We Are/DigitalVision via Getty Images

STAAR Surgical overview

April 4th ended up being a really fantastic day for shareholders of STAAR Surgical Company (NASDAQ:STAA). For those not aware, the company focuses on the production of implantable lenses for the eye, as well as delivery systems that are used to put those lenses in place. It makes other products as well, such as intraocular lenses and silicone lens based preloaded injectors. This is an interesting business operating in an interesting space. And those who own shares just got a nice bump higher. That’s because, after announcing preliminary sales for the first quarter of the 2024 fiscal year, the stock shot up, closing higher by 16.5%.

I hate to be the bearer of bad news, but my own view is that this is insufficient in order to justify owning units. It is great to see management report higher than expected revenue. In the long run, the company probably will do reasonably well. Having said that, shares remain very expensive. This is not the first time I have made this call. The last article that I published about the company came out in August of 2023. In that article, I called the company an eyesore. That play on words was inspired by just how expensive the stock was. And this was in spite of continued revenue growth.

You would think that, given this massive amount of upside, that shares would be proving me wrong. But that couldn’t be further from the truth. Even with this upside, shares are only up 4.6% since I rated it a ‘sell’ last year. That compares to the 15.6% rise seen by the S&P 500 over the same window of time. And since I first rated the company a ‘sell’ back in February of 2022, shares are still down 39.2% compared to the 15.5% upside seen by the broader market. Although the company continues to expand, it does struggle on the bottom line. Furthermore, shares are not only expensive on an absolute basis. They are also expensive relative to similar firms. Given these factors, I believe that the ‘sell’ rating I assigned the stock previously should still hold.

An early look

The 16.5% surge in share price that STAAR Surgical experienced on April 4th was driven by a press release that management came out with that covers preliminary net sales for the first quarter of the company’s 2024 fiscal year. According to management, revenue for that quarter should be in excess of $77 million. To put this in perspective, revenue in the first quarter of the 2023 fiscal year was $73.5 million. So this implies upside of at least 4.7%. It’s also important to note that this is well above the $72.6 million in revenue that analysts had been forecasting.

Although still only a small part of overall sales, the company’s ICL offering in the US is something that management is very excited about. According to the press release, sales for this offering should be around $5 million for the quarter. That’s 20% higher than it was one year earlier. In the EMEA (Europe, Middle East, and Africa) regions, revenue for this product line we’re up 11% year over year, while in the Asia Pacific region they were up about 9%. In China specifically, the company is looking at 10% growth. This is definitely encouraging.

Beyond this, management has not provided all that much in the way of detail. They did say that the increase in sales has caused them to re-evaluate revenue forecasts for 2024 as a whole. They believe that overall sales will be at the higher end of the previously announced range of $335 million to $340 million. Cash and cash equivalents, as well as investments that are available for sale, should come in at around $248 million. This compares to the $232.4 million reported one year earlier. Though it is worth noting that accounts receivable is expected to have dropped from $94.7 million to $70 million. Overall, these results are quite positive and I understand the bullishness with which shares were treated.

