, the distribution was $0.93 and the market price was $18.50 at the time of publication. This meant a yield close to 65% if that had kept up.

Now, with a market price of $15.75 and the most recent distribution at $0.79, investors are still looking at a yield around 60%.

However, if you bought after my last article and are still holding, your cost would be $18.50 and the most recent distribution is $0.79, your yield is more like 51%.

This decline in distribution size has led to a much lower trailing yield (“TTM”), which is now sitting at around 38.5%.

This yield is still insane to me, but is far more in line with what I expected from this fund: it will keep its current distribution yield high by eroding the price of the fund.

This has led to investors from inception receiving a total return of 10.60% while the fund’s price dove 21.63%.

Note: the “D” symbols in the chart are when dividends were paid out.

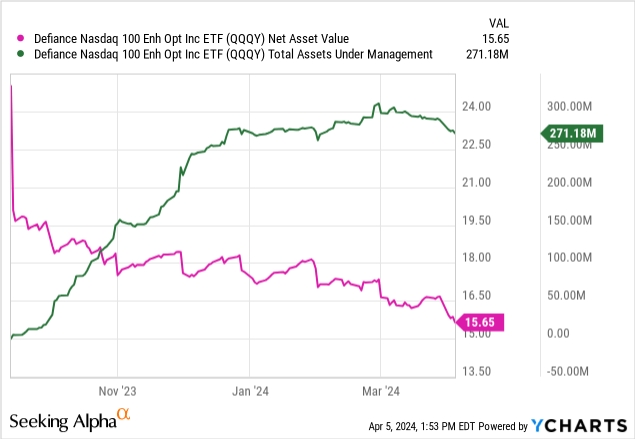

As you can see, the fund is distributing more than it earns from its options sales, as it is consistently declining in NAV even as AUM increases.

This overdistribution is a huge risk to the fund, which could slowly dwindle its way down to nothing while still maintaining their best marketing tactic: presenting a 50%+ distribution yield.

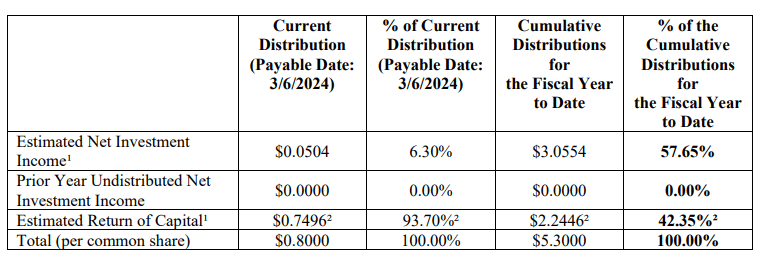

This NAV destruction is being transferred back to investors via return of capital (“RoC”) and unlike some RoC, which can be fancy accounting done on the manager’s part and is temporary, QQQY consistently sees 30-50% of its distributions given out at RoC.

Figure 4 (Defiance ETFs)

Market Risk

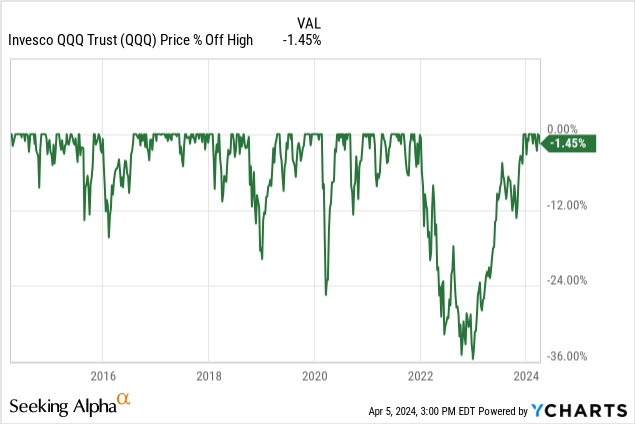

Due to the nature of 0DTE puts, the fund’s largest risk is a sudden and dramatic fall in the underlying index, the NASDAQ 100.

That has happened from time to time, but not during a time that QQQY has been around. This means that this risk is yet to be realized, and the damage it could do to QQQY is unknown.

While you can see that the index has always made it back from these drawdowns, QQQY does not capture the same upside as QQQ. It may not return to its highs after losing during sharp, sudden drawdowns because of the nature of put options.

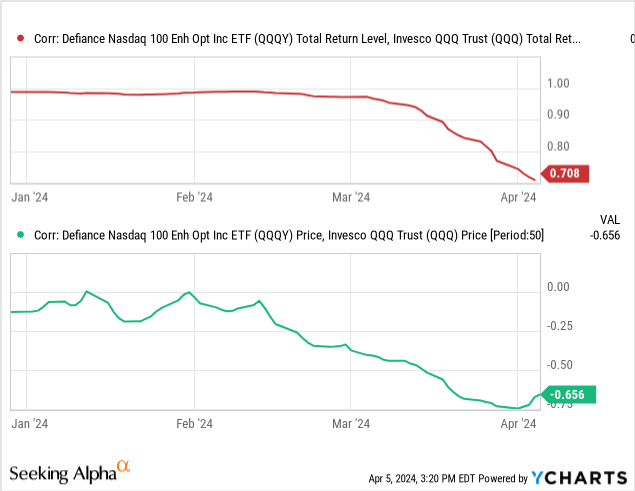

QQQY carries a fairly close correlation to QQQ on its daily returns.

QQQY changes its positions during market hours, so their exposure is constantly changing and it is impossible to predict how those historical crashes would have affected QQQY.

This risk of the unknown is not new to investing, and QQQ suffers from the same fate.

