alvarez

Intro & Thesis

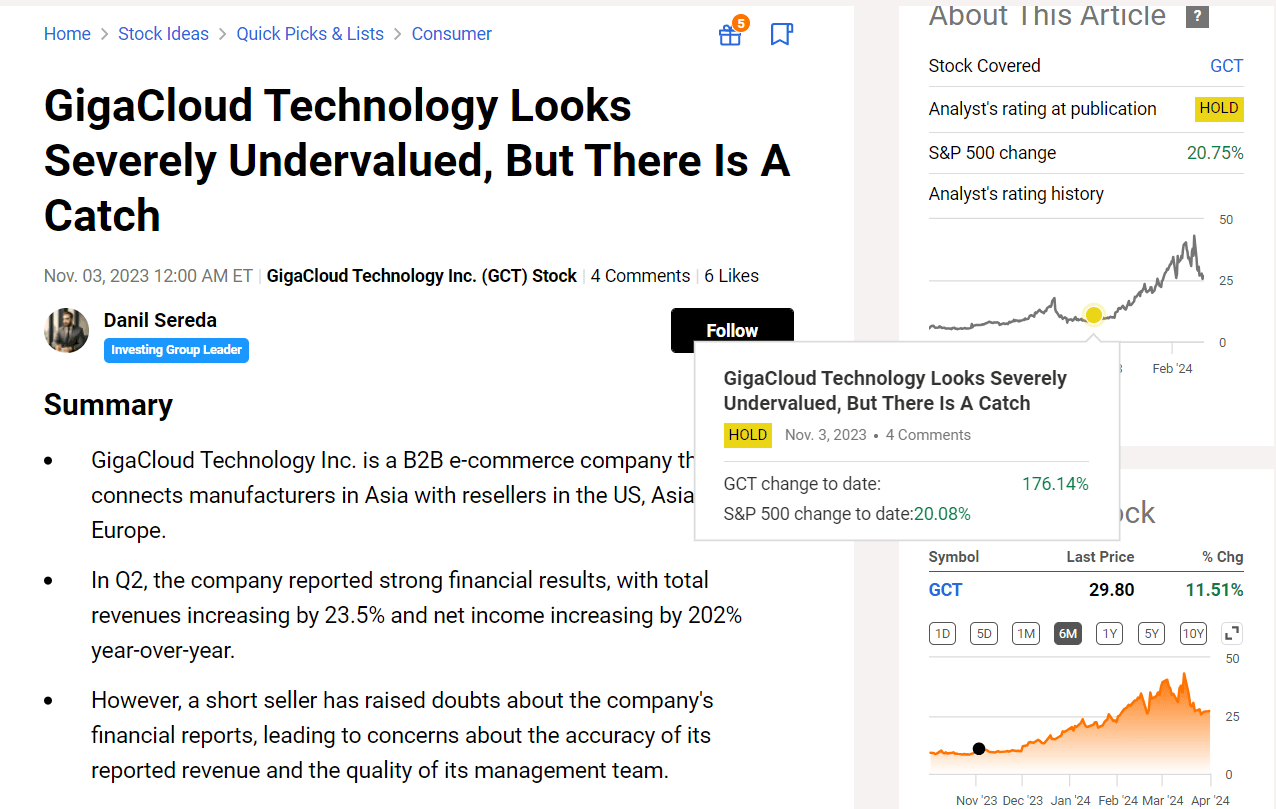

At the beginning of November 2023, I published an article on GigaCloud Technology Inc. (NASDAQ:GCT) stock, in which I concluded that the company looked severely undervalued, but due to surrounding concerns regarding its business practices, I issued a “Hold” rating at the time. My neutral call missed the rally as GCT outperformed the broader market by a factor of ~8.8x:

Seeking Alpha, my coverage of GCT stock

Nevertheless, my updated analysis leads me back to the same conclusion as before: the company’s continued and rapid growth against the backdrop of still low valuation multiples makes GCT look quite undervalued, but what bothers me is that GigaCloud was overdue with the release of its 10-K. In light of the concerns I outlined in my previous article, this fact doesn’t help GCT look like a less risky small-cap after the rapid rally of the last few months.

Why Do I Think So?