Author – SEC EDGAR Data

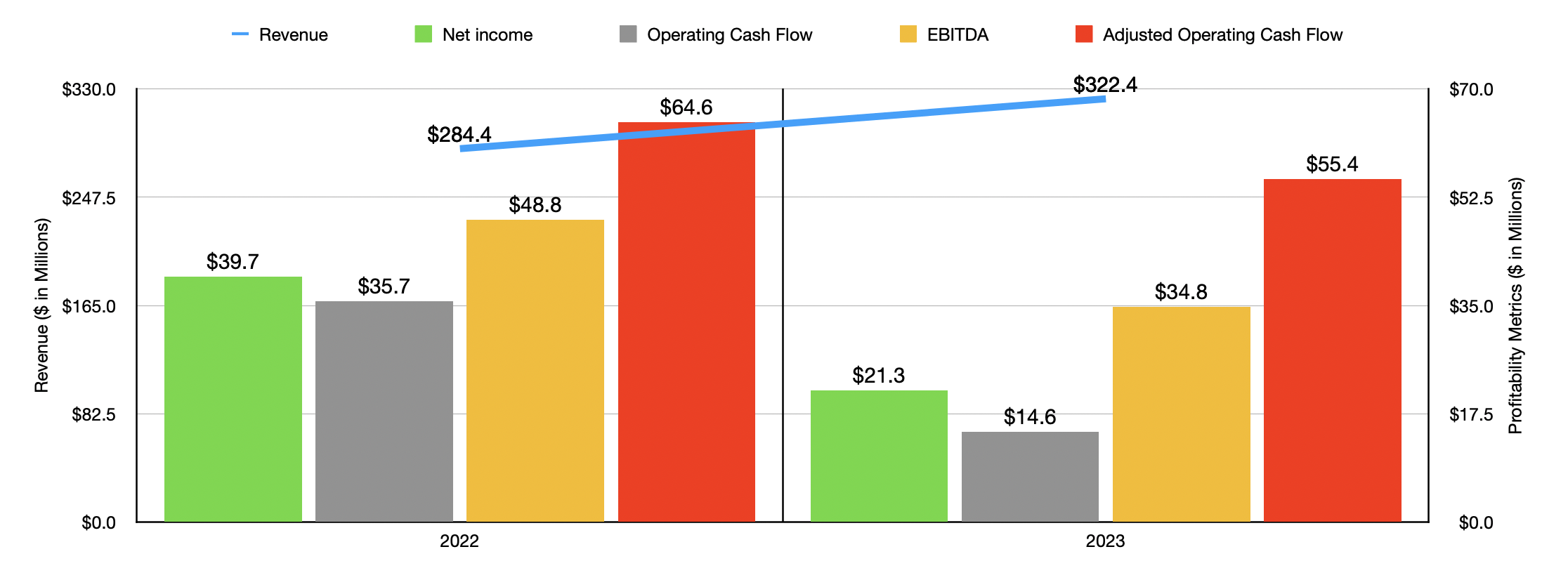

Unfortunately, I am not terribly optimistic about the company’s prospects in the near term. To see why, we need only look at results covering 2023 relative to 2022. On the positive side, revenue totaled $322.4 million last year. That’s 13.4% above the $284.4 million reported one year earlier. All of the company’s growth, and then some, from 2022 to 2023, came from its ICL offerings. Revenue jumped from $269.7 million to $319.4 million. This increase of 18.4% was fueled by a 19% surge in unit growth. The company benefited from a 21% surge in revenue associated with the Asia Pacific region as unit growth jumped by 22%. China was a particularly bright spot there, with revenue surging 25% compared to the 14% seen in India, the 11% seen in Japan, and the 11% seen in Korea. The EMEA regions saw a more modest 7% rise in revenue during this window of time. In the Americas, revenue is up roughly 11%. The US specifically saw a 9% rise in unit growth, while in Canada that number was 14%.

So far, all of this looks positive. However, the company has been facing some issues regarding profits and cash flows. Net income was cut by nearly half, plunging from $39.7 million in 2022 to $21.3 million last year. An increase in the firm’s general and administrative costs from 19.2% of sales to 22.4% of sales contributed to this, with increased salary and payroll tax expenses, outside services fees, facilities costs, and a variety of other factors, all negatively impacting returns. Selling and marketing expenses, meanwhile, went from 31.2% of sales to 33.4%. This was mostly due to higher advertising and promotional activities, as well as compensation associated with these actions. It is important to note that not all cost increases are negative. Research and development costs, for instance, jumped from 12.7% of sales to 13.8%. But in my view, this is understandable since the company is almost certainly continuing to develop new products while perfecting existing ones. In a sense, this is an investment in itself and its future.