That being said, options, and especially 0DTE options; are leveraged instruments that can incur losses exceeding those of the underlying. If QQQ falls, QQQY could fall faster.

This is why there is such a discrepancy between the correlation on price and total return. The total return carries an almost 1:1 correlation, with a recent dip due to the un-paid dividend coming up for April. However, the price carries a neutral to sometimes negative correlation at times.

This may be due to leveraged losses, or intra-day losses realized before new positions are taken.

Performance

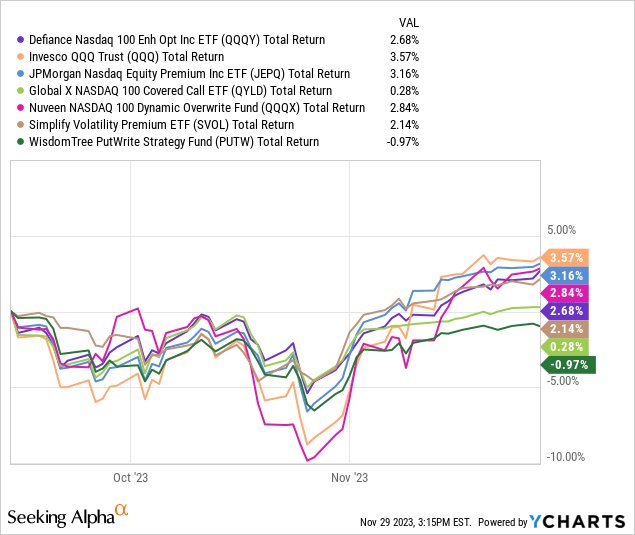

Back in November, I compared QQQY to several other similar ETFs. I want to bring them back again to see how things have changed. Here is the total return chart from my previous article, to give new readers some reference.

Figure 5 (YCharts)

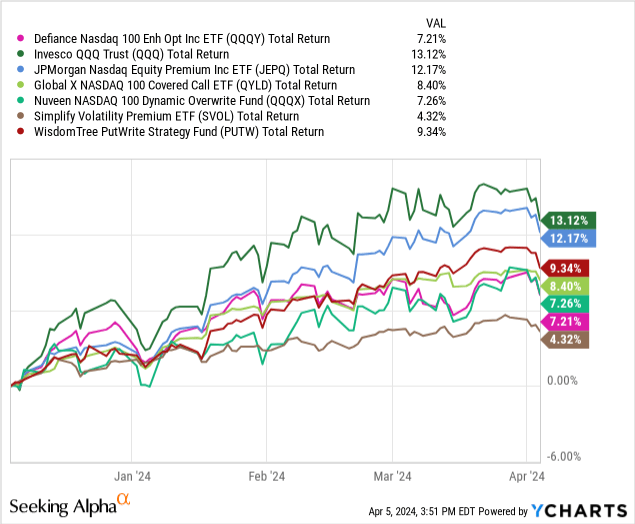

So how has this changed? This next chart starts when that one ends.

Note: the colors of each security has changed to conform to this article’s color coding.

In the last data set, the benchmark (QQQ) beat out all of the other funds in total return, and it still is. After-tax returns would make an even larger difference, as most of these funds distribute a large amount of their gains as dividends, whereas QQQ’s primary source of return is capital gains.

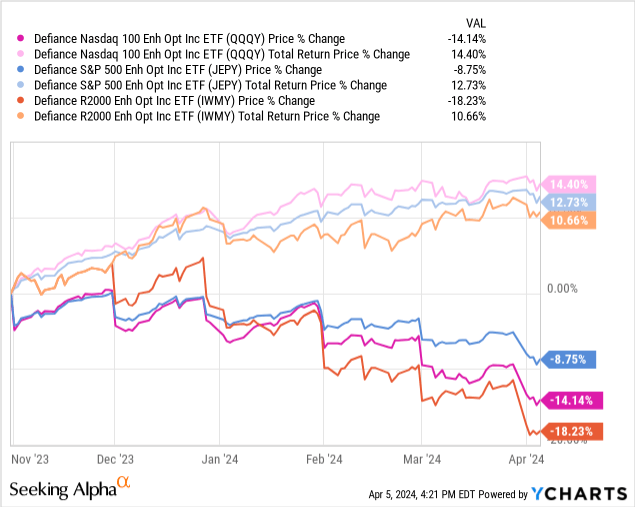

The next question is, how has it performed against its sister funds that track other indices like the S&P 500 and the Russell 2000?

Between the three of Defiance’s funds, QQQY has performed the best. This may be due to excess volatility in the NASDAQ 100 against the S&P 500 and the Russell 2000, but due to intra-day activity, it’s unclear exactly why the performance is the way it is. This excess volatility may not apply to the index itself, but specifically the strikes that the managers selected for the daily options.

Conclusion

The Defiance NASDAQ Enhanced Income ETF (QQQY) is still a hold from me, as it has yet to truly impress me with returns and it carries significant risks that have never been fully tested.

Without knowing how QQQY may respond to a black-swan-like crash, the fund carries far too much risk of sudden implosion. Think of it this way: I would not want to wear a bulletproof vest that had never been shot at before, even if the manufacturer swears that it really is bulletproof.

For now, the fund is eating at its NAV and AUM has levelled out. This combination does not bode well for QQQY’s future. I will be waiting and watching to see how things change. If we see QQQY really test its metal, and I feel safe enough to include it in my income portfolio, I will write another update.

Until that happens, there doesn’t seem to be enough of a bullish argument for its inclusion.

Thanks for reading.

Q2 2024 Earnings Call Transcript")