Let’s discuss everything in order. According to Seeking Alpha’s description, GigaCloud Technology Inc. is now a $1.2 billion market cap company that provides comprehensive B2B e-commerce solutions for large parcel goods. Their marketplace connects manufacturers in Asia with resellers in the US, Asia, and Europe, facilitating cross-border transactions for items such as furniture, home appliances, and fitness equipment.

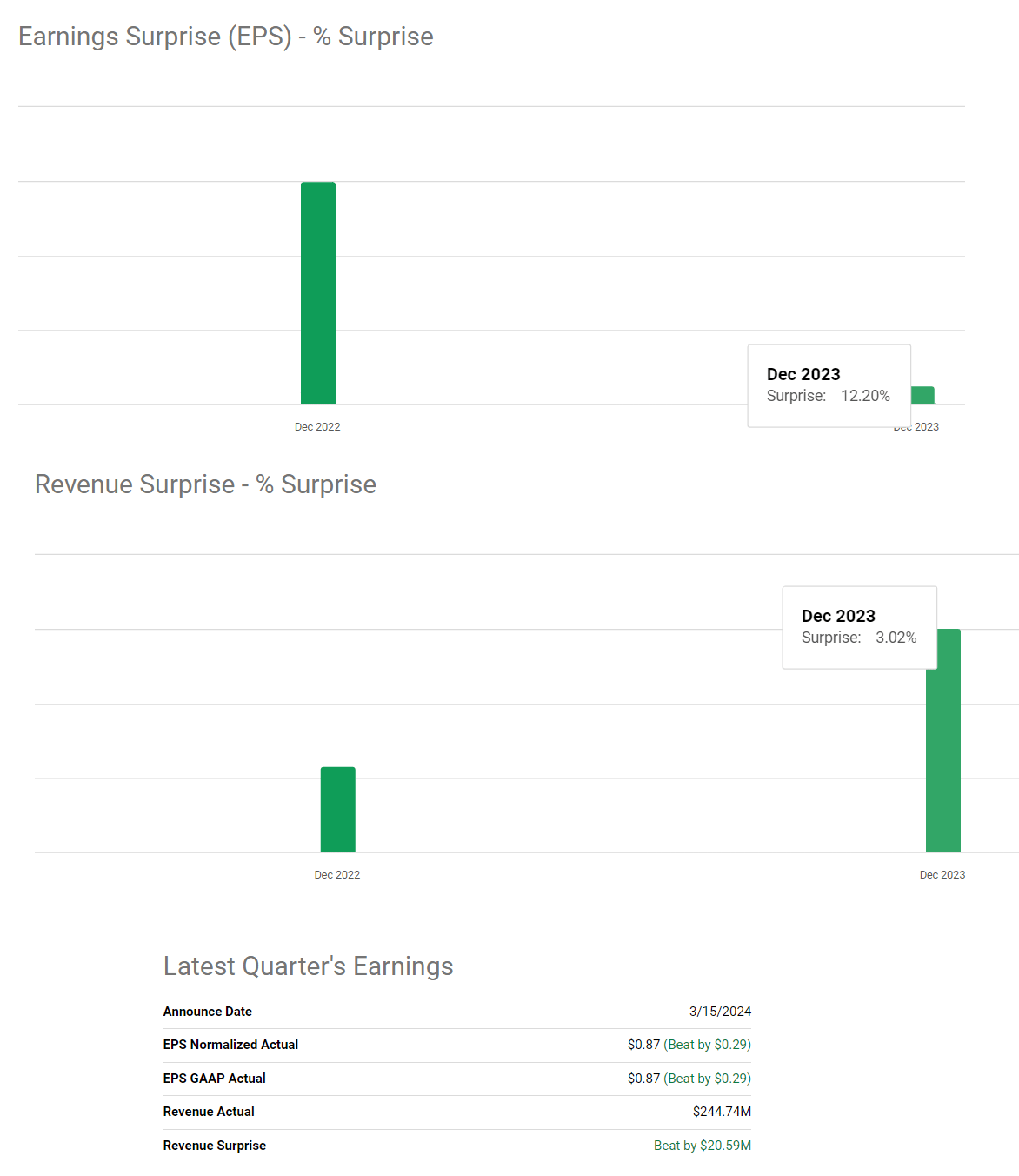

Based on the latest press release, in 2023 GigaCloud embarked on an impressive growth trajectory in its financial landscape with total revenue increasing by 43.6% YoY to $703.8 million and gross profit rising to $188.6 million — a staggering 127.0% YoY increase. The gross margin also expanded from 17.0% to 26.8% while the net income showed a similar picture of success, rising to $94.1 million (+292.1% YoY). The adjusted EBITDA rose to $118.3 million (+183.0% YoY). All these financial achievements helped GigaCloud to easily beat the consensus view regarding both revenue and EPS – for Q4 and for FY2023 as a whole:

Seeking Alpha data, author’s notes

Operationally, GigaCloud’s performance has also been remarkable with the GMV of the GigaCloud marketplace reaching $794.4 million (+53.3% YoY), thanks to “the growing popularity of the platform”. The influx of active third-party sellers, which increased by 45.5% to 815, and the uptick in active buyers (+20.5% YoY), underlined the platform’s growing reach and engagement, the management commented. Also notable is the increase in “spend per active buyer”, which rose by 27.2% to $158,569.

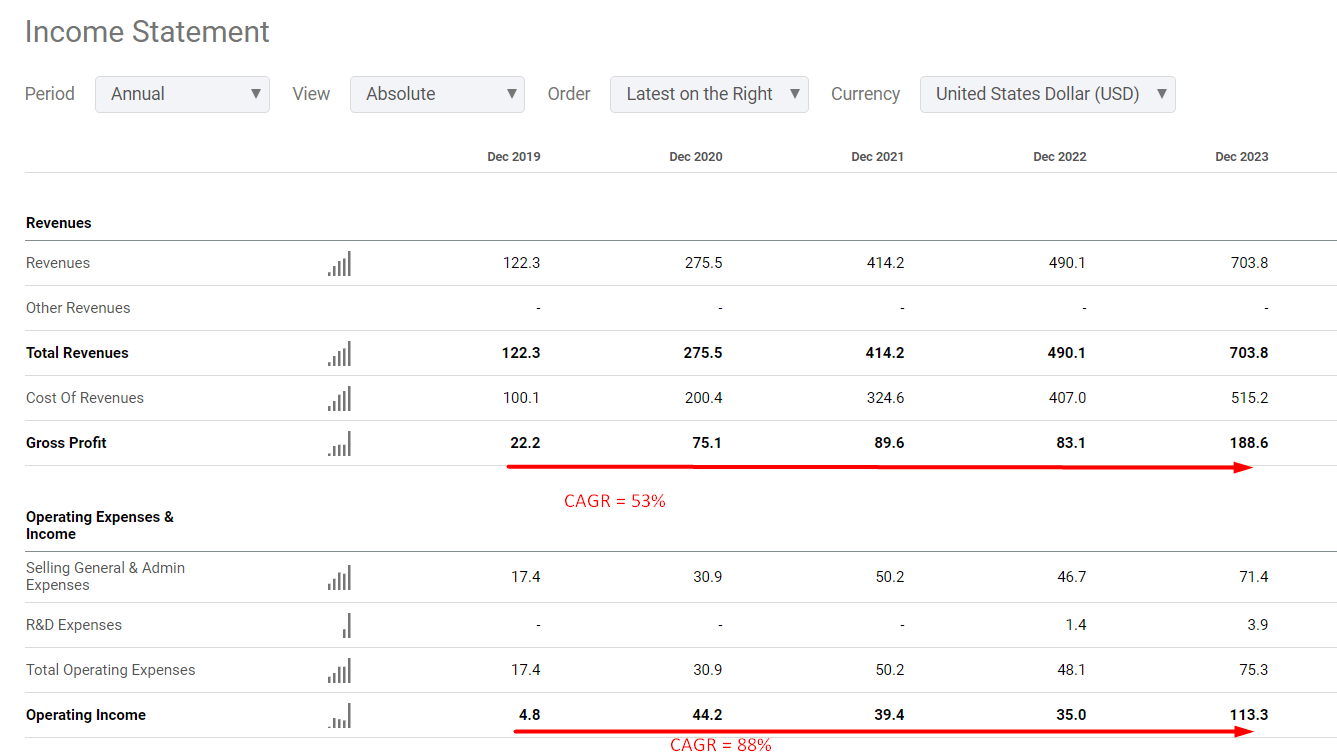

When examining the long-term financial trajectory of the company, we see that over the past 5 years, the revenue surged at a CAGR of 53% while the growth in EBIT has been even more remarkable – the CAGR here exceeds 88%. This level of growth, particularly in operating income, is notably high, even for a relatively small company like GCT.