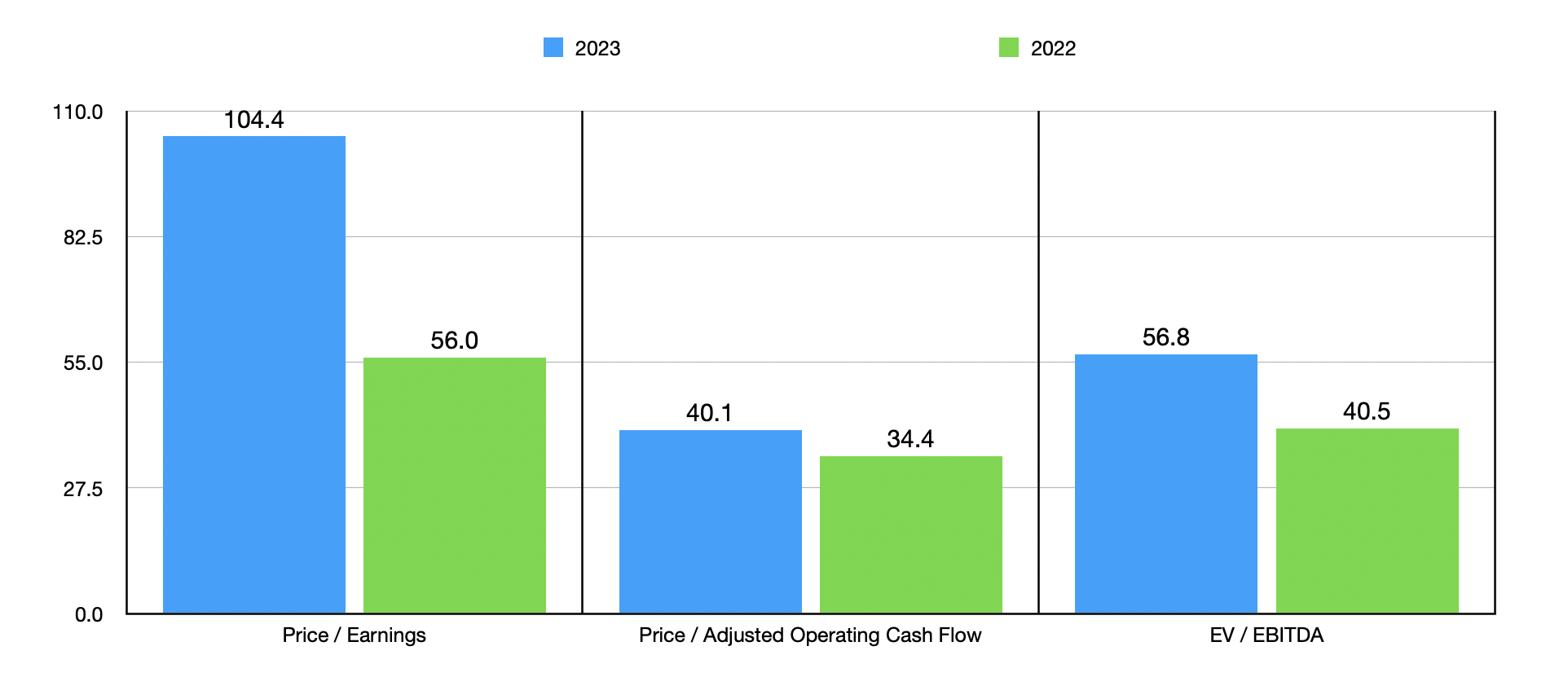

Unfortunately, other profitability metrics followed a very similar trajectory. Operating cash flow plunged from $35.7 million to $14.6 million. Even if we adjust for changes in working capital, we get a decline from $64.6 million to $55.4 million. Meanwhile, EBITDA for the company managed to fall from $48.8 million to $34.8 million. Although management provided guidance from a sales perspective for 2024, given how early it is in 2023, we really should focus on financial results for that year. In the chart below, you can see how I valued the company using data from 2023, as well as from 2022.

Author – SEC EDGAR Data

On an absolute basis, shares do look very pricey. This is true even if we use the more generous 2022 figures. But it’s not just about being pricey on an absolute basis. We also need to see how the stock compares to similar enterprises. In the table below, you can see just this for five firms. When it comes to the price to earnings approach, I found that four of the five companies ended up being cheaper than STAAR Surgical. The same holds true when using the price to operating cash flow approach. Meanwhile, when it comes to the EV to EBITDA approach, our candidate ended up being the most expensive of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| STAAR Surgical Company | 104.4 | 40.1 | 56.8 |

| UFP Technologies (UFPT) | 42.9 | 46.7 | 27.9 |

| Embecta Corp. (EMBC) | 13.4 | 16.1 | 9.8 |

| Avanos Medical (AVNS) | 27.0 | 28.3 | 16.0 |

| Neogen Corp (NEOG) | 252.3 | 27.1 | 19.8 |

| Merit Medical Systems (MMSI) | 44.1 | 28.9 | 19.5 |

Takeaway

As much as I like STAAR Surgical from an operational perspective and I find what it is working on to be fascinating, I do not believe that shares are attractively priced at this point in time. The higher-than-expected revenue does suggest that the long-term outlook for the company could probably be quite positive. But as an investor, it’s imperative not to overpay for growth. If revenue is expanding more rapidly and the bottom line for the company was improving at a nice clip, the story might be different. If you add on to this a scenario where shares should be trading at a discount to similar firms, I could see myself being rather bullish. But that’s not the case here. The fact that it’s the opposite leads me to keep the business rated a ‘sell’ for now.

Q2 2024 Earnings Call Transcript")