AaronAmat/iStock via Getty Images

Investment Thesis

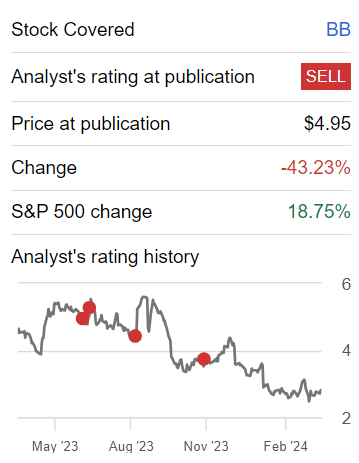

BlackBerry (NYSE:BB) delivered a very mixed set of fiscal Q4 2024 results. Simply put, its guidance is better than what seems on the surface. This is contrary to what many investors have opined.

Nevertheless, despite BlackBerry pointing to some traction in fiscal 2025 (not to be confused with calendar year), I maintain that this stock is a sell.

Rapid Recap

Back in November, I noted in a bearish analysis,

BlackBerry has for a long time been a battleground stock, with passionate bulls and bears both arguing for their side. And for a long while, it succeeded in plowing through.

But I believe that in the past few weeks, we’ve seen two events put in place that signal the beginning of the end for the bull thesis.

I recommend that investors call a day on this investment and salvage their capital.

Author’s work on BB

I’ve been openly bearish on BlackBerry for a long while. As a point of reference, the stock is down approximately 35% (including the premarket jump), while the S&P500 is up more than 18%. And I remain bearish on this stock, even though I do acknowledge some positive unexpected elements in this report.

Why BlackBerry? Why Now?

BlackBerry’s near-term prospects appear promising, particularly in its IoT segment which delivered its best-ever quarter for revenue and achieved strong growth in royalty backlog.

The company’s focus on securing design wins, such as with Hyundai Mobis and leading medical OEMs, underscores its competitive edge.

However, BlackBerry faces challenges in the near term, particularly concerning delays in software-defined vehicle programs, which impact the IoT segment’s growth potential.

Despite achieving record royalty backlog, the sluggishness in launching new software-defined vehicle programs is being reflected in its lackluster growth in this segment (to be discussed further soon).

Additionally, budget constraints among some of the company’s government customers are expected to hinder BlackBerry’s cybersecurity business from flourishing in the near term. However, BlackBerry continues to implement significant cost-saving measures to improve its profitability, which we’ll discuss momentarily.

Indeed, given this background, let’s now delve into its financials.

Guidance Requires Substantial Interpretation

BB revenue growth rates

Even though I’m openly bearish on BB, this doesn’t stop me from pointing out that BlackBerry’s guidance was meaningfully better than many investors on Seeking Alpha and elsewhere have declared.

In my graphic above, I’ve excluded the $218 million patent sales figure for the guidance only. I believe this helps add context. To repeat, the guidance graphic above has not been adjusted for the patent sales in fiscal Q1 2024.

Altogether, looking ahead, this implies that fiscal Q1 2025 is expected to be down about 6%. And perhaps more impressively, the later quarters of fiscal 2025 are expected to deliver some growth.

Furthermore, during the earnings call, some comments lead one to believe that the highly praised IoT segment may ultimately grow by around the mid-single digits. That’s far from solid growth for what is meant to be a coveted unit within BlackBerry, but it’s also far from a dead company walking.

Next, we’ll discuss its valuation.

BB Stock Valuation — 53x Forward EBITDA

As we look ahead, BlackBerry is expected to deliver approximately $10 to 20 million of adjusted EBITDA.

That being said, given that fiscal Q1 2025 is expected to see around negative $10 million of adjusted EBITDA, this implies that once BlackBerry gets over fiscal Q1 2025, there’s the inference that its underlying profitability should improve, with the remainder nine months of fiscal 2025 delivering about $20 million of EBITDA.

Therefore, if all goes well for BlackBerry, this could mean that the company would be on a path to delivering $30 million of EBITDA at some point in fiscal 2025. This leaves BlackBerry with minimal growth priced at 53x EBITDA.

Meanwhile, BlackBerry’s balance sheet now holds about $40 million of net cash. In fact, perhaps the best takeaway from this quarter is the paying down of its debt and the successful raising of $200 million at 3% interest rates.

The Bottom Line

In conclusion, while BlackBerry’s fiscal Q4 2024 results present a mixed picture, with guidance indicating better prospects than initially perceived, I maintain my bearish stance on the stock.

Despite some positive unexpected elements in the report, such as promising near-term prospects in the IoT segment highlighted by its best-ever revenue quarter and strong growth in royalty backlog, significant challenges persist.

However, BlackBerry’s ongoing efforts to implement cost-saving measures and improve profitability offer some hope.

Looking ahead, the guidance requires substantial interpretation, with fiscal 2025 expected to see some possible growth in the later quarters of this fiscal year.

Nonetheless, I maintain that having to pay 53x forward EBITDA for BlackBerry is simply too much.

Q2 2024 Earnings Call Transcript")