Seeking Alpha, author’s notes

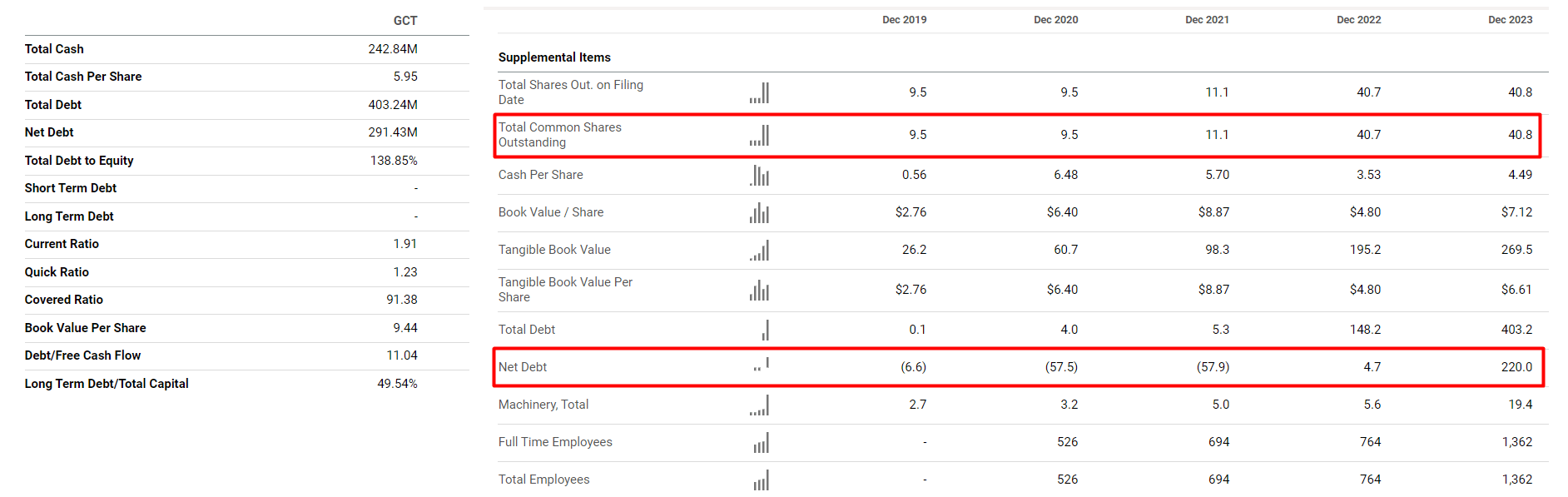

Recently, there’s been a notable increase in net debt on the company’s balance sheet, while the pace of share issuance has slowed down. In my opinion, this indicates a deliberate shift towards a more flexible capital structure, with a long-term focus on debt borrowing. This kind of capital structure shift should be favorable for shareholders, as it potentially reduces the WACC. So if the business growth rates moderate, the discount rate for future FCFs becomes less drastic compared to a scenario where the capital structure relies solely on equity capital.

In general, there appear to be no significant credit risks for GigaCloud, as indicated by a comfortable Times Interest Earned ratio of over 94 (calculated by the author).

Seeking Alpha, author’s notes

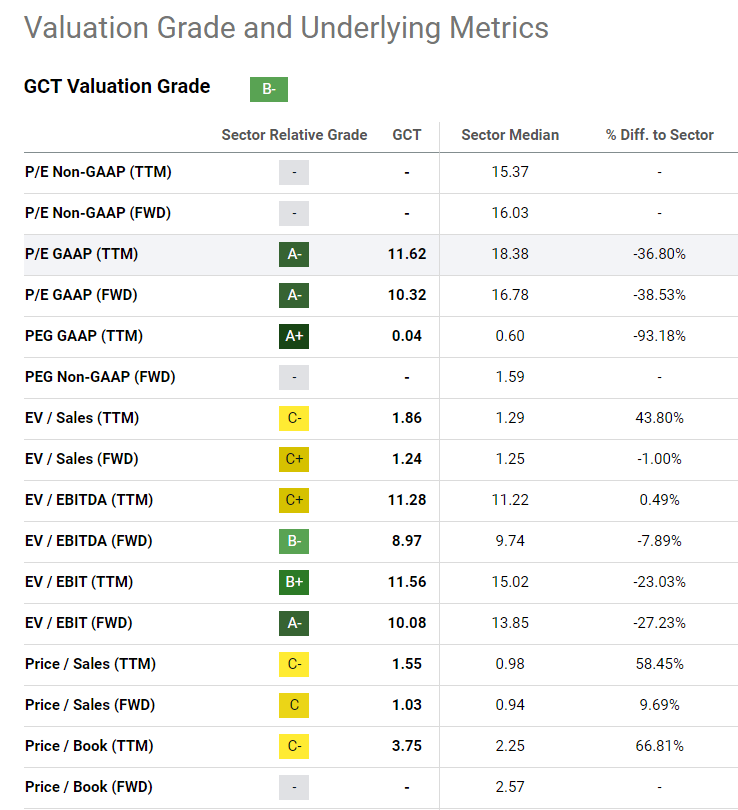

Given the robust financial strength outlined for GigaCloud, its current valuation appears strikingly cheap when assessed through individual valuation multiples such as PEG, P/E, or EV/EBITDA ratios:

GCT, Seeking Alpha

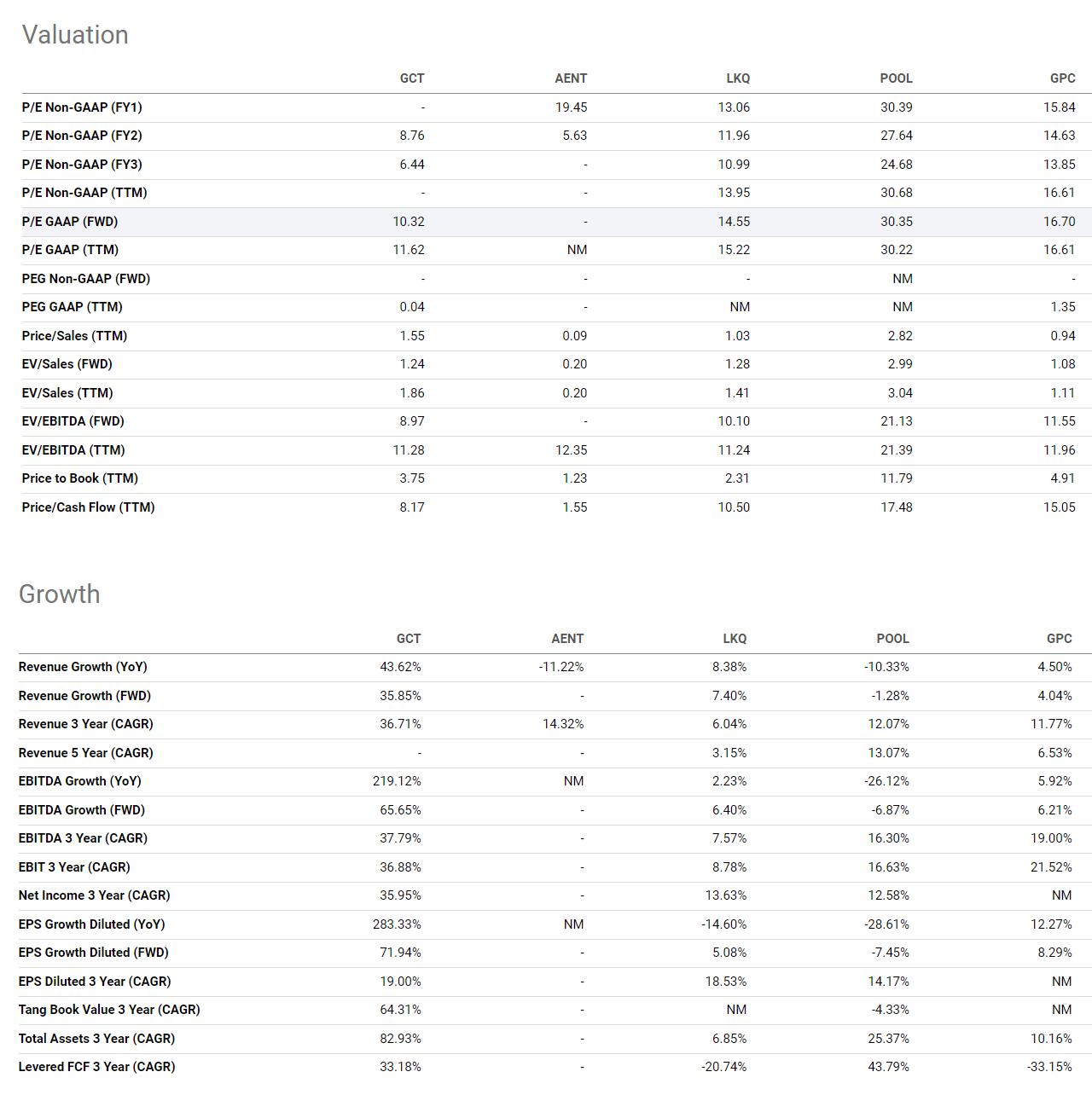

When comparing GigaCloud’s multiples with those of its industry peers (provided by Seeking Alpha Premium) it becomes clear that GigaCloud should receive a significantly higher valuation given that its growth rates are well above industry norms.

Seeking Alpha, GCT’s Peers

I think a price/earnings ratio of 15-20x seems fair – that would apply a “fair price” of $45.3 or an undervaluation of almost 50% to the last trading price.

However, here come some risks (that were included in my last article) that have led me to rate GCT as a “Hold” rather than a “Buy”.

The concerns about GCT stem from a report by Culper Research, a well-known short seller, which questioned the accuracy of GCT’s financial reports in September 2023 – particularly in relation to the company’s warehouse utilization and revenue. Culper suggested that GCT’s actual revenue may be lower than reported due to lower inventory utilization compared to major competitors. In addition, Culper questioned the credibility of GCT’s management and its claim about the use of AI, especially given that GCT’s previous reports did not list a software development division at the time AI was discussed.

While differences in load levels between GCT and competitors like Amazon (AMZN), FedEx (FDX), and UPS (UPS) could be attributed to variations in scale and business models, Culper found the lack of R&D spending concerning, especially considering the impressive range of AI-powered capabilities claimed by GCT. And I couldn’t help but agree with this then, in November 2023:

GCT works mainly in B2B and with certain types of products – then I really have questions about “AI”. How could the company achieve its current efficiency if it had no R&D spending at all last year?

The declared range of AI-powered capabilities looks pretty impressive and, in my opinion, is likely to entail high R&D costs that didn’t exist before, and at the time of Q2 FY2023, they amounted to only $0.5 million.

I do not presume to judge who is right, Culper Research or GCT, because I am not the SEC, but the very fact that there are some inconsistencies makes GCT a pretty risky investment in my opinion.

Source: From my previous article on GCT

Of course, GigaCloud representatives have dismissed Culper’s findings, claiming that “they are ” misleading and reflect a misunderstanding of the company’s business model.” Still, the inconsistencies cast doubt – especially when it comes to GCT’s lack of research and development in the past. I just can’t understand how this happened.

In addition, another risk factor has emerged – the delay in the release of the 10-K. As Marc Fagel (former SEC regional director for San Francisco) told Investor’s Business Daily, it’s hard to draw any conclusions, but it seems odd to report unaudited results when the delay in the release of the 10-K follows so soon after.

At the moment, the risk doesn’t seem too great, as the company eventually released its 10-K. We can’t know for sure: Maybe it’s because GigaCloud is still fairly new on the public scene and doesn’t have much experience in dealing with reporting to the SEC. But even so, it raises some questions. Any delay automatically adds to the risk, and we shouldn’t forget that as we move forward.

The Bottom Line

Despite the remarkable pace at which the company is expanding – both financially and operationally – and despite the attractively low valuation multiples, I’m inclined to maintain a neutral rating on GigaCloud stock today. The reality is that we can never be entirely sure of management’s integrity. Our assessment of this issue is based on various indicators – personally, I see too many warning signs surrounding the company. While many investors are betting on GCT’s growth potential, I cannot say with full confidence that the management is acting with complete transparency. If the data in the company’s official reports are indeed accurate, then perhaps the growth will materialize as expected. However, I’m not prepared to take that risk with my own money.

It’s a pass for me – again.

Thanks for reading!

Q2 2024 Earnings Call Transcript")